Kylo Ren really is a great example for how sci fi/fantasy writers should tailor their worlds to fit the times, so it could resonate with the actual audience reading them. There would be no point in making a Hitler villain anymore, because we’re not afraid of Hitler, we’re afraid of the 25-year-old malcontented white boy who fondles Hitler memorabilia while sulking in his room.

Somebody pointed out to me that the First Order aren’t coded as Nazis, they’re coded as neo-Nazis, which is worse, because these are people who looked at horrific historical atrocities with the benefit of hindsight and went, ‘Yes, that’s exactly what we should do again, but this time more’

People complaining that Starkiller Base is a rip-off of the Death Star and that Kylo Ren is a whiny emo fanboy don’t realize that this is exactly the point

*points upwards* THIS.

Tom Wright

Shared posts

deadcatwithaflamethrower: plain-flavoured-english: brainstatic: Kylo Ren really is a great example...

Tom WrightI think this makes an excellent point, but I somewhat wish we had a different "big bad" than an oversized Death Star.

killthebeatlesofficial: xenosagaepisodeone: lets all just be needlessly ominous for the rest of the...

lets all just be needlessly ominous for the rest of the year

if you live that long

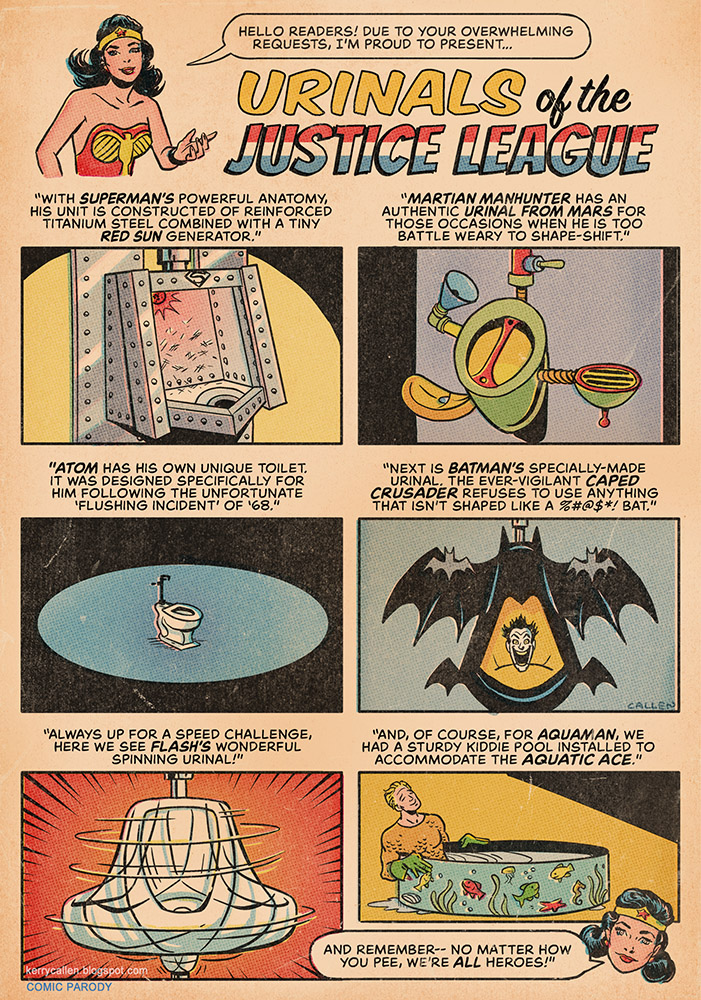

Urinals of the Justice League

Tom WrightThat last one is too real.

What Are the Best 20 Minutes of a Soccer Game?

Tom WrightMolly, Abinadi, what do you think about the 20 minutes he picked?

Ultimate players, what 20 minutes would you watch of an ultimate game?

Today I was really excited about a huge game in the English Premier League, Manchester United hosting Manchester City. They’re the top 2 teams in the EPL right now.

Today I was really excited about a huge game in the English Premier League, Manchester United hosting Manchester City. They’re the top 2 teams in the EPL right now.

The problem is, I had a busy day (some work, some play), and I didn’t have time to watch 90 minutes of soccer. So I set my TiVo to record it, and I sat down to watch it during lunch. My intention was to watch about 20 minutes of it.

But here’s the puzzle: Which 20 minutes are the best 20 minutes? I wanted to see the goals, but I also wanted to see some all-out gameplay. Soccer may not be interesting to everyone, but to a soccer player like me, watching nice passes, ball control, and defense is almost just as good as a quality goal.

I ended up choosing the following:

- Minutes 25-30: I figured this is when players are into the rhythm of the game and want to make something happen, but they’re not tired yet.

- Minutes 40-45: Teams often make a push right before halftime, especially if they’re behind or feel like they should have scored already.

- Minutes 65-70: This was pretty random–I wasn’t sure when to watch this part of the game.

- Minutes 85+: Even though players are tired, this can be a dramatic part of the game for one team. The downside is that a team in the lead is typically trying to slow down the game at this point, but I can fast forward through those parts.

What do you think? If you had 20 minutes to watch a 90-minute soccer game (or any sport you love), which 20 minutes would you choose?

#1652 – Happy

Tom WrightMaximumble I find is rarely good.

But when it is good, it's great.

My Greatest Fear #61: Forgetting to Refrigerate Leftovers

Tom WrightThis is truly horrifying. I share this deep-seated fear and empathize with his nightmare.

One of my favorite things are leftovers. Especially leftovers from a restaurant meal. When I order a sandwich or a burger at a restaurant, I almost always cut it in half and save one half for lunch the next day.

One of my favorite things are leftovers. Especially leftovers from a restaurant meal. When I order a sandwich or a burger at a restaurant, I almost always cut it in half and save one half for lunch the next day.

However, a few times in my life, I’ve somehow forgotten to put the food in the fridge at night, and I don’t realize it until the next morning. I’m haunted by these mistakes, as not only am I missing out on leftovers, but I’ve also wasted food. I don’t like to waste food.

