Chaitanya Patel

Shared posts

India Bullied by Foreign Portfolio Investors ~ What is New !?

How to Find Great Businesses, the Peter Lynch Way

One of the first books I ask new investors to read is Peter Lynch’s One Up on Wall Street.

The easy-going and simplistic stock-picking style discussed in this book brought Lynch great success in his profession as a fund manager at the US mutual fund company, Fidelity, where he generated an average annual return of 29% during 1977 to 1990.

Lynch wasn’t just a great investor, he had a wonderful way of getting across the secrets of his success in everyday language, exemplified by this warning of the perils of putting money into businesses that you don’t understand.

Another of his catchphrases was to “invest in what you know” and he believed everyone could use this advice to spot successful companies.

In fact, he got many of his best ideas at home or when wandering around shopping malls, rather than by poring over company accounts.

“I stumble on to the big winners in extracurricular situations,” he said. “Apple computers – my kids had one at home and then the systems manager bought several for the office. Dunkin’ Donuts – I loved the coffee.”

Now, he didn’t just go straight out and buy shares in the companies he spotted this way. Instead, he used these insights as a basis for further research. As he’s mentioned in his book, he was looking for shares that offered “growth at a reasonable price”. The idea was to avoid two common investment mistakes –

- Either paying too much for fast-growing companies;

- Or buying seemingly cheap firms without realising that they have stopped growing.

Lynch summarised his approach in 25 investing principles outlined as Peter’s Principles in his book Beating the Street.

Now, one of the Peter’s principles is – “Never invest in any idea you can’t illustrate with a crayon.”

He wrote in Beating the Street –

A class of seventh graders at an American primary school did a social studies project on stocks, the kids had to do their own research and dig up stocks for a paper portfolio. They sent their picks to Lynch, who later invited them to a pizza dinner at the Fidelity executive dining room, illustrating their portfolio with little drawings representing each stock. Lynch just loved this because it illustrates the principle that you should only invest in what you understand, the kids portfolio consisted of toy manufacturers, makers of baseball swap cards, clothing manufacturers and outlets, Playboy Enterprises (a couple of boys chose that one), Coke, and other stocks of that ilk.

With a portfolio notably lacking in glamorous technology ventures and entrepreneurial risk taking they went for solid stocks with excellent profits, their portfolio returned 69.6% against a background of a 26.08% gain in the S&P500 in 1990/91.

Now, this is a great idea – Never invest in any idea you can’t illustrate with a crayon – if you are searching for some great businesses to invest in for the long run. Of course, you must buy such businesses only after you research the ideas well, and only when they are available at reasonable prices as compared to the growth they promise.

Anyways, borrowing this idea from Lynch, I’ve tried to illustrate (through my poor drawing skills  ) some great businesses you can find in your own living room, kitchen, and bathroom.

) some great businesses you can find in your own living room, kitchen, and bathroom.

My list is in no way exhaustive, but it’s quite comprehensive as you can see in the two images below…

[Click here to open a larger image]

[Click here to open a larger image]

As you can see, most of us in India are connected to most of these businesses on a daily basis, and we also like the products/services of most of these companies.

So what stops you from researching them further if you are trying to search for those great investment ideas for your long-term portfolio?

Most of these are simple businesses, and have already created a lot of wealth in the past. But a lot of these businesses also have a great future potential, which you can identify only when you read about them, and understand them properly.

I find a lot of small, new investors complaining that they have a very small circle of competence. I’m sure this chart will erase all those complaints.

Knowing and researching 70+ stocks is, in no way, having a small circle of competence.

So go, find some great stock ideas by drawing things your understand, and then research them deeper. You never know when you paint a beauty!

Did UK electorate vote for austerity in polls?

The UK had the best performing of the G7 economies last year, with a real gross domestic product growth rate of 2.6 per cent. In 2009, the last full year of Labour government, the figure was minus 4.3 per cent. Moreover, far from being in depression, the UK economy has generated more than 1.9m jobs since May 2010. UK unemployment is now 5.6 per cent, roughly half the rates in Italy and France. Weekly earnings are up by more than 8 per cent; in the private sector, the figure is above 10 per cent. Inflation is below 2 per cent and falling.....the general government deficit has been nearly halved from 10 per cent in 2009 to 5.7 per cent last year; the structural deficit more than halved from 9.8 per cent to 4.2 per cent. The net public debt has been stabilised at roughly the same level relative to GDP as that of the US.Showing a growth rate after a decline is not a big achievement, although it's better than accentuating the decline itself. The crucial question is whether the UK is back to its pre-crisis level of GDP and how close it is to the trend rate of growth. Also, we have no means of knowing the answer the question: would Keynesian policies have produced better results?

RBI Housing Data Shows Housing Loans Are Taking 40% of Income as EMIs

RBI has released a report on Indian Residential Real Estate Prices. They use bank loan data to get an idea about housing prices. Since Banks appraise houses before giving loans on them, the RBI believes that “Banks and housing finance companies are comparatively practicable and reliable sources of property/house price data, due to their prominent role in institutional financing for housing as well as timely data availability in electronic form.”.

Price Data is Unreliable

This is largely, a load of bull, because not just anecdotally but in real life, I have seen the way appraisals for projects are handled, and the appraiser is actually paid for stating that the house is worth X, and he will not get any future business if he says it is worth less than X. In a way, it’s like valuing a startup – it is worth what the other side is willing to pay for it, and the appraiser will believe that look, if people are buying it at X, it’s worth X.… (Read On...)

'India's private banks will have half the share of the market in 10 years'

It appears that, by private, Lall means both domestic and foreign banks. Today, their combined share is less than a quarter. One can't expect much of an increase in foreign banks' share. So, for Lall's forecast to be come true, the domestic banks must increase their share from 15% to 40%. That's a tall order considering that domestic banks managed a share of just 15% in twenty years' time. I think it's more likely that total private share would be around 40% leaving public banks still dominant but much depends on how much the government is willing to support the public sector.

There's one more thing that's worth noting. The private sector is extremely profitable precisely because it's so small- it has stayed out of financing the infrastructure sector, by and large. If private banks are to grow, they will have to lend more to key sectors such as infrastructure. Such growth will come at a price- profitability won't be as high. Shareholders must hope that private banks don't chase growth as much as Lall thinks they will.

Delay your house

As you would have noticed, I wrote lot of pieces last year. It has again come down to around two a month. The frequency depends on my ability to generate ideas. Whenever possible I’ll write more frequently. Otherwise, I’ll try to stick on to at least twice a month.

Today I’m sharing (with some modifications) a piece I wrote last year.

I happened to meet two friends from our industry recently.

The conversation went around the year 2002 when all asset classes were at multi year low, with all round pessimism and gloomy global scenario after 9/11 incident.

We people who prefer equity are a tiny minority in this country. We feel equity is not given the right place it deserves in investors’ portfolio despite it being better than real estate.

We reviewed some presentations which had data as to real estate prices in prime areas of Chennai around 2002.

I chose Adyar for this piece. It’s because Adyar is the place I live. Some time ago ‘Economic Times’ carried data as to how Adyar is the richest locality in Chennai. We purchased the flat we live during the above period (2002-03). We paid Rs.2300/- per square feet for the 1000 Sq.ft 2 BHK we live in.

After 12 years, a similar flat (a new 2 BHK) is quoting around Rs.15,000 per sq.ft. We paid Rs.23 lakhs in 2002, the value of which is Rs.1.5 crores now.

