I am continuing my mini series on reading S1s (IPO documents). We are enjoying an IPO bonanza this year, so we might as well use it for some good and learn something.

When a company files for an IPO, I like to think if there is a publicly traded company that looks a lot like that company and if so, I lik to run some numbers comparing the two.

Well we have that exact situation with Uber filing to go public last week. Here is Uber’s S1.

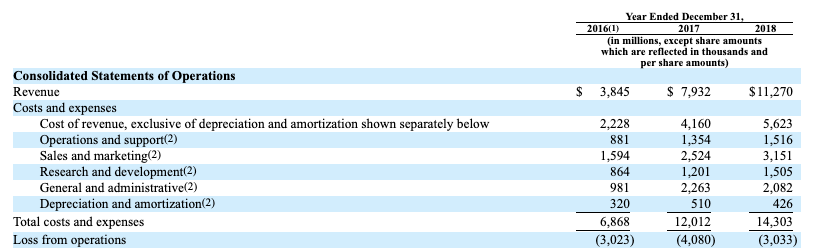

Here are Uber’s profit and loss numbers from their S1:

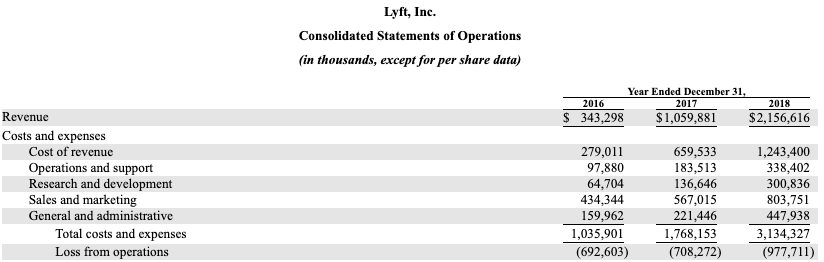

We can compare this to Lyft’s profit and loss from my prior blog post:

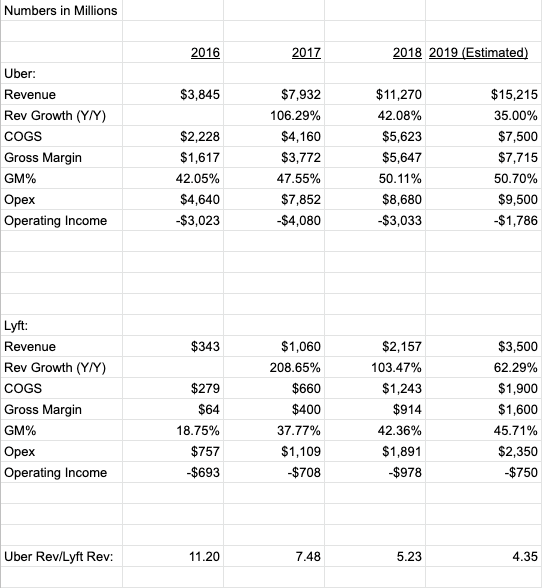

I put all of these numbers into a spreadsheet and added some estimates for 2019 that are nothing more than back of envelope guesstimates.

What you can see from this is that Uber is 4-5x larger than Lyft, growing a lot more slowly, has slightly better gross margins, and both are still losing a lot of money but both are moving towards getting profitable on operations in a few years.

Finally lets look at market valuations. Lyft is currently trading at a market cap of $17bn. If you say that Uber is 4-5x larger than Lyft, then Uber ought to be worth in the range of $70bn to $85bn.

There are other factors that will be in play when Uber eventually prices their IPO and trades. Uber owns minority interests in a number of other ridesharing businesses that could be worth as much as $10bn of additional value. On the other hand, Lyft is growing more quickly than Uber.

Ultimately we will see how the market values Uber. But from this analysis, and the public market comparables from Lyft, we can see that Uber should be worth quite a bit when it goes public.

Interoperability of state and value is likely to place downward price pressure on layer-1 blockchains that have no monetary premium, while enabling strong middleware protocols to achieve cross-chain, winner-takes-most dominance in their respective services. While not a perfect mapping to traditional use of the term middleware, these protocols can be thought of as anything sitting just below the interface layer (i.e., the applications the end user interacts with), but leveraging the lower-level functionality provided by layer-1 blockchains and interoperability protocols.

Others have called these service-layer protocols, as they focus on providing a specific service to the interface layer, be they financial, social, technological, etc. Financial services include things like exchange, lending, and risk-management; social services offer functionality like voting structures, arbitration, or legal-contract management; technological services include components like caching, storage, location, and maybe the granddaddy of them all, a unified OS for protocol services to be neatly bundled to the interface layer.

Financial-service protocols that Placeholder has invested in include 0x, Erasure, MakerDAO, and UMA, while Aragon is our main social-service protocol to date, and technological-service protocols that we work with include CacheCash, Filecoin, FOAM, and Zeppelin. All of these protocols have originated on Ethereum, but we believe interoperability of state and value—the promise of a Cosmos, Polkadot, and Ethereum 2.0 future—will allow these protocols to become horizontally defensible starting from Ethereum’s base.

Take MakerDAO, for example. Its token, MKR, can be thought of as an insurance pool for secured loans originated through the platform. The larger the overall value of MKR, the greater the insurance and therefore lower the risk for all users of the system. Let’s say FakerDAO pops up on Tron, providing the exact same service, but with its own native governance asset, FKR. Right now, it would be hard for the Maker team to leverage the value in MKR to secure a parallel system on Tron, but with interoperability of state and value it would become considerably easier.

Assuming the Maker team can build out for Tron before FKR gets to a similar value as MKR, then they should be able to deploy on Tron and provide a lower risk service than FakerDAO can, insured by the much larger pool of value stored in MKR. With two communities driving utility through MakerDAO, MKR’s pooled value is then likely to significantly outpace FKR’s, further widening the risk and quality of service-gap (Whether MKR holders would want to underwrite the risk of operating on another chain like Tron is a separate question).

We believe similar dynamics will play out for many other middleware protocols, though in different ways depending on the cryptoeconomic [1] and governance design of the system. Protocols whose reliability, security, speed, liquidity, or coverage scales with the size of the asset base and nodes supporting it, stand to do well in an interoperable world.

* * *

Footnotes:

[1] Most middleware protocols are likely to employ some variant of a capital asset as their cryptoeconomic model, where supply-siders must stake the asset to provide the service, giving them access to value-flows for so doing.

Sidenote: After viewing what we hold, some have asked why ether isn’t included. While we are fans of the Ethereum team, and think that people underestimate the soft-network effects of the system, we don’t hold ether (or any layer-1 smart contract blockchain) in part for the above reasons. We believe the middleware protocols we’ve invested in give us upside exposure to ether (if ETH appreciates in fiat terms then the quality assets that ride atop it tend to also appreciate in fiat terms, holding their value relative to ETH), while also protecting us from the downside exposure should more dominant layer-1 smart contract blockchains, or interoperability protocols, start to steal from ether’s value.

Facebook, believe it or not, has actually made virtual reality better, at least from one perspective.

My first VR device was PlayStation VR, and the calculus was straightforward: I owned a PS4 and did not own a Windows PC, which means I had a device that was compatible with the PlayStation VR and did not have one that was compatible with the Oculus Rift or the HTC Vive.

I used it exactly once.

The problem is that actually hooking up the VR headset was way too complicated with way too many wires, and given that I lived at the time in a relatively small apartment, it wasn’t viable to leave the entire thing hooked up when I wasn’t using it. I did finally move to a new place, but frankly, I can’t remember if I unpacked it or not.

Then, earlier this year, Facebook came out with the Oculus Go.

