Generally speaking, you pick an image for your desktop so that it looks good. But what if you can have a nice aesthetic and some helpful information? These infographic wallpapers should do the trick.

|

Generally speaking, you pick an image for your desktop so that it looks good. But what if you can have a nice aesthetic and some helpful information? These infographic wallpapers should do the trick.

|

|

Lots of different sounds can make you more productive while you work or study (particularly music you're not familiar with ), but video game soundtracks might be the best option of them all if you need to concentrate.

|

|

Since a car is one of the biggest purchases you'll ever make, you'll want to carefully weigh how much you spend on it. The Money Under 30 blog offers a few rules of thumb for what percentage of your income to budget for your next car.

|

|

We all want to raise happy and healthy kids, but sometimes it's harder than it sounds. This infographic takes a look at the studies behind what really affects kids' happiness and well-being.

|

|

Not too long ago, I jumped ship on an office job and career that was great, but not my passion. I took a huge risk to follow my dream, and learned a lot of lessons along the way. If you're thinking about following your dream or doing what you love, here are some tips to keep in mind before you do it, and some of my mistakes to learn from.

|

|

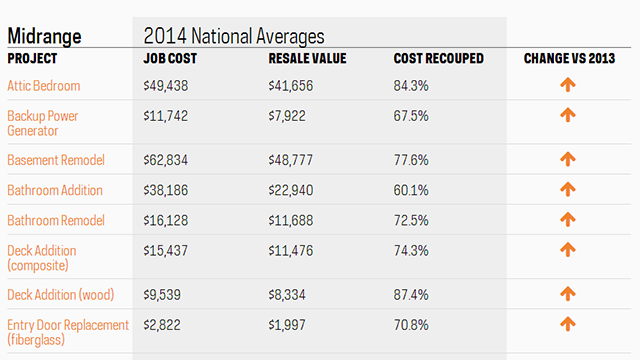

When it comes to adding on to your home or making a few renovations, it's easy to assume that whatever you invest in a remodel will get recouped on your home's value. This is not necessarily the case. Remodeling Magazine has some stats on which ones are most worth the investment, though.

|

|

I typically don't like to get involved in religious debates, but I find the current green juice frenzy way too amusing to resist throwing in my own $0.02. You would have to be living in a Wi-Fi-less cave to have not noticed the incredibly vocal community who believes juicing is the panacea of all that is good and healthy on earth.

|

|

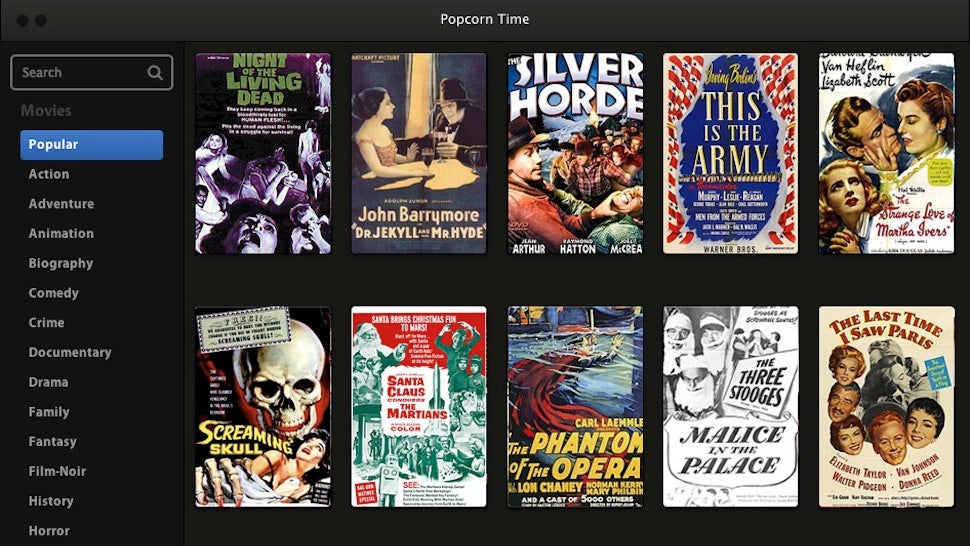

Windows/OS X/Linux: Popcorn Time is a free, open-source tool for browsing, downloading, and watching movies. Browse the app's huge collection of movies and documentaries, pick one, and click play. The app torrents the movie, starts playing it immediately, and streams it while the download finishes in the background.