If I want to sell the flat, it would go for lesser than Rs.15000 per sq.ft as it is more than 10 years old. However for the purpose of this discussion and to the joy of real estate enthusiasts, let us assume we would be able to sell the old flat at the price of the new flat.

We took one fund in 2002. We choose Reliance Growth Fund since one of the friend was from there. The NAV of Reliance Growth Fund (RGF) as on 1’st January 2002 was Rs.19.75 It’s NAV as on May 8th 2015 was 778.55.

RGF was once an excellent performer and turned out to be an average fund during last couple of years.

If I had invested Rs.23 lakhs in RGF instead of Adyar flat, it’s value would now be Rs.9.06 crores or say Rs.9 crores.

Unlike house where I’ve to pay 20% capital gains tax and where I would be getting lesser value than market price, in RGF there is no tax on the gains made and I get 100% of NAV (after adjusting for STT).

Out of the Rs.9 crores proceeds:

I can now buy a 3BHK+ 1 Study (2200 sq.ft @ Rs.15000 per sq.ft) for Rs. 3.30 crores in Adyar itself.

I can also buy any high end luxury car for around Rs.40 lakhs.

The balance Rs.5.3 crores, by prudently investing in instruments like MIP, I can withdraw 9% per annum. This means I get Rs.47.70 lakhs per annum or a nice pension of around Rs.4 lakhs per month.

All we should have done is to invest in equity in early part of the career and bought the house in the later part.

I’m not against real estate. In my opinion, it has potential to generate few percentage points more than inflation in the long run. Also we all want to own the home we live in.

Since we tie up huge net worth including decades of future income also into the house, we never get opportunity to create big wealth which equity is capable of providing us.

We need to debate if it would be wiser to create wealth during the first 20 years of career through equity and then go for owning a house.

This is just a thought. The idea may have merits and demerits.

To me, merits appear significant.

Atal Pension Yojna

Atal Pension Yojna(APY) scheme along with Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY) were launched by Prime Minister , Narendra Modi, in Kolkata on 9th May 2015. There was simultaneous nation-wide launch of the schemes through functions organised in various States and Union Territories . Our article Pradhan Mantri Suraksha Bima Yojana,Pradhan Mantri Jeevan Jyoti Bima Yojana and Atal Pension Yojna gave an overview of these schemes. This article answers frequently asked questions on Atal Pension Yojna.

What is Pension? Why do I need it?

A Pension provides people with a monthly income when they are no longer earning. Need for Pension:

- Decreased income earning potential with age.

- The rise of nuclear family-Migration of earning members.

- Rise in cost of living.

- Increased longevity.

- Assured monthly income ensures dignified life in old age.

What is Atal Pension Yojana?

Atal Pension Yojana (APY), is a pension scheme for citizens of India focussed on the organised sector workers. Under the Atal Pension Yojana, guaranteed minimum pension of Rs. 1,000, 2,000, 3,000, 4,000 and 5,000 per month will be given at the age of 60 years depending on the contributions by the subscribers.

Who can join Atal Pension Yojna?

Any Citizen of India can join APY scheme. The following are the eligibility criteria,

- The age of the subscriber should be between 18 – 40 years.

- He or She should have a savings bank account or open a savings bank account. It is necessary to have a bank account as contributions would be auto debited i.e would be automatically taken every month.

- He/she should be have mobile number and its details are to be furnished to the bank during registration.

- Government co-contribution is available for 5 years, i.e., from 2015-16 to 2019-20 for the subscribers who join the scheme during the period from 1st June, 2015 to 31st December, 2015 and who are not covered by any Statutory Social Security Schemes and are not income tax payers.

How many Atal Pension Yojana accounts I can open?

One can open only one APY account and it is unique.

Tax and Atal Pension Yojna

There are no tax benefits like 80C on contribution to Atal Pension Yojna. The pension received will be considered as Income from Salary and would be used in tax computation.

Who will not not receive Government co-contribution?

Those who are covered under statutory social security schemes are not eligible to receive Government co-contribution. For example, members of the Social Security Schemes under the following enactments would not be eligible to receive Government co-contribution:

- Employees’ Provident Fund & Miscellaneous Provision Act, 1952.

- The Coal Mines Provident Fund and Miscellaneous Provision Act, 1948.

- Assam Tea Plantation Provident Fund and Miscellaneous Provision, 1955.

- Seamens’ Provident Fund Act, 1966.

- Jammu Kashmir Employees’ Provident Fund & Miscellaneous Provision Act, 1961.

- Any other statutory social security scheme

So if you have an EPF account you can still open Atal Pension Yojna account but government will not contribute to your APY account. You would have to make full contribution for selected pension amount.

How much is Government’s co-contribution?

In APY, Government will co-contribute 50% of the total contribution or Rs. 1,000 per annum, whichever is lower, to the eligible APY account holders who join the scheme during the period 1st June, 2015 to 31st December, 2015. The Government co-contribution will be given for 5 years from FY 2015-16 to 2019-20.

How to open Atal Pension Yojna Account?

- Approach the bank branch where individual’s savings bank account is held.

- Fill up the APY registration form. The form in English can be downloaded from here.(pdf) and in Hindi from here. Forms are also available in other languages like Bangla,Gujarati,Hindi,Kannada,Marathi,Odia,Tamil and Telugu which can be downloaded from www.jansuraksha.gov.in/forms.aspx

- Provide Mobile Number.

- Provide Aadhaar Number.

- Ensure keeping the required balance in the savings bank account for transfer of monthly contribution.

Is Aadhaar Number compulsory for joining the scheme Atal Pension Yojana?

It is not mandatory to provide Aadhaar number for opening APY account. However, For enrolment, Aadhaar would be the primary KYC document for identification of beneficiaries, spouse and nominees to avoid pension rights and entitlement related disputes in the long-term.

Can I open Atal Pension Yojana Account without savings bank account?

No. For joining APY, savings bank account is mandatory.

Is it required to furnish nomination while joining the Atal Pension Yojana scheme?

Yes. It is mandatory to provide nominee details in APY account. The spouse details are also mandatory wherever applicable. Their Aadhaar details are also to be provided. Aadhaar is becoming an important number to have. Our article explains Aadhaar : What is Aadhaar, How to enrol,Check Aadhaar status,Download e Aadhaarin detail.

What is the mode of contribution to the account opened under Atal Pension Yojana?

All the contributions are to be remitted monthly through auto-debit facility from savings bank account of the subscriber i.e will be automatically deducted from the saving bank account of subscriber.

What is the due date for monthly contribution?

The due date for monthly contribution will be as per the initial date of deposit of contribution into APY.

What will happen if required or sufficient amount is not maintained in the savings bank account for contribution on the due date?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re 1 per month to Rs 10 per month as shown below:

- Re. 1 per month for contribution upto Rs. 100 per month.

- Re. 2 per month for contribution upto Rs. 101 to 500 per month.

- Re 5 per month for contribution between Rs 501 to 1000 per month.

- Rs 10 per month for contribution beyond Rs 1001 per month.

Discontinuation of payments of contribution amount shall lead to following:

- After 6 months account will be frozen.

- After 12 months account will be deactivated.

- After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

How much can one contribute in Atal Pension Yojana ?

Amount to be contributed monthly under the Atal Pension Yojna scheme depends on the age of the person who joins the scheme and how much pension 1000,2000,3000,4000,5000 Rs he wants. Please remember that once the person passes away the spouse(wife/husband) will get the pension and after death of spouse the nominees will get a lump sump amount.