The Go sported hardware that was about the level of a mid-tier smartphone, and priced to match: $199. Critically, it was a completely standalone device: no console or PC necessary. Sure, the quality wasn’t nearly as good, but convenience matters a lot, particularly for someone like me who only occasionally plays video games or watches TV or movies. Putting on a wingsuit or watching some NBA highlights is surprisingly fun, and critically, easy. At least as long as I have the Go out of course, and charged. It’s hard to imagine giving it a second thought otherwise.

The Virtual Reality Niche

That is the first challenge of virtual reality: it is a destination, both in terms of a place you go virtually, but also, critically, the end result of deliberative actions in the real world. One doesn’t experience virtual reality by accident: it is a choice, and often — like in the case of my PlayStation VR — a rather complicated one.

That is not necessarily a problem: going to see a movie is a choice, as is playing a video game on a console or PC. Both are very legitimate ways to make money: global box office revenue in 2017 was $40.6 billion U.S., and billions more were made on all the other distribution channels in a movie’s typical release window; video games have long since been an even bigger deal, generating $109 billion globally last year.

Still, that is an order of magnitude less than the amount of revenue generated by something like smartphones. Apple, for example, sold $158 billion worth of iPhones over the last year; the entire industry was worth around $478.7 billion in 2017. The disparity should not come as a surprise: unlike movies or video games, smartphones are an accompaniment on your way to a destination, not a destination in and of themselves.

That may seem counterintuitive at first: isn’t it a good thing to be the center of one’s attention? That center, though, can only ever be occupied by one thing, and the addressable market is constrained by time. Assume eight hours for sleep, eight for work, a couple of hours for, you know, actually navigating life, and that leaves at best six hours to fight for. That is why devices intended to augment life, not replace it, have always been more compelling: every moment one is awake is worth addressing.

In other words, the virtual reality market is fundamentally constrained by its very nature: because it is about the temporary exit from real life, not the addition to it, there simply isn’t nearly as much room for virtual reality as there is for any number of other tech products.

Facebook’s Head-scratching Acquisition

This, incidentally, includes Facebook: the strength of the social network is counterintuitive like virtual reality is counterintuitive, but in the exact opposite way. No one plans to visit Facebook: who among us has “Facebook Time” set on our calendar? And yet the vast majority of people who are able — over 2 billion worldwide — visit Facebook every single day, for minutes at a time.

The truth is that everyone has vast stretches of time between moments of intentionality: standing in line, riding the bus, using the bathroom. That is Facebook’s domain, and it is far more valuable than it might seem at first: not only is the sheer amount of time available more than you might think, it is also a time when the human mind is, by definition, less engaged; we visit Facebook seeking stimulation, and don’t much care if that stimulation comes from friends and family, desperate media companies, or advertisers that have paid for the right. And pay they have, to the tune of $48 billion over the last year — more than the global box office, and nearly half of total video game revenue.

What may surprise you is that Facebook landed on this gold mine somewhat by accident: at the beginning of this decade the company was desperately trying to build a platform, that is, a place where 3rd-party developers could build their own direct connections with customers. This has long been the stated goal of Silicon Valley visionaries, but generally speaking the pursuit of platforms has been a bit like declarations of disruption: widespread in rhetoric, but few and far between in reality.

So it was with Facebook: the company’s profitability and dramatic rise in valuation — the last three months notwithstanding — have been predicated on the company not being a platform, at least not one for 3rd-party developers. After all, to give space to 3rd-party developers is to not give space to advertisers, at least on mobile, and it is mobile that has provided, well, the platform for Facebook to fill those empty spaces. And, as I noted back in 2013, the mobile ad unit couldn’t be better.

This is why Facebook’s acquisition of Oculus back in 2014 was such a head-scratcher; I was immediately skeptical, writing in Face Is Not the Future:

Setting aside implementation details for a moment, it’s difficult to think of a bigger contrast than a watch and an Occulus headset that you, in the words of [Facebook CEO Mark] Zuckerberg, “put on in your home.” What makes mobile such a big deal relative to the PC is the fact it is with you everywhere. A virtual reality headset is actually a regression in which your computing experience is neatly segregated into something you do deliberately.

Zuckerberg, though, having first failed to build a platform on the PC, and then failing miserably with a phone, would not be satisfied with being merely an app; he would have his platform, and virtual reality would give him the occasion.

Our mission is to make the world more open and connected. For the past few years, this has mostly meant building mobile apps that help you share with the people you care about. We have a lot more to do on mobile, but at this point we feel we’re in a position where we can start focusing on what platforms will come next to enable even more useful, entertaining and personal experiences…

This is a fascinating statement in retrospect. Of course there is the blithe dismissal of mobile, which would increase Facebook’s valuation tenfold, because Facebook was only an app, not a platform. More striking, though, is Zuckerberg’s evaluation that Facebook was now in a position to focus elsewhere: after the revelations of state-sponsored interference and legitimate questions about Facebook’s impact on society broadly it seems rather misguided.

Oculus’s mission is to enable you to experience the impossible. Their technology opens up the possibility of completely new kinds of experiences. Immersive gaming will be the first, and Oculus already has big plans here that won’t be changing and we hope to accelerate. The Rift is highly anticipated by the gaming community, and there’s a lot of interest from developers in building for this platform. We’re going to focus on helping Oculus build out their product and develop partnerships to support more games. Oculus will continue operating independently within Facebook to achieve this.

This is related to the reasons why Oculus and Facebook are in the news this week; TechCrunch reported that Oculus co-founder Brendan Iribe left the company because of a dispute about the next-generation of computer-based VR headsets; Facebook said that computer-based VR was still a part of future plans.

But this is just the start. After games, we’re going to make Oculus a platform for many other experiences…This is really a new communication platform. By feeling truly present, you can share unbounded spaces and experiences with the people in your life. Imagine sharing not just moments with your friends online, but entire experiences and adventures. These are just some of the potential uses. By working with developers and partners across the industry, together we can build many more. One day, we believe this kind of immersive, augmented reality will become a part of daily life for billions of people.

This, though, makes one think that TechCrunch was on to something. Microsoft, to its dismay, found out with the Xbox One that serving gamers and serving consumers generally are two very different propositions, and any move perceived by the former to be in favor of the latter will hurt sales specifically and the development of a thriving ecosystem generally. The problem for Facebook, though, is that the fundamental nature of the company — not to mention Zuckerberg’s platform ambitions — rely on serving as many customers as possible.

I suspect that wasn’t the top priority of Oculus’s founders: virtual reality is a hard problem, one where even the best technology — which unquestionably, means connecting to a PC — is not good enough. To that end, given that their priority was virtual reality first and reach second, I suspect Oculus’ founders would rather be spending more time making PC virtual reality better and less time selling warmed over smartphone innards.

The Problems with Facebook and Oculus

Still, I can’t deny that the Oculus Go, underpowered though it may be, is nicer to use in important ways — particularly convenience — that are serially undervalued by technologists. As I noted at the beginning, Facebook’s influence, particularly its desire to reach as many users as possible and control the entire experience — two desires that are satisfied with a standalone device — may indeed make virtual reality more widespread than it might have been had Oculus remained an independent company.

What is inevitable though — what was always inevitable, from the day Facebook bought Oculus — is that this will be one acquisition Facebook made that was a mistake. If Facebook wanted a presence in virtual reality the best possible route was the same it took in mobile: to be an app-exposed service, available on all devices, funded by advertising. I have long found it distressing that Zuckerberg, not just in 2014, but even today, judging by his comments in keynotes and on earnings calls, seems unable or unwilling to accept this fundamental truth about Facebook’s place in tech’s value chain.