|

|

The unending rivalry between dogs and cats won't end today, but thanks to your debate we're going to at least find out which pet bests the other in a variety of categories. Here are your best arguments.

|

|

Whether it's served in a demitasse mug or a venti mochachino bucket, coffee is an essential, eye-opening morning ritual for many of us. But at what point does throwing back another vente doing you more harm than good?

|

|

The millennial generation is roughly defined as “people born between 1980 and 2000.” While it’s impossible to generalize about everyone born in a twenty-year span, especially when the older cohort didn’t even get mobile phones until they were legal adults. Experts have noticed broad trends, though: even when they are gainfully employed and can afford them, millennials are less interested in owning cars and houses than prior generations were at the same age.

That must have companies that run suburban big boxes like Costco stores worried. In a recent conference call, Costco CFO Richard Galanti told analysts that the retailer is looking to expand its offerings of organic foods and trying delivery.

Do those stereotypical giant packs of toilet paper appeal to young adults who are frugal, but don’t have the expansive basements and garages that they might have grown up with in the suburbs? In the coming decades, Costco will find out, and might change

Does Costco have a youth problem? [RetailWire] (via Time)

Out of the family members who shared the pizza, two became ill. “It was a like a rush, sweating, heart beating real fast,” the grandmother told TV station CBS2. Her grandson’s symptoms were different, and even more alarming: he says that he felt “dizzy” and “crazy,” and his grandmother reports that he “ran out the door butt naked.”

At the hospital, the grandmother and grandson both tested positive for marijuana intoxication, but insist that they weren’t exposed to the drug at home. They blame the mushrooms on the pizza. Why? The other two people who ate the pizza, two other grandchildren, had picked the mushrooms off their slices and didn’t eat them.

The restaurant owner says that the family’s allegations are impossible. “No, that’s incredible, because nobody smokes marijuana right here,” he told the TV station.

The family filed a police report. We’ll let you know the results of any investigation when we find out.

Only On CBS2: South LA Family Claims Pizza Shop Served Them Pot On Their Pie [CBS2/KCAL9]

For more than a year, some have accused nutritional supplement company Herbalife of operating a pyramid scheme and called for federal authorities to investigate the business. Today, the company confirmed that it is indeed under investigation by the Federal Trade Commission, though it did not reveal exactly why.

For more than a year, some have accused nutritional supplement company Herbalife of operating a pyramid scheme and called for federal authorities to investigate the business. Today, the company confirmed that it is indeed under investigation by the Federal Trade Commission, though it did not reveal exactly why.

In a statement released to the press, Herbalife confirmed that it received a Civil Investigative Demand from the FTC earlier today.

Without going into the nature of the investigation, the company said it “welcomes the inquiry given the tremendous amount of misinformation in the marketplace,” and that it will cooperate fully with the FTC.

“We are confident that Herbalife is in compliance with all applicable laws and regulations,” continues the statement. “Herbalife is a financially strong and successful company, having created meaningful value for shareholders, significant opportunities for distributors and positively impacted the lives and health of its consumers for over 34 years.”

This record [PDF] released by the FTC in 2013 includes 100 Herbalife-related complaints filed with the agency.

A number of the complaints involve Herbalife’s multi-level marketing business model, which sells the supplements through a network of independent distributors, who then sell the products and make money with those sales, as well as getting commissions from other people they set up in the business.

While some, including hedge fund manager Peter Ackworth at Pershing Square Capital, the one who has most directly attacked the company, say this is a pyramid scheme that only enriches those at the top, the company has previously defended itself saying its business model is used by others without facing similar accusations.

“Girl Scouts sell cookies on a direct-selling method, and nobody attacks them,” said CEO Michael O. Johnson in 2013.