For some reason this was on my mind last week, to the point that I actually had a nightmare about leaving a burger out on the counter overnight. I thought this was the result of going out to eat several times recently, but as you’ll see, it may have been a premonition.

Whenever I go home to Virginia, I bring a big cooler, and I buy an irresponsible amount of Gelati Celesti ice cream. It’s a small chain of stores that make the best ice cream in the world. I have access to great ice cream in St. Louis, but this is even better.

So on Saturday I stocked up on ice cream and loaded it into my sister’s freezer that afternoon. After an excellent evening that included a delicious meal and an escape room, I headed to bed in preparation for the long car ride back to St. Louis.

A few hours of restless sleep later, I woke up, brought my cooler over to the freezer…and found that someone had left the freezer door open all night.

My heart sank. This was bad. Fortunately, the saving grace was that the freezer was partially closed, so while the ice cream was soft, it was still mostly frozen. I packed it into the cooler, added some dry ice from the local grocery store, and hoped for the best.

This ice cream will last me months, so I won’t really know for a while if it has that crystalline texture ice cream gets when it melts and refreezes. But I’ll hope for the best.

Have you ever forgotten to put your leftovers in the fridge or freezer?

How to Play Well with Events

Tom WrightGreat article detailing exactly how I feel about Events.

By Derek Thompson (aldaryn)

For better or for worse, Star Realms is not the game it was upon release, and I don’t just mean that there are more ships and bases. The original core set was a fantastic deck-building game, but an inherent feature of its gameplay was a considerable slowness to the feedback loop. What I mean by that is, when you purchase a card, it usually takes at least a turn (if not several) for it to show up and do anything of use. The basic exception would be buying a card and then forcing a shuffle; the only other exceptions in the core set are Freighter, Central Office, and Blob Carrier, and those require some combination of ally effects and card draws to have immediate effect.

For better or for worse, Star Realms is not the game it was upon release, and I don’t just mean that there are more ships and bases. The original core set was a fantastic deck-building game, but an inherent feature of its gameplay was a considerable slowness to the feedback loop. What I mean by that is, when you purchase a card, it usually takes at least a turn (if not several) for it to show up and do anything of use. The basic exception would be buying a card and then forcing a shuffle; the only other exceptions in the core set are Freighter, Central Office, and Blob Carrier, and those require some combination of ally effects and card draws to have immediate effect.

Since then, we’ve had:

- Ships that can guarantee any size ship on top (Megahauler),

- Ships and bases that easily put things straight to play or in hand (Construction Hauler, Factory World, Moonwurm, Leviathan),

- Ships and bases that can be bought straight to the hand (Colony Seed Ship, Warning Beacon, etc.),

- Heroes that can be used immediately upon purchase with no prerequisites (and are inexpensive!),

- Gambits that can guarantee cards on top (Salvage Operation, Rapid Deployment),

- Events.

For whatever reason, despite all of these similar changes to the game – the shortening of the feedback loop – Events are by far considered the most offensive. My main assumption is that this is because some of them damage you and the rest offer a benefit to your opponent, and often a better one. My goal with this article is not to deduce why Events are the least popular expansion, but instead to teach you how to play well with them. You know, just in case.

The Five Principles of Event Play

The first, most basic step to dealing with Events is doing your best to avoid getting screwed by them. The next step is playing to them instead of just surviving them. Here are my five guiding principles for playing with Events.

Principle #1: They won’t be as surprising if you know what they do.

This may seem an obvious point, but I bet if you dislike Events – especially if you played with them a few times, hated it, and turned them off – you could not recite what the 12 cards do. In fact, it’s hard for me to remember them all sometimes (I tend to forget Galactic Summit). My conversations with many different Star Realms players have convinced me that the number one reason people dislike Events is because they feel like they happen “out of nowhere,” or “they didn’t see it coming.” While when they appear is random, what they do isn’t at all. I don’t need to write them down here as you can simply go to the Star Realms Card Gallery, but I do want to help you think more broadly about what the impact of an Event, in general, will be.

This may seem an obvious point, but I bet if you dislike Events – especially if you played with them a few times, hated it, and turned them off – you could not recite what the 12 cards do. In fact, it’s hard for me to remember them all sometimes (I tend to forget Galactic Summit). My conversations with many different Star Realms players have convinced me that the number one reason people dislike Events is because they feel like they happen “out of nowhere,” or “they didn’t see it coming.” While when they appear is random, what they do isn’t at all. I don’t need to write them down here as you can simply go to the Star Realms Card Gallery, but I do want to help you think more broadly about what the impact of an Event, in general, will be.

- 25% (3 out of 12) Events actually do damage to the players, while 1 out of 12 (8.3%) of the cards heal both players. These are the four 1-of cards; the Events you are far less likely to have. Of course, depending on the format, Supernova (8.3%) can be quite likely to flip another Event.

- Of the Big Eight, 4 of them (33% of the set) draw you cards immediately; while 6 of them (50%) are guaranteed draws for your opponent on their turn. (Those are the two big numbers, people.) Of course, the 2 Trade Missions (17%) do give you an immediate benefit.

- The usefulness of the 2 Comets (17%) depends entirely on whether you have a starter-heavy discard pile, but your opponent can always scrap from hand while you may not be able to.

Principle #2: The later in your turn it is, the worse Events are for you.

- This is not a hard-and-fast rule, but it’s a good rule of thumb. What good is a Quasar that draws you two Scouts when you’re out of trade? If you’d had at the start of the turn, you could have bought Command Ship instead of Frontier Station.

- Both Comets and Black Hole (25%) are awful for you when you have nothing to give them. For this reason, hold back two starters unless you absolutely need them for a purchase. NEVER play Vipers until you are done purchasing. NEVER HIT PLAY ALL. (Do as I say, not as I do.)

- If you are intending to buy more than one card this turn, buy the cheapest one first. Yes, there is a small chance that Supernova might consume the big card you wanted to buy, there’s one of those, and 6 Events that will help you buy stuff on this turn. If you’re going to have more trade this turn, when do you want to know that? When you have the most trade left to still work with.

