×You need to sign in to continue.

Shared posts

04 Jun 13:20

Partisan Bias Diminishes When Partisans Pay

by Alex Tabarrok

In November of last year I wrote:

Overall, I am for betting because I am against bullshit. Bullshit is polluting our discourse and drowning the facts. A bet costs the bullshitter more than the non-bullshitter so the willingness to bet signals honest belief. A bet is a tax on bullshit; and it is a just tax, tribute paid by the bullshitters to those with genuine knowledge.

A recent paper provides evidence. It’s well known that Democrats and Republicans give different answers to even basic factual questions when those questions are politically loaded (Did inflation fall under Reagan? Were WMDs found in Iraq? and so forth). But do the respondents really believe their answers or are they simply signalling their affiliations? In other words, are respondents bullshitting? In a new paper, Bullock, Gerber, Huber and Hill provide evidence that the respondents don’t actually believe what they say and the authors do so by making partisans pay for their beliefs. Dylan Matthews at Wonkblog has a good writeup:

They ran two experiments. In the first, they split respondents into two groups: Those in the control group were asked basic factual questions about politics; those in the treatment group were asked the same questions but were entered into a raffle for an Amazon gift card wherein their chances depended on how many questions they got right.

In the control group, the authors find what Bartels, Nyhan and Reifler found: There are big partisan gaps in the accuracy of responses.

…But when there was money on the line, the size of the gaps shrank by 55 percent. The researchers ran another experiment, in which they increased the odds of winning for those who answered the questions correctly but also offered a smaller reward to those who answered “don’t know” rather than answering falsely. The partisan gaps narrowed by 80 percent.

The paper also has implications for democracy. Voting is just another survey without individual consequence so voting encourages expressions of rational irrationality and it’s no surprise why democracies choose bad policies.

Hat tip: @jneeley78.

31 May 21:05

"The Nail" Encapsulates Every Dumb Thing About Relationship Arguments

Joswald1, Zerinsakech and one other like this

30 May 15:34

Outsourcing markets in everything

by Tyler Cowen

If you live in India, you can now get a job staring at a monitor that displays images of American doctors entering hospital rooms thousands of miles away. Your task is to sound an alarm if the doctor fails to wash his hands.

This may sound disturbingly similar to being an auditor for the telephone handset sanitizers guild, but in practice it turns out to be very effective. It also turns out that this Big Brotherish technology has gotten a big boost from the passage of Obamacare.

That is from Kevin Drum.

Joswald1 and -1 others like this

29 May 20:19

The Case For Fishing Regulation

by Joshua Hedlund

I read a book by Callum Roberts called The Ocean of Life: The Fate of Man and the Sea. I read it because I’m not afraid of facts that might support positions I oppose, even though it’s basically an environmentalist tome about how we’re destroying the ocean through overfishing, climate change, chemical pollution, plastic dumping, habitat destruction, invasive species, noisy ships, and a few other things I don’t remember. It’s almost enough to make you wonder how the ocean is still around, tempting you to believe in what the theologians call “common grace.”

These things don’t “keep me up at night” or “scare the pants off me” like they do the author, partly because I suspect some of those bad things cancel out, partly because I have more faith in the general size and resilience of the ocean, and partly because I have more faith in the ability of markets to respond to incentives to reverse and preserve it (and partly I suppose because of more faith in common grace).

But I found the chapter on overfishing very interesting. I had stumbled on info about overfishing in the past, but I had never seen the case presented so starkly and fully. Apparently we’ve been removing fish from the ocean so much faster than they’re being replaced that it’s starting to show pretty badly; despite all the huge advances in technology and productivity in the last hundred-plus years we’re catching far fewer numbers of a whole bunch of species simply because there’s so few of them left.

To catch the most fish in the long run, you should catch at a rate no quicker than the fish are replenished. Even though it might be easy to catch twice as many fish in one year, if you fish at that rate for too long, you are “depleting” the “fish stocks.” There won’t be as many fish left to reproduce next year, and you’ll have fewer fish to catch in the future – killing the proverbial goose that laid the golden egg.

But even if you’re smart enough to leave some easy fish alone this year as an investment that will pay off later, you don’t own the ocean, and you can’t really stop someone else from coming along to take extra fish now for greater short-term profits – even though it diminishes the long-term profits for everyone who’s trying to save those short-term profits for later.

This is a sort of market failure that economists call the “tragedy of the commons,” and I think it’s a reasonable case for some sort of government regulation – perhaps in the form of limits on how many fish are caught each year. There are apparently cases of governments doing that sort of thing and seeing some sorts of successes.

Part of the problem is that no one really owns the ocean, which is hard to do anyway because the water’s always moving, so it’s harder to have the property rights that give people the incentive to consider long-term profits over short-term profits. Callum’s book does mention some government efforts to establish private ownership in the fishing industry, and he hinted at its success, though he expressed skepticism at its broader potential. (I’m a little more biased to be optimistic that it could work quite well, but I doubt it’s a workable solution for the whole ocean.)

I can imagine a self-correcting fish market that would not require government intervention. As depleted fish get harder to find (it’s very hard to kill off all of them), their price goes up until demand drops, allowing the stocks to be replenished until they are plentiful enough to be caught again at a lower price. But the market has produced innovations that allow us to keep finding fish faster than price signals affect their demand, so if self-correction has potential, it hasn’t kicked in yet; supposedly we’ve already “reached a point where there are, by weight, more ships in the ocean than fish.”

There is also potential in private fishing in fish ponds on land, and I could imagine prices favoring them once fish finally get too hard to find in the ocean. But Callum claims that most of these fish are fed quite inefficiently from smaller fish from the ocean, so that’s not really any more sustainable. Though I wouldn’t be surprised if the industry figures out how to keep the entire food chain in the ponds.

In short, I see a lot of potential ways for the market to keep fish around even if we keep taking them out of the ocean at what is currently unsustainable levels. But due to what seems to be very obvious negative externalities, I also don’t have a problem with governments trying to help things along with quotas, even as I expect the quotas to often be affected by industry lobbying (and they’d be incorrect due to lack of knowledge anyway even without the lobbyists).

But as far as government regulations go, I don’t think the unintended consequences of fish quotas can get that bad. If they’re set too high (as Callum believes some certainly are), then it won’t be any worse than not having any at all. If they’re set too low, the fish stocks would just replenish so much that they could be adjusted later – it’s only temporarily adding to the public good. Yes, the government is limiting short-term profits, but since the fishers don’t own the fish anyway, that’s not much of an intrusion into personal liberties.

I’m probably missing some things from both sides, and I’m definitely no expert on fish, but these are my thoughts after reading that book and thinking a bit about it.

