Sometime back I had blogged urging caution on excessive accountability and transparency. Ajay Shah draws attention to an excellent paper by Cass Sunstein where he draws the distinction between transparency in the inputs and outputs of government activities and draws up the costs-benefits calculus,

Government can be transparent about its “outputs”: its regulations and its policies, its findings about air and water quality, its analysis of costs and benefits, its assessment of the risks associated with cigarette smoking, distracted driving, infectious diseases, and silica in the workplace. It can also be transparent about its “inputs”: about who, within government, said what to whom, and when, and why. The argument for output transparency is often very strong, because members of the public can receive information that can help them in their daily lives, and because output transparency can improve the performance of both public and private institutions. Where the public stands to benefit, government should be disclosing outputs even without a formal request under the Freedom of Information Act. In fact it should be doing that far more than it now does. The argument for input transparency is different and often weaker, because the benefits of disclosure can be low and the costs can be high. There is good reason for a large increase in output transparency -- and for caution about input transparency.

Sunstein quotes James Madison to make the point very powerfully,

It was . . . best for the convention for forming the Constitution to sit with closed doors, because opinions were so various and at first so crude that it was necessary they should be long debated before any uniform system of opinion could be formed. Meantime the minds of the members were changing, and much was to be gained by a yielding and accommodating spirit. Had the members committed themselves publicly at first, they would have afterwards supposed consistency required them to maintain their ground, whereas by secret discussion no man felt himself obliged to retain his opinions any longer than he was satisfied of their propriety and truth, and was open to the force of argument. . .. No Constitution would ever have been adopted by the convention if the debates had been public.

More fundamentally, information about inputs cannot be abstracted in isolation from its transactional context, whose literal reproduction is virtually impossible. In the absence, a specific input is vulnerable to being grossly misinterpreted and detract attention from the issue under consideration. This risk becomes amplified in a world of high voltage media spins and trials.

Consider the example of the deliberations of an internal committee of officials who have been appointed by the Government of India to give recommendations to fix an off-set price for the oil and gas exploration licenses. In the prevailing environment where the popular norms in favour of revenues maximisation and not benefiting private companies are entrenched, officials will be apprehensive of being marked out in public as having taken an opposing view and be insinuatingly referred to having favoured large private companies (in this case, it could be one particular large private group!).

One such view could be the legitimate opinion that an oil importing country like India should instead of maximising revenues seek to increase domestic production and thereby reduce import dependency, even if it runs the risk of benefiting the private explorer if it gets lucky and is able to strike resources at low extraction costs. This view could be reinforced by recent oil market developments - weakness in the oil prices, and failures to attract interest in much larger off-shore block auctions in Brazil and Mexico. I, for one, am strongly inclined to this view, as I have blogged earlier here.

Or consider a decision involving adjudicating on the imposition of a standard on effluent discharge from certain industries. One side, popular among environmentalists, favour zero liquid discharge (everything is reused) for certain categories of industries, which has become entrenched in popular media as the socially preferred option and anything else as a concession to polluting and corrupt firms. This has also, for whatever reasons, assumed significance in light of an affidavit submitted by the Ministry of Environment and Forests to the Supreme Court of India. However, practical considerations and experience from elsewhere would show that this is prohibitively expensive and may not be a prudent choice. But supporters of this view face the possibility of being branded as corporate stooges and vilified as corrupt.

More fundamentally, any public policy decision involves an exercise of weighing of public costs and benefits, at least some of which are realised over long durations and also involve significant private benefits. Complicating matters further, it is virtually impossible to make estimations with great accuracy and often times the realisations are way off from the original estimates. In such a complex decision making environment, it is important that decisions get taken after examining all dimensions and sides involved through a most open and liberal deliberative process. It is inevitable in such deliberations that people take positions and make arguments which would evolve, even change diametrically, along the process.

Making all this public, with the attendant risk of insinuating extracts quoted off context finding its way into a public media debate, would invariably affect the openness of the deliberative process by making officials reluctant to be on record with such views. For example, in the case of the debate on effluent discharge, at the least, the sceptics of the zero discharge would have played the critical role of steering the decision somewhere to the middle of the spectrum. They would have helped avoid populist extremism in the choice of effluent standards, and balance the requirements of environmental protection and economic growth.

It is for this reason that the US Freedom of Information Act provides for exempting privileged communications within or between agencies, including deliberative process privilege, from its jurisdiction. India's Right to Information Act however does not have this exemption. And its effects have been not to benign. Given that the 10th anniversary of the RTI Act just got over, it may be an opportune moment to revisit its provisions and refine them. Unfortunately, the political courage required for this may not be very forthcoming.

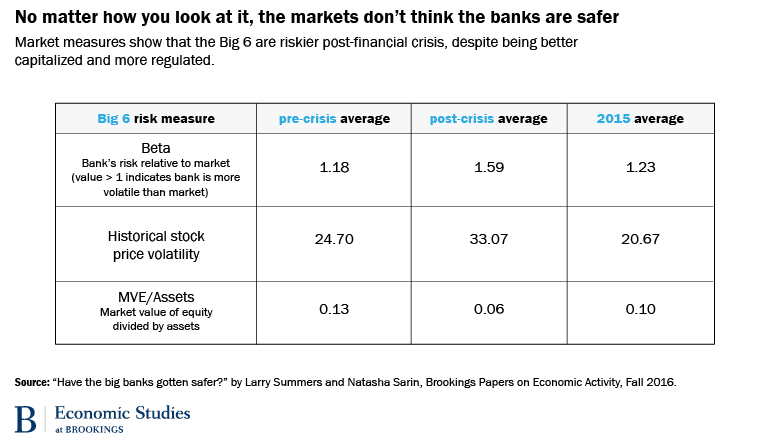

Wells Fargo- A retail bank with a halo around it. Considered so saintly and profitable that the Oracle of Omaha owns more than ten percent of the Bank. All of a sudden, in the eye of a storm as a structured fraud is uncovered and the misplaced faith in the corporate custodians is shaken once again. Wells Fargo fraud is not the first one and will certainly not be the lost. It is all a matter of discovery.

The problems of meeting investor expectations and focusing on that makes people do things that range from grey to black. I seriously doubt if ANY company, across the globe, will be snow white, when it comes to ‘integrity’.

There are two factors that impact integrity;

Promoter or management dishonesty that is intrinsic to most human beings. Very often, it is a matter of degree and rarely one of principle. Like using office stationery, office vehicle, company aircraft, club memberships etc at corporate expenses. Starting from things like this, it extends to milking the company from its operations to gold plating capital costs. This is true of at least ninety percent of companies.

The second one is a corollary of trying to pump up share prices. The pressure on quarterly earnings growth makes managements do strange things. This puts inordinate pressure, set unrealistic targets, fudge books and do other wrong things. The company can be promoter owned, in which case the stock price becomes a personal wealth issue. If there is a ‘professional’ management team, share prices become important because of ESOPs.

When I invest, I presume that every company has one of the two as a fundamental attribute. The second attribute is something about which awareness is low. The ‘professional’ greed to create so called ‘shareholder value’ leads to a lot of irrational things like:

Wrong capital allocation to give the impression of future earnings streams;

Wrong corporate actions like mergers / acquisitions at high prices to sustain the ‘pace’ of growth;

Relentless pressure on employees to meet impossible targets; and

Paying too much attention to stock price performance rather than remain focused on bottom line.

The Wells Fargo Bank case is summarized in this link:

Till the fraud was uncovered, this bank was a role model of a well run, profitable retail bank.