For getting guaranteed pension of Rs 1000 and lump sump of Rs 1.71 lakh to nominees amount one has to contribute at some sample ages is given below. Detailed table is provided here.

| Age of Joining | Years of Contribution | Monthly contribution |

|---|---|---|

| 18 | 42 | 42 |

| 20 | 40 | 50 |

| 25 | 35 | 76 |

| 30 | 30 | 116 |

| 35 | 25 | 181 |

| 40 | 20 | 291 |

Is there an option to increase or decrease the monthly contribution for higher or lower pension amount?

The subscribers can opt to decrease or increase pension amount during the course of accumulation phase, as per the available monthly pension amounts. However, the switching option shall be provided once in year during the month of April.

What is the withdrawal procedure from Atal Pension Yojana?

- On attaining the age of 60 years: The exit from APY is permitted at the age with 100% annuitisation of pension wealth.On exit, pension would be available to the subscriber.

- In case of death of the Subscriber due to any cause: In case of death of subscriber pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus would be returned to his nominee.

- Exit Before the age of 60 Years: The Exit before age 60 would be permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease.

How will I know the status of my contribution?

The status of contributions will be intimated to the registered mobile number of the subscriber by way of periodical SMS alerts. The Subscriber will also be receiving physical Statement of Account.

Will I get any statement of transactions?

- Yes. Periodic statement of APY account will be provided to the subscribers.

- If I move my residence/city, how can I make contributions to APY account?

- The contributions may be remitted through auto debit uninterruptedly even in case of dislocation.

What will happen to existing subscribers in Swavalamban Yojana?

The existing Swavalamban scheme may be automatically migrated to Atal Pension Yojana.

For age of subscriber between 18-40 yrs: All the registered subscribers under Swavalamban Yojana aged between 18-40 yrs will be automatically migrated to APY with an option to opt out. However, the benefit of five years of Government Co-contribution under APY would be available only to the extent availed by the Swavalamban subscriber already. This would imply that if, as a Swavalamban beneficiary, he has received the benefit of government Co-Contribution of 1 year, then the Government co-contribution under APY would be available only for 4 years and so on. Existing Swavalamban beneficiaries opting out from the proposed APY will be given Government co-contribution till 2016-17, if eligible, and the NPS Swavalamban continued till such people attain the age of exit under that scheme.

Other subscribers above 40 years who do not wish to continue may opt out of the scheme with lump sum withdrawal.Subscribers above 40 years may also opt to continue till the age of 60 years and eligible for annuities.

How are the contributions of Atal Pension Yojna invested?

The contributions under APY are invested as per the investment guidelines prescribed by Ministry of Finance, Government of India. The APY scheme is administered by PFRDA/GOVERNMENT.

Lumpsum Corpus that Nominee will receive

On death of person who was member of Atal Pension Yojna and his spouse(wife/husband), the nominees will receive a lump-sump amount shown in table below. The amount received will be based on how much monthly pension had the person who joined Atal Pension Yojna chose. For example if person chose 2000 Rs of Monthly pension amount, the lump-sump amount received will be Rs 3.4 lakh. If person chose Rs 5000 as monthly pension amount the nominee will receive Rs 8.5 lakh.

| Monthly Pension Amount (Rs) | Corpus (Rs) |

|---|---|

| 1000 | 1.7 lakh or 1,70,000 |

| 2000 | 3.4 lakh or 3,40,000 |

| 3000 | 5.1 lakh or 5,10,000 |

| 4000 | 6.8 lakh or 6,80,000 |

| 5000 | 8.5 lakh or 8,50,000 |

Agewise Atal Pension Yojna Contribution Chart

The amount that one has to contribute for monthly pension of Rs 1000, Rs 2000, 3000, 4000 & 5000 at ages between 18-40 is given below.

| Age ofEntry | Years of Contribution |

Monthly pension of Rs. 1000. | Monthly pension of Rs. 2000. |

Monthly pension of Rs. 3000. |

Monthly pension of Rs. 4000. |

Monthly pension of Rs. 5000. |

| 18 | 42 | 42 | 84 | 126 | 168 | 210 |

| 19 | 41 | 46 | 92 | 138 | 183 | 228 |

| 20 | 40 | 50 | 100 | 150 | 198 | 248 |

| 21 | 39 | 54 | 108 | 162 | 215 | 269 |

| 22 | 38 | 59 | 117 | 177 | 234 | 292 |

| 23 | 37 | 64 | 127 | 192 | 254 | 318 |

| 24 | 36 | 70 | 139 | 208 | 277 | 346 |

| 25 | 35 | 76 | 151 | 226 | 301 | 376 |

| 26 | 34 | 82 | 164 | 246 | 327 | 409 |

| 27 | 33 | 90 | 178 | 268 | 356 | 446 |

| 28 | 32 | 97 | 194 | 292 | 388 | 485 |

| 29 | 31 | 106 | 212 | 318 | 423 | 529 |

| 30 | 30 | 116 | 231 | 347 | 462 | 577 |

| 31 | 29 | 126 | 252 | 379 | 504 | 630 |

| 32 | 28 | 138 | 276 | 414 | 551 | 689 |

| 33 | 27 | 151 | 302 | 453 | 602 | 752 |

| 34 | 26 | 165 | 330 | 495 | 659 | 824 |

| 35 | 25 | 181 | 362 | 543 | 722 | 902 |

| 36 | 24 | 198 | 396 | 594 | 792 | 990 |

| 37 | 23 | 218 | 436 | 654 | 870 | 1,087 |

| 38 | 22 | 240 | 480 | 720 | 957 | 1,196 |

| 39 | 21 | 264 | 528 | 792 | 1,054 | 1,318 |

| 40 | 20 | 291 | 582 | 873 | 1,164 | 1,454 |

The official website of the scheme is www.jansuraksha.gov.in. National Toll-Free – 1800-180-1111 / 1800-110-001 and StateWise Toll free number are listed in this document Statewise Toll-Free (pdf)

Related articles:

- Pradhan Mantri Suraksha Bima Yojana,Pradhan Mantri Jeevan Jyoti Bima Yojana and Atal Pension Yojna

- Saving For Retirement : Pension Plans,NPS,EPF,PPF

- Returns of NPS

- How to Correct or Update Details in Aadhaar

- UAN or Universal Account Number and Registration of UAN

- EPF SMS What is EE, ER? How much on Withdrawal from EPF?

I have received SMS from ICICI Bank about Pradhan Mantri Jeevan Surakhsa Scheme but not about any other scheme. Banks are under pressure to make these schemes a success so you should also be getting calls from your bank. Should one join Atal Pension Yojna? Why or Why not? Are you planning to join Atal Pension Yojna? Will it help the people for whom it is targeted ?

What is full convertibility of the Rupee?

The RBI Governor, Dr. Raghuram Rajan has brought up the subject of full convertibility of Rupee again recently, and it will be interesting to see what steps he takes to make it happen in the future.

Capital account convertibility of the Rupee means the ability to convert INR into any foreign currency, and the foreign currency back to the Rupee at any time without any restriction on the amount at the market rates.

The obvious benefit of capital account convertibility is that it makes it easier for foreign investors to invest in your country as currency movement has no barriers, and they are assured that they will be able to take their money back to their country when the need is warranted.

The big drawback is that if a large number of investors decide to take out their money from the country at the same time then the local currency crashes. This is what happened in the Asian financial crisis when the currencies of Indonesia, Thailand and South Korea took a big hit, and needed support from the IMF to rescue them.

India has taken steady steps to full convertibility, and steps aimed at NRIs are the most visible with a lot of concessions made in the NRE and NRO accounts in the recent past.

