I have never been bitten by a dog (by an unfriendly dog to be precise). However, there were few friendly ones who would chase me for fun. Well it was fun for them but as a kid I didn’t particularly enjoy that kind of sport much.

So when I moved into my current apartment community, housing nearly two thousand flats, it felt nostalgic because the campus had multiple patches of large open areas which meant it was a boon for dog owners (and heaven for their dogs).

Few years back, it wasn’t uncommon to see few fitness conscious dogs taking regular morning and evening walks (along with their disinterested owners) inside the apartment campus. But as the resident population grew, the population of pets followed suit. Pretty soon, it became a common practice for dogs to relieve themselves anywhere in the campus.

The pet owners perhaps assumed that cleaning was a responsibility of maintenance staff which resulted in a campus littered with dog poop everywhere. It was ironical that the mess was equally disturbing for all residents (including those offending dog owners) but it was quite logical, in absence of any specific laws about pet poop mis-management, for people to keep their houses clean and compromise with the common area.

I couldn’t help but marvel at Aristotle’s insight about this issue. He said –

What is common to many is taken least care of, for all men have greater regard for what is their own than for what they possess in common with others.

Perhaps Aristotle’s neighbourhood had many pets too. Although, during his times people were probably more fascinated with horses than dogs. That reminds me of an interesting trivia –

In late 1800s the primary mode of transport was horse carriage and in New York city alone there were more than 150,000 horses. This resulted in more than three million pounds of horse manure per day that somehow needed to be disposed of. Holy s**t!

Pardon me for all the crappy (and stinky) discussion so far.  I think I digressed from the subject. Oh! I haven’t even introduced today’s subject yet. Sorry again!

I think I digressed from the subject. Oh! I haven’t even introduced today’s subject yet. Sorry again!

My mind, like an unchained monkey, hops from one branch of thought to other. That’s what I call “google-ification” of human mind. A phenomenon where even before you are finished thinking about a word, the google(ish) mind starts regurgitating interesting trivia about it.

The mental model that we are going to look at today is called Tragedy of Commons, TOC in short. It’s an important idea from the field of economics and ecology.

Tragedy of Commons

TOC is a phenomenon, as we have seen in the case of dog owners above, that results from actions that benefit the individual (meaning single persons, households, villages, companies or nations) in the short term but often end up hurting the collective.

Mind you, it’s not a cognitive bias neither a result of irrational human behaviour. On the contrary, it’s the perfect rational behaviour that leads to the long-term ruin of the common resources.

This shows how individually good decisions lead to collectively bad outcomes.

Gregory Mankiw, in his book Principles of Economics, explains the idea using this simple parable –

Consider life in a small medieval town. Of the many economic activities that take place in the town, one of the most important is raising sheep. Many of the town’s families own flocks of sheep and support themselves by selling the sheep’s wool, which is used to make clothing.

…the sheep spend much of their time grazing on the land surrounding the town…No family owns the land. Instead, the town residents own the land collectively, and all the residents are allowed to graze their sheep on it. Collective ownership works well because land is plentiful.

[Very soon] With a growing number of sheep and a fixed amount of land, the land starts to lose its ability to replenish itself. Eventually, the land is grazed so heavily that it becomes barren. With no grass left, raising sheep is impossible, and the town’s once prosperous wool industry disappears. Many families lose their source of livelihood.

What causes the tragedy? Why do the shepherds allow the sheep population to grow so large that it destroys the Town Common? The reason is that social and private incentives differ. Avoiding the destruction of the grazing land depends on the collective action of the shepherds. If the shepherds acted together, they could reduce the sheep population to a size that the Town Common can support. Yet no single family has an incentive to reduce the size of its own flock because each flock represents only a small part of the problem.

In essence, the Tragedy of the Commons arises because of an externality. When one family’s flock grazes on the common land, it reduces the quality of the land available for other families. Because people neglect this negative externality when deciding how many sheep to own, the result is an excessive number of sheep.

The Tragedy of the Commons is a story with a general lesson: When one person uses a common resource, he or she diminishes other people’s enjoyment of it. Because of this negative externality, common resources tend to be used excessively.

This mental model was further made popular by an American ecologist Garret Hardin. Charlie Munger spoke about this in his 2003 talk at University of California –

…the tragedy of the commons model, popularized by my longtime friend, UCSB’s Garrett Hardin. Hardin caused the delightful introduction into economics – alongside Smith’s beneficent invisible hand – of Hardin’s wicked evildoing invisible foot. Well, I thought that the Hardin model made economics more complete, and I knew when Hardin introduced me to his model, the tragedy of the commons, that it would be in the economics textbooks eventually. And, lo and behold, it finally made it about twenty years later. And it’s right for Mankiw to reach out into other disciplines and grab Hardin’s model and anything else that works well.

TOC Is Everywhere

TOC isn’t limited to just dogs and sheep. It applies to ecosystems, rivers, oceans, organisms or mineral resources.

Even meetings in office! Claims this post –

In a culture where anyone can call a meeting for any reason at any time, they will.

After getting familiar with this mental model, I started noticing it in many others places. In fact in my apartment complex (for that matter for any community living) I found few more TOC issues –

- The campus has designated car parking slots for each flat and if someone has multiple cars then they can rent one. However, the visitor parking area is free. A visitor parking area is supposed to be used as common resource. But TOC kicks in and what do you see? People start using the visitor parking for their extra cars. Not only that, people would even invite their friends’ and relatives’ to leave their cars in the visitor parking for many days.