In fact, Zuckerberg’s rhetoric around virtual reality has betrayed more than a lack of strategic sense: his keynote at the Oculus developer conference in 2016, a month before the last election, was, in retrospect, an advertisement of the company’s naïveté regarding its impact on the world:

We’re here to make virtual reality the next major computing platform. At Facebook, this is something we’re really committed to. You know, I’m an engineer, and I think a key part of the engineering mindset is this hope and this belief that you can take any system that’s out there and make it much much better than it is today. Anything, whether it’s hardware, or software, a company, a developer ecosystem, you can take anything and make it much, much better. And as I look out today, I see a lot of people who share this engineering mindset. And we all know where we want to improve and where we want virtual reality to eventually get…

I wrote at the time:

Perhaps I underestimated Zuckerberg: he doesn’t want a platform for the sake of having a platform, and his focus is not necessarily on Facebook the business. Rather, he seems driven to create utopia: a world that is better in every possible way than the one we currently inhabit. And, granted, owning a virtual reality company is perhaps the most obvious route to getting there…

Needless to say, 2016 suggests that the results of this approach are not very promising: when our individual realities collide in the real world the results are incredibly destructive to the norms that hold societies together. Make no mistake, Zuckerberg gave an impressive demo of what can happen when Facebook controls your eyes in virtual reality; what concerns me is the real world results of Facebook controlling everyone’s attention with the sole goal of telling each of us what we want to hear.

The following years have only borne out the validity of this analysis: of all the myriad of problems faced by Facebook — some warranted, and some unfair — the most concerning is the seeming inability of the company to even countenance the possibility that it is not an obvious force for good.

Facebook’s Mismatch

Again, though, Facebook aside, virtual reality is more compelling than you might think. There are some experiences that really are better in the fully immersive environment provided by virtual reality, and just because the future is closer to game consoles (at best) than to smartphones is nothing to apologize for. What remains more compelling, though, is augmented reality: the promise is that, like smartphones, it is an accompaniment to your day, not the center, which means its potential usefulness is far greater. To that end, you can be sure that any Facebook executive would be happy to explain why virtual reality and Oculus is a step in that direction.

That may be true technologically, but again, the fundamental nature of the service and the business model are all wrong. Anything made by Facebook is necessarily biased towards being accessible by everyone, which is a problem when creating a new market. Before technology is mature integrated products advance more rapidly, and can be sold at a premium; it follows that market makers are more likely to have hardware-based business models that segment the market, not service-based ones that try and reach everyone.

To that end, it is hard to not feel optimistic about Apple’s chances at eventually surpassing Oculus and everyone else. The best way to think about Apple has always been as a personal computer company; the only difference over time is that computers have grown ever more personal, moving from the desk to the lap to the pocket and today to the wrist (and ears). The face is a logical next step, and no company has proven itself better at the sort of hardware engineering necessary to make it happen.

Critically, Apple also has the right business model: it can sell barely good-enough devices at a premium to a userbase that will buy simply because they are from Apple, and from there figure out a use case without the need to reach everyone. I was very critical of this approach with the Apple Watch — it was clear from the launch keynote that Apple had no idea what this cool piece of hardware engineering would be used for — but, as the Apple Watch has settled into its niche as a health and fitness device and slowly expanded from there, I am more appreciative of the value of simply shipping a great piece of hardware and letting the real world figure it out.

That there gets at Facebook’s fundamental problem: the company is starting with a use case — social networking, or “connecting people” to use their favored phrase — and backing out to hardware and business models. It is an overly prescriptive approach that is exactly what you would expect from an app-enabled service, and the opposite of what you would expect from an actual platform. In other words, to be a platform is not a choice; it is destiny, and Facebook’s has always run in a different direction.

Convolution is probably the most important concept in deep learning right now. It was convolution and convolutional nets that catapulted deep learning to the forefront of almost any machine learning task there is. But what makes convolution so powerful? How does it work? In this blog post I will explain convolution and relate it to other concepts that will help you to understand convolution thoroughly.

There are already some blog post regarding convolution in deep learning, but I found all of them highly confusing with unnecessary mathematical details that do not further the understanding in any meaningful way. This blog post will also have many mathematical details, but I will approach them from a conceptual point of view where I represent the underlying mathematics with images everybody should be able to understand. The first part of this blog post is aimed at anybody who wants to understand the general concept of convolution and convolutional nets in deep learning. The second part of this blog post includes advanced concepts and is aimed to further and enhance the understanding of convolution for deep learning researchers and specialists.

What is convolution?

This whole blog post will build up to answer exactly this question, but it may be very helpful to first understand in which direction this is going, so what is convolution in rough terms?

You can imagine convolution as the mixing of information. Imagine two buckets full of information which are poured into one single bucket and then mixed according to a specific rule. Each bucket of information has its own recipe, which describes how the information in one bucket mixes with the other. So convolution is an orderly procedure where two sources of information are intertwined.

Convolution can also be described mathematically, in fact, it is a mathematical operation like addition, multiplication or a derivative, and while this operation is complex in itself, it can be very useful to simplify even more complex equations. Convolutions are heavily used in physics and engineering to simplify such complex equations and in the second part — after a short mathematical development of convolution — we will relate and integrate ideas between these fields of science and deep learning to gain a deeper understanding of convolution. But for now we will look at convolution from a practical perspective.

How do we apply convolution to images?

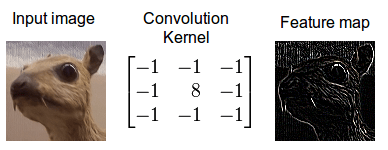

When we apply convolution to images, we apply it in two dimensions — that is the width and height of the image. We mix two buckets of information: The first bucket is the input image, which has a total of three matrices of pixels — one matrix each for the red, blue and green color channels; a pixel consists of an integer value between 0 and 255 in each color channel. The second bucket is the convolution kernel, a single matrix of floating point numbers where the pattern and the size of the numbers can be thought of as a recipe for how to intertwine the input image with the kernel in the convolution operation. The output of the kernel is the altered image which is often called a feature map in deep learning. There will be one feature map for every color channel.

Convolution of an image with an edge detector convolution kernel. Sources: 12

We now perform the actual intertwining of these two pieces of information through convolution. One way to apply convolution is to take an image patch from the input image of the size of the kernel — here we have a 100×100 image, and a 3×3 kernel, so we would take 3×3 patches — and then do an element wise multiplication with the image patch and convolution kernel. The sum of this multiplication then results in one pixel of the feature map. After one pixel of the feature map has been computed, the center of the image patch extractor slides one pixel into another direction, and repeats this computation. The computation ends when all pixels of the feature map have been computed this way. This procedure is illustrated for one image patch in the following gif.

Convolution operation for one pixel of the resulting feature map: One image patch (red) of the original image (RAM) is multiplied by the kernel, and its sum is written to the feature map pixel (Buffer RAM). Gif by Glen Williamson who runs a website that features many technical gifs.

As you can see there is also a normalization procedure where the output value is normalized by the size of the kernel (9); this is to ensure that the total intensity of the picture and the feature map stays the same.

Why is convolution of images useful in machine learning?

There can be a lot of distracting information in images that is not relevant to what we are trying to achieve. A good example of this is a project I did together with Jannek Thomas in the Burda Bootcamp. The Burda Bootcamp is a rapid prototyping lab where students work in a hackathon-style environment to create technologically risky products in very short intervals. Together with my 9 colleagues, we created 11 products in 2 months. In one project I wanted to build a fashion image search with deep autoencoders: You upload an image of a fashion item and the autoencoder should find images that contain clothes with similar style.

Now if you want to differentiate between styles of clothes, the colors of the clothes will not be that useful for doing that; also minute details like emblems of the brand will be rather unimportant. What is most important is probably the shape of the clothes. Generally, the shape of a blouse is very different from the shape of a shirt, jacket, or trouser. So if we could filter the unnecessary information out of images then our algorithm will not be distracted by the unnecessary details like color and branded emblems. We can achieve this easily by convoluting images with kernels.