It is easy for us to dismiss this as an “American” problem. I beg to strongly disagree. We have several ‘professionally’ managed companies run by employees with ESOPs. Ownership is diffused or subdued and the professionals call the shots. For instance we have banks like ICICI/HDFC etc where it is the CEO and team that runs the business. Yes, they may have a Board of Directors, but we all know that the Board will only know what the CEO wants it to know. Meeting four or five times a year does not give the Board of Directors any insight in to the business or even a whiff of what goes on in the day to day business. So, bury the thought that having independent directors matter.

No company can pass an absolute test in integrity. Somewhere, the tax rules and the lack of punishment, make it easy for the transgressor.

As an investor, it is good to realize and understand this. TRUST NO ONE. That way, you do not leave any room for disappointment. Check the cash flows. See the employee payments, the ESOPs and the lifestyles. Wherever you can. Of course, NO ONE is immune to a structured fraud. And also worry when someone stands out like a ‘sore thumb’. If someone sounds too good to be true, there is a strong possibility of a structured fraud.

The world of stocks and bonds is one big web of deceit and cunning. You have to be alert at all times. Concentration can heighten your risk. Diversification can delay the process to some end. Be a skeptic investor. That can minimize pain, should you get hurt.

FM, Arun Jaitley has earmarked Rs 700 billion (USD 10.5 billion) in bank capital injections in the four years to March 2019.

Ratings agency Fitch estimates, however, that USD90 billion in capital will be needed for Indian banks to meet Basel III banking rules due to be fully implemented by March 2019. Fitch says that 11 Indian banks may fail to meet those norms.

With the finance minister spelling out compulsions in providing additional capital for the PSU banks, it is a matter of time that we say consolidation and increased transition from public sector to private sector banks and NBFCs.

This provides a very large opportunity for organizations which are well capitalized and are diversified into multiple lending lines. I continue to believe businesses like HDFC Bank, Kotak Mahindra Bank, ICICI Bank, Bajaj Finance and others would do well over an extended period of time.

A recent front page story in the Indian Express came as a surprise examination for many economists in India. When currency policy is proposed, four ideas are useful:

Nobody knows what is the correct exchange rate. Asking a government official the correct price of the rupee is as pointless as asking him the correct price of steel or the correct level of Nifty.

We were once in a complicated world where RBI openly said that it had no framework. RBI governors heard pleas from importers and exporters, played favourites, and earned political capital. That period (1934-2015) is now behind us. Now, for the first time, RBI is accountable. It has an objective: inflation. The instrument (control of the policy rate) is used up in giving us the outcome (4% inflation).

Chasing an exchange rate objective can lead to small problems (e.g. the exchange rate management of 2002-2007 kicked off an inflation crisis from 2006) or big problems (the rupee defence of 2013). Wisdom in public policy involves avoiding such adventurism.

While an inflation targeting central bank should not pursue exchange rate policy, the exchange rate is an important input for an inflation targeting central bank. Changes in the exchange rate feed into domestic inflation through the price of tradeables. Thus, changes in the exchange rate are a useful input for forecasting inflation. The essence of good monetary policy is forecasting inflation [example]. RBI should consume the exchange rate, made by the market, as an input into its monetary policy process.

Last evening, the obstetrician came over to check on the wife, following the afternoon’s Caesarean section operation. Upon being asked how she was, the wife replied that she’s feeling good, except that she was still in a lot of pain. “In how many days can I expect this pain to subside?”, she asked.

The doctor replied that it was a really hard question to answer, since there was no definite time frame. “All I can tell you is that the pain will go down gradually, so it’s hard to say whether it lasts 5 days or 10 days. Think of this – if you hurt your foot and there’s a blood clot, isn’t the recovery gradual? It’s the same in this case”.

While she was saying this, I was reminded of exponential decay, and started wondering whether post-operative pain (irrespective of the kind of surgery) follows exponential decay, decreasing by a certain percentage each day; and when someone says pain “disappears” after a certain number of days, it means that pain goes below a particular threshold in that time period – and this particular threshold can vary from person to person.

So in that sense, rather than simply telling my wife that the pain will “decrease gradually”, the obstetrician could have been more helpful by saying “the pain will decrease gradually, and will reduce to half in about N days”, and then based on the value of N, my wife could determine, based on her threshold, when her pain would “go”.

Nevertheless, the doctor’s logic (that pain never “disappears discretely”) had me impressed, and I’ve mentioned before on this blog about how I get really impressed with doctors who are logically aware.

Oh, and I must mention that the same obstetrician who operated on my wife yesterday impressed me with her logical reasoning a week ago. My then unborn daughter wasn’t moving too well that day, because of which we were in hospital. My wife was given steroidal injections, and the baby started moving an hour later.

So when we mentioned to the obstetrician that “after you gave the steroids the baby started moving”, she curtly replied “the baby moving has nothing to do with the steroidal injections. The baby moves because the baby moves. It is just a coincidence that it happened after I gave the steroids”.

Imagine year 2019. You have retired, and you have received Rs. 120 lakhs as your provident fund accumulation. The bank is willing to pay you 2% interest on savings accounts and 4% p.a. interest of fixed deposits. The government has scrapped nsc, and kvp. Post office pays about 0.25% more interest but the have a […]

Most advanced economies have a nominal anchor for monetary policy in the form of an inflation target at 2%. This has presented difficulties when the policy rate hits 0%. This calls for using a new and more unpredictable tool -- quantitative easing -- or finding ways to force the short rate below zero. Both are difficult.

In addition to these arguments, there is a fiscal perspective that needs to be brought on the table.

Suppose we suddenly raise the inflation target from 2% to 4%. Suppose there is no disruption, everything works out smoothly. In the ideal scenario, the yield curve should parallel shift up by 200 bps at all maturities.

This would be bad news for persons holding nominal bonds issued by the government, persons holding nominal pensions, nominal bonds issued by private corporations, etc.

A person who has a nominal pension backed by a corporation will be angry about it. But there will be nothing she can do about it. Persons who hold claims upon the government would not accept these losses lying down. They would organise themselves politically and ask for compensation for the losses they would face if such a decision were taken.

How large are the magnitudes? Suppose a country has explicit nominal government bonds and implicit nominal pension debt adding up to 100% of GDP. Suppose this has an average maturity of 10 years. The 200 bps parallel shift of the yield curve would impose a loss of 20% which works out to 20% of GDP. There is no democracy in which monetary policy wonks are going to be able to impose a cost of 20% of GDP upon some people without a political fight. A negotiation would take place where the adversely affected persons will ask for compensation.

This negotiation will be a difficult one. As an example, envision the US Treasury, the US Fed, and bondholders sitting in a room arguing about 20% of GDP. Things become more difficult in countries where the government owes nominal defined benefit pensions.

If the negotiation works out smooth and clean, the debt/GDP of the country goes up by 20 percentage points. This will make bondholders and credit rating agencies more nervous about the fiscal solvency of the country. While some countries (e.g. Australia) have good fiscal health, most advanced economies do not.

The last and most troublesome issue is that of credibility and confidence. Many advanced economies have a difficult fiscal situation, particularly when off-balance-sheet liabilities are counted. The bond market has generally been quite well disposed towards these countries; e.g. the bond market assumes the US will solve its fiscal crisis, even though nobody can see how this would be done. One key element of this confidence on the part of the bond market is: trust in the 2% inflation target. As fiat money is anchored with a 2% inflation target, the fiscal authority cannot inflate away debt by using inflation surprises. This reassures bond holders who are then willing to lend money to the sovereign at low interest rates.

Suppose the negotiations associated with the increase in the inflation target don't work out well. Some bondholders walk away feeling they were unfairly forced to accept a loss. There will be less trust the next time around. The bond market will not trust the 4% inflation target in the way it has come to trust the 2% inflation target. It will demand a risk premium in exchange for bearing the risk that the institutional mechanism of monetary policy is not trusted for decades and decades to come.