Although full convertibility is sometimes given a shade of nationalistic pride by the media, and since only a handful of countries in the world have currencies that are fully convertible (most of them advanced economies), perhaps it is a matter of pride, but more importantly, it is the ability to access deep capital markets that can be used for investing into infrastructure or other projects that makes full capital account convertibility a desirable thing.

The other big benefit is the ability to settle India’s trade in INR as opposed to a foreign currency which is how almost all of it is done today.

I feel that full convertibility is not a ‘short number of years’ away as the RBI governor stated some time ago, but more likely many number of years away because of the situation the Indian economy is currently in, and in general the power it gives foreign investors over your exchange rate. Even our much bigger neighbor hasn’t been able to adapt a fully convertible Yuan despite their impressive reserves, and much better economic indicators.

{kind=link}

Why cash transfers may not work for food subsidies

First, cash transfers would replace the Public Distribution System (PDS). PDS, as Sinha points out, exists both for procurement as well as distribution- it is meant to take care of both the farmer and the consumer. Cash transfers can't take care of the farmer. Sinha rightly asks what would happen to food procurement once PDS is closed down.

Secondly, the old argument about high leakages in PDS is not as strong today given that leakages have come down generally and are pretty low in many states. Experience shows that wider coverage and lower prices help reduce leakages- and that is precisely what is intended under the Food Security Act. It would indeed be an irony that the PDS were to be shut down precisely when we appear to be on the verge of effecting a significant improvement in it.

How does wider coverage help? Well, the problem with focusing only on the BPL category is that a large number who qualify get left out. Making the system universal takes care of this lot. Moreover, having two prices, one for BPL and another for APL, is what creates incentives for leakages. This may sound paradoxical but the wider the coverage, the lesser is the leakage- this is because wider coverage addresses dual pricing which is the source of the leakage.

Thirdly, despite Jan Dhan Yojana, access to the banking system is difficult. So how do the poor access the cash they need to buy food? It will take years to put in place the architecture for reliable and accessible cash transfers.

Fourthly, if PDS outlets are closed, where do people go for food? The local kirana store is not a reliable substitute and, given that store owner doubles as a money lender, it could push more of the poor into debt.

There are other advantages to having PDS that Sinha mentions: the money saved on buying cereals goes towards buying better foods such as pulses; it protects the poor from the vagaries of price fluctuations. It will be difficult to offer protection against price fluctuation with cash transfers whatever the attempt to link these to inflation.

Cash transfers for food subsidies can be contemplated once we are at a higher income level, nutrition levels have improved and poverty is less acute than it is today. Dismantling the PDS right now is fraught with huge risk.

Charter Cities and Economic Zones

Charter City should be a Reform Zone, not a Concession Zone. Most zones are created to offer concessions to firms, not to implement reforms. The goal of a Charter City is reform, not giving out concessions, so in this sense, the motivation for a Charter City is totally different from the motivation behind most special zones.

Here are my two tests for whether a policy is a reform or a concession: Would you be happy if this policy lasts forever? Would you be happy if this policy spread to the entire country? If the answer to both questions is yes, it is a reform. If not, it is almost surely a concession, a gift to some special interest. A reform zone is a zone that implements one or more fundamental reforms.

5 steps forward, 2 steps back

- Monetary policy framework agreement (MPFA)

- Shift government bond market regulation to SEBI

- Shift commodity futures regulation to SEBI

- Establish the Public Debt Management Agency

- Shift regulation-making power for non-debt flows (under Section 6 of FEMA) from RBI to MOF

Two of these were rolled back today -- bond market regulation and PDMA. Here's a response by Ankur Bhardwaj in the Business Standard.

The lack of a bond market is going to weaken the monetary policy transmission, thus making it harder for the MPFA to work. The presence of debt management at RBI is a conflict of interest, which makes it harder for the MPFA to work. The reforms could have worked because they reinforce each other.

Now RBI will have excuses: lacking a monetary policy transmission, they were not able to do inflation targeting; owing to the problems of selling government bonds, they had to keep interest rates too low and SLR too high. The agent who has multiple objectives is accountable for none.

True or False?

Here is another list of True or False….answers you should find it yourself…my job is to confuse you..that I have done. I do not think Pattu has any calculator which will give you the answers…but cannot trust Pattu. He is capable of creating another 10 calculators to answer these T or F also!!

1. In the long run shares perform better than bonds especially if you do not mind some volatility during the journey.

2. Stock markets are now so safe that it is impossible that there would be great crashes like the 1929 depression, etc.

3. Doing a SIP in a mutual fund or in a bunch of equity shares has the same impact over a long period of say 20 years.

4. You should invest in companies with monopoly positions. They are always profitable.

5. You should invest in companies which make addicting products. They are always profitable.

6. A company with a good product and doing well is ALWAYS going to give the shareholders a good return.

7. EBIDTA is a far better indicator of what is happening than EPS.

8. During periods of high inflation interest rates are high, so equity returns are subdued.

9. The good returns from the stock market over the past 20 years is because of brilliant economic growth by good Indian businessmen and their growth, innovation, opening new markets, good management, and good skills.

10. Low P/E stocks are bargains because they are inexpensive to the market and the dividend yield ensures a good moat.

Answers should obviously be with explanation….

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

Case Study – How a 10-Year delay can Destroy your ‘Get-Rich’ Plan?

April 2016 where will the market be?

Where will the market be in April 2016? or say September 2015?

Frankly I do not know, and it does not matter. To make money in the equity markets, you need not know where the market will be 6 months from now or 12 months from now. It is completely irrelevant too.

You should have the ability to handle whatever the market does. You have to reach a stage of ‘indifference’ to the market. If suppose I can tell you with 100% accuracy that the market will give you a 12% return for the next ONE year, how will it matter? Even assuming that I am accurate it will not matter at all.

It would be far far more useful if I can predict a 40% fall or a 49% rise in the market. If at the beginning of the year you are willing to go 0% equity or a 90% equity the above prediction would have mattered. I am 90% in equity ALWAYS and so it does not matter about what you tell me about equity. My greatest strength is that I can take all the volatility and live with that. I have lived with the volatility of Franklin Prima over the past 15 years, and not regretted it. My belief was not in the quarterly performance, but in the fund manager, and I could stick around with the volatility. Like I stuck around with Franklin India Blue chip since the 1990s…or early 2001…

One of the richest men I know (stock market created genius) who has grown many people’s wealth, cannot predict the next 24 hours of the equity market. He accurately forecast some of the super multi baggers and held on to them for a couple of decades, without any worries. I have seen him pick up 2 million shares of a big company and he has been holding it for the past 23 years – while trading in them regularly!!

I really do not know anybody who knows anybody who can predict the markets. It is amazing to see 7 channels, 5 pink papers, and a zillion analysts trying to predict the movements in the equity market. I am actually more amazed to see these “market experts” come on television and predict wrongly day in and day out. They must be thick skinned and we must be fools to get confused between serious money making and entertainment channels.

When I talk about money / wealth creation for young people I remind the employees of good companies that they could pick up small numbers of shares of their OWN company (it does not work well, mind you) while doing a big chunky SIP on a regular basis. Sadly eve n people who have spent say 10 years in good companies like Cipla, HuL, Colgate, Lupin, Wipro, Asian Paints, Dr. Reddys Labs, Hdfc, Hdfc bank, …have not taken the initiative to build their own portfolios. Normally their argument is “Company does not have a regular plan….” or ‘we did not get enough ESOP’ or ‘the company should have given us the shares at a discount’.

