Chaitanya Patel

Shared posts

06 Jun 02:52

Will the hike in service tax be easily digested?

by Amol Agrawal

Veeresh Malik has an article in Money Life: An otherwise modest increase in service tax from 12.36% to 14% on an all-India basis would have gone largely un-noticed and without causing much of a flutter had it not been for the simple fact that this small change appears to be setting off huge reactions. These […]

06 Jun 02:52

Many business models…

by subra

Anybody who does a business has to have a business model. Whether it works or does not work is a completely different ball game, but people need to have a business model and make an attempt to make it work.

If you do not have a business model, you cannot create a company, employ people, employ resources, raise debt, capital, …well you just cannot grow it. This is true of any operation – whether it is expected to make money or just render community service like helping the accident victims or run an organisation for helping the needy, poor, children, senior citizens, etc.

Let us take the Financial services Industry and the Running Industry. In the financial services industry the big daddies who make a lot of money is of course the banking industry. Banks make money from you by accepting deposits (and lending it to a borrower at a higher rate), selling 3rd party products (Insurance, mutual funds, Reit, gold, etc.). Mutual funds take your money and manage it for a fee. Immaterial of whether you make money or not the fund house makes money. They love a bull market because they get more investors and their asset management money goes up even more. Good business model. If there are 50 in our country they believe that another 400 can come in and make money.

Life insurance also is a story similar to the mutual fund business.

Then there is distribution of financial products. Banks, national level distributors, brokers are the big players who have a lot of assets and make a lot of money and keep growing the business. There are 4-5 players in the digital aggregation space and they also seem to be doing a good job and will make tons of money going ahead. However there are huge risks in the fund management business and in the distribution business – so much so that the pure mutual fund sellers are a dying community. Will big people with a lot of technological investments be able to make money? Not so sure. This is because the people who sell are not necessarily the best people to give advice on what to buy. Conflict of interest is another issue – so the buyer may not want advice from the guys who sell (or so say the text books).

Then come the financial planners – these are the people who tell you where to invest and how much in each scheme..well these are the people who might ask you to use a model where you reduce the cost of investing by going direct. This is a good method for people who do not need any hand holding.

All models seem to be working. In a country with such pathetic mutual fund penetration, it is obvious that all models need to exist. Not everybody needs an adviser, not everybody needs to go online, not everybody can go direct. Most RMs in banks have a book which runs into crores…All business models work.

Then there are some disruptive people. They write what works for them. No vested interest for sure. No interest in you either. They are evangelists. Narcissism, if you may. Journalists, experts, bloggers, …they generally write based on their own experience. No. They have not met fund managers, operations people, customers, analysts, …nothing. However they can write, so they write.

Some bloggers do not understand what they write. Some write for money. Some write for fun. Some take money and write like they are independent. Some are biased. Some can be bribed. Some are foolhardy. Some can see all the options. Some cannot understand, some will not. Many can be bribed. Some cannot be bribed. Or it has not been attempted bribing him…

Like I said…Many people, many models.

I like the paid model better than the risky ‘free’ model….

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

05 Jun 03:13

More on India's power sector woes

by noreply@blogger.com (Gulzar Natarajan)

Indian Express has this to say about the actual power generation,

Of the country's total installed generation capacity of 2,68,603 MW, the peak demand met on May 23 was less than half at just 1,34,892 MW... at last count, 57 base-load thermal units across India's northern and western heartland were faced with 'reserve shut-down', a technical term for a unit shut down due to lack of demand. Grid managers point to this being indicative of tepid industrial load compensating for a surge in mid-summer domestic demand.

And Economic Times has this,

2014-15 recorded the lowest plant load factor in over 15 years with the country's power capacities operating at a mere 65%... There are no takers for all the generation capacity that is in place. There is demand but they don't have the money to pay for the power due to the health of the discoms (state distribution companies)... discoms across all states had incurred accumulated losses of Rs 2.51 lakh crore in 2012-13... The average gap between power generation costs and tariffs charged by state discoms is now 82 paise and makes generation unviable... no new power generation project has been announced in the past two years and the low PLFs as well as lack of clarity on bidding parameters for new ultra mega power projects has made investments unattractive for now.