For some advanced economies, under certain kinds of mishandled negotiations, the project of trying to raise the inflation target from 2% to 4% could lead to a sharp one-time increase in the debt/GDP ratio and a higher required interest rate for government debt. These two outcomes could significantly worsen the fiscal situation for the government.

These considerations should be brought into the picture when evaluating the costs and benefits of raising the inflation target from 2% to 4%.

Lee Kuan Yew, the “Father of Modern Singapore”, who took a nation from “Third World to First” in his own lifetime, has a simple idea about using theory and philosophy. Here it is: Does it work?

He isn’t throwing away big ideas or theories, or even discounting them per se. They just have to meet the simple, pragmatic standard.

Does it work?

Try it out the next time you study a philosophy, a value, an approach, a theory, an ideology…it doesn’t matter if the source is a great thinker of antiquity or your grandmother. Has it worked? We’ll call this Lee Kuan Yew’s Rule, to make it easy to remember.

My life is not guided by philosophy or theories. I get things done and leave others to extract the principles from my successful solutions. I do not work on a theory. Instead, I ask: what will make this work? If, after a series of solutions, I find that a certain approach worked, then I try to find out what was the principle behind the solution. So Plato, Aristotle, Socrates, I am not guided by them…I am interested in what works…Presented with the difficulty or major problem or an assortment of conflicting facts, I review what alternatives I have if my proposed solution does not work. I choose a solution which offers a higher probability of success, but if it fails, I have some other way. Never a dead end.

We were not ideologues. We did not believe in theories as such. A theory is an attractive proposition intellectually. What we faced was a real problem of human beings looking for work, to be paid, to buy their food, their clothes, their homes, and to bring their children up…I had read the theories and maybe half believed in them.

But we were sufficiently practical and pragmatic enough not to be cluttered up and inhibited by theories. If a thing works, let us work it, and that eventually evolved into the kind of economy that we have today. Our test was: does it work? Does it bring benefits to the people?…The prevailing theory then was that multinationals were exploiters of cheap labor and cheap raw materials and would suck a country dry…Nobody else wanted to exploit the labor. So why not, if they want to exploit our labor? They are welcome to it…. We were learning how to do a job from them, which we would never have learnt… We were part of the process that disproved the theory of the development economics school, that this was exploitation. We were in no position to be fussy about high-minded principles.

So Plato, Aristotle, Socrates, I am not guided by them...I am interested in what works... Click To Tweet

Indian stock markets have moved up quite a bit in last few months. Not only in absolute sense, i.e. index levels but also in terms of valuations.

Last I checked, the bellwether Nifty50 was trading at a PE of 24. And such high PE levels are known to cause losses in medium term. Here is a solid proof.

But don’t jump to any conclusion here.

The Indian stock markets are overvalued right now, no doubt. But there are few other things that should be kept in mind too.

It is increasingly becoming evident that the average investor has got back his interest in stock markets. And when that happens, it can have negative impact on near term returns.

But jokes apart, almost everything seems to be going in favor of markets – low oil prices, good monsoons, chances of lower interest rates, passage of GST bill, FII inflows, etc.

Average investor fears missing out on big returns and want to join the market action.

Unlisted companies are using this FOMO (Fear Of Missing Out) syndrome to come out with their [Always] Overpriced IPOs(which is not abnormal – IPOs always come in rising markets). Then AMCs are celebrating SIPs like festivals. But credit should be given to them as SIP is indeed the best way for retail investors to create long term wealth from stock markets.

Also, there is a lot of consensus about almost everything that is being said with a positive bias.

Everybody seems to be under the impression that its easy to make money in stocks. Apply for and IPO and Yo! – guaranteed listing gains! Even my wife was asking me one of these days to buy her something ‘golden’ as she recognized the dominance of green color in my portfolio.

Lets come back to the PE discussion for a moment. I told you that Nifty50 PE is above 24. Have a look at this graph:

This is a graph where I have plotted actual Nifty level (blue line) and hypothetical Nifty levels at PE24 (red line) and PE12 (green line).

If you observe carefully, the blue line seems to bounce off whenever it is about to touch either the red or the green line (bounce points highlighted by red and green circles).

Also, if you notice that big red arrow – that is our markets now. We are once again flirting with PE24 levels. So danger lights are on.

I know, this graph makes me look like someone trying to use technical analysis to draw out fundamental conclusions. But it is clearly evident.

Chances of markets sustaining above very high PEs is very low. There is always a reversion towards the mean (i.e. lower PEs in this case).

But don’t think that this should be the only criteria to assess market valuations. Also, simply basing your individual stock buy/sell decisions on broader market indicators is wrong. Its infact criminal!

But you need to be aware of what is happening in markets. And tracking few of these indicators (like I do in State of India Stock Markets every month) can be quote helpful. Atleast you are not taking decisions blindly.

High PE is No Guarantee of Stock Market Crash!

Yes. Just because markets have a high PE doesn’t mean that markets will crash.

Why?

PE Ratio = Price / Earnings

So if price (index level) remains same and earnings increase, the PE will naturally come down – i.e. valuations can come down even without price correction.

Talking of earnings (of all companies that are part of index), it is worth asking how are these companies doing on earning front? Or what are the projections for near term.

Most people expect and believe that earnings will improve going forward. One of the reasons being given is that the groundwork done by government in last two years has set the stage for revival. Then banks NPA mess will finally be over and interest rates will fall and this and that and what not….

So if earning do indeed improve, the markets will become reasonably valued without even a correction.

But if earning do not improve and given that valuations (expectations) are already very high currently, we cannot rule out a correction – small or large, I don’t know.

But markets have this uncanny habit of doing what nobody expects them to. There won’t be any correction when most people are talking about it. But the correction (or crash) will take place when most people aren’t expecting it.

As of now, the general perception is that near-term future is bright. So if markets were to surprise this general perception, it should fall. Now I think that Indian stock markets are overvalued in general (driven by hope that earnings will improve) and a correction here will be healthy. So if markets were to surprise me instead, they would ignore me and continue rising. My bad luck then.

But don’t forget that a good part of the recent upmove is fueled by FII money. And they can very quickly move in or out of the market – driven by news or other factors. So an abrupt fall in our markets, if FIIs decide that ‘enough is enough’ should not come as a big surprise.

What about other indicators (like Price/Book Value, Dividend Yield, etc.)?

If we just look at the numbers, all these indicators say that markets are overvalued.

I have already written about it recently. So you can go through following two articles and draw out your own conclusions

Some people talk about the Market cap to GDP ratio – a concept popularized by Warren Buffett. He is known to have said that this indicator is ‘probably the best single measure of where valuations stand at any given moment.’

This is calculated as follows:

Market Cap to GDP = Market Capitalization of country’s stock market / GDP of the Economy

So it requires two inputs – 1) Market Cap and 2) GDP.

Market Cap is easily known.

But even though GDP numbers are easily available, there are questions to be asked about reliability of the GDP data. There have been times when almost all other indicators have pointed in one direction and GDP growth rate pointed in other. So I don’t have a very high conviction on GDP numbers being published currently.

Due to lack of conviction here, its tough to use Warren Buffett Indicator (which makes use of GDP) to draw out any conclusive signals. So I prefer not to use Market Cap to GDP Ratio of India to discuss about stock market’s overvaluation or undervaluation.

Before we move forward, lets try to play devil’s advocate here. Since start of this article, I am trying to convey the message that markets may be overvalued. But for a moment, lets invert this discussion..

Can we somehow prove that Markets are not overvalued?

Lets try doing that:

It is true that before 2014 elections, Indian economy had one foot on the brake and other on the accelerator. So with high interest rates, high inflation, high crude oil prices, low demand and low capex, growth was sluggish. So this muted growth obviously didn’t lead to earnings growth.