Joswald1 and -1 others like this

22 May 17:35

Dead Crows: Avian Flew?

by noreply@blogger.com (Mungowitz)

Researchers for the Massachusetts Turnpike Authority found over 200 dead crows near greater Boston recently, and there was concern that they may have died from Avian Flu. A Bird Pathologist examined the remains of all the crows, and, to everyone's relief, confirmed the problem was definitely NOT Avian Flu.

The cause of death appeared to be vehicular impacts.

However, during the detailed analysis it was noted that varying colors of paints appeared on the bird's beaks and claws. By analyzing these paint residues it was determined that 98% of the crows had been killed by impact with trucks, while only 2% were killed by an impact with a car.

MTA then hired an Ornithological Behaviorist to determine if there was a cause for the disproportionate percentages of truck kills versus car kills.

The Ornithological Behaviorist very quickly determined the cause: when crows eat road kill, they always have a look-out crow in a nearby tree to warn of impending dangers.

The conclusion was that while all the lookout crows could say "Cah", none could say "Truck."

That's for Shirley, folks.

Joswald1 likes this

17 May 17:50

You Will Know Them By Their Unpopular Views, by Bryan Caplan

Consider a world where 80% of people are Conformists, 10% of people are Righteous, and 10% are Reprobates. The Conformists are epistemically and morally neutral, so they believe and support whatever is popular. The Righteous are epistemically and morally virtuous, so they believe and support whatever is true and right. The Reprobates are epistemically and morally vicious, so they believe and support the opposite of what the Righteous believe and support. In Dungeons & Dragons terms, the Conformists are True Neutral, the Righteous are Lawful Good, and the Reprobates are Chaotic Evil.

What happens? There are clearly two equilibria: one good, one bad. If the true&right is popular, then the Conformists and the Righteous have 90% of the vote, so the true&right prevails. If the true&right is unpopular, then the Conformists and Reprobates have 90% of the vote, so the false&wicked prevails.

Now suppose that in this world, you are trying to assess an individual's virtue. In the good equilibrium, identifying the virtuous is hard. Only 1 out of 9 supporters of the status quo is genuinely virtuous. The vast majority support the true&right out of sheer convenience. Identifying the vicious, however, is easy. In the good equilibrium, all supporters of the false&wicked are vicious.

The mirror image holds in the bad equilibrium. Identifying the virtuous is easy: Everyone who supports the true&right despite their unpopularity is virtuous. Identifying the vicious, in contrast, becomes hard. Only 1 out of 9 supporters of the status quo truly qualifies. The vast majority of supporters of the false&wicked don't support it out of conviction. They support the false&wicked to fit in.

This model is admittedly a gross oversimplification. But it conveys important insights about people's characters.

1. Conformists have good effects when the true&right is popular, and bad effects when the false&wicked is popular. But the difference in underlying virtue between good and bad societies is small. No individual chooses what's popular in his society. So if you're a conformist who simply supports whatever is popular in your society, they key fact about your character is that you're a conformist, not what you conform to.

2. On the plausible assumption that most real-world people are basically conformists, you can't accurately assess virtue by studying people's views in isolation. You have to look at their unpopular views. Believing true&right things despite their unpopularity is a sign of genuine virtue. Believing false&wrong things despite their unpopularity is a sign of genuine vice.

Consider, for example, the fact that almost all Americans now oppose Jim Crow laws. Is this a strong sign that they're more virtuous than Southerners in 1960? Not really. After all, how many modern Americans would still oppose Jim Crow if they grew up in a Jim Crow society? Only unpopular positions on Jim Crow reveal much about your character. Opposing Jim Crow in 1960 shows great virtue, especially if you live in the South. Supporting Jim Crow in 2013, similarly, shows great vice: You're willing to become a social pariah rather than betray the cause of evil.

On many issues, of course, the truth is unclear. Holding an unpopular view with a 50% chance of truth doesn't say much about your character. But there are plenty of clear-cut cases, too - and the more you know, the more there are. If you want to decipher virtue and vice from people's positions, these clear-cut cases are your Rosetta stone.

Hansonian caveat: If my analysis were well-known, then conformists might strategically adopt unpopular views in order to signal their virtue. Perhaps this already happens to some extent, explaining complaints about "moral posturing" and "moral preening." But human desire to fit in is so strong that this probably isn't a major factor in the world. People primarily posture and preen by poetically defending the popular. If you defy your society to embrace the clearly true&right, you're probably doing it out of virtue. If you defy your society to embrace the clearly false&wicked, you're probably doing it out of vice. And as Zoidberg says, "You're bad, and you should feel bad."

(26 COMMENTS)

What happens? There are clearly two equilibria: one good, one bad. If the true&right is popular, then the Conformists and the Righteous have 90% of the vote, so the true&right prevails. If the true&right is unpopular, then the Conformists and Reprobates have 90% of the vote, so the false&wicked prevails.

Now suppose that in this world, you are trying to assess an individual's virtue. In the good equilibrium, identifying the virtuous is hard. Only 1 out of 9 supporters of the status quo is genuinely virtuous. The vast majority support the true&right out of sheer convenience. Identifying the vicious, however, is easy. In the good equilibrium, all supporters of the false&wicked are vicious.

The mirror image holds in the bad equilibrium. Identifying the virtuous is easy: Everyone who supports the true&right despite their unpopularity is virtuous. Identifying the vicious, in contrast, becomes hard. Only 1 out of 9 supporters of the status quo truly qualifies. The vast majority of supporters of the false&wicked don't support it out of conviction. They support the false&wicked to fit in.

This model is admittedly a gross oversimplification. But it conveys important insights about people's characters.

1. Conformists have good effects when the true&right is popular, and bad effects when the false&wicked is popular. But the difference in underlying virtue between good and bad societies is small. No individual chooses what's popular in his society. So if you're a conformist who simply supports whatever is popular in your society, they key fact about your character is that you're a conformist, not what you conform to.

2. On the plausible assumption that most real-world people are basically conformists, you can't accurately assess virtue by studying people's views in isolation. You have to look at their unpopular views. Believing true&right things despite their unpopularity is a sign of genuine virtue. Believing false&wrong things despite their unpopularity is a sign of genuine vice.

Consider, for example, the fact that almost all Americans now oppose Jim Crow laws. Is this a strong sign that they're more virtuous than Southerners in 1960? Not really. After all, how many modern Americans would still oppose Jim Crow if they grew up in a Jim Crow society? Only unpopular positions on Jim Crow reveal much about your character. Opposing Jim Crow in 1960 shows great virtue, especially if you live in the South. Supporting Jim Crow in 2013, similarly, shows great vice: You're willing to become a social pariah rather than betray the cause of evil.