- In apartment complexes you can still enforce rules but what about houses which don’t really belong to a closed community? In Bangalore, and perhaps in all big cities, it’s common for people to build their houses without making provision for garage. Why? The road is a common resource and free of cost. So you see most of the roads being used as permanent parking areas by most of the car owners. TOC again!

I found this interesting piece of observation on Farnam Street blog about TOC –

While walking my dog around Philadelphia during the blizzard aftermath, I couldn’t help but notice an interesting trend. Virtually all of the houses with a single occupant or family (as indicated by a single doorbell or knocker) were shoveled clean. Nearly every house with multiple occupants — and most businesses — were unshoveled. This seems like a TOTC in reverse: A common good that requires work to maintain is ignored if there is a diffusion of responsibility.

If you really think about it, a lot of social vices are aggravated as a result of TOC.

Everyone wants to get rid of corruption but when it comes to getting our work done at public office we don’t mind paying a small bribe, knowing very well that it’s a harmful practice for the society over long term.

Peter Bevelin, in his book Seeking Wisdom, writes –

Why do people abuse the health care and welfare system? Isn’t it natural that people use the system if they don’t have to pay anything? And if people don’t have to pay for a benefit, they often overuse it. The more people that benefit from misusing the system, the less likely it is that anyone will draw attention to what really happens. Individually they get a large benefit and it’s a small loss for society. Until everyone starts thinking the same.

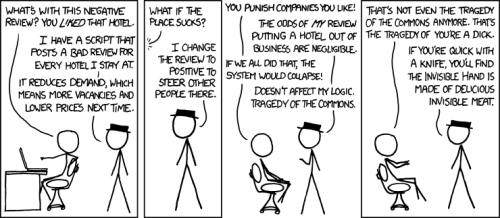

Here is a nice illustration from the house of Khan Academy –

Limitations of TOC

Before I start sounding like a man with a new hammer (TOC), let me talk about the limitations of this mental model. With all the rules, policies, taxes, and regulations at place a lot of common resources around us have become less prone to fall for TOC.

Even Garret Hardin revised his theory of TOC a bit to account for this factor. He wrote –

To judge from the critical literature, the weightiest mistake in my synthesizing paper was the omission of the modifying adjective “unmanaged.” In correcting this omission, one can generalize the practical conclusion in this way: “A ‘managed commons’ describes either socialism or the privatism of free enterprise. Either one may work; either one may fail: ‘The devil is in the details.’ But with an unmanaged commons, you can forget about the devil: As overuse of resources reduces carrying capacity, ruin is inevitable.” With this modification firmly in place, “The Tragedy of the Commons” is well tailored for further interdisciplinary syntheses. (source: extensions of tragedy of commons)

The word “managed” is an important key in addressing the issue of TOC. Let’s see how.

How To Solve TOC

Before jumping on the answers let me state that there are no silver bullet like solutions for this problem, however there are few ways in which you can manage and minimize the impact.

Singapore is a great example of how to solve TOC issues especially in dealing with traffic problems. My friend Jana Vembunarayan has compiled a great post on TOC and you should read it.

Broadly there are two ways to contain the problem of TOC.

First, an enforcement body (like government) can use regulations or taxes to reduce consumption of the common resource. Mankiv suggests in his text –

If the tragedy had been foreseen, the town could have solved the problem in various ways. It could have regulated the number of sheep in each family’s flock, internalized the externality by taxing sheep, or auctioned off a limited number of sheep-grazing permits. That is, the medieval town could have dealt with the problem of overgrazing in the way that modern society deals with the problem of pollution.

This is how the management committee at my apartment complex addressed the issues. They came up with strict rules for pet owners to take the responsibility of cleaning the mess themselves. Of course they had to facilitate poop disposal waste bins which made the task easier. Similarly management had to come up stringent policies and parking violation fines to control the TOC tendency in car parking problem.

The idea of carbon credits and its trading is to contain the carbon emission (pollution). There are some interesting insights in this article about how social entrepreneurs are working with TOC.

Second way is to turn the common resource into a private good. Mankiv writes –

The town can divide the land among town families. Each family can enclose its parcel of land with a fence and then protect it from excessive grazing. In this way, the land becomes a private good rather than a common resource. This outcome in fact occurred during the enclosure movement in England in the 17th century.

Here is an interesting thought – the attached toilet in your bedroom? Isn’t it a private good? May be one day pet lovers might consider installing dog-loo inside their houses. I think that would be sign of a developed country.

By the way here is an interesting piece of thought, although unrelated to the current topic of discussion but just can’t control the unchained monkey in my head, about characteristics of a developed country (or community) –

A developed country is not a place where the poor have cars. Its where the rich use public transportation.

I couldn’t find out who said this but if you know please tell me. Interestingly, Garret Hardin seems to be talking on the same lines in this video –

Conclusion

Before writing this post I was vaguely aware about the idea of TOC. But in the process of researching I learned a lot of new stuff. And as I have said before, that’s the primary purpose for me to compile this Latticework series.

I hope my learning doesn’t stop here. I expect to gain more insights from other people especially you, the reader.

Do participate in the discussion. Without your participation this post would mostly lie here like a boring monologue. Don’t hesitate to share your insights and feedbacks. I am especially looking forward to the ones which challenge the ideas presented here.

And please forgive me if I have sounded insensitive towards dogs. I don’t hate dogs. I love them especially when they are chasing other people.

Take care and keep learning.