And since Nifty PE looks at trailing earnings, the valuations do seem to be expensive.

But as I said in first few paragraphs of this article, there are a lot of things that are in favor of Indian now (low inflation, falling rates, GST, etc.). So if these favorable factors, combined with government’s push to give a boost to economy do actually work out, its possible that earning might grow more than expected. As a result, the valuations will come down and markets may make new life-time highs.

Now re-read the previous paragraph and observe the underlined words. A lot of if(s) and but(s) and might(s) and may(s).

So just too many things need to work one after the other. Its possible… But you know what I am trying to say here…

Looking Inside The Box When Everyone is Looking Outside the Box

Successful investors do what others aren’t doing.

It is very simple. Not easy ofcourse.

But let me be frank here – even though markets in general are not cheap, there are still pockets where undervalued stocks are available. But ofcourse, its not easy to simply go and find the most undervalued stocks in India just by looking at some financial parameters. The answer to the question ‘how to find undervalued stocks or companies’ is not an easy one.

I wrote an article titled Don’t ignore large caps. Its primarily about looking in places where other aren’t.

When most investors are going after fancy names and following stock gurus, it might make sense to take step back and look into the opposite directions.

Sometimes value sits in front of our eyes and we ignore it because everybody else is doing so.

We need to stay on a lookout for businesses that are being neglected, are out of news or in news because of wrong reasons. It is only then that we will get a good price (low price). You cannot get good news and good price simultaneously in stock markets.

What I am Doing Now?

Now its easy to quote someone like Charlie Munger here

Move only when you have an advantage. It’s very basic. You have to understand the odds and have the discipline to bet only when the odds are in your favor.

But it is difficult to implement it. We have our financial goals and other things that require our attention in life. Unlike lord, we are mere mortals

So what should you do?

Every man for himself. So before I give some uninvited advice about what others should do, let me first tell you what I am doing.

Now you don’t have to do what I am doing. I can take risks that you might not be willing to or shouldn’t. Given my background, I can (atleast try to) act as I talk about buying low and selling high and having a market crash fund.

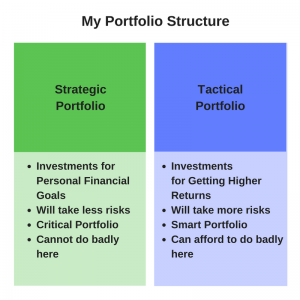

And here is a graphical guide that helps me keep a cool head when it comes to investments.

So as far as I am concerned, I want to strike the right balance between optimism and caution. And that is damn tough, honestly.

But I try to deal with it at two separate levels:

Strategic Portfolio + Tactical Portfolio

What is my Strategic Portfolio?

I am a common man. I have common financial goals that need to be fulfilled at all costs. And I don’t want my stock market predictions or flawed assumptions to come in way of my goal achievement. Plain and simple. So Strategic Portfolio is where I invest for my financial goals like financial freedom, etc.

To put it more simply, I can afford to not be a great investor in my strategic portfolio. But I cannot afford to be a bad investor in this part of my portfolio.

Read that again.

In this part of my portfolio, I continue to invest regularly in equity funds that I have chosen. I also invest in PPF and debt funds to maintain the overall asset balance of this portfolio. Since I believe that markets are overvalued right now, I will not put additional money in equity MFs here. If I have surplus, I will either stay in cash or push it in debt.

To summarize, base SIPs in equity funds continue. Investments in debt continue as per plan. But no additional investments (if surplus available) in equity linked products for time being.

Here I take slightly riskier bets with my money. No, I don’t borrow and invest. But I am comfortable taking additional risks in an effort to get higher returns. Again since my reading is that markets are overvalued, I am holding back my guns and not doing much here. Infact, I have sold some of the stocks from my non-core holdings.

To summarize my portfolio structure approximately, here is a graphical depiction:

I know what you must be thinking. I am holding my new investments (in tactical portfolio) and sort of being in cash, liquid funds and sitting out. What if I miss the rally (if that happens in near future)?

If that happens then so be it.

I can’t be right everytime.

Isn’t it? Nobody can.

I know that I run the risk of losing out if markets go against me. But I am doing what I am comfortable doing. 3 Cs of Cash + Courage + Crisis drive me.

Its very simple for me –

If markets go up, I am uncomfortable. If it goes down, I am comfortable.

Caution – Do not take any actions solely based on what has been written above or more importantly, after this sentence. Your money – Your responsibility.

What Should You Do?

First, spare a moment for this – History of stock market is full of examples where returns have been poor when everybody was thinking that returns will be great (latest example: 2007-2008).

As of now, I don’t know whether everybody thinks like that. But given what indicators tell, most people are quite optimistic (and may be over-optimistic) about future returns.

A solid 15% CAGR is like a no-brainer for most people – which they claim they can easily manage. To be honest, its hilarious to know such opinions. And this reminds me of a beautiful quote that Warren Buffett came up with in his letter to investors in 1997:

In a bull market, one must avoid the error of the preening duck that quacks boastfully after a torrential rainstorm, thinking that its paddling skills have caused it to rise in the world. A right-thinking duck would instead compare its position after the downpour to that of the other ducks on the pond.

So if I were you, what I do going forward will depend broadly on my time horizon and whether I am interested in lumpsum or regular investments. Specifically speaking…

I would let me SIPs continue that are directed towards my financial goals. No tinkering with that (atleast not now).

I will sell stocks that I know are crap but part of my portfolio.

I will have watchlist of stocks, which I will buy if markets do fall from here.

If my portfolio is already equity heavy (due to run-up in prices) and if I have surplus funds, I will hold on to it or put it in debt for time being. I will wait.

I know its easy to say all this. But when markets around you are going up, its tough to leave the party.

But I am telling you, its best to leave the party when you don’t want to.

Even after writing all this, don’t for a moment think that I have any special ability to predict anything. And as Jason Zweig says in this article,

Don’t let anyone (else) fool you into thinking that history or mathematics can identify some exact entry point at which you can know you’re buying back into stocks at a bargain level.

Also, when returns in recent past have been high, our awareness of increased-probability-of-lower-future-return decreases. But we must not forget that in markets, risks increase with increase in prices.

So the party is on. Be happy that markets are doing well. But combine this happiness with a bit of caution. Stock markets are overvalued and a little bit of caution won’t hurt you. Infact, it will protect you. A correction in 2016 or 2017 may not be as severe as crash of 2008 and 2009. But if there is no correction without any earnings improvement, it will be a bit surprising.

As for the crash, I have always maintained that stock market crashes are good opportunities for long-term investor to give booster shots to their portfolios. So have patience.

And as Warren says,

Be Fearful When Others Are Greedy and Greedy When Others Are Fearful.

In credit funds, the real issue is not about credit risk , it’s about liquidity risk !!

Long term investors have to focus on the trade off between – Expected returns vs Risk

There are two fund management organizations – IDFC MF and Axis MF, who have also communicated their views on credit funds. Let’s read them and see if we can get some additional perspectives.

You can read IDFC fund manager Suyash Choudhary’s thoughts on Credit risk here

Managing risks in investment – Credit vs Duration – Link

Highlights from the note

Long term investors have to focus on both expected return as well as risk when investing

Since this trade-offcan always change with changing triggers, the focus should be on expected return versus manageability of risks taken.

