imop:

manita de sirenita.

As we mourn Maya Angelou on the day after her death, it’s heartening to remember that she lived several more lifetimes than most in her 86 years, some filled with pain and struggle, some with great joy. While generally known as a poet, writer, teacher, actress, and activist, Angelou actually got her start in the public eye as a Calypso dancer and singer, even appearing in a film, Calypso Heat Wave and releasing an album, Miss Calypso, both in 1957. It’s said that Billie Holiday told Angelou in 1958, “you’re going to be famous but it won’t be for singing,” She was right of course, but Angelou retained the air of a performer as a reader of her work. Above, see her deliver an animated reading of her famous poem, “Still I Rise,” which references many of her past lives, including lines that seem to allude to her Miss Calypso days: “Does my sexiness upset you? / Does it come as a surprise / That I dance like I’ve got diamonds / At the meeting of my thighs?” The stanza is indicative of another quality among the many she enumerates, “sassiness.” But she begins the reading on a more sober note, with a statement about human resilience, the ability to get up and face the day, despite the fears we all live with. “Wherever that abides in a human being,” she says, “there is the nobleness of the human spirit.”

That resilience, the transcendence of painful personal and ancestral histories, was the great theme of Angelou’s work, whether in poems like “Still I Rise” or her revealing 1969 autobiography I Know Why the Caged Bird Sings, also the title of a poem from her 1983 collection Shaker, Why Don’t You Sing?. While the caged bird is a very personal symbol for Angelou, her poem “On the Pulse of the Morning,” which you can see her read above at Bill Clinton’s 1993 inauguration, speaks to the whole human species in elemental terms. Again she twines themes of transcending painful and bloody histories with those of the “nobleness of the human spirit.” The speaker of the poem is the earth itself, who addresses each of us as “a bordered country / Delicate and strangely made proud.” “History,” she writes in much-quoted lines from the poem’s ninth stanza, “despite its wrenching pain / Cannot be unlived, but if faced / With courage, need not be lived again.” For all the pain Angelou herself endured and faced with courage, it’s a sentiment she earned the right to proclaim. Her celebration of not only the particular African-American struggle, but also its part in the universal human struggle for dignity and purpose stands as her enduring legacy. She ends the poem where she begins her reading of “Still I Rise” above, with a call for us to treat each other with care and respect, to not be “wedded forever / To fear, yoked eternally / To brutishness”:

Here, on the pulse of this new day

You may have the grace to look up and out

And into your sister’s eyes, and into

Your brother’s face, your country

And say simply

Very simply

With hope –

Good morning.

Both poems will be added to our collection, 550 Free Audio Books: Download Great Books for Free.

Related Content:

Studs Terkel Interviews Bob Dylan, Shel Silverstein, Maya Angelou & More in New Audio Trove

Josh Jones is a writer and musician based in Durham, NC. Follow him at @jdmagness.

Maya Angelou Reads “Still I Rise” and “On the Pulse of the Morning” is a post from: Open Culture. Follow us on Facebook, Twitter, and Google Plus, or get our Daily Email. And don't miss our big collections of Free Online Courses, Free Online Movies, Free eBooks, Free Audio Books, Free Foreign Language Lessons, and MOOCs.

The post Maya Angelou Reads “Still I Rise” and “On the Pulse of the Morning” appeared first on Open Culture.

Marie de France

Poet, 12th Century CE

Claim to fame: Author of immensely popular works that challenged societal norms.

Marie de France was a 12th century medieval poet. Details of her life are scanty but she was probably born in France and lived in England, possibly writing in the court of King Henry II.

Marie was proficient in Anglo-Norman French, Latin and English. Her most notable work is the Lais of Marie de France, a series of twelve narrative octosyllabic poems that influenced the development of the romance genre.

The Lais are captivating stories that glorify the romance and suffering of courtly love. The poems are notable for defying the traditional religious ideals of virginal love and marriage. Marie wrote about adulterous affairs with the heroines seducing men, extricating themselves from loveless or abusive marriages, exhibiting self determination and sexual freedom.

Marie’s remarkable willingness to romanticise adultery in the 12th century “reminds us that people in the Middle Ages were aware of social injustices and did not just accept oppressive conditions as inevitable by the will of God”.

TertiarymattBucky remains relevant. And nice to see some women featured on C77.

It's easy to make a good-looking tech accessory. But creating something that has the looks, a semi-secret—yet intuitive—functionality, turns waste scraps into something beautifully functional and whose name is inspired by the ever-motivational Buckminster Fuller? Not so simple. "Call me trimtab" is the famous Fuller line that got grad students Mansi Gupta and Cassandra Michel talking. The word in question, which became the duo's product name, refers to a tiny surface on the end of a ship's rudder that manages the direction of the ship. The tiniest of pressures can send it sailing a different direction. The term also can describe an individual whose small changes lead to a big impact, which is spot-on for Gupta and Michel. The two students, less than a month out from graduating SVA's Products of Design program, met in a Business Structures class where they took on a sustainable design project that was to become TRMTAB.

It's the perfect moniker for two reasons: 1.) The entire design is based around a tab that pulls your tech up and out of its holder with a simple yank; and 2.) The materials that make up the accessories are all waste products from Gupta's family factory—decades-old Prachi Leathers.

Growing up seeing Prachi at work, Gupta's intention was always to make something from the scraps the factory produced—which is the reason she found herself in the Products of Design program. "Mansi came to design school to find ways of creating social impact projects that stem from Prachi," Michel says. "The upcycling initiative is her first attempt. But now that the upcycling process has been iterated on, she's even excited to take TRMTAB to help neighboring factories with their waste and offcuts."

Each run at Prachi Leathers turns over 4,000 pounds of scraps. Instead of thinking in terms of product quantity, Gupta and Michel are looking at creating their project on the scale of one run's waste at a time, starting with some good old crowdfunding. Check out their video for more information on how they're turning all of that excess leather into TRMTABs:

(more...)TertiarymattDem dots get down.

Pen Point Percussion (1951), a behind-the-scenes introduction to the sound visualizations and drawn-on-film animation of film pioneer Norman McLaren, from the National Film Board of Canada.

And below, another playful example of McLaren’s work, Dots (1940), which includes sounds that may be considered hilarious to young people.

In the archives: What does sound look like? Plus more visual thinking, and more animation by Norman McLaren, including Boogie Doodle, a favorite.

TertiarymattTalk about a rad job.

How does fire spread? How do different forest materials fuel it? How can firefighters better understand its behavior in order to control it? Why is the physics of fire so counter-intuitive and mysterious to us?

At The Fire Lab in Missoula, Montana, highly-trained researchers conduct controlled tests with wind tunnels, fire-whirl generators, and giant combustion chambers to reverse-engineer fire. High-speed camera technology records everything and allows them to analyze each detail. Their mission: “improve the safety and effectiveness of fire management by creating and disseminating the basic fire science knowledge, tools, and applications for scientists and managers.”

The Mysterious Science of Fire by Katherine Wells and Sam Price-Waldman at The Atlantic, another great conversation starter about fire prevention and safety tips, and using matches as tools.

Related reading from May 2013: Archaeologists Find Earliest Evidence of Humans Cooking With Fire.

Related watching: What’s happening when a match is lit?, Why do hot things glow?, firefighter helmet cam, and Smokey and The Little Boy.

Thanks, @faketv.

TertiarymattSome direct relation to NW folks in here, re: coal export terminals.

Yves here. One observation that is often made in advanced economies is that having their citizens reduce their greenhouse gas emissions is futile because emerging economies are not willing to adopt the same standards. For instance, China was particularly up in arms about the 2007 IPCC reports, and has taken the position in climate change confabs that since the West emitted lots of carbon in its course of development, younger economies have that right too.

What is not as well known, and what this post focuses on, is how major energy companies are stoking and reinforcing these attitudes, using the same playbook that the tobacco industry deployed so successfully. The article mentions coal exports in particular, and it’s worth noting that coal-burning electrical plants are particularly destructive from a climate change and health perspective (both mercury and particulate emissions).