- Likewise, think about Events when deciding to use Battle Pod / Battle Screecher / Swarmer / Ravager / etc. It’s often asked whether you should scrap a trade row card before buying or after. It entirely depends on whether there are good cards in the row for you, and whether you have trade, but now also depends on Events. If you can almost buy a big card, you might consider scrapping something else from the row at the beginning, in hopes of getting a boost from an Event. On the other hand, Events may give you a good reason to not use the ability at all (see next Principle).

- While I think you want Events to happen earlier in your turn, be careful at the end of a deck cycle. If you only have 0-2 cards left in your deck, Warp Jump / Quasar could flip your deck. So, if you are going to scrap from discard, do that before you buy or scrap from the trade row.

Principle #3: All Events (except Galactic Summit) accelerate the game state.

- In general, there are several things in Star Realms that show a sign of progress in the game. Decks with more purchases / fewer starters and lower life totals are the two big ones. After all, those are the two big goals: have an awesome deck and kill your opponent. All Events (okay, except Galactic Summit) push the game faster towards its end, by allowing for bigger purchases, damaging players, scrapping cards out, causing another deck cycle, and so on. Whether you want this to happen is another matter.

- Who’s the Beatdown? One of the most important Magic: the Gathering articles ever written was “Who’s the Beatdown?” by Mike Flores, almost 20 years ago. The main lesson applies even more to Star Realms, which is this: which deck are you? Are you the offensive player or the defensive player? Even in mirror matches, at any point time, one person is ahead in the aggressive role and one player isn’t. The same deck should be played differently depending on which role you are currently in. Your purchases should reflect this, and so should your interactions with Events. If you are the aggressive player, trying to kill your opponent as fast as possible, you want more Events to happen. They keep your opponent from having more time to take advantage of their slower moves, such as scrapping and base-buying. If you are the defensive player, you want fewer Events to happen, so be careful about your scrapping from the row and your timing of purchases. In particular, the more scrapped out you are, the less useful Events are for you.

- Gambits also accelerate the game. Keep this in mind when playing with both.

- Bombs happen earlier in the game and can be more game-defining. Players can get a turn 1 Ark to the top of the deck! This is especially true when playing with both Events and Gambits. Oftentimes, a race for a 7 or 8 cost card in a traditional game can be worthless, spending forever buying Explorers when your opponent Pods it away and beats you down in the meantime. With Events, it doesn’t take much to get 8 trade. This makes trade row control all the more important. Many of the times I’ve managed to beat the Ark, it was by using aggressive trade row scrapping to trigger Events and accelerate my play while not accelerating my opponent’s, who had very few cards to draw with Quasar / Warp Jump / Trade Mission.

Principle #4: Know your tips and tricks.

These don’t fall into any of my other principles, but are still important points to make about Events.

These don’t fall into any of my other principles, but are still important points to make about Events.

- In general, your opponent gets more out of an Event than you, since they get it at the start of their turn. The big exception to this is your last, winning, turn. If you get the kill shot, then they never get the benefit of those last Events. This cannot be understated. If you’re on death’s door but think you could win with just a little help, it is time to dig, dig, dig! (The other exception is Events that show up in the initial trade row, on the start of turn 1. However, since your opponent has a 5-card hand, they still probably get more out of it, though you get first crack at the trade row.)

- Certain cards have a very different valuation with Events. The big ones, of course, are trade row scrappers, Battle Screecher in particular. The other broad valuation change is bombs versus weak and midrange cards. It’s so much easier to get a bomb that they are much more viable, and weaker cards might be less worth the clutter in your deck or the danger in flipping the trade row. The Ark is even more of a game-warper than usual, because it’s accessible so much earlier. However, once a player has the Ark, subsequent Events work against the player with The Ark, by minimizing the advantage of a seriously scrapped deck.

- If you only have 0-2 cards in deck+discard, Warp Jump will not give you anything.

- Supernova can kill someone if it happens before you apply your damage. If you apply your damage and knock them to 5, and then Supernova happens, they will only go down to 1. This is always what happens with Black Hole and Bombardment, because damage is not applied until the opponent makes the choice on their turn, even if there is no choice to make. (And this is only for digital; Events can kill players and even cause draws in the paper game.)

- While it’s hard to see the psychology of a match in a digital game versus paper, it’s definitely there. Events can often put your opponent on tilt – or put you on tilt. Being prepared for them – even playing them to your advantage – makes a huge difference.

Principle #5: Practice.

I know people are very proud and protective of their win percentages online, but I’ve started to convince myself that that’s rubbish. The way you improve at any game is to try new things, lose, and try again. To play well with Events, you need to practice. In particular, you need to think of Events as part of a broader class of “mid-turn shenanigans” (see initial paragraphs) that can change things up. I also believe Battle Screecher and The Ark are important parts of learning to play with Events. I recommend playing W1HE with one or both Gambit sets attached – basically only sets that mess with you in this way. The games will feel very different, but you’ll quickly learn how to use caution after getting burned several times. Once you’ve learned to take those precautions, you’ll still use them in Bigdeck, when Events only trigger a fraction of the time. If you are that worried about your win percentage, then practice this against the Hard AI.

Summary

When Events first came out, I was pretty frustrated with them, to be honest. But over time I’ve not only enjoyed playing with them, I’ve taken them to be a legitimate advantage. Hopefully these pointers can give you the same edge. If you take nothing else away, just remember this: before moving a card off the trade row, ask yourself “What possible Events could flip, and am I prepared for them?”

How to Cut Costs with Tiny Living

Tom WrightWhat do you think? Is it viable to live in a tiny house?

Millions or perhaps billions of people live in tiny houses all over the world, so I've seen it work.

It's an attractive idea. Molly and I both work at home and we have two kids under three years old... so that may present a difficulty.

Tiny homes aren’t just a fad anymore — what started as a way to lower mortgage payments and utility costs following the Great Recession has developed into a worldwide movement. And Google searches for “Tiny House for Sale” have grown a whopping 900%.