On many issues, of course, the truth is unclear. Holding an unpopular view with a 50% chance of truth doesn't say much about your character. But there are plenty of clear-cut cases, too - and the more you know, the more there are. If you want to decipher virtue and vice from people's positions, these clear-cut cases are your Rosetta stone.

Hansonian caveat: If my analysis were well-known, then conformists might strategically adopt unpopular views in order to signal their virtue. Perhaps this already happens to some extent, explaining complaints about "moral posturing" and "moral preening." But human desire to fit in is so strong that this probably isn't a major factor in the world. People primarily posture and preen by poetically defending the popular. If you defy your society to embrace the clearly true&right, you're probably doing it out of virtue. If you defy your society to embrace the clearly false&wicked, you're probably doing it out of vice. And as Zoidberg says, "You're bad, and you should feel bad."

(26 COMMENTS)

Joswald1 and -1 others like this

14 May 13:28

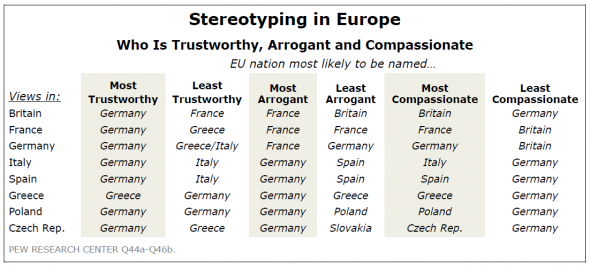

Stereotyping in Europe

by Tyler Cowen

Each column is interesting, for instance read down for “Most Compassionate.” It’s funny how many individuals do the same for themselves, I might add, in what has to be one of the simplest and most common of all intellectual mistakes.

Those results are from the new Pew report, summarized by David Keohane here. The French are growing increasingly disillusioned with the European project, and on key questions the French see the world as the Italians or Spanish do, not the Germans. And there is this: “The report also takes down a few German stereotypes. Apparently, Germans are among the least likely of those surveyed to see inflation as a very big problem and the most likely among the richer European nations to be willing to provide financial assistance to other European Union countries that have major financial problems.”

claudzim, Luke.stirling and 3 others like this

13 May 18:41

Slow motion video of kids trying new foods

by Jason Kottke

Joswald1 and -1 others like this

13 May 18:08

Marty Nemko: Don't Go to College, by David Henderson

The Daily Show had a nice segment this week on the case for not going to college.

The whole thing is quite good. Check out what the guy at the 2:40 point learned. The late Ayn Rand's term for his thinking is "concrete bound."

The one item on which I part company, not with Nemko but with the interviewer, is his advice to "learn Chinese." Of course, he was probably joking but many people who say that are not joking. When you tote up the number of hours it would take to learn Chinese, opportunity cost rears its ugly head. During that same amount of time, I would bet you could learn a huge about how to use a computer better and how to become rich, and you would still have time left over.

HT to Jeff Hummel.

(5 COMMENTS)

Joswald1 likes this

10 May 14:12

Is the Fed able to offset “austerity”?

by Tyler Cowen

Joswald1http://azmytheconomics.wordpress.com/2012/09/26/bad-at-level-targeting-or-good-at-rate-targeting/

I noticed this awhile back. The central bank is holding NGDP growth so steady you could shave with the graph.

David Beckworth serves up another very good blog post and directs us to this graph of nominal gdp; it seems aggregate demand has been recovering steadily:

Scott Sumner directs us to Marcus Nunes, but here is a quotation from Scott:

In 1937 real government purchases recoiled 4.2% and the economy tanked. In 2012 real government purchases were 4.8% below the 2010 level and the recovery is slow!

Surely something is going on that´s making comparable ‘fiscal austerity’ so much less damning in 2012 than in 1937.

And that ‘something’ is monetary policy.

Here are further remarks from Scott.

Joswald1 and -1 others like this

07 May 13:50

#935; In which Aliens land

by David Malki !

Joswald1The problem with reading Reddit regularly.

Matthew McCormick, Tertiarymatt and one other like this

06 May 15:02

The Pyramid of Macroeconomic Insight and Virtue, by Bryan Caplan

Joswald1I, of course am at the apex. Everyone who disagrees with me is tier 3, at best.

Many of my friends laughed at Paul Krugman when he wrote:

Maybe I actually am right, and maybe the other side actually does contain a remarkable number of knaves and fools.

Krugman continued:

The key to understanding this is that the anti-Keynesian position is, in essence, political. It's driven by hostility to active government policy and, in many cases, hostility to any intellectual approach that might make room for government policy.

At risk of sounding misanthropic, though, Krugman is entirely correct to look at "the other side" and see a remarkable number of knaves and fools. Krugman's mistake is that he ignores the comparable number of knaves and fools on his own side. A calm assessment would reveal that the entire spectrum of macroeconomic opinion is sorely in need of self-improvement. If you had to classify everyone with a position on the subject, you'd end up with a Pyramid of Macroeconomic Insight and Virtue that looks something like this:

Tier 1, the Base of the Pyramid (50%): Partisans who loudly support Status Quo Macro Policy (SQMP) as long as "their side" is in power, and angrily oppose SQMP when "their side" isn't in power. See all the Democrats who supported Clinton's austerity, and all the Republicans who supported Bush II's profligacy.

Tier 2 (30%): Ideologues who are sure that "active government policy" will work well/poorly, even though they can't even explain "their side's" arguments, much less the "other side's" arguments.

Tier 3 (10%): People who can parrot some basic textbook macroeconomics to support "their side," but who can't answer basic objections - or even accurately parrot the parts of the textbook that conflict with their views.

Tier 4 (7%): People who understand a few Undeniable Macroeconomic Truths. For Keynesians, these include: "Nominal wages are sticky," "A lot of unemployment is involuntary," and "Aggregate Demand matters." For anti-Keynesians, these include: "The safety net discourages job search and sustains unrealistic worker expectations," "99 weeks of unemployment insurance makes nominal wages stickier," and "Regular government spending is wasteful, and stimulus spending is worse."

The main problems with both groups: (a) Both loathe to acknowledge the other side's Undeniable Macroeconomic Truths; and (b) Both tacitly rely on a long list of Questionable Macroeconomic Exotica to reach their policy recommendations. For Keynesians, the exotica include: "Monetary policy has little effect on Aggregate Demand," "Nominal wage rigidity is a good thing because it sustains Aggregate Demand," and "No matter how much we cut taxes, people will just save the money." For anti-Keynesians, the exotica include: "Given the labor demand shock, workers are indifferent between unemployment and employment at the market wage," "Nominal wage rigidity doesn't matter because firms adjust non-wage benefits and labor intensity instead," and "The market is always right on average... except when the TIPS market keeps forecasting low inflation."