(YouTube)

Something about the prospective buyer’s message didn’t sit right with Mark, which is why he contacted Consumerist in the first place. He explained that he’s moving, and listed his used dehumidifier on Craigslist for $100. That’s about half what he paid for it.

“I received a baffling message that appears to be a scam, but I can’t seem to figure out how it works,” he wrote to Consumerist. The buyer wanted to buy Mark’s appliance, but didn’t want the whole appliance. He just wanted the sticker with the serial number, along with the cord.

Here’s his correspondent’s original message, spelling errors intact:

I will give you full price , but I need you after I pay to cut the cord 6 inches from the plug and scrape off the factory sticker and place it on gloss photo paper and put it in a bubble wrap insides manilla envelop and I will give $10 more for shipping through USPS and send it to me at [out of state address]. You can keep the unit.

Keeping the unit isn’t all that useful without the electric plug, but Mark could send it for recycling and wouldn’t need to pack it up to ship. What a great deal! But what would the other party get out of it? This didn’t sit right with Mark, which is why he wrote to us.

Mark must have missed our coverage of the Great Flaming Dehumidifier Recall. It’s easy to see how: Gree Electric Appliances made the appliances for brands ranging from GE to Kenmore to Frigidaire, adding brands and models along the way.

Mark was selling his dehumidifier for $100, but bought it new for closer to $200. While the refund from the manufacturer won’t cover the whole replacement cost of a new unit, something that irked many of our readers, it means that if Mark went along with this scheme, the scammer would make around $90 for not doing anything.

Since it is technically illegal to re-sell a recalled appliance, maybe this recall flipper is doing the used-appliance buyers of America a favor. Not so much with the used appliance sellers of the world, though, and this scheme definitely isn’t fair to manufacturers running recalls.

For some time now, we at Consumerist have been worried about Target, since the retailer’s pricing shows little to no grounding in reality. Now the disease has spread to Safeway, maybe. Reader David is still scratching his head over this shelf tag that he found last week.

He provides the wacky backstory: the limit on these “club price” bottles has varied over the last few weeks. First, it was “minimum 4,” then “limit 4.” Now there’s a limit of one, but you have to buy four to get a gas discount. Wha?

“The same product was also on an endcap, but there it was still marked as ‘limit 4,’” David writes. Oh. Okay. Why is there a limit of only one bottle of soda? THIS IS AMERICA!

At least we can explain that four-bottle minimum at the bottom: those can be any product for the gas discount, mix and match.

Each year, state legislators around the country introduce, debate, and even pass a number of bills claiming to better serve consumers who need help with short-term, low-value loans.

CURRENT ACTIONS

States such as Missouri and Utah are currently discussing the merits of such reform bills. The Missouri Senate approved SB 694, which bans rollovers, requires lender to offer an extended payment plan and removes a current interest and fee cap of 75%. The Missouri House is currently reviewing the bill.

The Utah House and Senate passed HB 127, which modifies the reporting requirements for deferred deposit lenders, requires lenders to file any lawsuits where borrowers live or obtained the loan and requires lenders do minimal checking to see if borrowers can afford loans. The bill is now waiting for the governor’s signature.

Marketed as a way to relieve consumers of the payday lending debt trap, reform bills generally include some of the following provisions:

Sen. Mike Cunningham, who sponsored the Missouri bill mentioned above, says it will protect consumers from some of the practices payday lenders have utilized for so long.

Missouri’s proposed reform comes less than two years after a group called Missourians for Equal Credit Opportunity helped put an end to a ballot initiative that would have allowed Missouri residents to vote for or against capping the state’s interest rate at 36%.

The current proposed bill does not feature any kind of rate cap, meaning interest for a typical two-week payday loan can balloon to more than 1,000%. Had the ballot initiative gone forward and passed, the cap of 36% would fall in line with what consumer advocates deem to be a reasonable rate for consumers to repay without falling into the debt trap.

“This is a positive, carefully crafted step toward consumer protection,” Rep. Jim Dunnigan, who sponsored the Utah reform bill, tells The Salt Lake Tribune.

“This is a positive, carefully crafted step toward consumer protection,” Rep. Jim Dunnigan, who sponsored the Utah reform bill, tells The Salt Lake Tribune.