If you’re looking to purchase or build a tiny house of your own, there are a few decisions you’ll need to make: Where do you want to put your tiny house, and do you want to rent the land or purchase it outright? Are you looking to build your house on a foundation, or do you want to put it on wheels and travel from coast to coast with your home in tow?

When compared to a traditional or big house, tiny houses could save homeowners a lot of money. But exactly how much you’ll save comes down to the type of living situation you want. We’ve taken a critical look at the choices that aspiring tiny homeowners often have to make, and how much each option costs when compared to living in a traditional home on a one-month to five-year scale.

Big house vs. tiny house

Here’s a hypothetical:

Kate wants to build a tiny house, while Tyler wants a traditional home. They decide to shop around, find the best options, and see how they compare:

- Both want their house built by professionals

- Both want to use existing utility systems (power, water, sewage, etc.)

- Tyler wants to take out a mortgage, while Kate wants to take out a personal loan.

Here’s how their costs stack up:

Property Prices

It doesn’t matter if you’re looking to build or buy — the land underneath your structure will most likely increase in value over time, and it’s one of the best investments you can make. So even before construction begins, you have to decide where you want to live, and what you’re willing to spend on ownership of your land.

According to a study of land prices by state conducted by the Lincoln Institute of Land Policy, the average land value across all 50 states (as of first quarter 2016) comes to approximately $106,893. And the closer you are to a city, the more likely you are to see that number increase at an exponential rate.

Additionally, between 1978 and 2016, the American house grew 950 square feet, while individual lots have shrunk to 0.19 acres. That’s not a lot of property.

There are a number of factors that go into determining the value of a piece of land: Proximity to major urban areas, the potential for economic growth, and the market value of the land itself. Because this value varies widely from area to area, whether rural or urban, it’s difficult to estimate the average cost of land.

Generally, prospective homeowners face two options when it comes to property pricing: Lease a plot of land, or buy the land outright. Tiny homeowners have a third option: Turn their home into an RV or mobile home, and use their tiny house to travel across the nation.

Whichever you decide, be sure to look up your state and local government’s zoning laws and building codes before you shop around.

Leasing or Buying Land

It’s not uncommon for tiny house owners to live on plots of land owned by friends and family, and pay rent directly to them.

Aspirant homeowners can also seek out properties with an existing accessory dwelling unit (ADU) agreement, which enables homeowners to build a second, smaller dwelling on their property. ADUs often come with system development charges (SDC), which are additional fees that vary from city to city.

But if you prefer more privacy, or you can’t find anyone willing to share their property, you might have to rent a plot of land.

But again, before you do, make sure that local zoning allows the construction of a home on your intended plot. For many locations, the minimum house size is 900 feet.

Websites like Zillow, Realtor.com, or LoopNet can help you find vacant lots available for both sale and lease. Another option is to utilize classified sites, like Craigslist or private social networking services like Nextdoor, to publish inquiries or check for rentals.

Parking a Mobile Tiny House

If you’re looking to bypass land costs altogether, plenty of tiny house owners place their homes on wheels instead of a foundation and make their home mobile.

Mobile tiny house owners face a different set of challenges than their stationary peers. For example, mobile home owners that prefer constant travel are still required to establish a permanent address — which they can do via RV friendly states or mail forwarding services.

It’s easy and cheap to find somewhere to park your tiny home on a temporary basis.There are plenty of RV camps across the nation, and on average rent is about $20 per night. But many states limit the maximum amount of time mobile homeowners can stay in one place.

However, many RV camps throughout the U.S. and Canada are showing growing acceptance of long-term, mobile home parking, allowing for longer stays at reasonable costs.

Purchase & Building Costs

The U.S. Census publishes a monthly update of average sales prices of new (traditional) homes sold within the United States. In September 2017, the Census found that the average sales price of a new home was $385,200 — that’s up almost $20,000 from just one year ago.

Building your own traditional house could be an even costlier venture, with average building costs coming in at $286,909, and that’s before the price of land.

However, the average cost to build a tiny home is only $23,000, before labor costs and not counting the price of land, as we’ve already covered. And the median cost for a professionally pre-built tiny home, complete with amenities comes in around $59,884. That’s an impressive savings, to put it lightly.

So once you’ve figured out where you’re going to live, the next decision you’ll have to make is whether to hire professional builders or do it yourself.

Hiring professional builders

There’s a number of professional construction companies that specialize in tiny houses, including 84 Lumber, New Frontier Tiny Homes, and Tiny Home Builders, while local builders can be found via a quick Google search.

Each organization offers a wide variety of floor plans and models, as well as itemized lists of materials and basic home shells, should you decide to go the DIY-route.

Buying a pre-built tiny house means you’re getting a complete home with all appliances pre-installed (which includes microwave, refrigerator, etc.). You’re also able to customize your home just as if you were building it yourself, designing in tandem with the builders.

Though this is the most expensive option available (again, median costs hover just under $60,000), you’ll know exactly how much you’re paying, the cost isn’t as volatile, and you’re guaranteed a professionally built home.

Building your own home

The do-it-yourself spirit is very strong among tiny house advocates: There’s no need to pay for labor costs, and with the right materials, you can reduce building costs to $20,000, on average.

If you do choose to build your own tiny home, and you’re able to build it yourself or get family and friends to provide (volunteer) labor, the only variable in cost will be the quality of materials you choose. The cost of materials varies from area to area, but for an outline of the essentials, check out this list from Tiny House, Giant Journey.

Many tiny home experts encourage aspiring builders to use reclaimed or salvaged building materials — such as reclaimed lumber, wood, or metal for your house’s exterior. Reclaimed materials are often cheaper and sturdier than if you purchased new. Habitat for Humanity ReStores can be a great source for quality recycled building materials, appliances, and more.

Building your own tiny house creates an opportunity for total customization of your home — so if you feel this is the best option for you, be sure to design and plan ahead.

The biggest downside of doing it yourself is that you’ll also have to set up your own utilities. That includes electrical wiring, waste disposal, and more.

If you’re more interested in the personal touches and would like to just build the facade of your house, many tiny house builders offer pre-built kits or shells for sale. Kits give builders everything they need to assemble their house, whereas shells deliver a completed foundation. With a shell, all you have to do is provide the finishing and decorating. Kits can cost anywhere from $2,000 to $35,000, while shells can range from $5,000 to $60,000.