My colleague Jannek Thomas preprocessed the data and applied a Sobel edge detector (similar to the kernel above) to filter everything out of the image except the outlines of the shape of an object — this is why the application of convolution is often called filtering, and the kernels are often called filters (a more exact definition of this filtering processes will follow below). The resulting feature map from the edge detector kernel will be very helpful if you want to differentiate between different types of clothes, because only relevant shape information remains.

Sobel filtered inputs to and results from the trained autoencoder: The top-left image is the search query and the other images are the results which have an autoencoder code that is most similar to the search query as measured by cosine similarity. You see that the autoencoder really just looks at the shape of the search query and not its color. However, you can also see that this procedure does not work well for images of people wearing clothes (5th column) and that it is sensitive to the shapes of clothes hangers (4th column).

We can take this a step further: There are dozens of different kernels which produce many different feature maps, e.g. which sharpen the image (more details), or which blur the image (less details), and each feature map may help our algorithm to do better on its task (details, like 3 instead of 2 buttons on your jacket might be important).

Using this kind of procedure — taking inputs, transforming inputs and feeding the transformed inputs to an algorithm — is called feature engineering. Feature engineering is very difficult, and there are little resources which help you to learn this skill. In consequence, there are very few people which can apply feature engineering skillfully to a wide range of tasks. Feature engineering is — hands down — the most important skill to score well in Kaggle competitions. Feature engineering is so difficult because for each type of data and each type of problem, different features do well: Knowledge of feature engineering for image tasks will be quite useless for time series data; and even if we have two similar image tasks, it will not be easy to engineer good features because the objects in the images also determine what will work and what will not. It takes a lot of experience to get all of this right.

So feature engineering is very difficult and you have to start from scratch for each new task in order to do well. But when we look at images, might it be possible to automatically find the kernels which are most suitable for a task?

Enter convolutional nets

Convolutional nets do exactly this. Instead of having fixed numbers in our kernel, we assign parameters to these kernels which will be trained on the data. As we train our convolutional net, the kernel will get better and better at filtering a given image (or a given feature map) for relevant information. This process is automatic and is called feature learning. Feature learning automatically generalizes to each new task: We just need to simply train our network to find new filters which are relevant for the new task. This is what makes convolutional nets so powerful — no difficulties with feature engineering!

Usually we do not learn a single kernel in convolutional nets, instead we learn a hierarchy of multiple kernels at the same time. For example a 32x16x16 kernel applied to a 256×256 image would produce 32 feature maps of size 241×241 (this is the standard size, the size may vary from implementation to implementation; ). So automatically we learn 32 new features that have relevant information for our task in them. These feature then provide the inputs for the next kernel which filters the inputs again. Once we learned our hierarchical features, we simply pass them to a fully connected, simple neural network that combines them in order to classify the input image into classes. That is nearly all that there is to know about convolutional nets at a conceptual level (pooling procedures are important too, but that would be another blog post).

Part II: Advanced concepts

We now have a very good intuition of what convolution is, and what is going on in convolutional nets, and why convolutional nets are so powerful. But we can dig deeper to understand what is really going on within a convolution operation. In doing so, we will see that the original interpretation of computing a convolution is rather cumbersome and we can develop more sophisticated interpretations which will help us to think about convolutions much more broadly so that we can apply them on many different data. To achieve this deeper understanding the first step is to understand the convolution theorem.

The convolution theorem

To develop the concept of convolution further, we make use of the convolution theorem, which relates convolution in the time/space domain — where convolution features an unwieldy integral or sum — to a mere element wise multiplication in the frequency/Fourier domain. This theorem is very powerful and is widely applied in many sciences. The convolution theorem is also one of the reasons why the fast Fourier transform (FFT) algorithm is thought by some to be one of the most important algorithms of the 20th century.

The first equation is the one dimensional continuous convolution theorem of two general continuous functions; the second equation is the 2D discrete convolution theorem for discrete image data. Here denotes a convolution operation, denotes the Fourier transform, the inverse Fourier transform, and is a normalization constant. Note that “discrete” here means that our data consists of a countable number of variables (pixels); and 1D means that our variables can be laid out in one dimension in a meaningful way, e.g. time is one dimensional (one second after the other), images are two dimensional (pixels have rows and columns), videos are three dimensional (pixels have rows and columns, and images come one after another).

To get a better understanding what happens in the convolution theorem we will now look at the interpretation of Fourier transforms with respect to digital image processing.

Fast Fourier transforms

The fast Fourier transform is an algorithm that transforms data from the space/time domain into the frequency or Fourier domain. The Fourier transform describes the original function in a sum of wave-like cosine and sine terms. It is important to note, that the Fourier transform is generally complex valued, which means that a real value is transformed into a complex value with a real and imaginary part. Usually the imaginary part is only important for certain operations and to transform the frequencies back into the space/time domain and will be largely ignored in this blog post. Below you can see a visualization how a signal (a function of information often with a time parameter, often periodic) is transformed by a Fourier transform.

Transformation of the time domain (red) into the frequency domain (blue). Source

You may be unaware of this, but it might well be that you see Fourier transformed values on a daily basis: If the red signal is a song then the blue values might be the equalizer bars displayed by your mp3 player.

How can we imagine frequencies for images? Imagine a piece of paper with one of the two patterns from above on it. Now imagine a wave traveling from one edge of the paper to the other where the wave pierces through the paper at each stripe of a certain color and hovers over the other. Such waves pierce the black and white parts in specific intervals, for example, every two pixels — this represents the frequency. In the Fourier transform lower frequencies are closer to the center and higher frequencies are at the edges (the maximum frequency for an image is at the very edge). The location of Fourier transform values with high intensity (white in the images) are ordered according to the direction of the greatest change in intensity in the original image. This is very apparent from the next image and its log Fourier transforms (applying the log to the real values decreases the differences in pixel intensity in the image — we see information more easily this way).

We immediately see that a Fourier transform contains a lot of information about the orientation of an object in an image. If an object is turned by, say, 37% degrees, it is difficult to tell that from the original pixel information, but very clear from the Fourier transformed values.

This is an important insight: Due to the convolution theorem, we can imagine that convolutional nets operate on images in the Fourier domain and from the images above we now know that images in that domain contain a lot of information about orientation. Thus convolutional nets should be better than traditional algorithms when it comes to rotated images and this is indeed the case (although convolutional nets are still very bad at this when we compare them to human vision).

Frequency filtering and convolution

The reason why the convolution operation is often described as a filtering operation, and why convolution kernels are often named filters will be apparent from the next example, which is very close to convolution.

If we transform the original image with a Fourier transform and then multiply it by a circle padded by zeros (zeros=black) in the Fourier domain, we filter out all high frequency values (they will be set to zero, due to the zero padded values). Note that the filtered image still has the same striped pattern, but its quality is much worse now — this is how jpeg compression works (although a different but similar transform is used), we transform the image, keep only certain frequencies and transform back to the spatial image domain; the compression ratio would be the size of the black area to the size of the circle in this example.

If we now imagine that the circle is a convolution kernel, then we have fully fledged convolution — just as in convolutional nets. There are still many tricks to speed up and stabilize the computation of convolutions with Fourier transforms, but this is the basic principle how it is done.

Now that we have established the meaning of the convolution theorem and Fourier transforms, we can now apply this understanding to different fields in science and enhance our interpretation of convolution in deep learning.