Credit risk and duration risk are both legitimate means to earn‘excess’ returns over fixed deposits

Duration Risk:

Duration risk works via a daily mark-to-market channel and hence offers more short term volatility in return profile (although the longer term profile may actually be much more stable)

Credit Risk:

Credit risk is binary in nature – either manifests or it doesn’t. This is especially true in a market like ours where there is hardly any secondary market price discovery for lower rated credit assets. Thus change in credit quality doesn’t get dynamically reflected in price changes

The difference really lies in the ability to respond in terms of curtailment of risk if the view changes on evolving developments

Duration risk can be managed on an ongoing basis since it is backed by a robust secondary market where one can buy and sell.

Credit risk cannot be managed on an ongoing basis which makes the ongoing management of the risk difficult.

Also, the relative choice (of how much of credit risk and duration risk to take) has to take into account the macro environment which either creates a tailwind or a headwind to each type of risk

You can read Axis fund manager Sivakumar’s thoughts on Credit risk here

Effect of credit default is lumpy and is not captured in daily mark to market. Thus the risk is not captured completely until a downgrade / default event

Apart from the credit risk concerns, the other reason that credit portfolios face a significant risk is the lack of liquidity in the secondary market in lower-rated instruments. This presents a contagion risk for the markets since in case there is a need for any investor to liquidate its portfolio over a short notice, it will be exceedingly difficult to do so.

Understand the credit profile of the fund before investing

Concentrated portfolio increases impact of credit event (i.e downgrades & defaults) – Affects a large part of concentrated portfolio

Not launched credit fund + Conservative approach to credit + Disciplined portfolios with tightly defined limits for most of our funds – >75% AAA – <2% per issuer AA- and below + Relatively liquid portfolios

Parting thoughts:

The above views from these two fund managers, confirm our concerns on credit funds especially on the “liquidity” risk.

Given the above arguments and if you agree with me on the liquidity concerns underlying credit funds then:

Stick to funds with high credit quality

As earlier stated, I personally tend to avoid credit risk in my debt fund portfolios.

I also derive far more comfort on the credit quality when it comes to Axis and IDFC debt funds because they share similar views as mine with regards to credit funds. And the best part is these guys communicate regularly, which also helps us understand their investment strategy. This is precisely the reason why you would have seen me include their funds in our debt selection here

That being said, the above notes from the two fund houses were provided purely with the intent of improving our understanding and by no means do I have any connection with them. While I may have a personal preference towards these two, there are obviously other major fund houses, which also have several funds with high credit quality and you are free to choose whichever suits you the best.

As always happy investing..Cheers

Disclaimer: No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments

The insightful paper, and accompanying blog article, by Ram Sewak Sharma about three big innovations in UIDAI got me thinking about my own UIDAI experience. What were the key innovations which made it work out well, especially as viewed from the lens of the private sector? What lessons can we take away? In addition to his three big ideas, I have one more.

`Asset light business' is the new buzzword among investors, especially venture capital and angel investors. The world’s largest taxi company owns no taxis – Uber; the world’s largest room provider owns no hotel rooms – AirBnb; the world’s largest movie house owns no movies – Netflix. This is the popular refrain among the fraternity of modern day startups and their cheer-leading investors. In a similar vein, it can be argued that the world’s largest identity provider owns no identity devices! To top, this was not a traditional start-up in a college dorm by a 20 year old. This is the Unique Identity Authority of India – UIDAI, a staid authority of the staid government of India manned by staid bureaucrats.

On 26 March 2004, Bharti Airtel announced a large, first-of-its-kind outsourcing contract with IBM. It essentially meant that Bharti Airtel, the telecom player will own no telecom equipment nor network hardware or software. It will simply acquire and own customers. IBM, in turn, took on the responsibility of managing all the complex hardware and software required to run a massive telecom operation. To add, IBM was to be paid a percentage of revenues that Bharti Airtel would earn, not a mere fat, flat fee as was the prevailing norm then. Bharti Airtel grew from a 6.5 million subscriber base to 250 million subscribers in 12 years, leaving most of its competitors behind. It is undeniable that this brave decision of Bharti Airtel to smart source its capital expenditure to IBM played a key role in its ability to scale so rapidly, which is probably forgotten in the annals of Bharti Airtel’s success.

It was then dubbed the `capex to opex' transformation by financial analysts such as myself, i.e. converting big sunk costs of capital expenditure to revenue generating operating expenditure, marking significant gains in efficiency and scale. When the cost of capital is high in India owing to capital controls, there is a natural gain when an Indian firm, which suffers from the elevated cost of capital in India, contracts-out the ownership of bulky capital assets to an MNC, which enjoys global levels of cost of capital.

When UIDAI embarked on providing a unique identity to a billion Indians across more than 6.5 lakh villages, the sheer scale was daunting. As the Ram Sewak Sharma paper rightly mentions, there was detailed thought behind the use of iris, field trials to test proof of concept etc. But perhaps the single biggest catalyst in converting this from a grandiose plan into reality was the decision of UIDAI to smart source identity data collection. Surely, the technology industry background of the founding Chairman of the UIDAI played a role in its decision to do a Bharti Airtel in public policy. Nevertheless, in hindsight, this decision to embrace the ‘capex to opex’ theme but adapt it to the Indian public policy environment, in my view, laid the ‘Aadhaar’ for Aadhaar to scale so rapidly.

In an otherwise typical government project, offices would have been set up in every district, personnel would have been hired, biometric scanners would have been purchased and then identity information would have been collected, all by a government body or a clutch of bodies. This would have meant incurring massive upfront capital costs of infrastructure, technology and people. The UIDAI instead tilted it on its head and decided to build an entire ecosystem of private vendors to do the data collection with costs of machine, people and infrastructure borne by the vendor. Essentially, this meant that there were ubiquitous but authorized and approved UIDAI data collection centres and camps that mushroomed all across the country in a short span of time which made it easy for residents to register. But in the public policy world unlike the corporate world, protecting downside risks are far more important than any potential upside gains, i.e. protecting data security of Indian residents is infinitely more important than any efficiency gains of outsourcing to private vendors. This was achieved by establishing strict oversight and control mechanisms that rested entirely with the UIDAI.

The UIDAI exercised stringent control of data encryption and validation. So, while biometric data of a billion Indians were collected by thousands of independent government and private agencies, all of them collected the data through a standardised software provided by the UIDAI that encrypted the data which was then sent back for validation to the UIDAI centre. The UIDAI incurred a cost of roughly Rs.65 for every successful biometric data of an individual. Thus, the UIDAI did not have to put up big financial plans and wait for funding from the Ministry of Finance before it could launch its activities across the country.

This was one of the biggest reasons that UIDAI could go from zero to 600 million unique identities in 4 years flat, perhaps the fastest of any government or even private sector initiatives in recent times anywhere in the world. This was the power of the `capex to opex' or `asset light' innovation in policy implementation. This philosophy of the UIDAI in eschewing the temptation to `build empires' but to `build forts' instead is a philosophy that can serve many large scale government project implementations well.

I’ve said this before, but I like it when research destroys a preconceived notion of mine. Today’s post stems from an exchange that I had with Jackdamn (what a name) on Stocktwits, talking about a chart created by dshort.

S&P 500 Percent Off High Since March 9, 2009. Chart by Doug Short. $SPX$SPY$DIA

To which he responded: That’s a great question. And it is a great question, but I’m not going to answer it directly here… because I think I am answering a better question.

Let me take you through my thought process, because I went through four different ways of trying to answer the question before settling on the better question, and getting the answer.

How do you summarize an area of a price graph in order to make comparisons of different periods? How do you determine when the market has been near highs for a long time, or far away for a long time? How does the intensity/distance below the high matter? If you are looking at troughs, where does one begin and another end?

I started by trying to identify the troughs individually, and the difficulty was trying to establish that in a mechanical way that did not require interpretation. I stumbled around playing with minimum periods between troughs, recovery levels before a new trough could start, moving averages to establish when a new trough was genuinely significant. Sigh.