Utah has a rather colorful history with the payday lending industry. The current reform bill grew out of scandals involving the industry and former Utah Attorney General John Swallow.

Recently, a Utah House Special Investigative Committee found that in 2012, Swallow funneled thousands of dollars he received from the payday industry in hard-to-trace ways in order to defeat a former representative who had pushed for reform of the often predatory loans.

NOT PASSING MUSTER

On the surface the bills seem to have the best interest of consumers at heart, but some consumer advocates claim these reforms are not as helpful as lawmakers would like people to believe.

“Provisions such as these are simply smoke and mirror provisions that allow the predatory debt trap to continue to harm consumers pay-day after pay-day,” says Diane Standaert, senior legal counsel for the Center for Responsible Lending.

In fact, when creating the Military Lending Act, which protects members of the military from predatory loans, the U.S. Department of Defense looked at a variety of provisions enacted by states to reign in payday lending.

In a report to Congress, the DOD concluded that even with all these “consumer bells and whistles,” the reforms do not stop the debt trap perpetrated by payday loans.

WHERE THERE’S A DEBT, THERE’S A WAY

For instance, provisions such as the rollover ban in the proposed Missouri law do nothing to protect consumers from predatory lending practices, Standaert says.

Lenders could easily circumvent the rollover ban by allowing consumers to repay their existing loan and immediately take out another. Similarly, the cooling-off period – a requirement that a borrower wait a set amount of time before taking out another payday loan – does little. Consumers can just take their business to another area lender or wait the typical 24 hours and take out a second loan.

For example, under Florida’s payday reform law, borrowers are limited to one outstanding loan at a time, may not roll over a loan and must wait 24 hours after paying off a loan before taking out another.

Despite the provisions, a 2007 Center for Responsible Lending study, “Springing The Debt Trap” [PDF], found that 63% of Florida payday loans go to borrowers with 12 or more loans per year, and 85% go to borrowers with seven or more loans per year. Additionally, 45% of new loans were taken out a day after previous loans were paid off and 88% of new loans were taken out in the same two-week pay period that a previous loan was paid off.

Determining the amount a consumer can borrow based on their monthly income, as proposed in the Utah reform, may seem reasonable, but advocates say the lack of underwriting used in the payday industry does nothing to prevent consumers from being on the hook for more than they can actually pay.

“A lot of times provisions that payday lenders promote, such as the ability to pay, is looking at borrowers gross monthly income,” Standaert says. “In practice, the provision means the loan principle can actually account for 50% of a borrower’s bi-monthly paycheck. With fees and interest tacked on, it could be even higher.”

OTHER OBLIGATIONS

Additionally, the provision fails to account for the borrower’s other obligations, such as mortgage or rental payments, medical bills, or credit card payments. As such, a borrower could owe more than 50% of their bi-weekly pay to the payday lender and cannot afford to both repay the loan and meet other obligations. Because payday lenders generally have access to a customer’s bank account, they are first in line to be repaid when a paycheck clears.

Suzanne Martindale, a staff attorney with Consumers Union, says the ability to pay provision of the Utah bill is rather weak and written in a way that makes it easy for lenders to find ways around it. A true debt-to-finance analysis requirement would ensure that consumers are only borrowing what they can reasonably pay back.

“That’s something that federal regulators have provided guidance over for banks that facilitate these types of loans,” Martindale says. “Direct Advance has gone out the window because of regulations that look at ability to pay.”

Under new federal regulations banks were tasked with determining a consumers ability to pay, rather than just requiring a borrower to flash a pay-stub.

JUST GIVE ME SOME MORE TIME

Because an average borrower is in debt for approximately 200 days of the year, it makes sense that reform bills would consider a way for consumers to more easily pay off their debt.

The inclusion of an Extended Pay Plan in the proposed Missouri bill means that borrowers would have up to 120 days to pay off their loan. The payment plans are based off of the consumers’ pay periods and no interest or fees are charged during the EPP. However, borrowers would only be eligible for the extended plan once a year.

While the extended plan could offer a bit of relief for consumers, advocates say, it ignores the fact that payday loans thrive off of repeat customers.