Insights from fluid mechanics

Fluid mechanics concerns itself with the creation of differential equation models for flows of fluids like air and water (air flows around an airplane; water flows around suspended parts of a bridge). Fourier transforms not only simplify convolution, but also differentiation, and this is why Fourier transforms are widely used in the field of fluid mechanics, or any field with differential equations for that matter. Sometimes the only way to find an analytic solution to a fluid flow problem is to simplify a partial differential equation with a Fourier transform. In this process we can sometimes rewrite the solution of such a partial differential equation in terms of a convolution of two functions which then allows for very easy interpretation of the solution. This is the case for the diffusion equation in one dimension, and for some two dimensional diffusion processes for functions in cylindrical or spherical polar coordinates.

Diffusion

You can mix two fluids (milk and coffee) by moving the fluid with an outside force (mixing with a spoon) — this is called convection and is usually very fast. But you could also wait and the two fluids would mix themselves on their own (if it is chemically possible) — this is called diffusion and is usually a very slow when compared to convection.

Imagine an aquarium that is split into two by a thin, removable barrier where one side of the aquarium is filled with salt water, and the other side with fresh water. If you now remove the thin barrier carefully, the two fluids will mix together until the whole aquarium has the same concentration of salt everywhere. This process is more “violent” the greater the difference in saltiness between the fresh water and salt water.

Now imagine you have a square aquarium with 256×256 thin barriers that separate 256×256 cubes each with different salt concentration. If you remove the barrier now, there will be little mixing between two cubes with little difference in salt concentration, but rapid mixing between two cubes with very different salt concentrations. Now imagine that the 256×256 grid is an image, the cubes are pixels, and the salt concentration is the intensity of each pixel. Instead of diffusion of salt concentrations we now have diffusion of pixel information.

It turns out, this is exactly one part of the convolution for the diffusion equation solution: One part is simply the initial concentrations of a certain fluid in a certain area — or in image terms — the initial image with its initial pixel intensities. To complete the interpretation of convolution as a diffusion process we need to interpret the second part of the solution to the diffusion equation: The propagator.

Interpreting the propagator

The propagator is a probability density function, which denotes into which direction fluid particles diffuse over time. The problem here is that we do not have a probability function in deep learning, but a convolution kernel — how can we unify these concepts?

We can apply a normalization that turns the convolution kernel into a probability density function. This is just like computing the softmax for output values in a classification tasks. Here the softmax normalization for the edge detector kernel from the first example above.

Softmax of an edge detector: To calculate the softmax normalization, we taking each value [latex background="ffffff"]{x}[/latex] of the kernel and apply [latex background="ffffff"]{e^x}[/latex]. After that we divide by the sum of all [latex background="ffffff"]{e^x}[/latex]. Please note that this technique to calculate the softmax will be fine for most convolution kernels, but for more complex data the computation is a bit different to ensure numerical stability (floating point computation is inherently unstable for very large and very small values and you have to carefully navigate around troubles in this case).

Now we have a full interpretation of convolution on images in terms of diffusion. We can imagine the operation of convolution as a two part diffusion process: Firstly, there is strong diffusion where pixel intensities change (from black to white, or from yellow to blue, etc.) and secondly, the diffusion process in an area is regulated by the probability distribution of the convolution kernel. That means that each pixel in the kernel area, diffuses into another position within the kernel according to the kernel probability density.

For the edge detector above almost all information in the surrounding area will concentrate in a single space (this is unnatural for diffusion in fluids, but this interpretation is mathematically correct). For example all pixels that are under the 0.0001 values, will very likely flow into the center pixel and accumulate there. The final concentration will be largest where the largest differences between neighboring pixels are, because here the diffusion process is most marked. In turn, the greatest differences in neighboring pixels is there, where the edges between different objects are, so this explains why the kernel above is an edge detector.

So there we have it: Convolution as diffusion of information. We can apply this interpretation directly on other kernels. Sometimes we have to apply a softmax normalization for interpretation, but generally the numbers in itself say a lot about what will happen. Take the following kernel for example. Can you now interpret what that kernel is doing? Click hereto find the solution (there is a link back to this position).

Wait, there is something fishy here

How come that we have deterministic behavior if we have a convolution kernel with probabilities? We have to interpret that single particles diffuse according to the probability distribution of the kernel, according to the propagator, don’t we?

Yes, this is indeed true. However, if you take a tiny piece of fluid, say a tiny drop of water, you still have millions of water molecules in that tiny drop of water, and while a single molecule behaves stochastically according to the probability distribution of the propagator, a whole bunch of molecules have quasi deterministic behavior —this is an important interpretation from statistical mechanics and thus also for diffusion in fluid mechanics. We can interpret the probabilities of the propagator as the average distribution of information or pixel intensities; Thus our interpretation is correct from a viewpoint of fluid mechanics. However, there is also a valid stochastic interpretation for convolution.

Insights from quantum mechanics

The propagator is an important concept in quantum mechanics. In quantum mechanics a particle can be in a superposition where it has two or more properties which usually exclude themselves in our empirical world: For example, in quantum mechanics a particle can be at two places at the same time — that is a single object in two places.

However, when you measure the state of the particle — for example where the particle is right now — it will be either at one place or the other. In other terms, you destroy the superposition state by observation of the particle. The propagator then describes the probability distribution where you can expect the particle to be. So after measurement a particle might be — according to the probability distribution of the propagator — with 30% probability in place A and 70% probability in place B.

If we have entangled particles (spooky action at a distance), a few particles can hold hundreds or even millions of different states at the same time — this is the power promised by quantum computers.

So if we use this interpretation for deep learning, we can think that the pixels in an image are in a superposition state, so that in each image patch, each pixel is in 9 positions at the same time (if our kernel is 3×3). Once we apply the convolution we make a measurement and the superposition of each pixel collapses into a single position as described by the probability distribution of the convolution kernel, or in other words: For each pixel, we choose one pixel of the 9 pixels at random (with the probability of the kernel) and the resulting pixel is the average of all these pixels. For this interpretation to be true, this needs to be a true stochastic process, which means, the same image and the same kernel will generally yield different results. This interpretation does not relate one to one to convolution but it might give you ideas how to the apply convolution in stochastic ways or how to develop quantum algorithms for convolutional nets. A quantum algorithm would be able to calculate all possible combinations described by the kernel with one computation and in linear time/qubits with respect to the size of image and kernel.

Insights from probability theory

Convolution is closely related to cross-correlation. Cross-correlation is an operation which takes a small piece of information (a few seconds of a song) to filter a large piece of information (the whole song) for similarity (similar techniques are used on youtube to automatically tag videos for copyrights infringements).

Relation between cross-correlation and convolution: Here [latex background="ffffff"]{\star}[/latex] denotes cross correlation and [latex background="ffffff"]{f^*}[/latex] denotes the complex conjugate of [latex background="ffffff"]{f}[/latex].

While cross correlation seems unwieldy, there is a trick with which we can easily relate it to convolution in deep learning: For images we can simply turn the search image upside down to perform cross-correlation through convolution. When we perform convolution of an image of a person with an upside image of a face, then the result will be an image with one or multiple bright pixels at the location where the face was matched with the person.

Cross-correlation via convolution: The input and kernel are padded with zeros and the kernel is rotated by 180 degrees. The white spot marks the area with the strongest pixel-wise correlation between image and kernel. Note that the output image is in the spatial domain, the inverse Fourier transform was already applied. Images taken from Steven Smith’s excellent free online book about digital signal processing.

This example also illustrates padding with zeros to stabilize the Fourier transform and this is required in many version of Fourier transforms. There are versions which require different padding schemes: Some implementation warp the kernel around itself and require only padding for the kernel, and yet other implementations perform divide-and-conquer steps and require no padding at all. I will not expand on this; the literature on Fourier transforms is vast and there are many tricks to be learned to make it run better — especially for images.