By Michael T. Klare, a professor of peace and world security studies at Hampshire College and the author, most recently, of The Race for What’s Left. A documentary movie version of his book Blood and Oil is available from the Media Education Foundation. Originally published at TomDispatch

In the 1980s, encountering regulatory restrictions and public resistance to smoking in the United States, the giant tobacco companies came up with a particularly effective strategy for sustaining their profit levels: sell more cigarettes in the developing world, where demand was strong and anti-tobacco regulation weak or nonexistent. Now, the giant energy companies are taking a page from Big Tobacco’s playbook. As concern over climate change begins to lower the demand for fossil fuels in the United States and Europe, they are accelerating their sales to developing nations, where demand is strong and climate-control measures weak or nonexistent. That this will produce a colossal increase in climate-altering carbon emissions troubles them no more than the global spurt in smoking-related illnesses troubled the tobacco companies.

The tobacco industry’s shift from rich, developed nations to low- and middle-income countries has been well documented. “With tobacco use declining in wealthier countries, tobacco companies are spending tens of billions of dollars a year on advertising, marketing, and sponsorship, much of it to increase sales in… developing countries,” the New York Times noted in a 2008 editorial. To boost their sales, outfits like Philip Morris International and British American Tobacco also brought their legal and financial clout to bear to block the implementation of anti-smoking regulations in such places. “They’re using litigation to threaten low- and middle-income countries,” Dr. Douglas Bettcher, head of the Tobacco Free Initiative of the World Health Organization (WHO), told the Times.

The fossil fuel companies — producers of oil, coal, and natural gas — are similarly expanding their operations in low- and middle-income countries where ensuring the growth of energy supplies is considered more critical than preventing climate catastrophe. “There is a clear long-run shift in energy growth from the OECD [Organization for Economic Cooperation and Development, the club of rich nations] to the non-OECD,” oil giant BP noted in its Energy Outlook report for 2014. “Virtually all (95%) of the projected growth [in energy consumption] is in the non-OECD,” it added, using the polite new term for what used to be called the Third World.

As in the case of cigarette sales, the stepped-up delivery of fossil fuels to developing countries is doubly harmful. Their targeting by Big Tobacco has produced a sharp rise in smoking-related illnesses among the poor in places where health systems are particularly ill equipped for those in need. “If current trends continue,” the WHO reported in 2011, “by 2030 tobacco will kill more than 8 million people worldwide each year, with 80% of these premature deaths among people living in low- and middle-income countries.” In a similar fashion, an increase in carbon sales to such nations will help produce more intense storms and longer, more devastating droughts in places that are least prepared to withstand or cope with climate change’s perils.

The energy industry’s growing emphasis on sales to these particularly vulnerable lands is evident in the strategic planning of ExxonMobil, the largest privately owned oil company. “By 2040, the world’s population is projected to grow to approximately 8.8 billion people,” Exxon noted in its 2013 financial report to stockholders. “As economies and populations grow, and living standards improve for billions of people, the need for energy will continue to rise… This demand increase is expected to be concentrated in developing countries.”

This assessment, explained Exxon CEO Rex Tillerson, will govern the company’s marketing plans in the years ahead. “The global business environment continues to provide a mix of challenges and opportunities,” he told financial analysts at the New York Stock Exchange in March 2013. While the demand for energy in the developed economies “remains relatively flat,” he noted, “energy demand for the economies of the non-OECD countries is expected to grow about 65% to support anticipated growth.”

In recognition of this trend, Exxon has undertaken a wide variety of initiatives intended to boost its sales capacity in China, Southeast Asia, and other rapidly developing areas. In Singapore, for example, the company is expanding a refinery and petrochemical facility that make up its “largest integrated manufacturing site in the world.” The refinery is being modified to produce more diesel, so as to better service the growing fleets of trucks, buses, and other heavy vehicles in the region. Meanwhile, the hydrocarbon processing facility at the chemical plant is being doubled to meet the rising demand for petrochemicals used in making plastics and other consumer goods, especially in China. (“China alone is expected to represent over half of global demand growth” for these products, Tillerson observed last year.)

To promote its products in China, Exxon has established a “strategic alliance” with the China Petroleum and Chemical Corporation (Sinopec), one of China’s state-owned energy giants. A key goal of the alliance is the establishment of an “integrated world-scale refinery and petrochemical complex” in eastern China which, Exxon officials noted, is to “become a major marketer of petrochemicals throughout China and petroleum products throughout Fujian Province.” A major component of this joint effort, the Fujian Refining and Ethylene Integrated Project, came on line in September 2009.

Exxon is also expanding its capacity to supply liquefied natural gas (LNG) to Asia. In partnership with Qatar Petroleum, it has built the world’s largest LNG export facility at Ras Laffan in Qatar and is building a mammoth LNG operation in Papua New Guinea. This $19 billion project, which began operation in April, includes a 430-mile pipeline to deliver gas from the island’s interior highlands to an export terminal near Port Moresby, the capital. “The project is optimally located to serve growing Asia markets where LNG demand is expected to rise by approximately 165% between 2010 and 2025,” said Neil W. Duffin, president of ExxonMobil Development Company.

Exxon is also expanding its capacity to supply liquefied natural gas (LNG) to Asia. In partnership with Qatar Petroleum, it has built the world’s largest LNG export facility at Ras Laffan in Qatar and is building a mammoth LNG operation in Papua New Guinea. This $19 billion project, which began operation in April, includes a 430-mile pipeline to deliver gas from the island’s interior highlands to an export terminal near Port Moresby, the capital. “The project is optimally located to serve growing Asia markets where LNG demand is expected to rise by approximately 165% between 2010 and 2025,” said Neil W. Duffin, president of ExxonMobil Development Company.

Next on the company’s agenda is a plan to draw on the natural gas being extracted in ever greater quantities from domestic shale formations in the United States via hydro-fracking and convert it into LNG for export to Asia. Although various American politicians have been pushing the strategic export of such supplies to Europe to “rescue” that continent from its reliance on Russian gas, Exxon has other ideas. It sees Asia, where gas prices are higher, as the natural market for its LNG — and U.S. foreign policy be damned. “By exporting natural gas,” Tillerson told the Asia Society in June 2013, “the United States could shore up the energy security of Asian allies and trading partners and stimulate investment in American domestic production.”

Big Energy’s “Humanitarian” Mission

In promoting such policies, Exxon’s executives are careful to acknowledge that growing concerns over climate change are generating increased resistance to fossil fuel consumption in Europe and other First World areas. When it comes to the rest of the planet, however, such concerns, they claim, should be outweighed by a “humanitarian” impulse to provide cheap fossil energy to poor people. Drawing on the arguments of Danish environmental renegade Bjørn Lomborg, author of The Skeptical Environmentalist, they argue that tending to the needs of the poor constitutes a greater priority than curbing global warming. “We must also recognize that there is a humanitarian imperative to meeting these growing global energy needs,” Tillerson typically asserted in 2013.

Asked why global warming shouldn’t be of greater concern, the Exxon CEO parroted Lomberg’s anti-environmental perspective. “I think there are much more pressing priorities that we… need to deal with,” Tillerson told the Council on Foreign Relations in June 2012. “There are still hundreds of millions, billions of people living in abject poverty around the world. They need electricity… They need fuel to cook their food on that’s not animal dung… They’d love to burn fossil fuels because their quality of life would rise immeasurably, and their quality of health and the health of their children and their future would rise immeasurably. You’d save millions upon millions of lives by making fossil fuels more available to a lot of the part of the world that doesn’t have it.”

Although the leaders of the other giant energy firms, including BP, Chevron, and Royal Dutch Shell, are less outspoken than Tillerson, they are pursuing a similar marketing strategy. “Demand growth [for petroleum products] comes exclusively from rapidly growing non-OECD economies,” BP noted in its recent report on the global energy outlook. “China, India, and the Middle East account for nearly all of the net global increase.” Like ExxonMobil, BP and the others are hard at work expanding their capacity to sell fossil fuels in these growing markets.

Nor are only the oil and gas companies pursuing this strategy. So is Big Coal. With coal demand declining in the U.S., thanks to the growing availability of low-cost natural gas generated by fracking, the coal firms are shipping ever more of their American output to Asia, which will contribute significantly to increasingly the carbon emissions there. According to the Energy Information Administration (EIA) of the Department of Energy, U.S. coal exports to China rose from essentially zero in 2007 to 10 million tons in 2012. Exports to India increased from 1.5 million to seven million tons and to South Korea from virtually nothing to nine million. Exports to just these three countries jumped by more than 1,000% during these years.