Tier 5, the Apex of the Pyramid (3%): People who freely acknowledge the whole list of Undeniable Macroeconomic Truths, while taking all Questionable Macroeconomic Exotica with a grain of salt.

Needless to say, we can argue about the precise percentages at each tier. But can you seriously deny that most people on both sides are partisans or ideologues? Can you seriously deny that most people who marshal textbook macro to promote or attack SQMP rarely "understand" more than a few bullet points in the textbook?

Wonks' main controversy about my Pyramid, I suspect, will focus on Tier 4 and the Apex: "You're Tier 4. We're Apex!" "No! We're Apex, you're Tier 4." I'm not going to settle this debate tonight. Instead, I'll simply ask: If you decry your opponents in Tier 4 as "fools and knaves," what do you call your allies in Tiers 1, 2, and 3?

Joswald1 and -1 others like this

01 May 16:33

The Hulk's Handshakes and Optimal Monetary Policy, by Garett Jones

The world's a complex place and we don't know a lot about how it works. To make matters worse, it's not just that we're ignorant about the world, we're ignorant about ourselves: We rarely know our own strength. Given our ignorance, how should we interact with the world around us?

William Brainard worked out one answer. With just a little bit of math, he looked at a situation where a policymaker was trying to reach some policy target by pushing on one particular policy lever. Perhaps it's the central bank trying to reach a GDP target over the next two years by setting short term interest rates, perhaps it's a doctor trying to reach a blood pressure target by prescribing a medicine, perhaps it's a dictatorial economic reformer trying to decide how many reforms to enact.

In all these cases, the more the policymaker does, the more uncertain she probably is about the effect of her actions. Experts have a lot of experience raising or lowering interest rates by half a percent so they have a sense of what happens afterward. But they have little recent experience cutting rates by 8 percent in a year in the rich countries. The same is true with blood pressure and economic reforms--experts know a lot about how tinkering works and have a tougher time guessing the effects of bigger changes.

So in many policymaking situations, more action means more uncertainty about the effects of the action. And if your goal is to be close to your target, then more uncertainty is a genuine cost of taking more action.

Hence, Brainard's Conservatism Principle. Alan Blinder, formerly vice chair of the Fed, summed the Brainard Conservatism Principle this way when he applied it to monetary policy:

Estimate how much you need to tighten or loosen monetary policy to "get it right." Then do less.

Why do less? Why isn't the best strategy for hitting the target to try to hit the target? Because more action creates more uncertainty, and you face a real tradeoff.

Extreme versions of this idea turn up in economics and politics from time to time. When the drunk looks for "keys under the lampost" he's taking the certain, low-risk path. When people say "Don't just do something, stand there," they are often noting that people who try to fix problems often create problems of their own. The Brainard Principle shares in those pieces of wisdom but sticks to cases where action is a continuum, where there are a range of options. And it tells us that whatever plain common sense recommends, we probably should do less.

Lessons:

1. If William Tell had been placed further away from his son, he would have aimed higher.

2. It's prudent to try out medium-size quantitative easing if the Fed doesn't know much about how QE works in large quantities.

3. When the Hulk shakes hands with people, most folks come away saying, "Gosh, that seemed like a pretty weak handshake." Also true for the teenage Clark Kent.

Yes, part of the reason to "do less now" when trying out new superpowers like QE is because you can try again later. But even if you only get one shot, Brainard proved that in some cases it's wise to pull your punches.

Humans, we don't know our own strength.

Coda: This is my last day here at EconLog, and I want to thank my co-bloggers Bryan and David for helping to make this such a rewarding experience, and I look forward to reading Art's posts over the coming months. EconLog is a great intellectual environment, I hope it continues for many, many years to come.

I will continue tweeting, so feel to follow: @GarettJones.

Joswald1, Ginnforheisman likes this

29 Apr 21:10

Lawmakers Exempt Selves, Families, and Staffs from Obamacare

by noreply@blogger.com (Mungowitz)

Seriously? We were supposed to pass it first and then find out what is in it?

And once they found out what was in it, they decided to exempt themselves, their families, and their staff? Congress, I mean. I don't know much about health care, but I don't think that this is a good thing.

Furthermore, when the Army said, "We don't need more tanks," the Congress said..."You WILL take more tanks, and you will *&$^%$ing LIKE it! We don't care about defense, we just want to spend more money!"

As Pope Leo X said, "God has given us the Papacy. Now let us enjoy it."

Nod to M.K., and Anonyman.

And once they found out what was in it, they decided to exempt themselves, their families, and their staff? Congress, I mean. I don't know much about health care, but I don't think that this is a good thing.

Furthermore, when the Army said, "We don't need more tanks," the Congress said..."You WILL take more tanks, and you will *&$^%$ing LIKE it! We don't care about defense, we just want to spend more money!"

As Pope Leo X said, "God has given us the Papacy. Now let us enjoy it."

Nod to M.K., and Anonyman.

23 Apr 13:38

Enlarge image i

Paul Sakuma/AP

Enlarge image i

Paul Sakuma/AP

9()) Copyright 2013 NPR. To see more, visit http://www.npr.org/.

Copyright 2013 NPR. To see more, visit http://www.npr.org/.

Why Amazon Supports An Online Sales-Tax Bill

Why Amazon Supports An Online Sales-Tax Bill

by Jacob Goldstein

Enlarge image i

Paul Sakuma/AP

If you:

1. Live in a state that charges sales tax

and

2. Buy something from an online store that does not charge you sales tax,

then you are supposed to:

3. Calculate the sales tax yourself and add it onto your annual state tax bill.

Not surprisingly, as we reported last week, almost no one actually does this.

As online retailing has grown, sales tax has been a growing issue for state governments, which say billions of dollars a year in sales taxes are going unpaid. Brick-and-mortar stores don't like it either, because it gives online retailers an advantage.

But states may soon be able to force out-of-state retailers to charge state and local sales tax. The Hill reports:

The Senate is expected to pass legislation this week that would empower states to tax online purchases.

EBay is fighting the bill. The company just sent out "tens of millions" of emails to its active U.S. sellers, asking them to fight the bill, the WSJ reports. The bill exempts businesses that have less than $1 million a year in sales. EBay wants the exemption to go up to $10 million a year.

Amazon, on the other hand, supports the bill. In fact, a company exec wrote a letter to Senators thanking them for introducing the bill.

What gives? Why would Amazon be supporting a bill that would require it to charge sales tax, and give up an advantage over local retailers?

There are a couple possible reasons.