Last year, a Consumer Financial Protection Bureau white paper [PDF] found that over the course of 12 months, more than one-third of borrowers will take out between 11 and 19 payday loans. Fourteen percent of borrowers will take out 20 or more payday loans within this same time period.

KEEPING THE CAP IN PLACE

Perhaps most alarming to consumer advocates is a provision in the Missouri bill that would remove the current law that caps interest and fees at 75% of the loan’s original principal, which translates to an annual interest rate of 1,950%.

“They have a pretty high fee cap to begin with, but now if they are repealing it, who knows what they would charge,” Martindale says.

The current rate cap in Missouri has done little to help consumers. Last year, Consumerist reported on a woman who took out a 26-month installment loan of $1,000 in 2008. After failing to repay the loan her debt ballooned into $40,000 because of fees and an interest rate of 240% imposed by the lender.

So, what will create meaningful reform for payday lending? A rate cap around 36%, consumer advocates say.

North Carolina, for example, once authorized payday lending by exempting payday lenders from its 36% rate cap, the law included a four-year sunset provision for lawmakers to reevaluate the industry effects on consumers before reauthorizing the practice. After seeing the documented debt trap, state legislatures decided not to continue with the exemption.

The 2007 CRL report found that after enforcing the interest rate cap, North Carolina saved $153 million.

“Following the enforcement of the usury law, borrowers reported being better off and glad to no longer have the product that looked easy to get into and in reality was hard to get out of,” Standaert says.

An interest cap would also be in line with the Military Lending Act, which effectively forbids the offering of payday and auto-title loans to active-duty service members by capping interest rates on all affected loans at 36%.

THE FINAL DAYS OF PAYDAY?

It’s important to remember, Standaert says, that since 2005 no state has passed a law that would legalize the 300% APR payday loan product – since that time a number of states have rolled authority back and enacted provisions such as rate caps to limit the debt trap.

Martindale, with Consumers Union, says the solution for ending predatory payday lending rests in the hands of the CFPB who has authority over payday lenders.

“We’re waiting to see what they are going to do as far as issuing regulations over small payday loans,” she said. “We could have federal standards soon.”

In the meantime, states will continue to discuss and perhaps implement reforms full of “bells and whistles,” and only pay lip service to the notion of real reform.

There are apparently three pizza places in Barrow, AK, the northernmost city in the U.S.

The Wall Street Journal has the story of the 25-year-old co-owner of a pizza place in Barrow, Alaska, that actually specializes in making deliveries.

Here are a few of the tidbits we learned about life north of the Arctic Circle.

1. The Busiest Season Is Winter

While you might hesitate to order in when the temperature drops below freezing, the driver says the coldest months are his prime time “because nobody wants to go outside” when the temperatures sink to minus-40 Fahrenheit. “At certain times, it’s normal to see a polar bear in the middle of the street.” We’re guessing they aren’t as cuddly as the ones you see in the Coca-Cola ads.

2. Gas Is Expensive, But He’s Got To Keep The Car Running

The driver says gas in Barrow costs more than $6/gallon, but he’s got to run the car for an hour in the morning — and that’s after he unplugs the engine block warmer — and keep the car running all day.

“If I turn it off for 10 minutes, it would freeze and die,” he writes.

He also has to use a heater to keep the inside of the car warm all day and night, otherwise the windows will crack.

3. Layers, layers, layers

“When delivering, I wear huge boots, three pairs of specially-made Eskimo socks, two pairs of pants, three hoodies, and a very big jacket,” explains the young man, who says his Hyundai Accent gets stuck somewhere every day during the winter.

If we can prevent or decrease the pain of arthritis with a relatively inexpensive supplement, why shouldn’t we? Americans spent an estimated $813 million on glucosamine and chondroitin sulfate supplements for ourselves and for our pets in 2012, despite the lack of evidence that it is at all helpful to prevent or alleviate arthritis. Now another study shows that the supplements don’t really help, and may actually do the opposite of what they’re supposed to.