Loans

There’s no way around it: When it comes to borrowing money for traditional housing, you need a mortgage.

With the average price of a house at $385,200 as reported by the U.S. Census and the current mortgage APR of 4.061% as reported by Wells Fargo, the average American owes a total mortgage of $666,926. That’s almost an additional $300,000 in interest.

It’s no wonder that the comparatively miniscule pricing of tiny houses — again, on average anywhere from $20,000 to $60,000 depending on labor costs — is so appealing.

Still, $60,000 is a lot of money. And though you may be planning to build your own tiny home, you may still have to pay for a plot of land. Even if you plan on turning your tiny home into a mobile home, you’ll still have to pay for upkeep and licensing fees.

Most banks consider tiny homes too small to qualify for a traditional mortgage, but if you need money to make your tiny home dreams come true, there are other options: Personal loans or RV loans.

Personal Loans

A personal loan is money borrowed from a bank, credit union, or independent lender for a non-specific purpose. This means personal loans can be used to finance a house, pay off debt, start a business, etc.

Like mortgages, personal loans offer fixed interest rates and flexible payment plans. Most personal loans are unsecured, meaning that unlike a mortgage, they don’t require collateral. And some may come at a lower rate.

LightStream, an offshoot of SunTrust bank, is one of the most highly regarded lenders for funding tiny house construction. Not only is it one of our top picks, but it’s recommended by tiny house builders 84 Lumber and Tiny Heirloom.

If you’ve financed your home, but still need money for land, you may be able to take out a “raw land loan.” Because it’s easier for borrowers to walk away from land without property, raw land loans require higher credit scores, down payments, and interest rates.

RV Loans

If you’ve opted to put your tiny home on wheels instead of a foundation, you might qualify for an RV loan. RV loans are personal finance loans available for the different classes of RVs and motorhomes.

RV loans are often unsecured and come with the same general interest rate as a personal loan. In addition to their personal loans, LightStream also offers an unsecured RV loan that covers anywhere from $5,000 to $10,000, as well as a secured motorhome loan for anywhere from $54,601 to $1,500,000.

RV loans tend to come with higher interest rates, averaging around 4-7%, as well as a 20% downpayment. In addition, RV loans aren’t designed for primary residencies — so you’ll need a permanent address to apply.

Utilities

Like mortgages, utilities (such as water, power, and waste) are one of the main areas where tiny homeowners can save when compared with traditional homeowners.

Electric costs average approximately 13 cents per kilowatt-hour, or $118 per month, and average water rates go for $68.14 per month. Often, traditional homes don’t have a say in utility prices. But, if you’re an aspiring tiny homeowner, you have two options when it comes to utilities: Plug into an existing grid, or become fully self-sustaining.

Often, location is the primary factor: The more rural the homestead, the more difficult it is to hook into existing municipal systems. But, even urban tiny home owners may choose to go the self-sustaining route for ecological or economic reasons. There are advantages and drawbacks to both.

Using an existing grid

If you choose to plug into existing power and water grids, you will have monthly utility costs — but the good news is utility bills will likely cost under or around $20 per month.

Before you build, be sure that your chosen property has traditional hookups, allowing homeowners to splice into the network with ease. If you’ve opted to stay at an RV park or tiny home neighborhood, you should be able to reach those hookups without any issues.

However, if you’ve chosen to live in a more rural area, there’s a chance those hookups may not even be on your property. You may have to run heavy-duty electrical cords for miles, which can be both dangerous and illegal.

If you do choose to hook into the grid, call your local power company beforehand. It’s the best way to find information on power requirements, costs, and where to hook in. Often electrical companies will charge a flat fee for a certain distance, (ex. 5 miles), and then add charges for anything over that distance.

You may also have access to electricity via electrical co-ops, which are smaller, member-owned power companies. Once you’re hooked in, you become a member and part-owner. However, electrical costs remain on par with traditional housing.

When it comes to bringing in water and removing waste from your home, the grid is your simplest option. If you’re in an urban area, you can splice directly into existing water and sewage systems.

If you’re in a more rural area, be sure to research your local water district for more information on where to hook up into the water network. Again, utility costs may be comparable to those of a traditional house.

Becoming self-sustaining

One of the biggest benefits of owning a tiny home is the ability to generate your own power, water, and waste disposal, living entirely off the grid. Not only does this save almost entirely on monthly utility costs, but it’s one of the most ecologically-friendly living options available today.

There’s another advantage: Choosing to set up self-sustaining utilities is possible no matter where you decide to call home. It’s equally applicable to both urban and rural living situations.

There are a few general disadvantages as well. Upfront costs are likely to be fairly high, and although you won’t be paying a monthly bill, these systems do require monthly maintenance.

Solar power is by far the most popular choice for bringing off-grid power to tiny houses. But there’s more to solar power than just the panels. You’ll also need batteries, a battery bank, and a DC-AC converter. (Plus, a backup generator might be helpful, just in case the clouds stick around.)

The price of solar panels can run anywhere from $340 to $20,000, depending on the size and complexity of the system you choose.

When it comes to bringing water into your tiny house, rainwater collection is a legitimate option. However, storage comes at a considerable cost, and it may not rain consistently enough to meet all of your water-based needs.

Another option is to install a tank-and-pump system in your tiny home, in order to collect, circulate, and pressurize water. The system is relatively inexpensive, water tanks can be found for under $100, and hoses for under $50. Installation and heating may cost a pretty penny, but so long as you refill your tank consistently, you’ll never have to pay another water bill.

There are two different types of wastewater: Greywater, which is water drained from sinks and showers, and blackwater, which is another word for sewage.

Greywater can be collected via a portable greywater tank and dumped whenever your house is connected to a utilities grid. If you prefer to stay off-grid, greywater can also be filtered and reused to water gardens or lawns.

Blackwater, on the other hand, must either be disposed of at pump stations or via a special composting toilet. This is one of the most cost-efficient aspects of a tiny home — simply sprinkle sawdust over your waste, and add it to a compost pile.