Reflecting, the low actual off-take, the CERC data on traded power price shows a continuously declining trend since 2009.

All these point to chronic distribution side weaknesses. Hobbled with massive debts and unable to even recover the full cost of service, distribution companies prefer the easy way out - load shedding or power cuts. The low capacity utilization is a reflection of this suppressed demand. Its impact on industries is debilitating.

Distribution sector reforms bounce against two very formidable challenges - political economy and state capability. Tariff increases, to capture atleast cost-recovery, will require political commitment across states, which may not be forthcoming. After a small blip the cost-revenue gap has been rising. Distribution loss reduction efforts appears to have plateaued off in recent years, with discoms finding it difficult to bring losses down below 20%. Only a handful of discoms have the administrative capability to carry out effective distribution feeder-wise energy audits over a long-enough period with sustained intensity that is required to bring down losses to single-digit levels.

There is more pain likely from the recent coal auctions for power projects. Promoters who have low-balled their bids, even quoting royalties to the government, in their eagerness to access fuel, have no option but to smuggle the fuel-charges into the fixed capacity charges. With the government firm on not allowing this, a face-off looks inevitable. Atleast some of the contracts are certain to unravel and others renegotiated. And this will all take up more time.

Unless the distribution side issues get addressed, it is only a matter of time before the vast majority of the stalled generation side investments that have gotten off the ground due to auctions and other recent measures get stalled again. In any case, given these demand trends, new investments will not be forthcoming as lenders and investors would be wary of putting their money in a sector where the demand side constraints appear insurmountable. The lack of new investments in the past two years will start to bite four years hence, severely constraining economic growth.

This is also a reflection of the difficult reform choices facing governments. Generation-side reforms, which are mostly decisional, are not where the constraints bind. The transactional challenges at the distribution side, involving managing the political economy and improving state capability, are where the real action is.

Solutions like selective feeder franchising skirts around the state capability problem but not the political economy one. However, it is possible that for certain categories of consumers, the political economy problem too can get addressed with a private provider. For example, industrial consumers, who currently suffer the brunt of erratic supply, are most likely to be willing to pay a higher tariff in exchange for reliability. Similarly, it may also be possible to get affluent consumers localized in certain pockets to agree for higher tariffs in return for reliability. The political economy as well as the credibility deficit with public distribution companies will come in the way of such a bargain by public entities.

The risk with this strategy is that it is likely to tip the system into another socially inefficient (albeit economically efficient) dual-market equilibrium, with reliable supply for certain (affluent) consumers serviced by private providers and erratic for other (poorer) consumers supplied by public discoms. But it is likely that the dynamics of competition set afoot by this would in turn force the discoms to become more efficient and also create the political environment for raising tariffs. But the transition can be disruptive and long-drawn. In the circumstances, the million-dollar question is whether the political establishment, across any Indian state, is willing to bite the bullet, and pursue this strategy, even if by stealth?

Solutions like selective feeder franchising skirts around the state capability problem but not the political economy one. However, it is possible that for certain categories of consumers, the political economy problem too can get addressed with a private provider. For example, industrial consumers, who currently suffer the brunt of erratic supply, are most likely to be willing to pay a higher tariff in exchange for reliability. Similarly, it may also be possible to get affluent consumers localized in certain pockets to agree for higher tariffs in return for reliability. The political economy as well as the credibility deficit with public distribution companies will come in the way of such a bargain by public entities.

The risk with this strategy is that it is likely to tip the system into another socially inefficient (albeit economically efficient) dual-market equilibrium, with reliable supply for certain (affluent) consumers serviced by private providers and erratic for other (poorer) consumers supplied by public discoms. But it is likely that the dynamics of competition set afoot by this would in turn force the discoms to become more efficient and also create the political environment for raising tariffs. But the transition can be disruptive and long-drawn. In the circumstances, the million-dollar question is whether the political establishment, across any Indian state, is willing to bite the bullet, and pursue this strategy, even if by stealth?

04 Jun 09:17

Adani Enterprises: What Happened Before 9:49AM Yesterday?

by Deepak Shenoy

We all know that there was a major demerger in Adani Enterprises yesterday. This involved shareholders getting shares of other companies, and the price of Adani Enterprises settled at Rs. 120 after yesterday’s Rs. 637.