Reason #1

Collecting state and local sales tax all around the country would require a fair bit of effort on the part of online retailers, because sales tax rules vary from state to state. That's not a huge deal for a giant company like Amazon, but it would be more of a burden for smaller online retailers. From Amazon's point of view, that's a good thing — it makes life harder for Amazon's smaller competitors.

That's why big businesses, despite what they may say, often like regulations. They make life harder for small, would-be competitors. But in the case of Amazon, this argument is less compelling: Amazon spent years doing everything it could to avoid charging sales tax.

Reason #2

Under current law, Internet retailers have to charge sales tax in states where they have a significant physical presence — like, say, a big warehouse. For a long time, Amazon kept warehouses out of big states so it could avoid charging sales tax in those states.

Brick-and-mortar retailers didn't like this, and started lobbying state governments to push for Amazon to charge sales tax. So Amazon changed its strategy. The company agreed to start paying sales tax in more states — and it started building huge warehouses near major metropolitan areas in those states.

The warehouses meant the company had to start charging sales tax. But having warehouses closer to big cities also allowed Amazon to start offering same-day delivery to millions of customers.

As the FT reported last year, the brick-and-mortar stores got the level playing field they wanted for sales tax. But they also got a new level of competition from Amazon. If the company can make cheap, same-day delivery work, it will eliminate one of the last advantages of physical stores.

Copyright 2013 NPR. To see more, visit http://www.npr.org/. Copyright 2013 NPR. To see more, visit http://www.npr.org/.

22 Apr 20:39

Fictional Hillary Clinton and the Real Cost of Political Egalitarianism, by Garett Jones

In fiction politicians can say what they really think of voters. Two examples:

1. The Onion reports Hillary Clinton's thoughts on whether she should run for President (questionable language):

...while I can't definitively say what my plans are one way or another, I can say that, at this point in my life, I'm strongly weighing whether or not I want to endure the absolute hell of appealing to you mindless, dumb-as-dirt simpletons again.

2. In Shakespeare's Coriolanus, a military hero pushed into running for office can't bring himself to pretend to be one of the people--his well-deserved pride gets in the way. He launches into a tirade in front of the voters; his words are more eloquent that that of the typical U.S. senator, but I imagine more than one senator has felt the same way:

You common cry of curs! whose breath I hate/As reek o' the rotten fens, whose loves I prize/As the dead carcasses of unburied men....

Then he complains to the voters, criticizing

Your ignorance, which finds not till it feels...

Coriolanus apparently thought there were lots of intuitionists out there among the voters.

The fictionalized HRC and Coriolanus both think that voters aren't all that rational, all that informed. And both think that it is beneath their dignity to act like commoners just to get elected. HRC doesn't want to drink beer with the guys; Coriolanus didn't want to (as another Shakespeare character put it)...

strip his sleeves and show his scars. And say 'these wounds I had'

...defending Rome's freedom. The candidate's quest for dignity, the candidate's rejection of egalitarianism, raises the cost of running for office.

And in modern politics, the demands for public egalitarianism are incessant. France's gauche caviar scandal is the latest: Hollande's former budget minister turned out to have a hidden Swiss bank account. Part of the scandal is the tax avoidance, part of it is that it shows he's not one of us, he's a rich guy.

All of these demands for equality get in the way of good government. That's a theme in Coriolanus, and it's a theme in economic theory. Economists usually think people should be paid in some kind of proportion to the value they create. But how much extra value does a great finance minister create compared to a mediocre alternative? France is a two trillion dollar economy, so if she raises economic growth per year by a mere one thousandth of one percent (0.001%), she would create $20 million in value each year she stays in office. And I don't think it's outlandish to believe that the best possible finance minister could raise France's GDP by two or three times that amount.

While you and I might disagree on who's a good choice for finance minister and who isn't, we can all agree that it would be easier to get a better shortlist for the job of finance minister if the job paid $20 million a year and it didn't require you to drive a Citroen while you were in office.

Crazy, you might say, no nation with a modicum of democracy could pay top officials like that, you might say, and if they did it would lead to corruption, you might say. In some cases you'd be right, but one nation with a modicum of democracy (I make no claims beyond the modicum) pays its top officials just under a million dollars a year and seems to get good results with relatively low corruption: Singapore. Quoting Bloomberg, though Wikipedia has more:

New ministers will make about S$1.1 million [$0.9 million US], down from S$1.58 million...

And note this embrace of elitism with just a dash of egalitarianism:

The salary of a new minister will now be benchmarked to the median income of the top 1,000 earners who are Singapore citizens and with a 40 percent discount "to signify the ethos and sacrifice that comes with political service..."

There's some evidence that when it comes to politician quality, you get what you pay for; Besley finds that higher pay for U.S. governors predicts governors with more experience in politics, and Ferraz and Finan look at Brazilian data and find a slower revolving door and better educated politicians in regions where politicians get better pay. But alas the egalitarian ethos in democracies makes it difficult to raise the pay of politicians.

The voters' love of egalitarianism is expensive.

Coda: This is my last full week guest blogging here at EconLog; I'm here through the end of April. It's been a wonderful experience, and I want to thank my readers and my co-bloggers for making it so rewarding, and to thank the excellent Arnold Kling and the good people of Liberty Fund for creating EconLog and making it such a vibrant place for candidly discussing free market economics.

My big project over the next year is finishing my book Hive Mind: How Your Nation's IQ Matters So Much More Than Your Own. It's under contract with Stanford University Press with tentative plans for release in Fall 2014; I discuss some of the big ideas behind the book in this article (PDF). Stanford has published two other books by my GMU colleague Chris Coyne, do take a look.

(12 COMMENTS)

Joswald1 likes this

17 Apr 15:27

The idea of wealth taxes is only getting started

by Tyler Cowen

Two top advisers to German Chancellor Angela Merkel have called for a tax on private wealth and property in eurozone debtor states to force the rich to fund rescue costs, marking a radical new departure for EMU crisis strategy.

Here is more. I tell you again, this will be a major issue for the next twenty years and not just in the eurozone. Take a look at all those state and local U.S. pension funds expecting seven percent rates of return.

Notice of the article is from @LindaYueh.

16 Apr 13:59

Why Do People Exchange?

by noreply@blogger.com (Mungowitz)

The newest, and last, of the Learn Liberty videos I did in March 2012. I like the way this one turned out, because it captures something everybody cares about. Free t-shirts!

UPDATE: One of the comments, on Youtube, was this: "This guy looks like Patrick!" (Which is true. I lost 40 pounds not long after filming this video. Pretty strange to look back at...)

UPDATE: One of the comments, on Youtube, was this: "This guy looks like Patrick!" (Which is true. I lost 40 pounds not long after filming this video. Pretty strange to look back at...)