There are also composting toilets that will do the work for you but can cost anywhere from $900 to over $2,000.

Conclusion

Tiny homes are one of the most cost-effective living situations available to homeowners today. Owners can choose to live on-grid and reduce their mortgage and other daily expenses, or they can go the self-sustaining route, becoming an eco-warrior while cutting their living expenses to a fraction of the original cost.

Whichever you choose, living in a tiny home is not impossible. There may be higher upfront costs when compared to a traditional house, but within a few months those costs will begin to even out. And in just a few year’s time, you’ll be amazed by how much you can save.

The post How to Cut Costs with Tiny Living appeared first on The Simple Dollar.

Fowl Play.

Tom WrightI am so hipster about hating holidays that this isn't even the type of stuff that bothers me. I've transcended this tripe.

Photo

Tom WrightThat pretty much sums up Thanksgiving, the most thankful time of the year.

When Your Shitty Health Insurance Doubles in Price

Tom WrightIf the topic is boring to you, I suggest skipping to the end where there are italicized bullet points about our current health insurance in the US.

I especially like bullet #4: If I can, I always see the nurse instead of the doctor. I find doctors to be rushed and busy, and I don't typically need their expertise when a nurse can just get me fixed up on a less-nuts schedule.

Also, bullet #3 makes so much sense to me. It feels like military marching, where we do it because we do it, that's why. Forcing residents to work so many hours and being sleep deprived is a stupid practice. Do I want my doctor to have learned his/her medical knowledge while they were sleep deprived? No, I prefer that my doctor was lucid and awake during all their acquisition of knowledge.

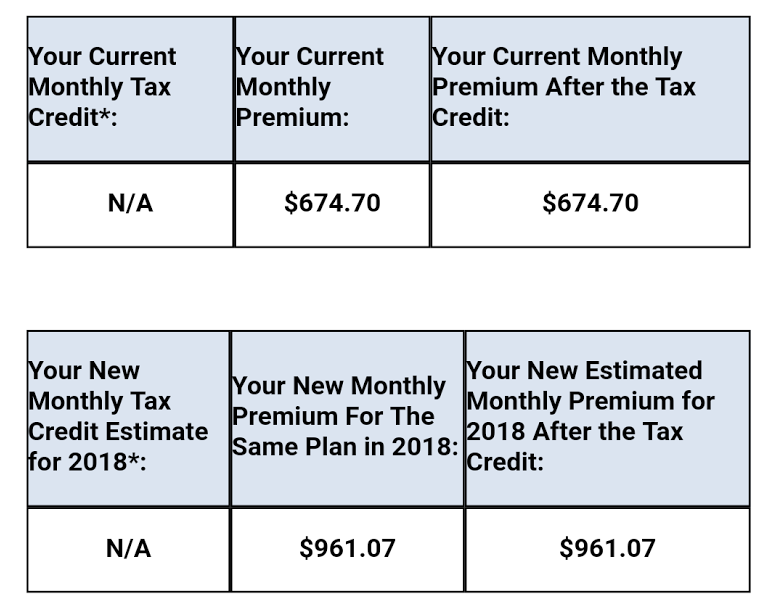

Well, despite Mr. Money Mustache’s outrageous optimism, I think we all saw this coming. I opened up my premium renewal email from Kaiser and saw this:

Well, despite Mr. Money Mustache’s outrageous optimism, I think we all saw this coming. I opened up my premium renewal email from Kaiser and saw this:

Figure 1: My new insane medical insurance premiums for the minimum available “Bronze” program, with a $6500 deductible.

My family’s monthly health insurance premium, which had already more than doubled in the last few years to $674 per month, was going up a further 44% for the coming year. For no good reason, other than perhaps the the current government’s attempts to kill off the Affordable Care Act. (By cutting various parts of the structure, the insurance market becomes less stable and predictable, and thus more expensive).

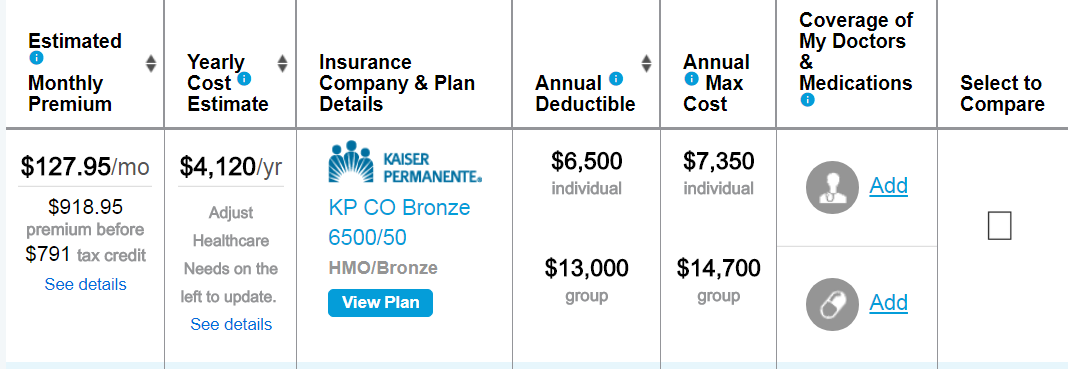

Now, before we go any further, I have to note that this is a situation that only affects high income earners. If we were really retired on a $30,000 passive income as we were for some of the decade before this blog started making significant money, our family’s monthly cost would be more like $128, due to tax credits and the Children’s Health Plus plan.:

Figure 2: Net insurance cost for a $30k per year family of three.

But in my email, I just saw the thousand bucks. And if you know how I feel about rules, unnecessary costs, and insurance in general, you can probably guess what my initial gut reaction was:

But, since I’m not sixteen years old anymore, I was eventually able to get past this first stage of the analysis and think about an actual course of action.

After all, all the power and freedom in the world is of no use at all, if you choose to wallow in your anger rather than taking steps to create the life you want. So I thought about why I was so angry. It boiled down to this:

The premiums are not an accurate representation of my risk.