The EIA summarized the situation this way: “Companies in key parts of the U.S. coal supply chain — both producers and railways — have increased sales to Asia because of rising Asian coal demand, overall strong export prices, and lower U.S. consumption of coal to produce electric power.” Looked at from another perspective, diminished carbon emissions from coal in the United States — much touted by President Obama in his embrace of natural gas — has no significance when it comes to climate change, because of the greeenhouse gases being produced when all that coal is consumed in Asia.

To increase sales yet more, the giant coal companies are promoting the construction of new shipping terminals on the West Coast, including two each in Oregon and Washington State. The largest of these, the Gateway Pacific Terminal near Bellingham, Washington, will handle up to 48 million metric tons of coal a year, most of it destined for China and other Asian countries.

Although the terminals are often promoted by local officials as sources of new jobs, they are sparking fierce opposition from community activists and Native Americans who view them as posing a severe threat to the environment. Claiming that coal dust and spills from trains and loading facilities will harm fishing sites they deem vital, members of the Lumni tribe are citing longstanding treaty rights in their efforts to block the Cherry Point Terminal, one of the planned Washington State facilities.

In the Pacific Northwest, opposition to the coal terminals and the rail lines that will be so crucial to their operation — some of which will traverse Indian reservations and pass through green-minded cities like Seattle — is gaining strength. The process has been similar to the way climate activists mobilized against the Keystone XL pipeline that, if built, is slated to bring carbon-dense tar sands from Canada to the U.S. Gulf Coast. But the coal companies and their allies are pushing back, insisting that their exports are essential to the country’s economic vitality. “Unless the ports are built on the West Coast,” said Jason Hayes, a spokesman for the American Coal Council, U.S. suppliers won’t be viewed as “reliable business partners” in Asia.

Although community and tribal opposition may succeed in blocking or delaying a terminal or two, most analysts believe that, in the end, several will be built. “There are two billion people in Asia who need more power, so eventually more U.S. coal will get onto global markets,” says Matt Preston, an analyst for the energy consultancy firm of Wood Mackenzie.

Perpetuating the Fossil Fuel Era

In the end, all these efforts to boost fossil fuel sales in Asia and other developing areas will have one unmistakable result: a sharp rise in global carbon emissions, with most of the growth in non-OECD countries. According to the EIA, between 2010 and 2040 world carbon dioxide emissions from energy use — the main source of greenhouse gases — will rise by 46%, from 31.2 billion metric tons to 45.5 billion. Little of this increase will officially be generated by the planet’s wealthiest countries, where energy demand is stagnant and tougher rules on carbon emissions are being put in place. Instead, almost all of the growth of CO2 in the atmosphere — 94% of it — will be sloughed off on the developing world, even if a significant part of those emissions will come from the combustion of U.S. fossil fuel exports.

In the view of most scientists, an increase of carbon emissions on this scale will almost certainly lead to a global temperature rise of at least four degrees centigrade and possibly more by the end of this century. That’s enough to ensure that the changes we are already seeing, including severe droughts, stronger storms, raging wildfires, and rising sea levels, will be eclipsed by exponentially greater perils in the future.

Everyone will share in the pain from such warming-induced catastrophes. But people in developing lands — especially the poorest among them — will suffer more, because the societies they live in are least prepared to cope with severe catastrophes. “Climate-related hazards exacerbate other [socioeconomic] stressors, often with negative outcomes for livelihoods, especially for people living in poverty,” the UN’s Intergovernmental Panel on Climate Change observed in its most recent assessment of what global warming will mean for planet Earth. “Climate-related hazards affect poor people’s lives directly, through impacts on livelihoods, reduction in crop yields, or destruction of homes, and indirectly through, for example, increased food prices and food insecurity.”

Certainly, the giant fossil fuel companies bear a moral, if not as yet in our society a legal, responsibility for the intensification of climate change and the lack of serious response to it. Beyond this, their carefully planned strategy of selling carbon products to those most at risk can only be viewed as outright immorality. Just as health officials now condemn Big Tobacco’s emphasis on cigarette sales to poor people in countries with inadequate health systems, so someday Big Energy’s new “smoking” habit will be deemed a massive threat to human survival.

Above all, Big Energy is insuring that one small ray of good news when it comes to climate change — the contracting use of coal, oil, and gas across the developed world — will prove meaningless. The economic incentive to sell fossil fuels to developing countries is undeniably powerful. The need for increased energy in developing countries is no less indisputable. In the long run, the only way to meet these needs without endangering our global future would be through a mammoth drive to expand renewable energy options there, not by shoving carbon products down their throats. Rex Tillerson and his cohorts will continue to claim that they are performing a “humanitarian” service with their new “tobacco” strategy. Instead, they are actually perpetuating the fossil fuel era and helping to create a future humanitarian catastrophe of apocalyptic dimensions.

TertiarymattWow, this is crazy hard. #annieshare

This week's logo is really hard... and really pink.

The post Completely Unreadable Band Logo of the Week: Win a Prize Pack from Steamhammer/SPV! appeared first on MetalSucks.

Tonight’s comic probably isn’t going to help me sell my movie rights.

TertiarymattMore good stuff in here. Incidentally, it's not getting a lot of press, but the territory dispute between Vietnam and China is serious business.

Giddy up: John Lopez’s Wild West welded animal sculptures – in pictures Guardian

American War Dead, By the Numbers American Prospect

The loss of Memorial Day’s meaning is just one way we short-change veterans Guardian

Monsanto: the Toxic Face of Globalization Monsanto

Can Rural Brooks Actually Pose A Threat To The Environment? OilPrice. Headline misleading, but the substance is important.

Atlas hid: Uber has set up a decoy office to keep drivers away from its shiny new HQ

Malaysia Airlines Flight 370: Gov’t releases raw satellite data linked to plane’s path CBS

China’s housing “Titanic” MacroBusiness

China Middle-Class Protests Turn Violent After Petitions Ignored Bloomberg

Vietnam accuses China of sinking boat Financial Times

Heads roll across Europe in wake of polls Financial Times

Euro-Election Post-Mortem… Cassandra

Winner Accuses French Government of “Massive” Election Fraud Wolf Richter

Europe must create jobs to counter populist wave – Merkel Irish Times. This would be funny if it weren’t so pathetic.

France urges reform of ‘remote’ EU BBC

Russia joins global dash for shale in policy volte-face Ambrose Evans-Pritchard, Telegraph

Ukraine

Obama talks Ukraine, swipes at Putin Politico

Ukrainian leader vows swift action against ‘pirates’ Washington Post

Ukraine launches air strikes against pro-Russia militants Financial Times

Ukraine president: calm ‘in hours’ amid airport battle Guardian

Ukraine Forces Appear to Oust Rebels From Airport in East New York Times

Big Brother is Watching You Watch

Glenn Greenwald to publish list of U.S. citizens that NSA spied on Washington Times

Snowden ‘considers’ returning to US – report RT (furzy mouse)

E.U. Debates Which Nation Will Regulate Web Privacy New York Times

Obamacare Launch

Obama Administration Moves To Unilaterally Make Billions Available To Insurance Companies Under The ACA Jonathan Turley

How Obamacare Will Screw Black Doctors Daily Beast

Doctors Surveyed On First 120 Days With New Obamacare Patients Forbes

Health Care Cost-Sharing Works — Up to a Point New York Times

EPA Set to Unveil Climate Proposal Wall Street Journal. Um, while the US fracks, which releases methane?

Republican Warmongers Should Be Held Accountable for VA Scandal Alternet

Rove: Clinton ‘old and stale Politico. Sexism alert.

Flashboys and “Investor” Outrage Triple Crisis

FT v. Piketty

Thomas Piketty’s real challenge was to the FT’s Rolex types

FT analysis of my book is ‘ridiculous’, says Thomas Piketty Independent (furzy mouse)

Class Warfare

Global income distribution: From the fall of the Berlin Wall to the Great Recession VoxEU

“The US Labor Market is Not Working;” Antonio Fatas “On the Global Front” Angry Bear (psychohistorian)

Krugman: How American Capitalism Fails—and Northern European ‘Socialism’ Succeeds—at Job Creation Alternet (furzy mouse)

Antidote du jour (Planet Earth, via Lambert):

TertiarymattAlso good for removing botflies, maybe?

Many, many thank yous to my studiomate and friend Lucy Bellwood for filling in for me this week while I flail around with Muppet arms over the Oh Joy, Sex Toy book Kickstarter!

You’ve got 24 days left to pre-order a copy of the Oh Joy, Sex Toy book and help increase the page rate we pay to our guest cartoonists!