But guess what, a few investors had no clue.

The markets opened at 9:15 am. For the first half hour, there was tiny volumes, but the price of the share kept dropping steadily, until it hit the 120 mark at which point it stabilized. People were apparently buying – in quantities like 5000 shares a minute or so, and the price went from Rs. 500 down, not instantly but gradually. The guy who bought at Rs. 500 would be super-unhappy.

This is very strange and obviously the first set of buyers had no idea this was happening. And it’s not really apparent why there wasn’t any heavy selling either. The first set definitely got gypped – but it really was their fault, since it was well known that the stock would say it.… (Read On...)

04 Jun 09:16

This Is How Delhi Cops Are Implementing Ban On Uber [158 Cabs Seized In 24 Hours]

by NextBigWhat

The Delhi transporation ministry has rejected the license of Uber and Ola citing legal violation issues and the transportation minister stated that they are working on a special plan to take action against banned taxi services in the capital.

Several teams will be formed to seize the taxis of such companies, said the minister.

The special plan is very simple.

Use the Uber app. Call the cab and seize it!

In the last 24 hours, the cops have caught 158 Uber cabs!

Smart way to implement ban on Uber in Delhi. Traffic Cops call Uber cab using APP, whn it comes, thy impound it. 158 caught in lst 24 hrs

— Anurag Dhanda (@anuragdhanda) June 3, 2015

Who says cops aren’t tech savvy !

And by the way, will this make Uber launch autonomous self-driving cars in India (before US)? #justkidding!

Uber Automonous Vehicle : Bring It ON!

The post This Is How Delhi Cops Are Implementing Ban On Uber [158 Cabs Seized In 24 Hours] appeared first on NextBigWhat.

04 Jun 03:20

Crazy Debt Levels and Falling Stock Prices – A Double Whammy For Lenders

by Deepak Shenoy

In a very smart piece, Value Research shows us how crazy our debt levels have gone. Here’s a good list: (Thanks @b50)

Lanco, for instance, is run by a politician, and has debt levels of 36,000 cr. If you sold all the shares of the company in the market today, you’ll get less than Rs. 1,200 cr. In fact, make that 1,100 cr. because the stock fell another 7% today. Probably someone tried.

This is not a good story but its what repeats in every single of the stocks above. Big debt, promoter pledging, and boom, we have a massive fall in the stock. Bhushan Steel (all you want to know about it) is in such a deep hole no one really knows what to do – they now have over Rs. 38,000 cr. in debt, and are valuing the coal blocks, where allocations to them have been cancelled, at cost because they believe they will be paid back.… (Read On...)

04 Jun 03:20

Do Something Syndrome

by Shane Parrish

“We trained hard, but it seemed that every time we were beginning to form into teams we would be reorganized. I was to learn later in life that we tend to meet any new situation by reorganizing, and what a wonderful method it can be for creating the illusion of progress while producing confusion, inefficiency, and demoralization.” — Roman satirist Petronius Arbiter

I was flipping back through one of my favorite books, Seeking Wisdom, when I came across this quote in the section where Bevelin talks about ‘Do Something Syndrome.’

There is something almost poetic in the way that Petronius so succinctly captures a phenomenon that most of us have been through.

There are numerous reasons why someone may choose action over the more logical course of inaction — some conscious and others subconscious. We may, for instance, act on bad advice when we haven’t done the work to understand a problem, we may succumb to peer pressure, the idea that ‘everyone is doing it,’ we may follow our hearts (and buy that fancy car we really want instead of keeping the reliable one we have), blindly follow the lead of an expert, or, perhaps most dangerously, we may simply want to appear like we are doing something.

Maybe we just can’t sit still. This idea isn’t new.

“I have often said that the sole cause of man’s unhappiness is that he does not know how to sit quietly in his room.” — Blaise Pascal

We all have moments where we fall victim to the curse of Do Something Syndrome. In fact the modern organization is full of do something syndrome. The key is to try and realize when we are doing it and back away.

So next time you feel the urge to do something for the sake of doing something remember these words of wisdom from Bevelin:

The 19th Century American writer Henry David Thoreau said: ‘It is not enough to be busy; so are the ants. The question is: What are we busy about?’ Don’t confuse activity with results. There is no reason to do a good job with something you shouldn’t do in the first place.”