I tried a lot of different things, and I could create rules that mostly made the troughs look decent, but I could never get it to be fully mechanical or lack arbitrariness. Why this trough and not that? The same criticisms can be applied to dshort’s graph as well.

I finally pulled out of my mental gymnastics when I concluded: couldn’t I just take the area under the maximum line in percentage terms and use that as a measure, say over a 200-day period? 200 days is arbitrary, and so is the measure, but that is less than most of the measures that I considered, and at least this one corresponds to a relatively simple calculation.

So if you look at the red line in my graph above, you will note that it has dipped below 2.0 five times in the last 66 years, in 1954, 1959, 1964, 1995 and 2014. These observations followed periods where the markets moved to new highs rather smartly and without a lot of downside volatility. Then there were 3 times that the measure peaked higher than 64, in 1975, 2003 and 2009. These times followed incredible market falls, and were great times to be putting money into the market.

Below you can see a table of values for how often the measure is below a given threshold. It’s only above 64 about 5% of the time, and below 2 about 3.5% of the time. My main thought is this measure is this: high values of the measure probably are a “buy signal.” Low values of the measure aren’t necessarily a “sell signal.”

That signals are asymmetric should not be surprising. The largest factor in most long-term market moves, the credit cycle, is also asymmetric. It’s like my continuing series, Goes Down Double Speed. Bull markets have shallower moves and longer duration, the same way that the bull phase of the credit cycle goes. Extend credit, extend credit, extend credit… loosen standards, loosen standards, loosen standards… tighten spreads, tighten spreads, tighten spreads, etc. Then in the bear phase it is DENY CREDIT!! TIGHTEN STANDARDS!! SHEPHERD LIQUIDITY!! SURVIVE!! Short and sharp. Painful. Prices are lower, and yields higher at the end.

To close this off, where is this indicator now? It’s around 8, which is near the 40th percentile… kind of a blah figure, not saying much of anything… which is good in its own way. The market meanders and hits a few new highs, sags a little, comes back, hits a few new highs, etc. Not many people believe in it, but we are inches off the highs. Odds are we go higher from here, but not aggressively higher.

One final note: we are in the fourth and final phase of the credit cycle now, so don’t get too aggressive. Debt is getting higher inside nonfinancial corporations. Be wary, and do your fundamental due diligence on balance sheets.

Unique Identification Authority of India (UIDAI) had the goal of issuing unique identification numbers to every resident of India. In a country as large as ours, this was a difficult task to achieve. UIDAI has largely accomplished this within a short period of about six years. I believe it was able to do this only because it took many innovative and bold decisions. In a recent paper I examine some of these innovations. The paper also tries to derive lessons from UIDAI that could be applied in other government projects.

The Use of Iris Scans

The UIDAI felt that unless iris images were used in addition to fingerprints, it would not be able to fulfil its mandate of unique identification. However, there were many concerns related to the use of iris images. Was this technology mature enough? Was it too expensive? Were there enough vendors in the market to prevent lock-in?

The UIDAI set up a committee to deliberate on the issue of which biometrics to collect and what standards to use for unique identification. This committee recognised the value of using iris images in improving accuracy. However, it fell short of recommending the inclusion of the iris in the biometric set and left the decision to UIDAI.

After a detailed examination, the UIDAI came to the conclusion that the inclusion of iris to the biometric set was necessary for a number of reasons, such as ensuring uniqueness of identities, and achieving greater inclusion. In retrospect, this turned out to be one of the most important decisions of the UIDAI.

On-field trials

The practice of conducting on-field trials was an important innovation. When UIDAI began its mission, there were many questions inside and outside the organisation on whether the very idea of unique identification for every resident was feasible at all. The idea of using biometrics to ensure the unique identification and authentication of all residents in India was an untested one. There were many assumptions behind it, and the data required to test the validity of these assumptions was not available. For instance, most of the research done on using biometrics for identification or authentication was done in western countries, and that too, on relatively small numbers of people.

The knowledge which had been produced by Western researchers was not applicable in the Indian context. Could the fingerprints of rural residents and manual labourers be captured successfully, or would they be excluded from Aadhaar? What about the iris images of old or blind people? Do the devices available in the market serve the purpose? What would be the most efficient and effective way to organise the process of enrolment? These questions needed to be answered if the project was to be successful.

The strategy adopted at UIDAI was to conduct a set of trials (called Proofs of Concept, PoCs) in several states across the country. The areas were selected to be representative of real-life enrolment and authentication. A number of biometric capture devices of different makes were used, and several different enrolment processes were tried out. The PoCs were carefully designed to answer sharply articulated questions, either to verify UIDAI's assumptions, or to capture the data required to fill in gaps in the UIDAI's knowledge. In essence, the scientific method was applied to create the knowledge that was pertinent to the decisions that had to be made at UIDAI. Resources had to be allocated to this work, and in return for that, major sources of project risk were eliminated.

The results of the PoCs indicated that the major hypothesis of the UIDAI was correct: that it was indeed possible to capture biometric data that was fit for the purpose of deduplication and verification. The results also showed that iris capture did not present any major challenges. An efficient enrolment process was devised using the data captured during these trials.

Competition

The last innovation considered in the paper relates to competition. Given the scale and importance of the project, the UIDAI felt it was important to increase efficiency and reduce costs by leveraging the competencies available in the private sector. At the same time, it was also essential to avoid a situation where any one private player could exercise significant power over the effective functioning of the Aadhaar system: the Authority wanted to ensure that there was a competitive market for providing services to it. To promote such a competitive market, the Authority used a two-pronged strategy of using open standards (creating standards where there were none), and using open APIs (Application Programming Interfaces).

The Authority used this strategy in procuring vendors for deduplication. Algorithms for deduplication had never been tested at the scale required in this project. To reduce the risk of poor quality deduplication, the UIDAI came up with a novel solution. It decided to engage three biometric service providers (BSPs), instead of just one. These BSPs would interface with the UIDAI systems using open APIs specified by the Authority. This decision helped avoid vendor lock-in, and increased scalability.

The UIDAI selected the three top bidders on the basis of the total cost per deduplication. Even after these three vendors were selected, the Authority was able to set up a competitive market among them, using an innovative system to distribute deduplication requests among them. Vendors were paid on the basis of the number of deduplication operations they were able to carry out, and the Authority allocated operations to them on the basis of how fast and how accurate they were. This led to a situation where the BSPs were constantly competing with each other to improve their speed and accuracy.

Where standards were not present, the UIDAI was willing to create new standards in order to increase competition. At the outset of UIDAI's work, every biometric device had its own interface, distinct from the interfaces of other biometric devices. If a capture application wanted to support 10 commonly used devices, then the application developer would have to implement 10 different interfaces. This would have made it costly to bring new devices into the project, even if these new devices were cheaper and better. In order to avoid this situation, the UIDAI created an intermediate specification. Vendors could implement support for this specification, and their devices could be certified. This allowed all capture applications to work with all certified devices.

Lessons

The success of the UIDAI offers many lessons for other government projects. Perhaps the first lesson that can be drawn from it is that innovation is indeed possible within the government. Government processes need not prevent it from taking innovative decisions. In fact, processes commonly used within the government, such as expert committees and consensus-based decision-making, can provide methods to examine difficult issues in a credible manner. High-quality procurement and project management skills can help the government outsource many functions that are currently housed within it.

The paper also suggests that scale and complexity need not be deterrents to private sector participation: in fact, the large scale of government projects can make the project more attractive to private parties. Another lesson government agencies could learn from the UIDAI is the need to test major hypotheses through field trials before launching projects at scale. Conducting such field trials provides an opportunity to change the design or the implementation roadmap well in time, thus saving precious public money from being wasted.