Tertiarymatt"Now that anti-European political parties have a substantial Trojan horse within Brussels, they will likely set to work undermining its efficacy on every front. That, in turn, will win them more seats over time at home and within Brussels as their skepticism delivers a self-fulfilling failure for the EU."

That sounds like a rather familiar strategy.

By David Llewellyn-Smith, founding publisher and former editor-in-chief of The Diplomat magazine, now the Asia Pacific’s leading geo-politics website. Originally posted at MacroBusiness

European elections are in the process of delivering huge swings extremes of the Left and Right extreme. From the Financial Times:

France’s nationalist extreme right turned European politics upside down on Sunday, trouncing the governing Socialists and the mainstream conservatives in the European parliamentary elections which across the continent returned an unprecedented number of MEPs hostile to, or sceptical about, the European Union in a huge vote of no confidence in Europe‘s political elite.

According to exit polls, the Front National of Marine Le Pen came first in France with more than 25% of the vote. The nationalist anti-immigrant Danish People’s party won by a similar margin in Denmark. In Austria, the far right Freedom Party took one fifth of the vote, according to projections, while on the hard left, Alexis Tsipras led Greece‘s Syriza movement to a watershed victory over the country’s two governing and traditional ruling parties, New Democracy conservatives and the Pasok social democrats.

…In Britain, the Nigel Farage-led insurrection against Westminster was also tipped to unsettle the polticial mainstream by coming first or second in the election. The Tories, the biggest UK caucus in the parliament for 20 years, faced the prospect of being pushed into third place.

In Germany, the most powerful EU state, Chancellor Angela Merkel’s Christian Democrats scored an expected easy victory, but Germany also returned its first eurosceptics in the form of the Alternative for Germany as well as its first neo-Nazi MEP from the Hitler apologists of the National Democratic Party of Germany, according to German TV projections.

These results are enough to complicate but not derail the European project, for now. There are two ways to look at this. The first is expressed by Gideon Rachman at the FT:

The protest vote is not nearly big enough to be labelled a comprehensive rejection of the EU, its political values and its economic crisis management over the five years since the last European elections. Eurosceptics, broadly defined, are projected to win about 130 of the EU legislature’s 751 seats. Given that the EU has just gone through the biggest financial shock and recession of its 56-year history, the damage could have been greater.

…The triumph of Marine Le Pen and her FN spreads more poison into French politics than at any time since the 1954-62 Algerian war of independence. It makes even more arduous the task of Mr Hollande and Manuel Valls, his new prime minister, in executing the modernising economic reforms on which a healthy Franco-German partnership at the helm of the EU depends.

The UK Independence party’s success will pile pressure on David Cameron, the British premier, and his Conservative party to harden its stance even more on EU issues.

Although there’s not enough in the European shift to derail Brussels, there is more than enough in the domestic political implications for pro-European leaders to weaken their commitment.

The second interpretation is less sanguine. If there is one lesson from pre-war Germany that is worth bearing in mind it is that obstructionist politics is a long term winning strategy for power.

Now that anti-European political parties have a substantial Trojan horse within Brussels, they will likely set to work undermining its efficacy on every front. That, in turn, will win them more seats over time at home and within Brussels as their skepticism delivers a self-fulfilling failure for the EU.

TertiarymattI continue to be impressed by these link roundups. Tons of solid stuff in them.

In dogs’ play, researchers see honesty and deceit, perhaps something like morality WaPo

A glimpse into nature’s looking glass — to find the genetic code is reassigned: Stop codon varies widely Science Daily

Emotion Markup Language 1.0 (No Repeat of RDF Mistake) Another Word For It

Denied again by people he hated, gunman improvised AP (transcript).

Only Tool Left Eschaton

Barack Obama, Wall Street co-conspirator David Sirota, Salon

QE reduction in time for next speculative kickoff Michael Hudson

‘Unpacking the First Fundamental Law’ James Galbraith, Economist’s View (gordon). Must read.

Reviewing Lawrence H. Summers’s Review of Piketty II: The Post-1980 Rise of Extreme Inequality in America Washington Center for Equitable Growth. Fun post.

Why should tech people care about public pension scandals? I’m glad you asked… Pando Daily

Big Brother Is Watching You

The eBay hack, the loss of 140 million records, and the PR fiasco Kevin Townsend

HOW THE US INSTITUTIONALIZED SURVEILLANCE Al Jazeera

The NSA is Not Made of Magic Bruce Schneier

A Google Glass Feast EV Grieve. Glassholes dump on restaurant for protecting its patrons privacy, aided by Google’s preferential treatment of Google+ in search.

Ukip storms European elections Telegraph

Eurosceptics storm Brussels FT

Front National wins European parliament elections in France Guardian

SYRIZA scores first election win but coalition stands firm after EU vote Ekathimerini

Europe’s brutal discipline Le Monde Diplomatique

Ukraine

Petro Poroshenko claims Ukraine presidency BBC. Chocolate tycoon.

The Irreversible Crisis of the Ukrainian Experiment Roberto Orsi, Euro Crisis in the Press (barrisj)

The State Department’s Ukraine Fiasco Consortium News (RS)

Ukraine: Major “Western” Think Tank Admits Defeat Moon of Alabama. Putin in the catbird seat, right where he always was. Can’t we just pay off all the neo-cons and ship them, together, to a faraway island?

Western intervention will turn Nigeria into an African Afghanistan Guardian

14 Ways of Looking at Thailand’s Military Coup Smoke and Mirrors

What the U.S. Can Learn From Brazil’s Healthcare Mess The Atlantic

ObamaCare

The Legality of Delaying Key Elements of the ACA vs. Obama’s ACA Delays — Breaking the Law or Making It Work? NEJM

I.R.S. Bars Employers From Dumping Workers Into Health Exchanges Times. But dumping others is fine!

Treating veterans in private hospitals could ease pressure on VA facilities Guardian. No underpants gnomes, neo-liberals: 1) Starve public programs; 2) Run PR campaign; 3) Privatize and profit!!!

The party’s over LRB

How “tightness” vs “looseness” explains the U.S. political map WaPo. Pleased to see that Maine is #5 on the scale of looseness, right behind Nevada. State averages conceal, though. Pennsylvania is in the second quintile of tightness, but Philly is more than loose; it’s positively slack.

Class Warfare

An Anonymous Rich Person Is Hiding Money All Around San Francisco HuffPo. Flinging coins to the peasants and watching them scramble.

Always Low Wages, More Pollution: Why Barack & Michelle Obama Relentlessly Shill For Wal-Mart Black Agenda Report

These Housekeepers Asked Sheryl Sandberg to Lean In with Them. What Happened Next Will Not Amaze You Crooked Timber. I gotta tell ya, my jaw just dropped.

Equal Rights to Profit from Impoverishing People and Causing a Great Extinction Event Ian Welsh

But they’re too complicated! Pharyngula (Avedon)

The Trigger-Happy University The Baffler

How much have white Americans benefited from slavery and its legacy? Marginal Revolution

Can the Nervous System Be Hacked? Times

Taking Print from Print Culture & Leaving the Public Sphere Behind The Junto

Antidote du jour, Animals in War Memorial, London, UK (via):

Memorial Day bonus tune:

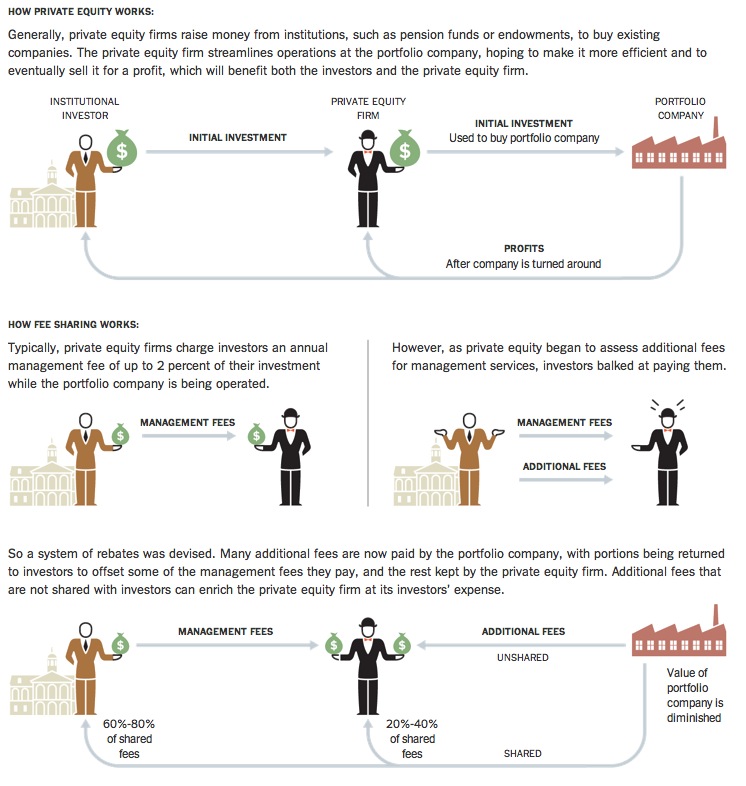

TertiarymattA big chunk of reading on bad behavior by PE.