Gimme a break. Stop watching television – or switch channels.

Remember NOBODY predicted the Great Depression. Nobody predicted the Japanese market decline.

Americans believe that ‘dollar cost averaging works’ because that country has been able to control world politics. At least in India for the foreseeable future SIP will work. Making a quick start is far more important than making a perfect start after 2 years!! Do It.

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

Knowledge is a handicap for salesmen

“Subra tell me If we ask you to train our sales people by what percentage will our sales go up?”

I am confronted with this question very often. I really have no clear answer to this. In fact I can only say that the KNOWLEDGE will go up. I have no facts to prove that:

- More knowledge leads to more sales

- A more knowledgeable salesman will get bigger closures

- A salesman will say all that I tell him

- A salesman will change his spots because I have done a 2 day ‘knowledge’ training

- A salesman’s boss will give him that much time to do a sensible sales

- A salesman will be actually allowed to do a Needs Analysis

- A salesman will be actually allowed to follow the Needs Analysis

So with all these limitations, I have to answer very gingerly and be politically correct.

A salesman who does not know that pension is taxable can easily sell a pension plan, but a person who knows that it is ELSS that is in an EEE mode (as of now) HAS to offer a product with a less commission. Sigh.

The ULIP commissions are 40% upfront. So if a client were to buy a pension plan for Rs. 300,000 annual premium, the salesman gets Rs. 120,000 as commission, but if that Rs. 300,000 goes into a mutual fund, the commission is Rs. 1200. You can only hope that in the long run the clients realize this and the good word spreads and you make up in volume what you lost in ‘knowledge’.

The salesman in a bank says ‘sir the pension can be withdrawn’. For him/her NOT KNOWING that the amount is taxable at a very high rate is a HUGE ADVANTAGE. Who suffers is of course, the client!!

‘Why a balanced fund, when an equity fund is giving good returns’ – will be answered by a salesman as “yes sir you can invest in an equity fund too’ – the speed of the closure is more important. A knowledgeable person may be able to explain about the tax structure…

A RM in a bank is no intellectual threat to an IIT, IIM grad who thinks he is a stud (the world keeps telling him that) …so he buys a ULIP from her paying Rs.50000 a month for 25 years.

However, when I laugh at his product selection or make a sly remark, I am behaving like a school teacher. In vengeance he goes back to her and buys another product from her.

This is called cutting the nose to spite the face. God bless.

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

Telecom Companies are NOT Losing Money To Data Services: The Net Neutrality Debate

The arguments by Telecom Operators against “Net Neutrality” – or their desire to not just charge users but also website and application owners for allowing users to access that content – is also financial. They say a lot of things about their revenue being cannibalized, that they have to make spectrum investments and so on. Let’s meet their financial fears head on.

The basis of this article is to state that:

- There is no loss to telcos on account of Whatsapp or Skype increased usage, or for that matter, any application. Their “loss” will get converted to profits in data, and with way more usage, substantially higher profits and revenues.

- Data is in fact driving their revenues up, far more than anything else.

- Regulatory changes in anti-spam regulations have already dropped SMS and call volumes.

- The investments in spectrum and infrastructure by the telcos is a function of their regular operation, is amortized over many many years, and realizes revenues in a back-loaded manner.

When You Buy a Bank…

An ad from 1947: “The Uphill Task Ahead”

My friend Veer shared this advertisement from 1947.

After 68 years, Indians are still fighting a war on poverty and it is still an “Uphill Task Ahead.” Very little has changed since 1947 in the economic environment, and what little change there has been regressive. Certainly relative to 1947, Indians have progressed but relative to others, India has slipped further behind.

Note that in the advertisement, the attitude is one of collectivization, that we have to mount a war on poverty by “closing ranks” and “unitedly attack”. That sets the stage for a top-down, command-and-control regime.

A country of free people should not resemble an army. Soldiers inhabit a hierarchical structure where orders flow from the top and they have no freedom in choosing whether or not to obey. That’s an obvious operational difference between an army and a society of free citizens. But there is a more salient functional difference too.

The basic function of a society is the production and consumption of wealth; the basic function of an army is not the production of goods and services but rather to resist foreign forces. By organizing or even conceptualizing a society as an army invariably leads to loss of civic freedom, and inspires fear and suspicion of all things not domestic. This distinction can be illustrated by examining the two Koreas. North Korea most closely resembles an army. Its citizens lead a Hobbesian existence — “solitary, poor, nasty, brutish and short”. South Koreans enjoy greater freedom and a materially rich life as a consequence of that freedom.

For India to prosper, Indians must somehow become free of the command-and-control regime that India inherited from its colonial masters, and Nehruvian socialism continued uninterrupted. The politicians who do the commanding and controlling of course have no incentive to grant freedom to Indians. Most tragically, though, Indians are not even aware that they are not free. They are still irredeemably committed to the task of fighting a war against poverty.

It is all karma, neh?

Zomato Acquires MaplePOS To Launch PoS System

Zomato has acquired MaplePOS, a cloud-based point-of-sale product for restaurants.

Post acquisition, the product will be called Zomato Base.

Base is an Android-based POS system that uses custom hardware for a more reliable and flexible product experience. It offers restaurants features such as menu and inventory management, and has a built-in payment solution to accept debit and credit card payments. This acquisition takes us a step closer to providing end-to-end tech to the restaurant industry.

We’re probably the only food-tech company in the world that is building products for consumers as well as restaurant businesses. There is a lot that can be done if we are able to build a technology platform that connects consumers to restaurants and vice versa, and we believe that a world-class cloud-based POS system is the first step towards building that platform.

Zomato Base will be topped with features such as Menu Management, Inventory Management, Recipe Management, Customer Relationship Management, Data Analytics, Electronic Receipts, Offline Transaction Support, Payment Gateway Integration etc.

This is the first product acquisition for Zomato. Since July 2014, Zomato has acquired 7 companies in various parts of the world to extend its reach in the restaurant search space. This includes the acquisition of Urbanspoon, which gave Zomato a dominant position in Australia, Canada, and the United States.

Zomato will work on integrating the POS product’s services with the consumer product over the next few months; after the integration, Zomato will start offering Zomato Base to restaurant businesses across the world this fall.

Very recently, Info Edge invested INR 155 crores in Zomato.

The post Zomato Acquires MaplePOS To Launch PoS System appeared first on NextBigWhat.

A Quick Note To The Founders Who Were Hiding.. [Net Neutrality Debate]

So far, very few ‘funded’ founders came out in the open and talked openly about the net neutrality issue.

Why? Because it’s a double-edged sword.

[A] You can easily say *Fuck You* to AirtelZero (or similar opportunity) and win the community love.

BUT.

[B] What if your competition goes ahead and does a deal – you are screwed.Plus, inherently such platforms can be used to drive marketing – so ‘never say never’.

That is, keep the channel open. And DON’T SPEAK.

None of them came out clearly in the open and uttered a word (except for some like Deepinder of Zomato).

Now that Flipkart has done the ballsy job of declaring its stand on Airtel zero, several founders are now *issuing* press releases supporting net neutrality. Because they have to ‘look good’. They need to ride the ‘Flipkart wave’ at any cost!

This is the screenshot of my inbox post today’s Flipkart announcement.

My 2 cents to these founders: You are a chicken. You are a mere watcher with no guts to take a stand of your own. Don’t be a pretentious dick. Don’t bother to send us press releases.

The post A Quick Note To The Founders Who Were Hiding.. [Net Neutrality Debate] appeared first on NextBigWhat.