The value of medical insurance is pretty easy to estimate: the National Institute of Health calculates that the average person consumes about $449,000* in health care spending over an 80-year lifetime, or $5600 per year. This is less than my plan’s deductible alone, which eliminates the value of insurance right off the bat. My plan really only covers catastrophically expensive events, which means it is unlikely that I will ever use it.

Plus, most medical spending is loaded towards the last decades of life, where the Medicare program already picks up the bulk of the costs. And, we are healthier than average – aside from one baby delivery about twelve years ago, none of us have ever actually benefited from health insurance in over nineteen years in the country.

When you add up these factors, it is obvious that the insurance is a bad deal. When presented with overpriced insurance, I always just choose not to buy it, which is also called “self-insuring”. But whenever I talk about self-insuring for medical expenses, everyone asks the same question:

“But what if you do get hit by a falling piano and have to spend months in the Intensive Care Unit?”

The answer is that I guess I’d receive some large medical bills!

I’m not denying that an expensive treatment absolutely can never happen to me. I’m just putting an estimate and a limit on how much I am willing to pay for insurance on it.

Remember, health insurance is not really health insurance. It’s just “large medical bill insurance” – a shaky precaution against having to pay for expensive procedures, so you can keep your investments instead of using them to pay the bills, perhaps eventually becoming poor enough that you are covered by public health insurance (Medicaid). A better name for it might be wealth insurance.

We have been trained to think that going without medical bill insurance is very risky. But that’s just because the subject appears frequently in the news. If it weren’t such a hot topic these days, the average person without a chronic illness would rarely think about it.

After all, by comparison, what precautions have you taken against being hit by a meteorite? There could be one streaking towards you right now. It could kill you, or your children, or it could leave you with a lifetime of chronic care costs. Are you telling me you don’t have separate meteor insurance? Why not?

In 2013 a 60-foot chunk of rock came from space and hit Russia with the force of 30 Hiroshimas. The human race escaped with just 1500 injuries, but only because the rock came in at a shallow angle and landed in a very remote area.

If space rocks are too far-fetched, how about motor vehicles? If you choose to drive a car, you are willingly throwing yourself into a far riskier situation than simply self-insuring for medical bills. Even more dangerous, statistically: being inactive and/overweight, a boat in which over 66% of us sail every day.

The point is that while huge, uncovered medical bills are inconvenient, they are rare. Therefore, my willingness to pay for insurance against them must have a limit. I’d definitely pay $50 per month for it, but should I be willing to pay $1000?

What about $2000? $4000? $12,000 or $1 million per month? I think that everyone would hit their “Fuck That” point somewhere in there.

And remember, this problem of expensive medical procedures is unique to the US. You can take your dollars almost anywhere else in the world and pay out-of-pocket to get the same (or better) quality care for a fraction of the cost. At some point, a rational person has to be willing to stop overpaying for this inefficient system.

After doing the math, I decided that my limit is definitely less than $1000, which means I should at least consider other options. So I looked into some of them:

- Full Self Insurance

- 2.9 Months per year of Self Insurance (to avoid IRS penalty)

- Medical Tourism

- joining a “Healthshare Ministry” like Libertyshare

- expat insurance like Cigna

- Artificial poverty (reducing my income to a level where we’d qualify for subsidies)

Self Insuring is the easiest choice: you just don’t renew your insurance and start banking that sweet surplus right away. There is a tax penalty for that: $695 per adult, $347 per child, or 2.5 percent of your adjusted gross income – whichever is greater. Thus, a family with $100,000 of income would pay a $2500 fee. With my new premium at $11,500 per year, the penalty would still be cheaper all the way up to $461,000 in income. Plus, there are a surprising number of qualifying exemptions, including a death in the family within the last three years, a category which unfortunately includes me.

A 90 Day Insurance Vacation is the lightweight version of self-insurance. The penalty only applies if you were uninsured for three months or more. So if you start your insurance during the enrolment period but then cancel it on, say, October 2nd, you cut your premiums by about 25% in exchange for the reduced risk protection. Just be sure to postpone your Wingsuit Jumping vacation until at least the new year.

Medical Tourism is an important thing that every US resident should be aware of. After all, we live in the country with the most overpriced medical procedures in the world – why should we insist on doing 100% of our shopping here? This would be like insisting you buy only US-produced goods and services: no electronics, no shoes, no Amazon and no blueberries in winter. We should all read a book or two on the subject to understand just how easy it is, to free ourselves from the US-centric assumption that doctors are shockingly expensive.

There’s a lightweight version of medical tourism too: simply comparing insurance pricing from one state and city to another. From a quick search I see that Colorado is one of the more expensive states for health insurance, with New York being the worst, and the best three being California, Utah and New Mexico. As with everything, it’s good to shop around when choosing where to live, and regularly challenge yourself by asking, “Is this where I’d settle down if starting from scratch?”

Health Sharing Ministries like Liberty HealthShare looked like the most promising loophole. Due to the strong influence of organized religion in the US, if you can join one of these, you are exempt from the tax penalty. The downside is the same as the upside: these ministries are exempt from ACA rules, which means they can drop you for having a pre-existing condition. And they also want you to affirm their value system, which can range from agreeable stuff like “taking care of your health” to excluding coverage for things that violate religious taboos like abortion or attempted suicide.

Expat Insurance sounded promising when I first heard about it from some fellow Canadian early retirees who write the blog Millennial Revolution. Companies like Cigna will cover you for worldwide medical costs for a fraction of what we pay here in the US. But the hitch is it only applies if you are truly on the road and don’t actually reside here. So it’s not an option for now. But in the long run when I retire to an oceanfront compound (or commune?) in Costa Rica, yes.

Reduced Income is the last and least feasible option on the list for me right now, but it’s genuine and not even artificial in the case of the typical early retiree.

Suppose you are retired with, say, a mortgage-free home and $800,000 in index funds, and living on a plentiful $30,000 per year. Your income tax return will show only about $18,000 in dividends, some of them even tax-exempt. On top of that, you’ll sell just a few shares and pay taxes only on the capital gains. This taxable income in the mid-20s will keep you in a very low tax and health insurance bracket.