Welcome! We anticipate that some of you are new to this site and have visited to access the 12 private equity limited partnership agreements that we published in searchable form. You can find them here and here.

But we also thought you might want to familiarize yourself with our recent coverage of the private equity industry.

By way of background, I’ve been in and around the financial services industry for my entire career. I joined the corporate finance department of Goldman in the early 1980s, when Wall Street was criminal only at the margin. I then went to McKinsey, and in the mid-1980s, started up and led the mergers and acquisition department for Sumitomo Bank, then the world’s second largest bank. Next, I founded a management consulting practice that did McKinsey-style consulting for wholesale banks and trading businesses, and also provided transaction advisory services to private equity firms, hedge funds, and substantial individuals (Forbes 400 level).

In 2006, I launched Naked Capitalism, which provides incisive analysis and commentary on finance and the financial services industry. We have an active following on the Hill and at all the major financial regulators.

Over this period, we’ve written over 200 posts on private equity. In the last year, we’ve increased our focus on the industry. In addition to the limited partnership agreements release, other stories we’ve broken include:

Los Angeles Public Pension Fund Tells Us It Is a Happy, Trusting Victim of Investment Managers (2014)

Claire’s Stores: Private Equity Broker-Dealer Violations in Action (2014). How Apollo couldn’t be bothered to comply with most of the usual niceties to make transaction fees look like fees for services that were actually provided.

IRS Wakes Up to Private Equity Scam (2013). On how an IRS crackdown on management fee waivers (the device used to obtain capital gains treatment) is underway.

Why You Should Not Trust the Financials of Private Equity Owned Companies (2013). On how a widely used software platform, iLevel Solutions, is built from the ground up to convince PE investors and the SEC that Blackstone and other PE firms have implemented robust financial controls over the companies they own. The reality, however, is the opposite: by design, iLevel gives PE firms unprecedented ability to cook the books of their portfolio companies while maintaining a facade of compliance.

How Private Equity Executives Like Blackstone’s Tony James Engage in Dubious Side Deals (2013)

In addition, we’ve provided commentary and analysis on the private equity industry, such as:

Wall Street Journal Exposes Possible Grifting by Private Equity Kingpin KKR and KKR Capstone (2014)

McKinsey Gives “Dare to Be Great” Speech to Private Equity Investors as Returns Fall (2014)

Private Equity’s Lake Woebegon Fallacy: All Investors Are Above Average (2014). On how the widely-accepted premise that investors can invest solely in top-quartile funds is absurd on its face

Wall Street Journal Exposes Entirely New Private Equity Tax Scam (2014)

Whistleblower Describes How Private Equity Firms Flagrantly Violate SEC Broker-Dealer Requirements (2013)

Matryoshka Doll, Private Equity Edition (2013)

Memo to Eliot Spitzer: Private Equity Firms are Scamming New York City (2013). We highlighted early that the SEC was discussing fee abuses at private equity firms (admittedly then in general language). We discussed why the industry was so keen to keep limited partnership agreements secret:

The sad truth is nobody who invests in PE looks closely at whether PE firms are complying with the fee and expense provisions of their agreements. Part of the reason is that the PE firm lawyers draft the terms in these LPAs to be almost incomprehensible. Another reason is, astonishingly, that PE investors have accepted the argument of PE firms that these contract provisions are a form of “trade secret.” Public pension fund investors have almost universally acceded to the demands of PE firms to exempt the LPAs and cash flow reports from state FOIA laws, which keeps the eyes of the press and the public off the documents.

This information lockdown prevents a worst-case scenario for scamming PE firms, that a mid-level accounting employee at a portfolio company would use public documents to compare the payments made to fund investors with what was taken from the portfolio company where the accountant works. State qui tam laws, which are designed to prevent precisely this type of abuse by awarding a portion of the government’s recovery to people who uncover fraud, would provide a powerful incentive for employees at portfolio companies to rat out their PE overlords. But that’s not going to happen as long as public pension fund PE investors keep the contracts and cash flows behind the FOIA wall.

Why is a Price-Fixing/Collusion Lawsuit Against the Biggest Names in Private Equity Getting Only Cursory Notice? (2012). On a class action lawsuit, Dahl v. Bain Capital Partners, against the eleven biggest and most blue-chip names in the private-equity industry, including Blackstone, Carlyle, Goldman, and TPG, for price collusion on “club” deals.

We’ve also discussed the private equity rush into the single family rental market:

We Speak About Private Equity Rental Housing and SEC Problems on RT (2014)

Slumlord Wannabe Blackstone Violates Local Housing Laws by Making Tenants Maintain Rentals (2014)

Rental Income Falls 7.6% in Three Months in Blackstone’s First Home Lease Securitization (2014)

How the Foreclosure Crisis Made the Rich Even Richer (2013)

So Who is the Dumb Money Ruining the Rental Housing Market? (2013)

Private Equity Residential Landlords Rushing to Cash Out via IPOs(2013)

We’ve also had a series of posts from an industry insider:

Private Equity Collusion on Deals (2012)

Private Equity: The Mechanics of Intellectual Capture (2012)

Private Equity Fund Terms (2012)

Some of you may have read Chris Witowsky’s coverage in peHUB about our ongoing efforts to pry private equity return data out of CalPERS:

* * *New York Times Column Strikes Back, Obliquely, at Our CalPERS Private Equity Data Suit (2014)

CalPERS Tries Ineffective Mudslinging in Response to Our Ongoing Private Equity Investigation (2014)

Prominent Retiree Chides CalPERS for Repeating Conduct that Led to Past Private Equity Scandals (2014)

Reuters Writes About Our Suit Against CalPERS to Obtain Private Equity Data (2014)

We Sue CalPERS Over Denial of Our Private Equity Public Records Act Request (2014)

Over the coming months, I anticipate we’ll get to know each other even better.

TertiarymattI look forward to a potential backlash against the PE firms that have been conning people and mooching off the misfortunes of others.

Last week, the Wall Street Journal released an important story that chronicled how the private equity industry kingpin KKR systematically took advantage of its credulous investors via taking questionable charges through its related company KKR Capstone. That story depended critically on the Wall Street Journal obtaining the terms of the investment from a 2006 KKR limited partnership agreement so that it could ascertain whether the investors had authorized these charges. Readers may recall that the private industry heretofore has kept these contracts under lock and key, insisting zealously that they be kept in the strictest confidence possible by those who obtain access to them.

We’ve published 12 private equity limited partnership agreements (LPAs), including the KKR limited partnership agreement that key to the Wall Street Journal’s story, in a searchable format that you can view here and here. We obtained the documents through the Pennsylvania Treasury’s public e-contracts library. Until now, it appears virtually no one knew that they had been made public. And you can be sure that if anyone associated with the private equity industry had recognized what had occurred, they would have shut this window immediately.

It is hard to overstate the significance of Pennsylvania’s release of these private equity limited partnership agreements. This development will change the industry forever. Even a superficial reading of these documents shows that investors and policy-makers were naive to treat private equity general partners as deserving of the blind trust they had placed in them.

For decades, private equity (PE) firms have asserted that limited partnership agreements (LPAs), the contracts between themselves and investors, should be treated in their entirety as trade secrets, and therefore not subject to disclosure under Freedom of Information Act laws in any jurisdiction. These private equity general partners argued that the information in their contracts was so sensitive that it needed to be shielded from competitors’ eyes, otherwise their unique, critically important know-how would be appropriated and used against them. In particular, PE firms have made frequent, forceful claims that their limited partnership agreements provide valuable insight into their investment strategies. The industry took the position that these documents were as valuable to them as the formula for Coca-Cola or the schematics for Intel’s next microprocessor chip.

