Turning Services Into Experiences

Financial planning, when it’s done right, is a pretty amazing experience. A prospective client comes to see you in the belief they’ve simply got a pension or investment problem, and ends up (a few weeks or months later) with a plan that’s changed their life and their relationship to money.

When it all goes well, it’s a process you could call transformative. But let’s be honest – not every interaction is like that.

The rise of the experience economy

In their 1999 book The Experience Economy, Joseph Pine II and James Gilmore predicted a new age of consumer behaviour and consumption; a move away from goods and services towards experiences, ultimately towards those that are truly transformative.

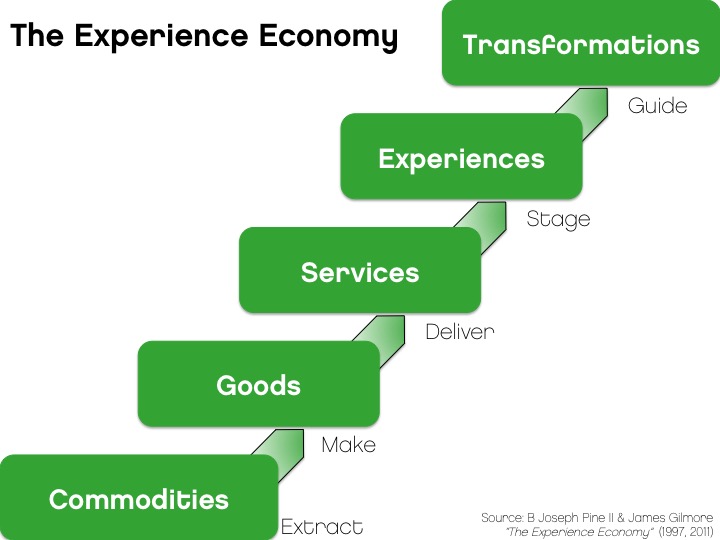

Take a look at their diagram below:

Think of some of the top ‘client experience’ brands, like Apple or Disney; or themed restaurants like the Hard Rock Cafe. They’ve taken a simple task or service (buying a computer or a meal), and turned it into a memorable experience. When you return home from a visit to the Hard Rock Cafe you don’t talk about the quality of your hamburger. You talk about the memorabilia, and the memories evoked by some of the guitars or the artists they were attached to. It’s powerful stuff.

Financial planning as an experience

You only need to look at our profession to see Pine and Gilmore’s ideas over the last century borne out in practice:

- Money was originally a means of exchange (commodity)

- The managed fund was developed (goods)

- Advisers were introduced into the distribution chain (service)

The final two steps aren’t always achieved, but when financial planning is done well, it changes the process into an experience, and in some cases a transformative one.

“The experience revolution will help people be happier by nudging them to spend less time and money on having things, and more of their time and money doing things.”

James Wallman,

Stuffocation: Living More With Less

Once you understand how transformative financial planning can be for some clients, you can’t stop yourself from thinking about how you might institutionalise that type of experience. The truth is for most firms it isn’t always repeatable. But the great firms are thinking long and hard about how to make financial planning repeatedly transformative.

Recently, Abraham Okusanya shared with us his positive spin on the emergence of robo-advice. His point was that many of the repetitive tasks in the financial planning process could and should be done by robots (or computer systems), not people. I concur with his view.

However there is disruption on the way from technology. When the various parts of our value chain are broken down and stripped out as separate services, they will return to being merely a commodity, which will see them valued as such too; priced very cheaply, or free.

The real threat for financial planning businesses will be in failing to create a combined, complete and transformative client experience. If you allow clients to buy the component parts of what you do, then it’s a race to the bottom. If you instead focus on delivering lifestyle outcomes for clients (helping them to ‘live more’), then there is the opportunity to stay relevant, appreciated and profitable for the long term.

Pine and Gilmore argued in their book that businesses need to create memorable events for their customers, and that memory itself then becomes the product — the ‘experience’. They also believed that more advanced ‘experience’ businesses can begin charging for the value of the ‘transformation’ that their experience offers. In 2015, I believe this is financial planning.

Making it conscious

Most financial planning firms have progressed from commodity, to product, to service – which is great. The next level is creating that client experience – doing a good financial planning job while making the process fun and enjoyable for clients. I’ve worked with a few firms in recent years who have grappled with that issue.

The final and ultimate level is transformation, while nirvana is institutionalising that transformation so that it’s not something you do every month or so, but something you do consistently – being aware of what you are doing and doing it on purpose.

Price vs value

Personally, I’m hesitant to get on the price reduction train that seems to be gathering steam, and you should be too. The only way to avoid pricing pressure is to be deliberate in the experience you create for clients.

Think about things that financial planners have not typically considered before. What would help make your clients’ experience fun, fabulous and life changing? Many of the component parts are already in place (great questions, interactive technology), yet there are too many elements that have been designed by an unhealthy fear of compliance. These ruin the experience of many clients, so consider how you can effectively balance the client experience with compliance requirements.

Our greatest challenge as a profession is to create something memorable.

This is what the leaders are working on right now. Are you?

The great firms are thinking long and hard about how to make financial planning repeatedly transformative.

The great firms are thinking long and hard about how to make financial planning repeatedly transformative.