At lower levels, convolutional nets will not perform cross correlation, because we know that they perform edge detection in the very first convolutional layers. But in later layers, where more abstract features are generated, it is possible that a convolutional net learns to perform cross-correlation by convolution. It is imaginable that the bright pixels from the cross-correlation will be redirected to units which detect faces (the Google brain project has some units in its architecture which are dedicated to faces, cats etc.; maybe cross correlation plays a role here?).

Insights from statistics

What is the difference between statistical models and machine learning models? Statistical models often concentrate on very few variables which can be easily interpreted. Statistical models are built to answer questions: Is drug A better than drug B?

Machine learning models are about predictive performance: Drug A increases successful outcomes by 17.83% with respect to drug B for people with age X, but 22.34% for people with age Y.

Machine learning models are often much more powerful for prediction than statistical models, but they are not reliable. Statistical models are important to reach accurate and reliable conclusions: Even when drug A is 17.83% better than drug B, we do not know if this might be due to chance or not; we need statistical models to determine this.

Two important statistical models for time series data are the weighted moving average and the autoregressive models which can be combined into the ARIMA model (autoregressive integrated moving average model). ARIMA models are rather weak when compared to models like long short-term recurrent neural networks, but ARIMA models are extremely robust when you have low dimensional data (1-5 dimensions). Although their interpretation is often effortful, ARIMA models are not a blackbox like deep learning algorithms and this is a great advantage if you need very reliable models.

It turns out that we can rewrite these models as convolutions and thus we can show that convolutions in deep learning can be interpreted as functions which produce local ARIMA features which are then passed to the next layer. This idea however, does not overlap fully, and so we must be cautious and see when we really can apply this idea.

Here is a constant function which takes the kernel as parameter; white noise is data with mean zero, a standard deviation of one, and each variable is uncorrelated with respect to the other variables.

When we pre-process data we make it often very similar to white noise: We often center it around zero and set the variance/standard deviation to one. Creating uncorrelated variables is less often used because it is computationally intensive, however, conceptually it is straight forward: We reorient the axes along the eigenvectors of the data.

Decorrelation by reorientation along eigenvectors: The eigenvectors of this data are represented by the arrows. If we want to decorrelate the data, we reorient the axes to have the same direction as the eigenvectors. This technique is also used in PCA, where the dimensions with the least variance (shortest eigenvectors) are dropped after reorientation.

Now, if we take to be the bias, then we have an expression that is very similar to a convolution in deep learning. So the outputs from a convolutional layer can be interpreted as outputs from an autoregressive model if we pre-process the data to be white noise.

The interpretation of the weighted moving average is simple: It is just standard convolution on some data (input) with a certain weight (kernel). This interpretation becomes clearer when we look at the Gaussian smoothing kernel at the end of the page. The Gaussian smoothing kernel can be interpreted as a weighted average of the pixels in each pixel’s neighborhood, or in other words, the pixels are averaged in their neighborhood (pixels “blend in”, edges are smoothed).

While a single kernel cannot create both, autoregressive and weighted moving average features, we usually have multiple kernels and in combination all these kernels might contain some features which are like a weighted moving average model and some which are like an autoregressive model.

Conclusion

In this blog post we have seen what convolution is all about and why it is so powerful in deep learning. The interpretation of image patches is easy to understand and easy to compute but it has many conceptual limitations. We developed convolutions by Fourier transforms and saw that Fourier transforms contain a lot of information about orientation of an image. With the powerful convolution theorem we then developed an interpretation of convolution as the diffusion of information across pixels. We then extended the concept of the propagator in the view of quantum mechanics to receive a stochastic interpretation of the usually deterministic process. We showed that cross-correlation is very similar to convolution and that the performance of convolutional nets may depend on the correlation between feature maps which is induced through convolution. Finally, we finished with relating convolution to autoregressive and moving average models.

Personally, I found it very interesting to work on this blog post. I felt for long time that my undergraduate studies in mathematics and statistics were wasted somehow, because they were so unpractical (even though I study applied math). But later — like an emergent property — all these thoughts linked together and practically useful understanding emerged. I think this is a great example why one should be patient and carefully study all university courses — even if they seem useless at first.

Solution to the quiz above: The information diffuses nearly equally among all pixels; and this process will be stronger for neighboring pixels that differ more. This means that sharp edges will be smoothed out and information that is in one pixel, will diffuse and mix slightly with surrounding pixels. This kernel is known as a Gaussian blur or as Gaussian smoothing. Continue reading. Sources: 12

Image source reference

R. B. Fisher, K. Koryllos, “Interactive Textbooks; Embedding Image Processing Operator Demonstrations in Text”, Int. J. of Pattern Recognition and Artificial Intelligence, Vol 12, No 8, pp 1095-1123, 1998.

There is much talk these days that startup valuations have decreased and may continue to do so and that the amount of time it takes to fund raise may take longer. As I have pointed out in previous posts, 91% of VCs surveyed believe prices are declining (30% believe substantially) and 77% believe that funding will take longer than it has in the past.

This has led VC & entrepreneur bloggers alike to similar conclusions: start raising capital early and be careful about having too high of a burn rate because that lessens the amount of runway you have until you need more cash.

But the hardest question to actually answer is, “What is the right burn rate for your company?” and if anybody gives you a specific number I would be a bit skeptical because there is no universal answer. It’s a very personal topic and I’d like to offer you a framework to decide for yourself, based on the following factors:

How Long is it Taking to Raise Capital at Your Stage in the Market?

The earlier the round, the less capital you need and the more reasonable your valuation the less time that is needed generally to raise capital. In other words, raising $2 million at a $6 million pre-money valuation has always been easier & quicker than raising $20 million at any valuation.

I know it sounds obvious but just so you understand: There are more capital sources available for earlier-stage capital, the information on which they are evaluating the investment is less (it is almost certainly just team and product) and the risk of the investor getting things wrong is diminished. When you raise larger rounds there is more “due diligence,” which includes: calling customers, looking at financial metrics, doing cohort analysis (looking for trends like changes in churn rates), evaluating competitor positioning and understanding more of the competency of your executive team.

While there is no “one size fits all” I used to give the advice that you should plan about 4.5 months for fund raising start to finish and make sure you have at least 6 months of cash if it takes longer. In recent years it seems many deals got done in 2-3 months or shorter and that still may be true at the earliest stages.

My advice: be cautious, start early, get to know investors before you need capital, do your research on who is a likely good fit and understand that fund-raising is always part of your job – not something you do in “fund-raising season” for 2-3 months every other year. People who think of fund raising as a “distraction away from the core business” fundamentally don’t understand that running a business comprises of: Shipping products, selling to & servicing customers, marketing, HR, recruiting, financial reporting AND making sure you have enough money to support operations.

In other words, fund-raising is a permanent part of the job of the CEO (and CFO) of a company so whether you allocate 5% of your time to it or 20% – it is a year-round activity even if just in the background.

When you ask yourself how Uber became the powerhouse it is – in addition to great software & operations and the right innovation at the right time – it was also the fact that they knew how to constantly tap the capital markets to grow the business, making it harder for many competitors to do so.

Who are Your Existing Investors?

How much your company should burn should also have a direct correlation with who your existing investors are and I strongly advise that you have open conversations with them about their comfort levels and also the level of support you are likely to receive going forward. I’m surprised how few entrepreneurs have this open conversation with their investors.

In fact, most entrepreneurs I know don’t ask – why is that? Wouldn’t you rather know where you stand? There are ways to do this politely and even if your investors don’t answer as directly as you may like – there is at least something that can be read into this.

So. If you have a strong lead investor known for backing his or her entrepreneurs in tough times and that investor gives you a sense for her comfort level in writing your next check then you can have a higher burn rate than if you don’t feel you have a strong lead investor.