Now that we can look at the actual language in limited partnership agreements, we can see what any sophisticated user of legal instruments would guess: the PE firm lawyers describe the strategy in the broadest, most general terms to give the private equity fund as much latitude as possible. For example, here is the investment strategy language from the KKR 2006 Fund:

2.1 Objectives The objective and policy of the Partnership are to invest in (i) Securities of Persons formed to effect or which are the subject of management buyouts or build-ups sponsored by the General Partner or any Affiliate thereof and (ii) Securities of Persons the investment in which the General Partner reasonably expects to generate a return on investment commensurate with the returns typically achieved in previous KKR-sponsored buyouts, build-ups and growth equity investments.

Claiming this statement is a trade secret is analogous to the U.S. Navy claiming classified status for the fact that it operates ships on oceans.

Moreover, if you read the balance of section 2.1 (“Objectives”), you see that that most of the remainder of the paragraph deals with the goal of tax avoidance, with 195 words in the paragraph dedicated to this issue. When KKR claims the limited partnership agreement is a trade secret, it’s not hard to surmise that these tax games are a big part of what they are really trying to hide. But now that we can look across a series of limited partnership agreements, it’s clear that the tax strategies are highly parallel across funds. To the extent that there is anything distinctive, it’s in minor details relating to the implementation of the tax scheme, and not its objective or design.

The closer you look, the harder it is to find information in the LPAs that even approaches a bona fide trade secret. Could it be the management fee? Platinum Equity Capital Partners III says in its LPA (p. 158) that the management fee during the commitment period is equal to “0.4375% per quarter”. At the same time, in its publicly-available Form ADV Part 2 (p. 4), the firm discloses that “Platinum Equity Capital Partners III, L.P., together with its Parallel Funds, is subject to a Management Fee of up to 1.75% [annually] of committed capital…” (1.75% = 0.4375% X 4). So, apparently that’s not the trade secret either.

Key person terms are another provision of LPAs that PE firms have asserted rise to trade secret status. The idea behind a “key person” provision is that certain individuals are critical achieving the sought-after investment returns and the investors thus depend on their expertise and experience. The agreements provide that if any of these “key persons” depart or otherwise can no longer work for the private equity firm, the limited partners can stop contributing capital to a fund or even force its dissolution.

Let’s look at Milestone Partners IV, where in section 3.2(h), you can see that both John P. Shoemaker and W. Scott Warren are defined as the sole “key persons”. Are we supposed to be surprised by this? Both Shoemaker and Warren are described on the firm’s website as Milestone’s sole managing partners. So there is nothing really a secret about this either, nor is it easy to see how disclosure of Shoemaker’s and Warren’s key person designation, even if it were previously a secret, would hurt Milestone upon disclosure.

So what might be the reason for such stringent efforts to maintain secrecy? We described one reason why private equity firms are keen to keep limited partnership agreements confidential last year:

This information lockdown prevents a worst-case scenario for scamming PE firms, that a mid-level accounting employee at a portfolio company would use public documents to compare the payments made to fund investors with what was taken from the portfolio company where the accountant works. State qui tam laws, which are designed to prevent precisely this type of abuse by awarding a portion of the government’s recovery to people who uncover fraud, would provide a powerful incentive for employees at portfolio companies to rat out their PE overlords. But that’s not going to happen as long as public pension fund PE investors keep the contracts and cash flows behind the FOIA wall.

How realistic is that scenario? Two days ago, the New York Times’ Gretchen Morgenson quoted a high-level SEC official discussing the practices of PE firms: “In some instances, investors’ pockets are being picked.” So, it’s reasonable to suspect obscuring this “pocket picking” is a major reason why general partners insist on keeping LPAs hidden.

A cursory look shows that the KKR, TPG, and Platinum LPAs all contain management fee waiver provisions (see language relating to “Increased Capital Amount” in KKR; “Waiver Election Amount” “Waiver Contribution” and “Waiver Earnings” in Platinum; 6.02(c)-The Management Company may “elect to waive all or a portion of the Management Fee…” “for a number of quarterly periods determined by the Management Company” in TPG). We have written extensively about this tax dodge, whereby PE firms con their investors into enabling a scheme that allows private equity general partners to convert what would otherwise be ordinary income into capital gains. The PE firms purportedly “waive” their management fees in return for supposedly receiving additional carried interest compensation. This is similar to telling your boss not to give you the raise he’s offered, but to buy you Yankees season tickets with the money instead, and claiming that the transaction is tax free.

The IRS has been grumbling for some time that it’s on to this maneuver and takes a dim view of it. In April, a high-ranking official made a speech intimating that the IRS is finally clamping down. Regulations will be issued shortly that will clarify that, under existing law, fee waivers are do not achieve the claimed tax result. Somebody needs to ask the investors in the KKR, TPG, and Platinum funds how they justify cooperating with this scheme in light of the IRS’ vocal disapproval.

The LPAs also reveal potentially illegal efforts for the funds and their investors to hide arcane but important forms of income called “UBTI” (“Unrelated Business Taxable Income”) and “ECI” (“Effectively Connected Income”). The idea behind both UBTI and ECI is that tax exempt investors should not be able to hide behind their tax-free status to operate businesses that would have a competitive advantage because the profits aren’t taxed. As a result, UBTI federal tax is assessed on U.S. non-profits and ECI federal tax on foreign investors in U.S. funds to level the playing field.

One of the few ways that limited partners have pushed back against the general partners is that the limited partners have demanded and won a de facto fee reduction via the sharing of general partner transaction and monitoring fees with limited partner investors (as we’ve also discussed, the degree to which there actually were any services rendered is open to question). But for the limited partners to take their partial rebate of these fees would clearly constitute UBTI/ECI absent any special maneuvering to avoid the tax.

PE firms long ago came up with the idea of crediting these rebates against the management fees otherwise owed by investors, rather than writing checks to investors. The argument for why these management fee offset arrangement doesn’t implicate UBTI/ECI gets fairly arcane, but the key point is that the PE firms take the position with the IRS that “Hey, we’re not sending the investors checks, so it’s not UBTI/ECI.”

Now that we can scrutinize LPAs, however, we see that some do call for checks to go back to the investors. For example, on p. 158, Section 3.02(d) TPG’s limited partnership agreement says:

(d) On a cumulative basis, the Management Fee due in respect of each Limited Partner (including any additional Limited Partner) shall be reduced by an amount equal to one hundred percent (100%) of such Limited Partner’s share of Net Fee Income, if any, B-3 received by the Management Company, any Principal or any Affiliate of the Management Company, in each case in connection with such Person’s activities as a representative, or on behalf, of the Partnership. To the extent that the amount referred to in the preceding sentence exceeds the Management Fee due in respect of such Limited Partner, such excess shall be carried forward and, if not previously applied against such Management Fee, shall (notwithstanding paragraph 4.02(d) of the Partnership Agreement) be paid by the Management Company (or its Affiliate) to such Limited Partner upon liquidation of the Partnership [emphasis added].

Oops.

What this complicated section provides for is that TPG will roll forward any management fee credits that can’t be applied in a given period because the management fee has already been reduced to zero. If any remain at the end of the fund life, the investors get a check. So, rather than there being the potential for payment issuance in any particular accounting period, TPG has pushed the accounting around so that any check is issued just once, at the end of the fund life. But it’s the same either way, and the key point is that the practice pretty much destroys their argument that these payments are not subject to UBTI/ECI tax. Other of the LPAs have this same feature (see, for example, Palladium at p. 100 section 4(b))

Some of the language in these documents is so sneaky that, if the investors’ lawyers didn’t flag it in the legal review process, they are arguably guilty of malpractice. And, if their lawyers did point it out, yet the investors ignored the problem, one can only ask: What were they thinking?

We’ll offer just one very disturbing example of how the PE firms use language to mislead, from the “Definitions” section of the KKR 2006 Fund LPA. A careful reading reveals that all of the following are defined terms: “KKR”, “Affiliate”, and “KKR Affiliate”. Critically, “KKR Affiliate” is much narrower than what “KKR” and “Affiliate” mean when defined separately. And KKR clearly understood that what was and wasn’t an affiliate was key to its KKR Capstone fee-hogging activity. As we noted in our analysis of the Wall Street Journal story on KKR Capstone, whether or not the SEC goes after KKR on this matter hinges on whether it accepts KKR’s tortured defense.