So What Path Did the Mustache Family Take?

I brought all this stuff up to Mrs. MM – the other, less morally-outraged, leader of our household. Our conversation brought up a few things:

- Although a $12k insurance bill is insane, we would not even notice a $12,000 difference in income taxes if the brackets were to change. We currently have a high income, but this has not caused us to increase our family spending at all. This is because of the magic of living below your means: once you have enough money, the surplus is just that: a big, fat, awesome bonus. Since I want this enormous surplus to go back to society over my lifetime, why should I be upset about some of it paying for other peoples’ health insurance right now?

- But, I countered, this doesn’t apply to everyone. The typical MMM reader earns enough money to be hit by these higher premiums, and many are raising families and running small businesses, thus purchasing health insurance on the open market. At the same time, they are trying to save as much money as possible to reach financial independence while they are still young enough to enjoy it. Burning $12,000 per year on mostly-useless insurance can wipe out 25% or more of the amount you could otherwise save for retirement.

- Given this, the Healthshare ministry was one of the better compromises. However, she felt that pretending to agree with a religion (especially if it’s one that actively oppose some things we value like same-sex couple equality and women’s reproductive rights) wasn’t worth it for us.

- In my own hypothetical pre-retirement situation (a self-employed couple making $200,000) I would probably go for full self-insurance, simply paying the tax penalty whenever necessary and using medical tourism for any expensive procedures.

- But also remember that if you’re a high-income business owner, your business can pay for your health insurance with pre-tax money. This cuts your net cost after taxes by 30-40%, making it a subsidized program after all.

So in the end, we’re just letting the policy auto-renew for now, using that last bullet point as a consolation prize. And these premiums will probably remain outrageous, unless we fix the underlying problem in the US: it’s not the insurance, it’s how much money we waste on medical care. If the Medical system could grow a Money Mustache**, I am certain we could cut our costs down by at least 75%, just as the average consumer can cut their costs by a similar portion just by learning to life a joyful and efficient life.

Further Research:

After this article came out, a reader told me about the site “Health Care Bluebook“, which allows consumers to look up typical costs of various medical procedures. Many are less expensive than I had assumed.

Footnotes:

* I adjusted the NIH paper’s 2000 numbers to 2017 dollars.

** Ideas for making US healthcare less expensive – please critique and add your own in the comments!

- Eliminate the 75% of healthcare spending we currently waste on self-imposed lifestyle diseases: eliminate subsidized urban car infrastructure in favor of muscle-powered transportation. Treat soda and products with added sugar in the same way we currently treat liquor. Treat health and fitness (rather than medical treatment) like a human right, instead of a vanity accessory just for rich mountain-dwellers and celebrities.

- Make health care purchasing look more like Wal-Mart and Amazon, and less like the DMV. Every standard procedure needs to be listed on a menu with a price, and those need to be on the front door so they are subject to competition. By huge national or even international companies and co-ops.

- Drastically increase the supply of doctors, and make the job more enjoyable: Cut mandatory work hours for residents from 80 to 40 per week. Modernize the medical school curriculum to eliminate pointless memorization, reflect current technology and reduce the cost of the degree. Open the borders to qualified doctors from other countries. Allow telemedicine – let doctors in other countries certify easily for US diagnostics and prescriptions.

- Elevate nurses to do all the stuff they already do, but in their own clinics without working for a doctor and paying the money up the chains.

- Start using search engines and artificial intelligence for diagnosis, rather than flawed and expensive humans.

- Open state and national boundaries for insurance and hospital services with only the required regulations for safety as we do with other imports.

- Eliminate the right for anybody to sue for medical malpractice, or indeed for pretty much anybody to sue anybody else for anything. Let’s make our professional reputation and our actions public and then just suck it up like adults, reinvesting the enormous proceeds currently wasted on litigation.

- Figure out if we can make single-payer health insurance work for us as it already does for most countries. There are many benefits, but the biggest is probably just eliminating all the mental energy we each waste on thinking about this mundane topic. As an analogy, imagine if every citizen had to hire their own police force for personal security – just think of how much energy and fear would be wasted on this topic, which we barely have to think about right now. As it turns out, it works the same way with health insurance.

Superphilosopher

Tom WrightThe truth behind it all.

corvidaezero: “As the father of no daughters because I’m...

Tom WrightTell 'em, kid.

“As the father of no daughters because I’m literally in 8th grade, I think sexual harassment is bad.”

These kid are the future.

Hip and Clavicle donated these amazing dragons to our silent auction!

Tom WrightEmily wants these so bad.

Hip and Clavicle is dedicated to charity!

Oh. My. Goodness. Just look at those awesome dragons. That is incredible. I’ve seen these with my own eyes and I still can’t get over how awesome this art is.

There are plenty more cool art pieces at Hip and Clavicle’s website, so go check that out, and come on out to the convention to bid on these great dragons.

Thanks Hip and Clavicle!

Ironmark Games donated to our Play-to-Win event again!

Tom WrightThis game is the boss, and I hope I win it in the silent auction (because I can't win it in the Play-to-Win).

Ironmark Games sent us two copies of San Ni Ichi and art books!

San, Ni, Ichi is a quick and light trick-taking card game designed to be played as a “filler” game while waiting for other games to finish or when time is limited.

San Ni Ichi is a super-fun game, so come on out and play it for the chance to win a copy! You’ll get the art book as well!

Thanks Ironmark Games!

Alternate Histories donated an awesome poster to our event!

Tom WrightThis is the kind of stuff that Natalie has been emailing people to donate. Super-cool.

Infantry.

Tom WrightAnd that's how you came to our family. Do you have any other questions?

brainstatic: Hey remember early last year when the Large Hadron Collider overloaded and broke down...

Tom WrightThis brings up a very good point.

Hey remember early last year when the Large Hadron Collider overloaded and broke down and people were like “phew good thing nothing weird happened like a shift in reality.” Maybe it’s time to revisit that.

Mr Sys Admin or Mr Admin Sys

Tom WrightUncool.