If you have mostly angels or don’t feel your existing investor can support you without new capital from the outside then you might want a smaller burn rate.

Remember those party rounds that became so popular over the past few years because they allowed higher prices and more favorable terms for entrepreneurs? Well if you took that option I would simply advise that you be a little bit more cautious with your burn rate. Here’s why: If you have 5 firms who each gave you $500k you have 3 distinct problems:

No one (or two) investor “owns” responsibility for helping make things better. You have a version of the Tragedy of the Commons in which no individual actor owns responsibility for making the shared resource better. The opposite of this is a strong lead who owns responsibility because of the Pottery-Barn Rule popularized by Colin Powell in which “you break it, you buy it (or own responsibility for fixing it).

With so little (relatively) at stake nobody has a strong economic incentive t make things better. If each firm is only in for $500k and things go wrong they don’t mind taking a write-off and the upside of making things better often isn’t worth it because their ownership is too small.

You also have the “free rider problem” because if 3 of the 5 parties are willing to support you and 2 aren’t (the free riders) often the 3 won’t want to bother or will want to recap the company because no investors like bailing out free riders. And recaps hurt founders so often people just avoid doing them. If they’re only 1 of 5 they might rather just take the write off.

Are Your Existing Investors Over Their Skis?

This is another thing I strongly advise entrepreneurs to understand and even talk with their VCs about. Let me play open book so you can understand the situation better.

At Upfront Ventures 90% of the first-check investments we do are seed or A-round (and 2/3rd of these are A-rounds) with about 10% of our first-checks (in number) being B-rounds. As a primarily A-round investor with a nearly $300 million fund our average first-check size is about $3.5 million. We invest about half of our fund in our initial investments and we “reserve” about 50% of our investments to follow on in our best deals.

Obviously if a company is doing phenomenally well we’ll try to invest more capital and if a company is taking time to mature we’ll be more cautious. But even companies that take time to mature will usually get at least a second check of support from us as long as they are showing strong signs of innovating and as long as we believe they are still committed to the long-term viability of the business and as long as they show financial prudence.

In our best deals we hope to invest $10-15 million over the life of the fund.

So if we’ve invested $3-4 million in your company there is a strong chance you will get some level of support from us because on a relative basis we are not “over committed” and even in tough times for you, allocating $1-2 million is part of our scope and strategy to get you through unforeseen situations.

If on the other hand we have committed $10 million and if you don’t have 3 other investors around the table and if you’re burning $800k / month (implying you need $10 million more to fund one-year’s operations or nearly $15 million to fund 18 months) – we’re simply “over our skis” in order to help you because we wouldn’t put $25 million in one company at our size fund. So even if we LOVE your business you are stretching our ability to fund you in tough times.

You ought to have a sense for your existing investors’ capacities relative to your company.

How Strong is Your Access to Capital?

Talking about existing investors is one way of talking about “access to capital” because if you already have VCs then you have “access.” And then you’re just assessing whether you can get access to new VCs or whether your existing VCs can help you in tough times.

I talk about “access to capital” in the context of fund raising because it is the biggest determinant of your likelihood of raising. If you went to Stanford with a bunch of VCs who you count as friends (and who respect you) plus you worked at the senior ranks of Facebook, Salesforce.com, Palantir or Uber – you have very strong access – obviously.

But many people aren’t in this situation. If your company has raised angel money and maybe some capital from seed funds that are less well known or are new – then your access to capital may be less strong.

What is Your Risk Appetite?

It is also impossible to tell you the right burn rate for your company without knowing your risk tolerance. Quite simply – some people would rather “go hard” and accept the consequence of failure if they don’t succeed. Other people are more cautious and have a lot more at stake if the company doesn’t succeed (like maybe they put in their own money or their family’s money).

So whenever people ask me for advice I normally start by asking:

How much time have you put into this company already?

How much money have you personally or your friends/family invested? Is that a lot for them?

How risk averse are you? Are you generally very cautious or prefer to “go all out for it or die trying?”

There is no right answer. Only you can know. But check your risk tolerance.

Again, I know this sounds very obvious but in practice it isn’t always. Some companies may be able to become “cockroaches” or “ramen profitable” but cutting costs and staff substantially and getting to a burn rate that last 2 years. But that could impact the future upside of the company. So you might have a company that is “medium valuable” in the long-run because with no capital it was hard to innovate and create a market leader. That’s ok for some entrepreneurs (and investor) and not for others.

Also. You may think that it’s ok to “cut to the bone” but you may find out that your team didn’t want to join that sort of company so you may cut back really far only to find that the remaining people leave. Simply put – if you’re going to cut to the bone make sure that the team you intend to keep is aligned culturally with this decision.

Being ramen profitable is the right decision for some team and the wrong decision for others. Only you know. Keep your burn rate in line with your: Access to capital & risk tolerance levels.

How Reasonable Was Your Last Valuation?

There are two other factors you may consider. One is how reasonable your last round valuation was. If you raised $10 million at a $40 million pre-money on a company with limited revenue and if your investors are telling you that they’re concerned about your future because they doubt that outsiders will fund you at your current performance level then I would be more cautious with my burn rate – even if it means slashing costs.

There are only four solutions to this problem:

Confirm inside support to continue funding you – even if outsiders won’t

Cut burn enough that you can eventually “grow into” your valuation; or

Adjust your valuation down proactively so that outsiders can still fund you at what the market considers a normal valuation for your stage & progress

Go hard and hope that the market will validate your innovation even if the price may be higher than the market may want to bear

How Complicated is Your Cap Table?

Cap Table issues are seldom understood by entrepreneurs. Again, my best advice is to talk with your VCs openly or at least the ones you trust the most to be open.

If you raised a $2 million seed round at a $6 million pre then a $5 million A-round at a $20 million pre then a $20 million B-round at a $80 million pre and if your company has stalled you may have a cap table problem. Let me explain.

The $20 million investor may now believe that you’re never going to be worth $300 million or more (they invested hoping for no less than a 3x). So if they’re in the mindset that they’re better off getting their $20 million back versus risking more capital then they may prefer just to sell your company for whatever you can get for it. Even if you sold for $20 million they’d be thinking “I have senior liquidation preference so I get my money back.”)

The early stage investor probably still owns 15% of your company and thought he or she had a great return coming (after all – it got marked up to $100 million post-money valuation just 12 months ago!). But they are “over their skis” on ability to help you because they’re an early-stage investor so they’re dependent on your B-round investor or outside money.

They don’t want you to sell for $20 million because they may still believe in you AND they know that they’ll get no return from this (and your personal return will be very small).

You are in a classic cap table pinch. You don’t even realize that the later-stage investor doesn’t support you any more.

Solution: For starters get your seed & A investors helping. They may be able to persuade your B-round investor to be more reasonable. They may push you to cut costs. They may suggest cap table adjustments as a compromise. Or they may ferret out that your B-round investor just won’t budge. But at least you’ll know where you stand before deciding what to do about burn.

Note that I’m not making any value judgments about seed, A or B (or C or growth) investors. Just trying to point out that at times they’re not always aligned and most entrepreneurs don’t understand this math.

Appendix:

As with yesterday I’m still at a soccer tournament with my son (he’s asleep – but we made the championship round!). So I have no time to edit or word check. I hope this post is at least helpful for those surveying what to do about burn rates and the market. And if I made mistakes or typos feel free to let me know and I’ll fix tomorrow.

At the Upfront Summit in early February, we had a chance to have many off-the-record conversations with Limited Partners (LPs) who fund Venture Capital (VC) funds about their views of the market. While I’m not an LP, the following post represents my discussions with more than 100 LP firms – specifically ones that do fund VCs – and full survey data from 73 firms, so I’ve tried to capture the essence of what I’ve learned.