The term “Affiliate” has the meaning that readers of corporate agreements would expect and refers to both entities and individuals. A “KKR Affiliate” refers only to entities controlled directly or indirectly by KKR.

This distinction matters a great deal. Section 6.3.1(b) appears to provide the fund investors with the critical protection they need against various forms of fee skimming that both KKR entities and their executives might otherwise be free to pursue with the fund’s money or the money of portfolio companies:

The General Partner, KKR and the KKR Affiliates will not engage in any transaction with the Partnership or any Portfolio Company or subsidiary thereof unless the terms of the transaction are on an arm’s-length basis and no less favorable to the Partnership or such Portfolio Company than would be obtained in a transaction with an unaffiliated party…

What is clearly intended here is for investors to read the term “KKR Affiliates” as synonymous with “Affliates” of “KKR”. But that’s not what it means. If it did mean “Affiliates” of “KKR”, the restriction would prevent KKR executives from having side businesses that they could force the fund or the portfolio companies to hire for purported “services”. This is not a hypothetical situation. We documented that Tony James, the COO at Blackstone, has just such a business that is active in industries in which Blackstone owns portfolio companies. The investors no doubt believe they got a restriction on related party activities, but Blackstone’s agreements almost certainly contain similar language which permits this sort of abuse.

For decades, the NSA kept its domestic spying activities under wraps, claiming that it served as a wise and responsible steward of the powers with which it had been entrusted. Similarly, the private equity industry has insisted for decades that none of the usual SEC and FOIA transparency requirements should apply to its activities, but that the general partners should be trusted to comply with the law and treat investors fairly.

Snowden’s documents revealed that much of the NSA’s domestic spying is arguably illegal, and that a primary objective of the secrecy surrounding it was to shield the NSA from accountability and oversight, since that would curb the scope of the agency’s actions. The private equity industry now finds itself in much the same situation, albeit in this case, there’s no Snowden-like insider who chose to break institutional rules and give confidential information to journalists. Here, a public pension fund had simply made them public and it took a surprisingly long amount of time for anyone to notice.

Nevertheless the uncomfortable analogy to the NSA’s fetish with secrecy remains. Here the exposure of key documents reveals the private equity industry’s claims that the general partners obey the law are false. Instead, critical elements of their scams and violations of public interest depend on their being hidden from view.

The document release also reveals what dupes the investors have been. The SEC has already reached that conclusion, stating in a recent speech that investors have done a poor job of negotiating agreements so that they protect their interests and have done little if any monitoring once they’ve committed to a particular fund. As we’ll chronicle over the next few days, anyone who reads these agreements against the disclosures that investors are now required to make to the SEC and the public in their annual Form ADV can readily find numerous abuses, which range from bad-faith dealing to potentially criminal conduct. And remember, investors have far more detailed information, and also can ask the general partners questions if they detect practices that look sus.

But rather than live up to their fiduciary duties, pension funds that have invested in private equity funds haven’t merely sat pat as they were fleeced; even worse, they’ve been staunch defenders of the private equity industry’s special pleadings.

The private equity industry’s obsession was never about competing effectively. It was a self-serving ploy to shield the documents from scrutiny, since third parties might ferret out how private equity firms increase their already substantial profits at the expense of complaint, clueless investors. And as we’ll discuss in more depth, quite a few general partners have been both relentless and shameless in how they’ve gone about it.

TertiarymattSomewhat slapdash pdf of his talk on the click-through. As always with him, he makes a grim sort of sense.

Peter Watts digs into the relationship between evolution, surveillance, and the human spite reflex, as they relate to online privacy and government spying.

TertiarymattFirst record is available for free/cheapness on Bandcamp, too.

![]()

(Our Russian contributor Comrade Aleks is back with yet another interview, this time with J.Luoto, the drummer of Finland’s Slug Lord.)

Let me introduce you to Slug Lord of Finland. This band have played bloody sinister sludge’n’stoner doom tunes since 2010, yet they had a long break after release of their self-titled album in 2011 because of some line-up changes. Anyway, their second full-length Transmutation was released literally a month ago and J.Luoto (Slug Lord’s drummer) found some time to discuss details about the new album.

***

Terve J.! How are you man?

Thanks for asking! We’ve just received our latest album’s batch from press and are getting ready to send them to all the crazy folks who pre-ordered it.

Let us start with that old ’n’ good question about the band’s origin – what are the main milestones of Slug Lord?

We’ve known each other since childhood and played shit together for years. On the ruins of some less serious band projects we formed a doom band. During some intense listening and jamming songs of bands like Pentagram, Electric Wizard, Acid King, and Witch, we gave birth to Slug Lord. Within this genre we found the ways to express our musical ambitions as a unit and in the loudest and heaviest way we could. Then we recruited the singer Johanna Rutto, recorded the first self-titled album with her, and also made a few gigs. After her departure we’ve been more than happy with the original trio lineup and continued the path with a passion for playing live and making more records.

Does this mean that Slug Lord (with its stabilized line-up) will now work full speed on playing more gigs and recording more songs?

We’ll keep gigging at a steady pace. There’s a few already booked this year, most importantly the Kiarama festival in Pori on September 12th-13th. Now that we just released our second album Transmutation, we could fit in a few more gigs for the summer — touring a little and promoting the album.

Making the album was a tediously slow process at times because of other commitments in our personal lives. We also accepted almost any gig offer we got and took time off from making the album to concentrate on the gigs. It was fun to not lock ourselves into one thing, but it postponed the album’s release. We’re planning to record the next album with a faster method, maybe even like a “live in studio” type of thing. We have one album’s worth of new songs already nearly finished and a lot more coming, and I can’t wait to get to record them!

Now you have the new album Transmutation and a new vocalist — who is he? And where is Johanna Rutto? A sludge band with female vocals would be pretty attractive.

Actually you can hear voices from all three of us on Transmutation. Our guitarist did all the lead vocals, though, and he also sings live, so we might as well credit him as the singer in the band. Johanna left the band with no hard feelings. We’re still friends, she is still making music, and I wish all the best and great success for her.

I think that Slug Lord became heavier and dirtier with the new album. Was it a normal process for you? Or was this transmutation totally uncontrolled?

It was intentional, but came out naturally. The new album showcases our live sound more accurately and it better matches the course we set ourselves to pursue originally. But with that done, you never know in what direction the following releases will take us.

Can you name one or two bands that had the most significant influence upon you?

These two need to come from childhood, and for myself it was Metallica and Nirvana, who got me into rock and metal music. Through that period I also loved all kinds of home computer music I got my hands on, especially the classic composers on the C-64.

You have pretty atmospheric and psychedelic elements in the songs “Orgy with the Dead” and “Vorthex”. What are your main psychedelic influences? And what drove you to write “Orgy with the Dead”?

Psychedelia in any art form can be inspiring and definitely influences us in songwriting. In addition to music, we’re movie and comics buffs. In terms of substance abuse, we mostly stick with alcohol.

The creation process for “Orgy with the Dead” was one of the most collaborative we’ve had in the band. Usually one of us brings along a nearly complete skeleton of riffs and structures that we then finalize together. But here it was just about throwing a riff there and a riff here and a lots of jamming together that eventually created the song. The collective idea was to create something heavier, darker, and more twisted than we had before, while also having these atmospheric moments in between to balance the overall feeling of the song.

The album consists of songs with such names as “Gastropoda”, “Orgy with the Dead”, “Triumphant Drunk”, and so on. Can you sum up the song’s subjects?

The lyrics were written by the other guys on those songs, so unfortunately I’m not the correct person to ask. Anyway, as I interpret it, “Triumphant Drunk” is a gritty portrayal of going apeshit when intoxicated in the most traditional Finnish style. “Orgy with the Dead” and “Gastropoda” drift more in certain moods, horrors, and mythology, and I don’t want to give them away too much.

Slug Lord: “Vortex”

We didn’t actively contact any labels. Our method of doing PR is mostly sitting on our asses and waiting for the contacts to come to us. So far it’s proven effective enough, because we are actually now under negotiations with a label. But more on that later when there’s something to announce…

What kind of constructive feelings do you put in your music?