How was the FY 2014-15 for Equities,Debt,Gold

The financial year 2014-15 threw up several surprises for investors. The sustained rally in equities surprised bulls and bears alike while debt investments did fairly well. But assets like real estate and gold, long considered defensive bets, floundered.

FY 2014-15 for Stocks,Debt,Real estate and Gold

During the fiscal 2014-15,

- Sensex has gone up by 5,571.22 points, or 24.88 per cent to 27,957.49 from 22,386.27 on March 31, 2014. Sensex had touched all-time high of 30,024.74 on March 4 this year.the NSE’s Nifty zoomed by 1,786.80 points, or 26.65 per cent, to settle the fiscal at 8,491 after scaling lifetime high of 9,119.20 on March 4 2015.

- Gold has been on the back-foot for over three consecutive years now vis-a-vis equities after outperforming stock market for more than a decade. Gold prices have come down to Rs. 26,575 per 10 grams from Rs. 29,300 per 10 grams on March 31, 2014. Similarly, silver prices have slid to Rs. 37,200 per kg from Rs. 43,400 per kg.

- Foreign Institutional Investors made a net equity investment of Rs. 1.09 lakh crore in 2014-15, and a further Rs. 1.64 lakh crore into debt markets — Rs. 2.73 lakh crore in all, as per the latest data available with Central Depository Services Ltd (CDSL). This was the highest net inflow by FIIs since being allowed to invest in Indian capital markets (equity and debt) over two decades ago in November 1992. The previous high was in 2012-13, when the net investments climbed to Rs. 1.68 lakh crore.

Here is a report card of various investment classes during the financial year.

How the asset classes fared in 2014-15

Different asset classes perform at different times

How equities,debt,gold has performed over the years

Mutual Funds in FY 2014-15

Fifty-one years have passed since the launch of US-64, India’s first mutual fund(it was launched in 1964) Financial year 2014-15 has been good for the Indian markets having posted their biggest gain in the past five years with a return of nearly 25%. Most fund categories made money, thanks to a buoyant equities market and a secular-trending rate cycle. In 2014-15, the country’s 44 fund houses together saw a growth of 31 per cent in their asset base to Rs 11.88 lakh crore at the end of March 31, 2015, according to data released by the Association of Mutual Funds in India (Amfi). The AUM stood at Rs 9.05 lakh crore in preceding fiscal and has been on the rise since 2011-12. In February 2015, the asset base of all the mutual fund companies breached the Rs 12-trillion mark. It took 188 months (or 15.6 years) for the Indian mutual fund (MF) industry to grow from Rs 79,500 crore (in July 1999) to Rs 12.02 lakh crore in February 2015 a gain of 1,412 per cent. It grew over 33 per cent in the last 14 months alone. Mutual fund (MF) industry’s assets base has surged by nearly Rs 3 lakh crore in 2014-15 . To the mutual fund industry’s assets under management (AUM) have barely reached Rs 12 lakh crore even as fixed deposits have almost six times as much, at Rs 70 lakh crore.

But there are two funds that have given nearly four times the index returns in the last one year. Among funds with Assets Under Management (AUM) of nearly Rs 1,000 crore Sundaram SMILE Fund has given investors a return of 105.55% while DSP Black Rock Micro Cap Fund posted a return of 97.83%. In other words both these funds have doubled investors’ money over the last one year.

10 year and 20 year return of mutual funds

A comparison of AMCs’ net profits for financial years 2013-14 and 2012-13 found that industry profits shot up in excess of 56 per cent over the previous year. The growth in profits is skewed, favouring large fund houses.The 21 profit makers in the industry collected Rs 1,567 crore while the 20 loss makers lost Rs 303 crore. HDFC MF retained its top spot with an AUM , followed by ICICI Prudential MF, Reliance MF , Birla Sun Life MF and UTI MF. Richer AMCs are able to leverage their size and strength to pull even further ahead of the rest, Ref: Expert Take – Story of AMCs: The rich are getting richer

Profit and Assets of large Mutual Fund companies in India

IPO, QIP,OFS

Money raised from equity markets doubled to Rs. 58801 crore in the financial year, the highest since 2009-10, as companies used the buoyancy to mobilise funds mainly under the QIP (qualified institutional placement) route. Fund raising in 2014-15 was substantially through the 55 QIPs which saw Rs.28429 crore being mobilised from institutional investors, up 202% compared to the previous year

There were no big ticket IPOs during the year. Despite a stable government coming into power and the resultant buoyancy in the secondary market, only eight main-board IPOs came to the market collectively raising a Rs.2769 crore in 2014-15. This included only one Rs. 1000 crore plus IPO (Inox Wind-Rs. 1020 crore). The response from the public to the IPOs of the year, was mixed. While three IPOs received good response (Sharda Cropchem at 51 times, followed by Snowman Logistics at 46 times and Wonderla Holidays at 32 times), only three were oversubscribed by more than three times. During the last fiscal, just one IPO, which mobilised Rs. 919 crore, hit the market. The highest-ever mobilisation through IPOs was in 2007-08 when companies raised Rs. 41323 crore. As many as 103 companies, which received approval from market regulator SEBI since April 2009 to collectively raise Rs. 48150 crore, allowed these to lapse, despite approvals being valid for a period of one year. In addition, 58 companies which had filed their offer documents with SEBI since April 2009 to collectively raise Rs. 17685 crore withdrew their offer documents.

Despite a huge target of Rs. 58425 crore of divestment for 2014-15, only Rs. 24338 crore, or just 42% of the target, was achieved. On an overall basis, PSUs (public sector units) contributed 41% of the total equity mobilisation. Offers for sale (OFS) through stock exchanges, one of the major routes used in the last two years, primarily for helping promoters of already-listed companies in complying with the minimum public shareholding requirement, saw a huge increase. Companies raised Rs. 26935 crore through 28 OFS in 2014-15, an almost four-fold increase compared to the previous year. The mega OFS of Coal India, which raised Rs. 22558 crore, propped up mobilisation under the route. Mobilisation of funds through rights issues increased 48% to Rs. 6750 crore in 2014-15

Reference : Times of India Equity fund raising hits five-year high in 2014-15

Related Articles:

- Returns of Stock Market, Gold, Real Estate,Fixed Deposit

- Best and Worst Mutual Funds : Difference in returns

- Ups and Downs of Sensex

- Understanding Returns: Absolute return, CAGR, IRR etc

- Stock Market Index: The Basics

The new fiscal year is expected to see the highest economic output growth in recent years. Oil enters uncharted waters in FY 2016, as the question on everyone’s lips is if it will fall further. The government is planning one issue very month to meet its divestment target of Rs.69,500 crore. A freeing up of foreign investment in insurance is likely to lead to some new listings.Fund houses are upbeat about the industry’s performance for the current fiscal (2015-16) as equity markets are expected to continue their momentum, making the segment attractive. Going forward, however, whether which funds will continue to outperform is anybody’s guess. Gold is expected to stay muted. The MF industry itself has a disclaimer that says past performances are not indicative of future performance of the schemes. How are you planning your investment strategy in FY 2015-16?

Satyam and the Case of Big Hairy Manipulative Scamming Promoters in the Stock Market

The case of Satyam has finally been decided.

In December 2008, just after the collapse of Lehman brothers, one of India’s largest outsourcers, Satyam, decided to buy a promoter-run listed firm, Maytas Constructions, which was in the business of real estate. Why would an IT company buy a real estate firm? Good question, and this was being asked by everyone just as the stock price kept falling. As institutions got more antsy, Satyam founder Ramalinga Raju came out with startling statement: he had falsified accounts of the company to show higher profits. The cash balances – which would have occurred as a result of high retained profits – were non-existent, with a hole of over Rs. 5,000 cr.