We All Know That Dollars into Venture Have Gone Up …

As a starting point, we know that the dollars into venture have steadily rebounded to pre great-recession levels, with just under $30 billion committed to US technology venture capital in 2015. While there is much discussion about VCs starting to pull back on their investments into startups, the LPs we surveyed don’t expect to slow the pace of investment into VC funds themselves – at least for the foreseeable future.

…But LPs Have Been Putting Out More Money Than They Are Getting Back

LPs have been feeling great about venture capital due to holding valuable paper positions in companies like Uber, Lyft, Airbnb, Dropbox, all of which they feel confident will drive large cash distributions in the future. However, they have been sending VCs far more investment checks in the last ten years than they’ve gotten back as distributions. In fact, if you add the capital flows of the past ten years, there have been just shy of $50 billion in net cash outlays.

And that’s real cash that LPs can’t put to work in other asset classes. So one problem often not talked about is that if LPs don’t get money back and accumulate more cash outflows, eventually they will either have to pare back investments into venture or they’ll have to increase the percentage of dollars they allocate to venture (at the expense of other asset types).

LPs Still Believe Strongly in Venture Capital as a Diverse Source of Returns

The good news for our industry is that the LPs who fund the VC industry are still very big believers in the long-term gains they will get from venture and are still allocating capital to the industry in good times and bad. That’s money that fuels our startup ecosystems. In our poll of 73 LP funds, we saw only 7% who felt they were overweight in venture given the current market climate, versus 22% of the firms who are actually looking to grow their dollars in venture.

And while there is a narrative that most LPs only want to invest in the long-standing Silicon Valley brands that have existed for the past 40 years, there is evidence that many LPs understand that it is possible for new entrants in our industry to stake out grounds of differentiation. In just over a decade, new firms like USV, Foundry, Spark, True Ventures, First Round, Greycroft (I might add Upfront) have made names for themselves from a non-traditional Silicon Valley stance. More recently, Thrive, Homebrew, IA Ventures, K9, Social + Capital, Cowboy, SK Capital, Ludlow, Forerunner and many, many others have emerged as newly differentiated brands. There are so many I fear that listing a few will get me in trouble with the many I didn’t list. Sorry!

But here’s the chart that should hearten all new firms … 40% of LPs tell us that they’re looking to add new names to their rosters.

LPs See The Over-Valuations and Don’t Like It

All isn’t completely rosy in the LP views of the venture industry. LPs have followed the recent press about the over-valuation and over-funding of the startup industry, and they experience these phenomena first hand. Some 75% of LPs polled said they are concerned about investment pace, burn and valuations; for now, only 6% seem “deeply concerned.”

I suspect that over the next 18 months, they’ll see another phenomenon that they likely haven’t seen since 2008-09: mark-downs of the VCs’ portfolios. This strangely may come even more quickly in the more successful funds, because any funds (ours included) who still hold some public stock from a recent IPO will likely be seeing write-downs sooner due to the immediacy and transparency of public stocks being repriced.

But the problem for LPs is that as VCs write bigger checks with increased frequency, these firms go “back in the market” to raise funds more quickly than in the past. A normal VC fund raises a new fund every three years if they are strong performers. Some are slightly faster – two and a half years – and sometimes it takes longer to deploy capital, closer to four years. In recent years, some funds have literally raised new funds inside of 18 months – staggering amounts of capital at that. I suspect those days will end soon, and 61% of LPs polled said they felt VCs were coming back to market too quickly.

The Biggest Area of Concern is Late Stage Investments

With valuations rising fastest in late-stage venture and the competition that is well-known from corporate VCs, mutual funds, hedge funds (and even LPs), it is unsurprising that LPs are most concerned about late-stage VC. 68% of LPs surveyed expressed caution that the late-stage part of the market is over-valued.

But of course, for every angle of the market where one person sees caution, another spots opportunities. Some LPs have privately speculated that later-stage VCs may have a field day in the next 18 months, buying up large positions in firms with strong revenue at attractive prices given the recent squeeze on funding. It’s not an opportunity for the weak of stomach, as these deals are hard to get done and even harder to keep on course. But there’s no doubt, some will make money.

Another Area of Concern is in the Seed Investor Class

I have also heard LPs express concern over the last few years about the seed stage of venture. One narrative is that too many funds have been created, and without a strong sense of differentiation, there will be too many mediocre seed funds. Another big area of concern expressed by LPs is that some seed funds may get “squeezed” in both good scenarios and bad. In good scenarios, they don’t have funds large enough to follow their winners. In bad markets, they can be wiped out by recaps and liquidation preferences unless they save enough reserves to protect their positions.

The data itself bears out some of these fears. 89% of LPs survey expressed some level of concern about the seed market. 65% said they will invest in seed funds but are very discerning about which ones, and 23% expressed concern that there are just too many seed funds – they’re worried about capacity. Anecdotally, most LPs believe the best seed funds still deliver superior returns to other parts of the market, but they simply can’t put enough dollars to work in the handful they truly respect.

Many Seed Investors Have Solved the Cash Problem with Opportunity Funds

A few years ago, the best seed funds responded to the challenge of being cash-strapped by raising “opportunity funds,” which can invest in the seed investor’s best deals as those deals grow. Of course, this raises a host of questions about conflicts of interest, valuations, and whether early-stage investors are well-suited to invest in later-stage deals. But both seed investors and LPs alike agree that as long as these programs are managed sensibly, their existence is useful. A whopping 85% of LPs were favorable to opportunity funds as long as they were done with a pragmatic approach and with favorable economics.

Most LPs Don’t Believe That Traditional VCs are Being Squeezed

Occasionally, some of the larger funds will argue that traditional VCs will be “squeezed.” They say that “the big guys are getting bigger and can compete for the full lifecycle of investments” on one side, and “the seed investors are out-hustling traditional VC” on the other side. Frankly, I’ve never believed this argument. As a traditional VC, the growth of seed funds has been a blessing to me because it increases the total number of startups for us to evaluate. We’ve also become very adept at partnering with seed funds.

And other than a handful of deals that scale in the blink of an eye, I really haven’t felt too much pressure from bigger VCs moving down into our territory. Funds that are more comfortable writing $20 million checks in more proven businesses simply don’t want to also compete for less proven deals in need of $4-5 million.

Luckily, LPs seem to agree with this thesis. Only 17% bought the premise that traditional VCs are being squeezed, versus 34% who prefer to focus the majority of their efforts on traditional A/B round VC funds. And of course, 50% want a good balance across all stages: seed, traditional and growth.

Perhaps the Biggest Change in the LP Ecosystem is the Number Now Seeking Direct Investments

The booming tech markets and the dollars being allocated in the venture sector have created one seldom-discussed consequence over the past three years – the sheer number of LP dollars looking for “direct investment” (i.e., dollars going directly into portfolio companies vs. the funds themselves).

Nearly 40% of all LPs surveyed said that direct investments were becoming an important part of their program (17% said they’re very important), and a further 44% of LPs are opportunistically doing direct investments. There are even LP fund-of-funds who raise capital with a main marketing pitch of providing better access to direct investments.

Summary

LPs remain staunch supporters of the venture capital industry, and their investment pace into VC seems likely to hold steady for the next one to two years (barring any unforeseen negative market events). This support will start to meet headwinds in the next three to four years if our industry doesn’t find a way to drive more exits and recycle capital back into the ecosystem. Without some cash distributions, eventually LPs will become stretched. I expect the LP conversations in the next 12-18 months to be about the inevitable mark-down of VC portfolios; however, many LPs are long on venture capital for the same reasons I am. Any correction will be followed by the long march of technology disruption and the profits disproportionally allocated to the winners.