Conclusion

The UIDAI could achieve its objective because it adopted a different approach from most government organisations. It took tough decisions, such as the one to use iris images; it expended resources on building pertinent knowledge, by constantly experimenting on the ground and learning from these trials; and it exploited private-sector competition to achieve its task at the lowest cost. It should be noted that this is not an exhaustive list of its innovations, but without these three decisions, it is unlikely the UIDAI would have been able to fulfil its mission.

Even large government projects can be done fast and efficiently. Government processes need not be obstructive. In fact, the mechanisms of bureaucracy, such as committees, adherence to financial regulations, and desire for consensus, can help to resolve difficult issues and take tough decisions. Well-designed pilots and field-tests can help the government evaluate the effectiveness of large programs, so that it can deploy public resources more usefully. High quality procurement and contract-management processes can enable the government to leverage the dynamism of the private sector to provide public goods effectively.

Acknowledgements

I am grateful to Prasanth Regy and Ajay Shah, both of NIPFP, for stimulating discussions.

The author is Chairman, Telecom Regulatory Authority of India (TRAI) and was part of the founding team at UIDAI.

If you have been following my debt fund related posts, you would have noticed that I generally tend to avoid credit risk in debt fund portfolios. In today’s post we will explore the thought process that goes behind my decision to avoid credit risk.

If you are new to the blog, you can go through my earlier post here to get an understanding of credit risk in debt MF portfolios.

What is a credit fund? Credit funds are basically debt mutual funds which lend a major proportion of our money to relatively riskier corporate companies and in turn earn higher interest rates for us. So when you look at the fund portfolios, you will see a relatively larger proportion of debt papers which are rated below AA. (Credit rating is an indication of the underlying company’s health and its ability to repay its debt. The lower the rating, the lower are its chances to repay its debt on time.)

Eg Franklin India Dynamic Accrual Fund

Higher proportion of “below AA” rated papers..

Source: Morningstar

which helps in providing higher interest rates..

See that.. a whopping 10.87% compared to a current YTM of ~7.5-8% for most of the short term funds which invest in high quality papers (i.e predominantly AAA rated papers). These funds generally have Yield to Maturity (i.e interest rate return) which are 1 to 2% above short term funds which invest only in high credit quality papers.

Credit funds generally invest in short maturity papers between 1-3 years and the modified duration is mostly around 1-2 years. Thereby the “interest rate” risk taken to improve returns is kept at moderate levels and these funds primarily depend on the “credit risk” taken to generate additional returns.

The basic idea behind credit funds is that – by deploying their own analysis to these lower rated papers, the fund management research team would be able to identify certain companies which have much better health (than evaluated by credit rating agencies) or is expected to improve and hence the company’s ability to repay its debt is much better than perceived. This allows the fund to benefit from higher interest rate paid by these companies provided the fund manager’s evaluation is correct and the underlying companies to which they have lent repay their debt and interest on time.

Certain fund houses also take sufficient collaterals (in the form of covenants, shares, real estate securities etc) to offset the losses if there is a default from the issuer. Some have inbuilt agreements for priority in repayments to ensure that they exit when they see any small sign of distress.

Credit funds generally come under different names such as accrual funds, corporate bond funds, credit opportunities funds, income opportunities etc. If you need to know the subtle difference refer here. Given so many confusing names used to refer to various credit fund schemes, the best way for us will be to check for the credit quality of the underlying portfolio and decide

The chances of us getting attracted to credit funds is very high given 2 reasons:

Higher past returns compared to short term funds in the recent past Source: Valueresearch

Expense ratios are higher and hence more incentive for advisors to sell these funds to usExpense ratios compared to short term funds are higher by atleast 0.5 to 0.8%.

Now the key is to understand the underlying risk behind the higher returns..For that we need to find the answer to a simple question.

What happens when some of the underlying borrowers get downgraded in terms of credit rating or worst case, default and do not repay the interest and borrowed amount?

For the purpose of understanding, let us hypothetically assume that, a credit fund has lent our money out to 20 corporate borrowers equally and has 5% equal exposure to each debt security. Now assume that the financial health of one particular company to which the fund has lent starts deteriorating and hence its chances of paying back its borrowing and servicing interest reduce. Usually the credit rating agencies evaluate this scenario and reduce the rating provided to the company. This is technically called a credit rating downgrade. To understand better, you can check the actual Amtek Auto downgrade credit rating reports here and here.

This leads to an immediate price drop for the debt security of the company. Logic being lower rated papers will need to have a higher interest rate given the reduced rating and higher risk. But as the underlying interest payment for a debt security is prefixed, the prices of the debt security will have to adjust (in this case, decline to a certain extent) to match with the higher interest currently demanded by the new investor.

This is an impact on a paper which was downgraded from AA- to C. Below chart data is only for illustration purpose.

Now while the exact decline in prices would be dependent primarily on the nature and severity of downgrade, going by past history, we will assume that approximately 30-50% of the debt security price will get eroded under a credit downgrade situation. This will mean that there will be a negative price impact of -1.5% to -2.5% in the fund (30% to 50% decline on a 5% allocation). Worst case if it is a default then the entire 100% of the security holding will have to be written off i.e 5% decline for the fund.

This risk is called credit risk and as seen above is very simple to understand. At the first look, it seems like an “ok” kind of risk to take provided we ensure that the fund is adequately diversified among many borrowers and the additional returns (which we get more often than not) are high enough to compensate for the risk taken. Credit downgrades and defaults are not very frequent. And even assuming the fund manager gets 2 calls wrong and has 2.5% exposure each, the overall downside may be around 1.5% to 2.5% on the NAV. But if everything goes right we end up making around 1-2% extra returns.

All fine till now. But unfortunately, there is another risk which we have forgotten to take into account. Liquidity risk. What the heck is that??. In simple words, it means that there are not enough buyers, so even if there is a price being theoretically quoted, finding a buyer at the quoted price is not easy (think of real estate).

This is precisely, in my opinion, the biggest issue when it comes to credit funds. Indian bond markets are still underdeveloped and most of the lower rated papers are extremely illiquid which means they are extremely difficult to sell in bad times.

Let’s listen to what the great investor Mr Howard Marks has to say about liquidity..

“Usually, just as a holder’s desire to sell an asset increases (because he has become afraid to hold it), his ability to sell it decreases (because everyone else has also become afraid to hold it). Thus (a) things tend to be liquid when you don’t need liquidity, and (b) just when you need liquidity most, it tends not to be there.”

If you have some time, do read his entire writing here . Trust me. It will be well worth your time.

Think of it this way. On one side you have the lender (that is us who have invested in the fund) who can take out money anytime and on the other side the fund has invested in a few illiquid debt securities which cannot be immediately sold off in the market. Now if due to some reason (generally a credit downgrade or default event) a lot us panic and decide to take our money from the fund you can imagine the plight of the fund. The fund may get stuck with the downgraded paper and be forced to sell its more liquid holdings as there is a rush to redeem units. And as the pace of redemptions increase, both its security selection and its portfolio concentration can go completely out of whack leaving the existing investors with a far more riskier portfolio for no fault of theirs. And there lies the crux of the entire problem!!