{kind=link}

Joswald1 likes this

11 Apr 14:01

It’s all about supply and demand, not just demand

by Tyler Cowen

The unexpectedly large number of American workers who piled into the Social Security Administration’s disability program during the recession and its aftermath threatens to cost the economy tens of billions a year in lost wages and diminished tax revenues.

Signs of the problem surfaced Friday, in a dismal jobs report that showed U.S. labor force participation rates falling last month to the lowest levels since 1979, the wrong direction for an economy that instead needs new legions of working men and women to drive growth and sustain a baby boomer generation headed to retirement.

Michael Feroli, chief U.S. economist for J.P. Morgan, JPM +0.88% estimates that since the recession, the worker flight to the Social Security Disability Insurance program accounts for as much as a quarter of the puzzling drop in participation rates, a labor exodus with far-reaching economic consequences.

Here is more, from Leslie Scism and Jon Hilsenrath. And there is this:

Of the nearly nine million former workers receiving federal disability payments, more than 2.5 million are in their 20s, 30s and 40s.

“It is difficult to overstate the role that the SSDI program plays in discouraging” employment among these young people, Messrs. Autor and Duggan said in one of their research papers, urging reform.

Joswald1 and -1 others like this

09 Apr 04:21

Investment and Inefficient Charity

by Scott Alexander

After rushing home from Utah I made it to a talk on efficient charity which St. Paul of Rational Altruist put together at the Berkeley Faculty Club.

(I should probably mention that from now on I will be preceding the names of leaders in the effective charity movement with the honorific “St”, because people’s social status and recognition ought to accurately track the level of effect they are having on the world. If through persistence and self-sacrifice someone manages to save the lives of a couple dozen people they never met, I don’t think even the harshest advocatus diaboli could object to an impromptu sainting or two.)

First, St. Elie of GiveWell talked about his organization’s efforts trying to research which charities did the most good and defended the idea of radical transparency – GiveWell’s procedure of meticulously recording everything they do and criticizing themselves ad infinitum in an attempt to become better and more evidence-based.

Then Robin Hanson of Overcoming Bias got up and just started Robin Hansonning at everybody. First he gave a long list of things that people could do to improve the effectiveness of their charitable donations. Then he declared that since almost no one does any of these, people don’t really care about charity, they’re just trying to look good. Then he told the room – this beautiful room in the Faculty Club, full of sophisticated-looking charity donors who probably thought they were there to get a nice pat on the back – that they probably thought that just because they were attending an efficient charity talk they weren’t like that, but that probabilistically there was excellent evidence that they were.

I have never seen a group of distinguished Berkeley faculty gain so sudden and intuitive an appreciation for the Athenians who decided to put Socrates to death. I spent the whole speech grinning like an idiot and probably scared Robin a little. And okay, some of that was because I woke up really early to get to the airport today and had become dangerously overtired and mentally imbalanced, but the rest of it was just that he sounds exactly like he does on his blog, he’s a great speaker, and it was just really funny in a train-wreck sort of way to watch a whole room of innocent and basically decent people get Hansonned. The man is one of a kind and his complete and obviously deliberate imperviousness to normal social niceties needs to be declared a national treasure.

But he made some genuinely unsettling points.

One of his claims that generated the most controversy was that instead of donating money to charity, you should invest the money at compound interest, then donate it to charity later after your investment has paid off – preferably just before you die, since donating money after death is legally complicated. His argument, nice and simple, was that the real rate of return on investment has been higher than the growth rate for 3000 years and this pattern shows no signs of changing. If you donate the money today, your donation grows with the growth rate, but if you invest it, it grows with the interest rate. He gave his classic example of Benjamin Franklin, who put his relatively meager earnings into a trust fund to be paid out two hundred years later; when they did, the money had grown to $7 million. He said that the reason people didn’t do this was that they wanted the social benefits of having given money away, which are unavailable if you wait until just before you die to do so.

And darn it, he was totally right. Not about the math – there are severe complications which I’ll bring up later – but about the psychology. On even the most cursory self-examination, my mind totally recoils at the thought of donating everything I’m going to donate to charity in a single lump sum just before I die. It just gibbers “But…but…you need to be a good person before then!” I’m not saying you can’t tear down Robin’s substantive argument in a bunch of good mathematical ways. I’m saying his ad hominem argument about my motivations seems to be true regardless.

Then he started talking about how you should only ever donate to one charity – the most effective. I’d heard this one before and even written essays speaking in favor of it, but it’s always been very hard for me and I’ve always chickened out. What Robin added was, once again, a psychological argument – that the reason this is so hard is that if charity is showing that you care, you want to show that you care about a lot of different things. Only donating to one charity robs you of opportunities to feel good when the many targets of your largesse come up and burdens you with scope insensitivity (my guess is that most people would feel more positive affect about someone who saved a thousand dogs and one cat than someone who saved two thousand dogs. The first person saved two things, the second person only saved one.) In retrospect this is absolutely true and my gibbering recoil at this problem isn’t just Yet Another Cognitive Bias but just good old self-interest.

Now that I have identified what this pattern feels like, I can look back in my memory and notice more examples. Probably the worst is that an efficient charity group was actually slightly interested in having me interview to work with them back in February-ish and I declined because I already had a career plan – and one from which I could make lots of money to then donate. This may end up being the correct decision and in fact probably is, but I already know that’s not why I did it. I did it because a cognitive paranoia I cultivated for pretty good reasons but can’t turn off at will tells me that doing anything not directly measurable is just my brain lollygagging about and inventing clever stories about why it’s so great, and I only get credit for direct obvious quantitative sacrifice. Working for an efficient charity organization, even if I was able to redirect other people’s money in valuable ways that ended up outweighing the utility of making lots of money myself, wouldn’t be enough to overcome my brain’s suspicion that I wasn’t actually doing any good after all.

Thankfully, Robin’s last point was that the most effective thing to do is to stop beating yourself up and be exactly as irrational as is necessary to convince your mind to go along with the whole “efficient charity thing” instead of freaking out and giving up in disgust. I have already measured about how irrational that is and I don’t see too much reason to change my decision now. Still, no sainthood for me just yet.

So let’s get to the fun part. How do we debunk Robin’s assertion that we should invest charitable givings and donate them only at the end of our lives?

St. Elie discussed this for a little while at the talk and gave what I thought was an unexpectedly good answer. He said that the world is getting better so quickly that we are running out of good to be done. After the initial burst of astonishment he explained: in the 1960s, the most cost-effective charity was childhood vaccinations, but now so many people have donated to this cause that 80% of children are vaccinated and the remainder are unreachable for really good reasons (like they’re in violent tribal areas of Afghanistan or something) and not just because no one wants to pay for them. In the 1960s, iodizing salt might have been the highest-utility intervention, but now most of the low-iodine areas have been identified and corrected. While there is still much to be done, we have run out of interventions quite as easy and cost-effective as those. And one day, God willing, we will end malaria and maybe we will never see a charity as effective as the Against Malaria Fund again.