If we can prevent or decrease the pain of arthritis with a relatively inexpensive supplement, why shouldn’t we? Americans spent an estimated $813 million on glucosamine and chondroitin sulfate supplements for ourselves and for our pets in 2012, despite the lack of evidence that it is at all helpful to prevent or alleviate arthritis. Now another study shows that the supplements don’t really help, and may actually do the opposite of what they’re supposed to.

We’ve been discussing this for years. The logic of “well, it can’t hurt” can actually hurt you. Glucosamine and chondroitin supplements have been shown to interfere with some blood-thinning medications. This study, published in the latest issue of the journal Arthritis & Rheumatology, shows something even worse. Bone marrow lesions are thought to worsen arthritis pain, and participants who took the supplements actually had more of them than participants in the control group. Since there were only a few hundred people in the study, this is far from definitive, but it’s not a sign that you should rush out and buy a new bottle of glucosamine, either.

The theory behind taking the supplements makes sense, and some very early studies showed that it worked. They consist of supplements that form the building blocks of cartilage. Therefore, if arthritis is what happens when cartilage deteriorates, putting more of those substances in the body would make cartilage last longer, rebuild it, or … something. The theory was nice, but further studies have showed that the supplements don’t actually help.

Glucosamine Fails to Prevent Deterioration of Knee Cartilage, Decrease Pain [Arthritis & Rheumatology]

One more reason to skip glucosamine for your knee pain [Consumer Reports]

An onlooker snapped this exclusive photograph of the crime scene.

The Belleville News-Democrat reports that two men — ages 17 and 25 — stole cash (and, for the sake of our inner child, we’re going to believe they also made off with a tray of burgers) from a McDonald’s in Cahokia, IL, just across the river from St. Louis.

The hamburglars then led police on a high-speed chase into the nearby town of Centreville, where they promptly ran into the car of Centreville Mayor Marius “McCheese” Jackson, who sadly does not have a massive cheeseburger head or strut around town wearing a “Mayor” sash.

The mayor was taken to the hospital, but luckily he did not leak too much ketchup.

The suspects were apprehended after the crash and the stolen money was recovered, though there’s no mention of that tray of burgers we completely made up earlier.

You might look at a bottle of laundry detergent and idly wonder whether the bottle really contains 96 loads’ worth of soap. Then you probably keep on using the soap and forget that you ever questioned the wisdom of the label. Fortunately, our clean and fresh colleagues over at Consumer Reports have a calculator and a mission to save us all from inaccurate dosing caps.

You might look at a bottle of laundry detergent and idly wonder whether the bottle really contains 96 loads’ worth of soap. Then you probably keep on using the soap and forget that you ever questioned the wisdom of the label. Fortunately, our clean and fresh colleagues over at Consumer Reports have a calculator and a mission to save us all from inaccurate dosing caps.

Target’s house brand for household products, Up & Up, put out a nice, big 150-ounce bottle of their liquid detergent. The claim that this is enough detergent for 96 loads, and the instructions tell customers to fill it up to the clearly marked fourth line in the cap.

The problem is that the math is wrong, or at least a little bit misleading: filling the cap to that fourth mark gets you 70 capfuls of detergent total, not 96. It’s not news to Consumerist readers that Target has occasional problems with math, so Consumer Reports contacted the company to let them know about the discrepancy.

It turns out this wasn’t a math error, but a laundry error. See, you’re not supposed to fill the cap up all the way most of the time: a regular load of laundry goes up to maybe the second line on the cap. The fourth line, presumably, is for loads of extra-dirty clothing.

Target plans to “promptly” correct the instructions on bottles – whether this means they’ll put stickers on the bottles already on shelves will be interesting to see.

Target fixes dosing directions on Up & Up detergent [Consumer Reports]

NBC4 Washington |

2 Dead, Car Burst Info Flames During Crash PotomacLocal.com PRINCE WILLIAM COUNTY, Va. – Two people were killed and three injured early Sunday morning in a car crash in Prince William County. Police said a Honda Civic was making a left turn from Va. 234 onto Minnieville Road when it crossed the path of a GMC ... Police: Teens Busted in Failed Marijuana HeistPatch.com 2 killed in crash in Prince William County, Va.WVVA TV all 64 news articles » |