Let’s get back to our earlier example where the fund has lost 1.5% due to 30% decline in one debt paper which was earlier 5% of the overall portfolio (now the same paper would be ~3.5% of the portfolio). Generally, the biggest investors in debt mutual funds are the corporates. They have large treasury teams who are in charge of the investments and keep monitoring every fund day in and day out. Now they realise that 1.5% knock is fine, but if the paper defaults then it will lead to an additional loss of the remaining 3.5% in the debt paper. So they decide to take their money off. Now every other corporate and savvy investors do a similar sort of calculation and decide to pull off the money before the situation worsens. So suddenly there is a large amount of people removing their money from the mutual fund (called redemption pressure). Now the fund manager unfortunately is not able to sell off the downgraded debt security as its difficult to find a buyer even even at its so-called market value. So the fund manager has no choice but to sell the high quality debt papers which are liquid. Now assume the redemptions are large and almost 50% of the fund money is taken out (I am exaggerating but you get the point). Now all this while the dumb me who is also the investor in the fund remains blissfully unaware of all this happening and see my fund’s portfolio after a month. I am shocked to see that now I am stuck with not 3.5% of the original downgraded highly risky paper in my portfolio but rather 7% of the same security in the portfolio as the 50% of the liquid higher rated debt securities of the fund is already sold. And my existing fund portfolio looks a whole lot different with most of the high rated and liquid securities being sold off. Oh shit how unfair.

Relax. The fund house obviously realizes this and tries to address this by two ways

Side Gate – The fund simply doesn’t allow anyone to take their entire money out. It puts a restriction on the amount an investor can redeem from the fund. Now if that sounds ridiculous and completely unfair. Read here to see what happened to two credit funds managed by JP Morgan when one of its debt security Amtek Auto got downgraded. And remember my rant about the corporates being the smarter and more resourceful guys. Go on check this link.

Recently the market regulator SEBI obviously concerned by the proceedings, post this event, has put in a new rule that, even in case of a systemic liquidity crisis, no redemption requests of up to Rs.2 lakh can be subject to restrictions. For redemption requests above Rs.2 lakh, AMCs will redeem the first Rs.2 lakh without restriction while the remaining money can be subject to any restriction imposed by the AMC. Further, restrictions on redemptions can be imposed only for a specified period of time that cannot exceed 10 working days in any given 90-day period.

Side pocket – The fund simply isolates the affected portion as a separate fund with a seperate NAV. So except for the affected portion you are free to redeem the remaining portion if they want. The proportion of investor money (in the scheme) linked to stressed assets gets locked until the fund recovers dues from a stressed company.

Out of these two options, “side pockets” seem like a better option as explained here. The argument goes like this – the side pocket concept would provide the required liquidity to the investor and ensures that their entire money is not stuck. Further it also ensures that the early sellers in the fund do not benefit at the cost of the remaining investors.

Now the only flipside is the subtle unintended consequences. A fund manager who knows that the side pocket option is not available will be forced to be much more prudent and aware of the risks he is taking. If the option of a side pocket exists, then the fund manager may venture out to take unwarranted higher risks to provide higher returns as anyway they can use a “side pocket” if something goes wrong.

For once, the regulator SEBI also seems to share my concerns and post the recent JP Morgan – Amtek Auto debacle has warned against the future usage of side pockets by Indian mutual funds (see here)

So adding to the problems, the funds from now on cannot use the side pocket option in future and the side gate option also has several new restrictions imposed by SEBI. This means the credit funds will find it more difficult to handle redemption pressures if at all it arises. And since the side pocket option is not there, investors will want to exit as fast as possible fearing possible “redemption freeze” scenario which ironically will only exacerbate the redemption frenzy. Phew.

Assuming you survived the post till here, the simple summary is that more than the credit risk it is actually the liquidity risk which is the real problem in credit funds.

Since these credit events are not very frequent, the bigger risk is that we may tend to under appreciate the very nature of risk!!

Now my thought process has always remained very simple. From heart I am an equity guy. All my chase for returns happens in equities. Debt funds personally has always been about safety. A few percentage plus or minus in debt returns, really doesn’t make a huge difference to me.

My primary usage of debt fund is a parking space for near term needs and as a part of my asset allocation strategy (i.e changing the mix of equity and debt based on valuations). So typically I will be needing this debt money desperately to buy equities when there is a crisis and equity markets have crashed (now whether I am able to pull it off in reality is a different issue). The last thing I want is for my debt fund to say that “Sorry boss, we have stopped redemptions due to a liquidity crisis”. Credit funds given their inherent structure have a high probability of getting screwed up in these scenarios. So my simple laymanistic reasoning being – why take so much tension for debt returns. As it is equities give me enough of it, but at least the long term payoff is worth the pain

As always, investing is a very personal thing and you are free to invest in credit funds but please ensure that you are not buying only because of the past returns and make sure you really understand the underlying risks (especially the liquidity risk).

“Who is rich?

He who is satisfied with his lot.” — Ben Zoma

***

A short parable on contentment today, from Plutarch’s Life of Pyrrhus, one of a series of biographies by the great Greek historian Plutarch that were later collected as Plutarch’s Lives.

Pyrrhus was the King of Epirus, a region of Greece. As he lays out his plan for a conquest of Rome, his advisor Cineas decides to take a step back and help Pyrrhus see himself in a mirror — to do a second-step analysis of his goals. Contained in that conversation is a great deal of wisdom about life. We suggest thinking deeply about what it means for your own.

“The Romans, sir, are reported to be great warriors and conquerors of many warlike nations; if God permit us to overcome them, how should we use our victory?”

“You ask,” said Pyrrhus, “a thing evident of itself. The Romans once conquered, there is neither Greek nor barbarian city that will resist us, but we shall presently be masters of all Italy, the extent and resources and strength of which any one should rather profess to be ignorant of than yourself.”

Cineas after a little pause, “And having subdued Italy, what shall we do next?”

Pyrrhus not yet discovering his intention, “Sicily,” he replied, “next holds out her arms to receive us, a wealthy and populous island, and easy to be gained; for since Agathocles left it, only faction and anarchy, and the licentious violence of the demagogues prevail.”

“You speak,” said Cineas, “what is perfectly probable, but will the possession of Sicily put an end to the war?”

“God grant us,” answered Pyrrhus, “victory and success in that, and we will use these as forerunners of greater things; who could forbear from Libya and Carthage then within reach, which Agathocles, even when forced to fly from Syracuse, and passing the sea only with a few ships, had all but surprised? These conquests once perfected, will any assert that of the enemies who now pretend to despise us, any one will dare to make further resistance?”

“None,” replied Cineas, “for then it is manifest we may with such mighty forces regain Macedon, and make an absolute conquest of Greece; and when all these are in our power what shall we do then?”

Said Pyrrhus, smiling, “We will live at our ease, my dear friend, and drink all day, and divert ourselves with pleasant conversation.”

When Cineas had led Pyrrhus with his argument to this point: “And what hinders us now, sir, if we have a mind to be merry, and entertain one another, since we have at hand without trouble all those necessary things, to which through much blood and great labour, and infinite hazards and mischief done to ourselves and to others, we design at last to arrive?”

Cineas is saying, in so many words: Why go to all the trouble of trying to own the world when you can be happy and content right now? Unfortunately, Pyrrhus fails to heed the advice.

The great Scot Adam Smith, after recounting the above story in his Theory of Moral Sentiments, uses it as a way to remind us to be very careful with our continual discontentment:

The great source of both the misery and disorders of human life, seems to arise from over-rating the difference between one permanent situation and another. Avarice over-rates the difference between poverty and riches: ambition, that between a private and a public station: vain-glory, that between obscurity and extensive reputation. The person under the influence of any of those extravagant passions, is not only miserable in his actual situation, but is often disposed to disturb the peace of society, in order to arrive at that which he so foolishly admires.

The slightest observation, however, might satisfy him, that, in all the ordinary situations of human life, a well-disposed mind may be equally calm, equally cheerful, and equally contented. Some of those situations may, no doubt, deserve to be preferred to others: but none of them can deserve to be pursued with that passionate ardour which drives us to violate the rules either of prudence or of justice; or to corrupt the future tranquillity of our minds, either by shame from the remembrance of our own folly, or by remorse from the horror of our own injustice.