St. Paul lists several other reasons on his blog. First of all, the US’ tax deduction laws favor spreading your donations out among as many years as possible. Second, you might become a worse person in fifty years and decide you don’t want to give your massive accumulated savings to the poor after all. He also lists a few other arguments, none of which in my opinion have quite the same power as those two.

Most of the people at the meeting today were not radical singularitarians – not all saints can be prophets. But if you believe, as I do, that we’re within about a century of a technological singularity of some sort or other, three new considerations come into play. First, affecting the singularity – either bringing it forward, pushing it backwards, or changing its nature – may be a unique and fantastically high-leverage charity target which will not be available (or may be less available) fifty years from now. Second, if a singularity goes wrong and kills us all, we lose our opportunity to donate to charity later. Third, if a singularity goes right, it’s a pretty good bet that people won’t need malaria nets anymore.

Suppose I will die at age 78 – ie fifty years from now. And suppose I want to donate $10,000 to charity. If I decide against Robin’s strategy, I donate $10,000 today, perhaps to Ethiopia. Ethiopia has a growth rate of about 7%, but let’s assume it can’t keep that up over the next 50 years and its average is 5% (this is still quite high). In 2063 Ethiopia ends up with $115,000 extra or so, which I round off to $150,000 because it can be enjoyed by a couple of generations rather than simply appearing at the end of the period.

Suppose I decide in favor of Robin’s strategy. A couple of investment sites say to expect 7% rate of return, so I can expect about $300,000 (all these numbers are adjusted for inflation, I think).

(if these numbers are right, then using the “efficacy of charity declines as things get better over time” argument means you have to believe in a 50%-in-fifty-years decline in charitable efficacy, which seems like a pretty high bar)

Okay. Now what if the world ends (or progresses beyond the need for charity) in 2062 – forty-nine years from now? In that case, giving now leaves Ethiopia with that $150,000, and waiting till later leaves them with nothing.

I don’t know enough math to do the integral properly, but I can do it at different points and then sum it up. If the world ends in ten years, saving loses $15,000. If the world ends in 20 years, saving loses $25,000. In 30, $45,000. In 40, $70,000. At 49.999, $150,000. If there’s an equal chance of the world ending at any one of those times, on average the world ending before you can donate loses you $60,000. But if the world doesn’t end, saving gains you an extra $150,000. So unless you think the world is more than 70% certain to end before you die, saving like Robin suggests is the best option.

And okay, there are so many problems with this analysis I don’t even know where to start (and I bet commenters will point out ones I missed). I hope someone can do some more rigorous math on this question. But the Fermi calculation gives me the opposite result from the one I was expecting and this is very awkward and I was totally intending to close up this essay with “and therefore, math tells us investing charitable donations is clearly a bad idea.” Instead I’m just going to keep recoiling and gibbering.

08 Apr 14:45

Why the U.S. helps defend South Korea and what can go wrong

by Tyler Cowen

It is not because we need to subsidize their defense per se, to cite one argument which some non-interventionist critics have attacked. It is so, when North Korea behaves in a ridiculous manner, the South can respond (not respond) with great restraint. What we are subsidizing is a) a feeling of security, and b) not building nuclear weapons in response. We do something broadly similar for Japan.

The potential problem is when the same U.S. acts which produce a feeling of security in South Koreans produce a feeling of insecurity in North Korean leaders. And the broader game we are playing, with numerous allies, means we might end up pushing some individual confrontations beyond an optimal point (e.g., how would Israel respond with Iran if we wavered on South Korea?) Might we have to overinvest in the South Korean feeling of security — from a strictly Korean peninsula point of view — to keep Japan, Israel, Taiwan, the Saudis, and others “in line”?

It would be good if the North Korean leadership would read this blog post, as they would then realize that what to their eyes appears to be American “overstepping” is done for the sake of other audiences. It is problematic for the American government to itself communicate this point. Imagine announcing “we don’t stand by South Korea as much as it appears, we are just doing this because Israel faces a signal extraction problem and we can somewhat sway their inference toward relaxing about their own security situation.”

It would be bad if the Saudi leadership would read this blog post (or understand this to begin with). The American government would then have to produce a feeling of security for South Korea all the more.

05 Apr 13:25

Ayn Rand Live?

by noreply@blogger.com (Mungowitz)

Joswald1Time for more regulation?

It's as if Ayn Rand is writing history, more than 20 years after her death. An email from Pelsmin:

Every now and then I hear someone say this entire presidency is aimed at destroying America. Personally, I think that’s extreme, and it’s really aimed at “moving us to our proper place in the world,” which is less dramatic but also directionally misguided.

But then I read this story in today’s WaPo, explaining how the Obama administration wants to encourage aggressive mortgage lending to low-credit/low income buyers. They are working to assure banks that they won’t be held responsible for failed mortgages as long as they conform to FHA guidelines, and that the government (taxpayers) will repay on defaults.

Under FHA guidelines “a borrower can get a home loan with a credit score as low as 500 or a down payment as small as 3.5 percent.” The DOJ is getting involved. The only difference I can find with 2008 is that back then the government was pushing home loans with nothing down to high-risk individuals, with an implicit backing of Fannie Mae, and now the government is pushing home loans with nothing down to high-risk individuals, with an explicit backing from FHA. I didn’t think Washington could stun me. But here we are, the ashes of the economy still warm, and they’re breaking out the matches and gasoline again. And is this possible: “since the financial crisis in 2008, the government has shaped most of the housing market, insuring between 80 percent and 90 percent of all new loans”? Do we again have banks operating under the moral hazard of making loans with government assurance of repayment? Also, what’s the logic of the statement “as young people move out of their parents’ homes and start their own households, they will be forced to rent rather than buy, meaning less construction and housing activity.” I guess this is somehow possible, but don’t they need to live somewhere besides the basement? So they will move into homes they own, or homes they rent. Construction will be needed for buildings occupied by owner or buildings occupied by renter. What am I missing? This is the most disturbing news story I have read in years. Really.

Phone call for Joe Tham. You doubted me. What do you say now?

Every now and then I hear someone say this entire presidency is aimed at destroying America. Personally, I think that’s extreme, and it’s really aimed at “moving us to our proper place in the world,” which is less dramatic but also directionally misguided.