After 6 long years, the courts have finally declared Raju guilty of fraud. Meanwhile the company was taken over by Tech Mahindra and merged into it, with even the central government involved on coordinating the rescue.… (Read On...)

Rich People Spend More

It is very satisfying when research corroborates naive intuition. We expect water to flow downhill and when research after much painstaking data analysis concludes that indeed water flows downhill, it is a valuable addition to human knowledge and understanding. Switching off sarcasm mode now. I entered that mode when I read “Rich People Are Great at Spending Money to Make Their Kids Rich, Too” in The Atlantic. (Hat tip: Rajan.) An accompanying graphic shows “Share of Spending on Certain Categories, by Income Group” —

Naive intuition and a bit of introspection is sufficient for one to conjecture that relative to the non-rich the rich (1) spend more money on everything, and therefore (2) spend more on luxuries. The poor have to worry about keeping body and soul together. So most of their spending has to go into the essentials needed for present survival — food, clothing, shelter. The future is important to all but concern for the future has to be sacrificed for the present. That is, the poor have to heavily discount the future out of need, not out of myopia. Worrying about the future is a luxury when your present is precarious.

So here’s the concluding paragraph of the article:

It’s boring to point out that having more money affords you more food, more clothes, more housing, and more cars. But the richest families actually spend less on food, clothes, housing, and cars than the poorest families as a share of their income. The real difference between the rich and the poor is that the rich spend a larger share of their much larger income on insurance, education, and, when you drill into the housing component, mortgages—all of which are directly related to building wealth, preserving wealth, and passing it down in the form of inheritance of direct investments in the lives of their children.

Fact is that insurance, education, owing a home, etc, are luxuries. That the rich would buy more of those relative to the poor makes absolute common sense. So what’s the real difference between the rich and the poor? People are the same but depending on whether they are rich or poor, they behave differently in what they consume.

The rich are different from you and me (assuming that you, like me, are not rich), as F. Scott Fitzgerald remarked to Hemingway. Hemingway replied, “Yes, they have more money.”

(Digression: The wiki talk page explains that “this never actually happened; it is a retelling of an actual encounter between Hemingway and Mary Colum, which went as follows:”

Hemingway: I am getting to know the rich.

Colum: I think you’ll find the only difference between the rich and other people is that the rich have more money.

End digression.)

Human nature is comprehensible and universal. Consequently human behavior is to a large extent predictable but you need to know the circumstances. Differences in behavior is partly due to differences in circumstances. Circumstances are beyond the control of individuals, and even groups. (In economics, the term is exogenous — things that are external and that have to be taken as given and unalterable from within.) How people behave is not a reflection of their intrinsic nature but what any other human would do under similar circumstances. That’s the point of this little post.

It is not a man’s world

Guys (and girls) when you get into a marriage be careful about your money. Currently the odds are in favor of the women. Totally.

So if a man leaves Rs. 20 crores to his son, his son’s wife (ex wife) can ask for half of that within one year of marriage. Talk about money, ring fence your property, women take care of your jewellery…life is not so simple after all…

Many marriages are ending in trouble and on the rocks..be careful. Collect video evidence that the gifts from the girls house are coming voluntarily (if in doubt take it in writing). Record a lot of evidence about girl being happy, keep it in your records.

Make sure that doctors reports are preserved, and there are no self inflicted wounds…

Serious not joking. Now I know 3 boys going through very tough times – rich boys girls reasonably well off but asking for 9 digit settlements…

http://mindblowing.tv/the-painful-truth-of-indian-men-becoming-victim-of-indian-laws-made-for-women/

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

Marriage pressure: On boys!!

If you think the marriage pressure is only on girls, you are sadly mistaken!! There is a lot of pressure on boys too.

Even when a boy is “in love” and wants to marry a girl of his choice the following demands are pretty normal:

– Why do you not buy a house of your own?

– How long will you stay with your parents?

– See staying with your parents is fine, but they have just a 1bhk how can you live in such a small place?

– You have a motorcycle? Is it not dangerous? Can you not afford a car?

– Why do you not take up a foreign assignment – that way both of you can live alone!!

– Is your salary not too low? My nephew is in “Wxdrf” and he is almost on double of this salary.

– You are paying the EMI of this house, but there is not enough space for all the 4 of you. You must do something about it.

– Now you are staying in this house…will your father give to you or will it have to be shared with her?

– Both you and your father are paying the EMI and the house is in joint names…but what happens to your dad’s portion of the amount paid? Will your siblings come for a share?

-Why are you spending so much on the repairs of this house? You are not sure whether you will inherit this house.

ALL THESE ARE QUESTIONS THAT BOYS HAVE BEEN ASKED BY THE POTENTIAL INLAWS…..bechare ladke…

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

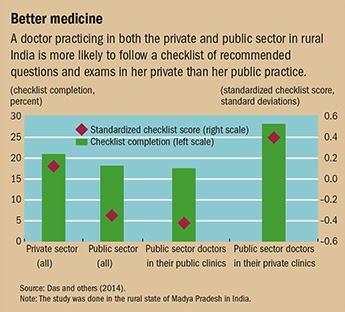

The last mile challenge with public service delivery

In particular, it points to recent studies involving vignettes and survey which highlight the quality problem - less time spent with patients, non-adherence to treatment protocols, wrong treatment prescriptions, over-treatment etc - being faced by health care systems in developing countries. They write,

Consultation time varies from as little as 1.5 minutes (public sector, urban India) to 8 minutes (private sector, urban Kenya). Providers ask on average between three and five questions and perform between one and three routine examinations, such as checking temperature, pulse, and blood pressure. In rural and urban India, important conditions are treated correctly less than 40 percent of the time; when patients receive a diagnosis, it is correct less than 15 percent of the time. Unnecessary and even harmful treatments are widely used by all providers and in all sectors, and potentially lifesaving treatments, such as oral rehydration therapy in children with diarrhea, are used in less than a third of interactions with highly qualified providers. Less than 5 percent of patients receive only the correct treatment when they visit a provider... Public doctors in primary health clinics prescribed antibiotics for diarrhea 75.9 percent of the time, spending 1.5 minutes to reach a treatment decision.However, while the quality of care is poor in both private and public sectors, it is far less inferior in the former. Interestingly, they also find that "patient-centered interactions and treatment accuracy were highest in private sector clinics with public doctors", underlining the higher median quality of doctors in public systems.

Such activities, what Lant Prtichett has described as "thick" activities, are more transactional, requiring continuous engagement by human agents, and difficult to script into monitorable actions which can be supervised with information. They stand in contrast to "thin" activities that are informational and involve some form of logistics which can be readily monitored using information.

This assumes great significance as the government in India grapples with the scaling up of transactional activities like Clean India, Skill India, Open-defecation Free India, and so on.

Zoning regulations and the next generation of urban reforms

A 2005 study by Mr Glaeser and Raven Saks, of America’s Federal Reserve, and Joseph Gyourko, of the University of Pennsylvania, attempted to derive the share of property costs attributable to regulatory limits on supply. In 1998 this “shadow tax”, as they call it, was about 20% in Washington, DC, and Boston and about 50% in San Francisco and Manhattan. Matters have almost certainly got worse since then. Similar work by Paul Cheshire and Christian Hilber, of the London School of Economics, estimated that in the early 2000s this regulatory shadow tax was roughly 300% in Milan and Paris, 450% in the City of London, and 800% in its West End. The lion’s share of the value of commercial real estate in Europe’s most economically important cities is thus attributable to rules that make building difficult... the net effect of these costs is felt more by the poor than by the rich.