…Hmm, didn’t really get the question ![]()

Hah, let me try again… Look, heavy sludgy music has a kind of destructive vibe. It’s okay for you and me somehow, but sometimes I talk about such music with people unfamiliar with metal and they determine that it is as “destructive”. So do you see in the music a kind of… mmm… spiritual content maybe…

I wouldn’t say there’s deep spiritual content in Slug Lord. We end up using stuff that all of us can relate to; heavily intimate content washes off easily especially when lyrics are worked on together. But we do have a mutual vision of emotions that we want the music to bring up in you, and indeed someone could perceive them as unpleasant. It’s a mix between impending despair and alluring groove.

J., Slug Lord is based in Tampere and it’s the most populous inland city in any of the Northern countries. What would you advice to visit if any of our readers go there?

One place worth mentioning is our local pub and venue Varjobaari. It’s a small pub and in the outskirts of the town, but a most valuable meeting place for the local doom & psychedelic scene and holds frequent gigs for tons of interesting underground bands.

Okay, but what sorts of local beer can you recommend? I have tasted Koff, Karhu, Sandels… Karjala… The last one was not bad, but indeed I would prefer German Schneider. I need to know what I should lay my hands upon the next time I visit Finland ![]()

Yeah, all those bulk lagers are popular in Finland. But the microbrewery scene is starting to get some commercial recognition and is growing rapidly. Our bassist, who has in recent years involved himself deeply in the beer gastronomy, suggested breweries like Hiisi, Pyynikin käsityöläispanimo, and Stadin panimo, if you can find their products.

There’s a museum of Tove Jansson in Tampere. How often do you pilgrimage to this sacred place and how do you like the Moomin family?

Nothing wrong with the Moomins. The original books and comics have some quite surprisingly crazy bits with drug use, making moonshine, and generally a melancholic atmosphere with some dark humour. You should check them out.

I need to go and read some of their apocalyptic stories again right now! Thank you for your time J.! Let us finish the interview on this note! God speed to Slug Lord!

Thank you!

https://www.facebook.com/sluglord

Photos by Jouni Parkku

TertiarymattJust so we're clear, that's a gorilla Dracula using a coffin to sword fight an Irish Ninja Doctor.

27p56 is a post from: The Adventures of Dr. McNinja

| Ads by Project Wonderful! Your ad could be here, right now. |

TertiarymattShould maybe read this?

Into the Forest

by Jean Hegland

1996, Dial Press

Recommended? Yes.

I was lying in bed sick.

“Hey,” I said to my friend, “what book should I read?”

“Have you read Into the Forest?” he asked.

“No,” I said.

“Read that,” he said. “Post-apocalypse.”

“Is it going to be like The Road?” I asked. I was sick. I didn’t want to read something as doom and gloom as The Road.

“Not really,” he said.

I’m glad I decided to believe him, even if I’m not sure he was telling the truth.

Nell and Eva are two teenage sisters, homeschooled in Northern California. Their mother dies of cancer a year before the power and telephones begin to fail, and soon the girls’ tiny world just shrinks and shrinks.

Into the Forest is a post-apocalyptic story unlike any other I’ve read. My usual preference is for huge sweeping sagas of reformed societies and shantytowns, or the epic adventures of a roaming band of misfits who just want to survive. You know, classic post-apocalyptic stuff. Into the Forest isn’t that. It’s an intimate portrait of a family. It’s about coming of age in a society that is, slowly and surely, disintegrating. It’s a book about death and love and it’s a book about the forest.

If you want the spoiler-free review, it’s as simple as what lies above: this is a damn good book and worth reading. (Which is to say, there are some spoilers ahead.)

read the rest at anarchogeekreview.com

TertiarymattSome really good stuff in here.

100-year-old beggar celebrated as living saint in Bulgaria Agence France-Press

Mt. Gox founder helps (briefly) tank another crypto-currency Pando

Mouthbreathing Machiavellis Dream Of A Silicon Reich Baffler (Barry Ritholtz). OMG, some people are taking Moldbug seriously? I looked at some of his stuff years ago and concluded the pretentiousness to content ratio was seriously out of line (aside from not being too keen about where most of his arguments led….)

German Court Rules That You Can’t Keep Compromising Photos After a Break-Up Slashdot

Nascent El Nino threatens to leave some Asian economies parched Nikkei

China clamps down on US consulting groups Financial Times

Chinese fighters fly close to SDF planes above E. China Sea Nikkei

France and Europe: Shocks Ahead Economist

Fatal shooting at Jewish Museum in Brussels Financial Times

Voters do walk of shame Daily Mash

Ukraine

Ukrainians vote for new president BBC

Ukraine vote could highlight a generational divide Washington Post

Putin Plays Down Cold War Threat as Ukraine Tensions Rise Bloomberg

The Russia China Axis continues to form Ian Welsh

Ukraine: Major “Western” Think Tank Admits Defeat Moon of Alabama

Big Brother is Watching You Watch

‘Smart pills’: A revolution in medicine, or a troubling invasion of privacy? Washington Post

The NSA is capturing nearly every phone call in Afghanistan, WikiLeaks claim NSA

The year of living more dangerously: Obama’s drone speech was a sham Guardian

VA says more veterans may use private medical services Los Angeles Times

Which Working Families Party? Jacobin

Are Mortgage Credit Conditions “Tight”? Michael Shedlock

U.S. Retailers Missing Estimates by Most in 13 Years Bloomberg

Buying Insurance Against Climate Change Robert Shiller, New York Times. Lordie, this is what traders call “wrong way risk” that if the insured-against event comes to pass, there will be so much other Bad Stuff going on that the insurers will be unable to pay out. Credit default swaps written against subprime debt was a classic example.

FT v. Piketty

My view on Piketty’s critique by the FT Branko Milanovic (larry)

Is Piketty All Wrong? Paul Krugman

Stress Test: The Indictment of Timothy Geithner Dean Baker, Firedoglake

Class Warfare

Sheryl Sandberg and Harvard’s Housekeepers Jacobin

The Economics of Contempt CounterPunch

A Point of View: Happiness and disability BBC

Antidote du jour. This is OIFVet’s Eva:

TertiarymattI love seeing things rendered in this style.

I have never seen this! Seen Bayuex Tapestry parodies, but not as commentary during an actual war.

Anyone in the political or public relations game knows that the best way to make a disclosure but minimize its impact is to do so on day before the long holiday weekend.

If the government had the ability to make an announcement they’d rather not make during a major holiday break, they would. And the New York Times, which does have that luxury, looks to have done precisely that with an important article on private equity fee abuses by Pulitzer Prize winning reporter Gretchen Morgenson. As we’ll see shortly, this isn’t one of her 1000 or so word weekly “Fair Game” columns; this is substantial piece of original reporting discussing several types of private equity fee abuses.

So why would the Grey Lady bury an important article by running it on long weekend? Oh, and worse, that has anodyne headline, “The Deal’s Done. But Not the Fees,” which doesn’t flag who the perps are? One has to assume that the Times isn’t too keen about rocking the boat with powerful financiers, particularly since the incoming New York Times editor, Dean Baquet, who has a track record of avoiding controversial reporting. In addition, former Lehman Brothers partner and art world denizen Michael M. Thomas dates the beginning of the end of the New York Times as a journalistic institution from when Punch Sulzberger joined the board of the Metropolitan Museum. As Thomas remarked, “He needed to be dining with people he should be dining on.”

Make no bones about it, the Morgenson story, which comes on the heels of a Wall Street Journal exposing industry leader KKR’s far too clever and potentially impermissible dealings with its house consulting firm, KKR Capstone, discloses important new fee abuses, including getting paid for services never rendered.

One of the things that the broader public may not realize is that the normally complacent investors in these funds, known as limited partners, have been pushing back against the fees charged to them by the private equity firms, who in industry parlance are called general partners. Thus this fee chicanery is particularly important because it reveals a concerted effort by the general partners to out-fox the limited partners and continue to extract more in rents from the limited partners than they think is warranted and thought they had agreed to pay. It’s an up-market version of Elizabeth Warren’s famed “tricks and traps.” . From the Morgenson story:

“In some instances, investors’ pockets are being picked,” Andrew J. Bowden, director of the S.E.C.’s office of compliance inspections and examinations, said in a recent interview. “These investors may be sophisticated and they may be capable of protecting themselves, but much of what we’re uncovering is undetectable by even the most sophisticated investor.”

Actually, what Bowden is suggesting is worse than Warren’s objections to sneaky hidden terms in impenetrable consumer contracts. While Bowden says that the general partners are waging a successful document/deal structuring complexity war against limited partners, his “pockets are being picked” suggests the SEC is also seeing cases of flat-out embezzlement.