But then I read this story in today’s WaPo, explaining how the Obama administration wants to encourage aggressive mortgage lending to low-credit/low income buyers. They are working to assure banks that they won’t be held responsible for failed mortgages as long as they conform to FHA guidelines, and that the government (taxpayers) will repay on defaults.

Under FHA guidelines “a borrower can get a home loan with a credit score as low as 500 or a down payment as small as 3.5 percent.” The DOJ is getting involved. The only difference I can find with 2008 is that back then the government was pushing home loans with nothing down to high-risk individuals, with an implicit backing of Fannie Mae, and now the government is pushing home loans with nothing down to high-risk individuals, with an explicit backing from FHA. I didn’t think Washington could stun me. But here we are, the ashes of the economy still warm, and they’re breaking out the matches and gasoline again. And is this possible: “since the financial crisis in 2008, the government has shaped most of the housing market, insuring between 80 percent and 90 percent of all new loans”? Do we again have banks operating under the moral hazard of making loans with government assurance of repayment? Also, what’s the logic of the statement “as young people move out of their parents’ homes and start their own households, they will be forced to rent rather than buy, meaning less construction and housing activity.” I guess this is somehow possible, but don’t they need to live somewhere besides the basement? So they will move into homes they own, or homes they rent. Construction will be needed for buildings occupied by owner or buildings occupied by renter. What am I missing? This is the most disturbing news story I have read in years. Really.

Phone call for Joe Tham. You doubted me. What do you say now?

04 Apr 13:49

AI and GE, by Bryan Caplan

My favorite question from this year's Ph.D. Micro midterm:

(18 COMMENTS)

Please share your answers in the comments. I'll post the best responses - and my suggested answer - in a day or two.Suppose artificial intelligence researchers produce and patent a perfect substitute for human labor at zero MC. Use general equilibrium theory to predict the overall economic effects on human welfare before AND after the Artificial Intelligence software patent expires.

(18 COMMENTS)

28 Mar 20:05

"Right" out of their minds

by noreply@blogger.com (Angus)

People, this morning I have to write about right wingers who have totally lost their minds.

Let's start with the trivially mean and stupid. Yes, Rep. King, I'm talking about you. Complaining publicly that the Obama girls shouldn't be going on vacation while the country is struggling. Nice job nimrod.

Now to the New York Post, and the inimitable Thomas Sowell, who stumbles his way to the innuendo that quantitative easing in the US is the same as Cyprus' haircut on bank depositors. There's only one problem with his argument: THERE IS NO INFLATION TOM!!!! When when when will these inflationistas learn how to read a chart:

Finally to the dumbest of the dumb for the day at least. Art Laffer and Stephen Moore in the WSJ on "The Red State Path to Prosperity". Hey guys, repeat after me: THE RED STATES ARE THE POOR STATES! Please please please, learn how to read a chart before you make fools of yourselves.

Here are the 10 richest states: Maryland, New Jersey, Connecticut, Alaska, Hawaii, Massachusetts, New Hampshire, Virginia, California, Delaware.

Here are the rankings for the no income tax Southern states Laffer & Moore are so proud of: Texas (25th), Florida (38th), Tennessee (44). They also brag on Louisiana (41), North Carolina (39), Oklahoma (45th) and Kansas (28th).

Illiterate and angry is no way to go through life, guys.

Let's start with the trivially mean and stupid. Yes, Rep. King, I'm talking about you. Complaining publicly that the Obama girls shouldn't be going on vacation while the country is struggling. Nice job nimrod.

Now to the New York Post, and the inimitable Thomas Sowell, who stumbles his way to the innuendo that quantitative easing in the US is the same as Cyprus' haircut on bank depositors. There's only one problem with his argument: THERE IS NO INFLATION TOM!!!! When when when will these inflationistas learn how to read a chart:

Finally to the dumbest of the dumb for the day at least. Art Laffer and Stephen Moore in the WSJ on "The Red State Path to Prosperity". Hey guys, repeat after me: THE RED STATES ARE THE POOR STATES! Please please please, learn how to read a chart before you make fools of yourselves.

Here are the 10 richest states: Maryland, New Jersey, Connecticut, Alaska, Hawaii, Massachusetts, New Hampshire, Virginia, California, Delaware.

Here are the rankings for the no income tax Southern states Laffer & Moore are so proud of: Texas (25th), Florida (38th), Tennessee (44). They also brag on Louisiana (41), North Carolina (39), Oklahoma (45th) and Kansas (28th).

Illiterate and angry is no way to go through life, guys.

26 Mar 15:39

What to look for in the Cyprus deal

by Tyler Cowen

1. Output on the island could easily decline by 25% or more, and I don’t think that will involve much subsequent mean-reversion. There will be a deflationary shock, an uncertainty shock, an “austerity shock,” a credit contraction shock, and a few other negative shocks as well. The Cypriot government will not be fiscally well situated to support the safety net or automatic stabilizers.

2. It’s never a good sign when a deal is structured so that no one has to vote on it. (Correction: various European legislatures may be voting on it, but no one in Cyprus.)

3. The deal itself still doesn’t cough up all the money, but rather relies on subsequent tax increases and privatizations to come up with at least another billion euros. Believe it or not, the numbers don’t add up.

4. “This was not a good weekend for Russian billionaires.”

5. I wonder if the two main banks even have the money they claim they do. Who tells the truth going into a deal like this?

6. Capital controls in Iceland are expected to remain in place at least through 2015, which would make seven years (and counting). That is a better run country with lots of fish and aluminum smelting. You can expect the same or longer from Cyprus, and that’s assuming this deal can last that long, which I doubt.

7. ELA assistance is now, all the more obviously, contingent rather than certain. Who would keep their money in the “good bank” which is being folded into Bank of Cyprus? Why would anyone do this? Given a shrinking economy, surely this bank cannot afford to pay very much to retain deposits, since rates of return on domestic assets will be negative and capital controls will limit or prevent investments in foreign assets.

8. The capital controls will have to be strict. What will the price of a Cypriot euro be, relative to a German euro? 50%? I call this Cyprus leaving the euro but keeping the word “euro” to save face. And yet they fail to reap most of the advantages of leaving the euro, such as having an independent monetary policy.

9. Given that the nation is uh…corrupt, and the account holders are very often money launderers (duh), how effectively will those capital controls be enforced? Won’t the banks end up drained, one way or another? Of course remittances will need to be sent abroad to purchase “essential services,” right? Who picks up the tab for the total collapse of all the banks? Won’t the euros that are left depart Cyprus altogether?

10. Next up may be Slovenia…

Addendum: A summary of the deal is here. And here are some very good comments. Here are more details on capital controls.

Joswald1 and -1 others like this

No more posts. Check out what's trending.