Chang-Tai Hsieh, of the University of Chicago Booth School of Business, and Enrico Moretti, of the University of California, Berkeley, have made a tentative stab at calculating the size of such effects. But for the tight limits on construction in California’s Bay Area, they reckon, employment there would be about five times larger than it is. In work that has yet to be published they tot up similar distortions across the whole economy from 1964 on and find that American GDP in 2009 was as much as 13.5% lower than it otherwise could have been. At current levels of output that is a cost of more than $2 trillion a year, or nearly $10,000 per person.

In a recent paper Matthew Rognlie, a doctoral student at MIT, noted that the rising share of national income flowing to owners of capital, rather than workers, is largely attributable to increased payments to owners of housing. Capital income from housing accounted for just 3% of the total in 1950 but is responsible for about 10% today.

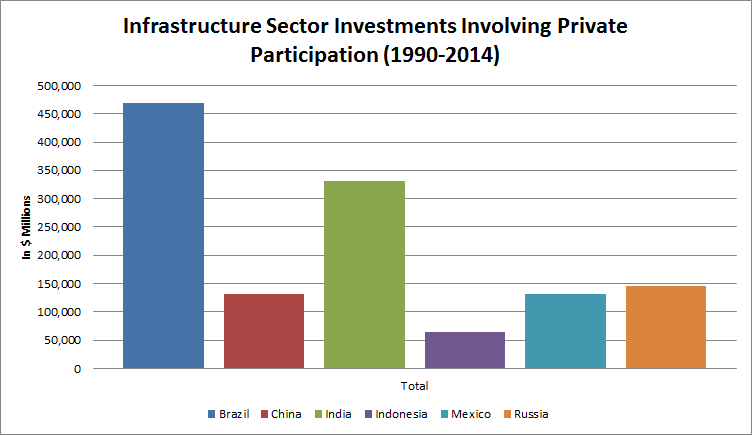

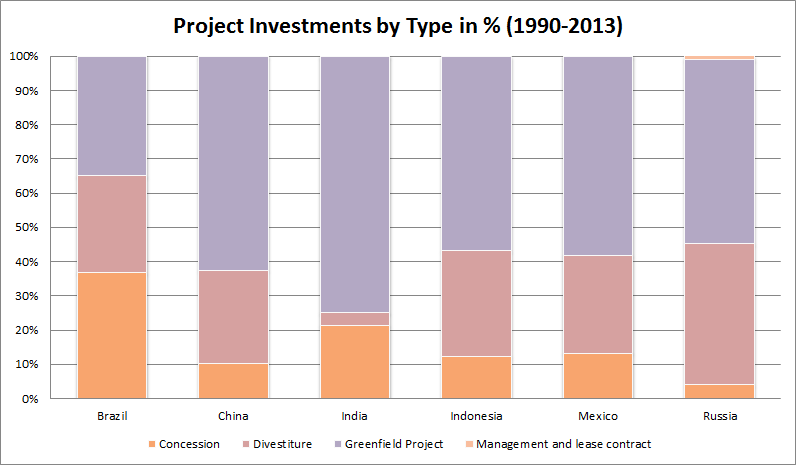

Private participation in infrastructure

Listening to WRONG people

Surely you have heard these few phrases…let me tell why they are dangerous:

1. High Risk Leads to High Returns:

When I talk about ANYBODYs portfolio in a class one student will say this “high risk, high returns”. In most of the portfolios that I have reviewed there has been RISK ELIMINATION, not risk embracing. Most of the people would have removed some money from the market when the market was booming. Or when they needed to buy a house, or an office. Or simply to put it into a debt instrument. So most of the wealth created has been by REDUCING RISK not by increasing risk.

Think about this: If high risk lead to high returns always, where is the risk?

Extending it a little further does it man Highest Risk is Highest Returns? What happened last time when you took high risk? did it lead to highest returns?

2. The easy money has been made:

Forget what Subra says..they were lucky to have been in the market in the 1990s and buy all those great bluechips at low prices. WRONG. WRONG. WRONG. Many of my shares which have made money would have made money for you even if you had bought it as late as 2008. Like Cholamandalam. Hdfc bank. Kotak bank. Even shares like Kajaria ceramics, Essel Propack. These were available at very low prices. Procter and Gamble was available for 1000 in Dec 2013.

It is about good shares. In fact I think the genius in me….is not the buying, but the ability to hold during such a fantastic joy ride – like Hdfc Ltd, Hdfc bank, Nestle, Colgate, Gsk, PnG…etc. Yes of course I can be accused of buying Tata steel and Tata power and holding on for too long a time. However I can live with that allegation. After all you do not get up one day and say “i have had enough of power companies let me go to Fmcg” – your portfolio creation is a dynamic processes. At this point in time I like Tata Steel, Tata Power and Bharti Airtel. All these companies have made me a lot of money in trading, so happy to hold an investment / trading position DESPITE knowing that none of them is an immediate multibagger. Some of these companies mentioned are STILL capable of delivering market defying results.

3. I have seen BULL MARKETS before, it ends badly:

People who have stayed a long time make this statement. I think it is like saying “do not live, one day you will die”. I have seen my grandparents, uncles, aunts, cousins, friends, ….die. All ended badly. This sounds so comic does it not? After all only when things get bad it ENDS. So you cannot sit and worry about death, you need to go and get a life.

Can you imagine a play? It ends. And somebody says “its over”. Then they switch off the lights and all go home. THIS NEVER HAPPENS IN THE MARKETS.

One day Fmcg will run out of steam and you may find some other market leader – Infra? auto? banks? I do not know but surely markets do not end. A few companies do. Sure. Some very well run companies had no clue about what will happen to them. Some industries closed won (the film camera). Some games go out of fashion. Some businesses lose out on profitability. In big cities even closed companies have a fantastic asset list for you to strip…

So do not get carried away. Sure if your goals are 3 years away you should be about 60% of the corpus in debt market..and every month you should sell off something in equity and rebalance….HEY THAT IS YOUR PROBLEM….not the markets problem

Yes one day you will end. Right now, keep investing.

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

The "secular stagnation" opportunity

My greatest concern about Larry’s formulation, however, is the lack of attention to the international dimension. He focuses on factors affecting domestic capital investment and household spending. All else equal, however, the availability of profitable capital investments anywhere in the world should help defeat secular stagnation at home. The foreign exchange value of the dollar is one channel through which this could work: If US households and firms invest abroad, the resulting outflows of financial capital would be expected to weaken the dollar, which in turn would promote US exports. (For intuition about the link between foreign investment and exports, think of the simple case in which the foreign investment takes the form of exporting, piece by piece, a domestically produced factory for assembly abroad. In that simple case, the foreign investment and the exports are equal and simultaneous.) Increased exports would raise production and employment at home, helping the economy reach full employment. In short, in an open economy, secular stagnation requires that the returns to capital investment be permanently low everywhere, not just in the home economy.

Stagnation Land has the technologies, businesses, and even capital, all searching for opportunities. It also faces an aging population and resultant demand for different kinds of labor. Emerging Land has rising productivity, remunerative investment opportunities, growing consumer demand, and a large pool of labor. The complementarity could not have been any more mutually beneficial. The scope for a new growth compact between the two countries could not have been more opportune.