Charles Munger says, ‘We’ve got great flexibility and certain discipline in terms of not doing some foolish thing just to be active – discipline in avoiding just doing any damn thing just because you can’t stand inactivity.’

What do you want to accomplish? As Warren Buffett says, ‘There’s no use running if you’re on the wrong road.’

Still curious? Most of what you’re going to do today is not essential.

--

Sponsored By: Greenhaven Road Capital: You think differently - now invest differently.

04 Jun 03:06

Prisoner’s dilemma (not the game theory one)..

by Amol Agrawal

Gopalkrishna Gandhi has a stirring tale of state of our prisons: Imagine—for a moment—you are in prison. You may have committed a crime which has thrown you into the slammer, or you may not have. You may be innocent and should not be where you are. A violation of traffic rules, a momentary lapse of judgment, […]

04 Jun 02:15

Tough questions that your adviser will NOT ASK

by subra

Most of us want to be DIY but have almost no comprehension of what it takes to be a Do It Yourself Investor. An adviser quickly sizes up the investor and decides how much to interfere with a client or whether there is any need to disturb the client’s learning process.

However all investors need to answer these questions. If they have an adviser he/she should help them through this trauma:

1. If you do not know how much return you are getting in each of your investment (your return not the scheme CAGR. Go and check it out. See if there is a difference.

2. 99% of the people reading this blog will be better off with low cost investing – and in India that need not be the Index.

3. A good fund manager with a good track record will not come free. A good adviser who knows his job will more than justify his fee.

4. It is very difficult beating the market on a consistent basis. Hey, it is not impossible either. Do give it a swing….and I do not know why you keep chasing every trip.

5. Do you really understand conflict of interest?

6. Are you really an aggressive investor ? If the sensex tanks 25% will you buy aggressively?

7. I know you like jargon, but just because you are a contrarian it does not mean you will drive when the signal says stop.

8. I know you invested because of your gut feel, but sir, your gut sucks. My elementary Investment valuation 101 would have warned you against this.

9. Of course I do not like RMs, but your 3 Ulip plans are amazingly stupid investment decisions, but I can live with that.

10. Buying from your RM just because he calls you 1222 times a day is as bad as sexual harassment that your boss did to your young married friend. Just change your bank branch or RM.

11. Your younger age mistakes were much better…your latest Unit linked plan with a committment of Rs. 200,000 per month for 3 years is SUPER AMAZINGLY STUPID. Now go live with that.

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

03 Jun 09:49

What makes HDFC Equity Mutual fund one of the oldest and successful funds?

by Amol Agrawal

It is always an interesting question. What makes an mutual fund equity fund scheme successful over a long run? Based on efficient market theory, one should not really be seeing a active mutual fund beat markets over a long run. I mean some short term performance can be signalled to just luck which reverses soon as we […]

03 Jun 09:49

Is Make in India campaign copied from Swiss land?

by Amol Agrawal

Not sure how much truth is there to this. There is an eerie similarity of the lion used in Make in India campaign to a similar lion (on the wheels as well) used by a Swiss Bank (Cantonal Bank of Zurich in Switzerland). The govt obviously refutes. I doubt it, given how lion is such […]

03 Jun 09:49

Steel is the stand-out example of this over-capacity,

Steel is the stand-out example of this over-capacity,

China over-capacity fact of the day

by noreply@blogger.com (Gulzar Natarajan)

From an excellent article in the WSJ, on how the massive excess capacity in China is exacerbating global disinflation and economic weakness,

Milk producers in New Zealand, coal miners in Australia and sugar growers in Brazil have been forced to cut their prices after finding they had overestimated commodity demand from China. At the same time, Chinese manufacturers, stung by their country's economic slowdown and excess capacity, are flooding export markets with finished goods such as tires, steel and solar panels.

With China’s slumping construction industry requiring less steel than had been expected, the country has become a massive global exporter of the metal, weighing on global prices. Last year, China exported 94 million metric tons of steel, more than the total output of the U.S., India and South Korea, the world’s third, fourth and fifth largest producers. UBS analysts estimate the world has excess steel-production capacity of 553 million metric tons a year, much of it in China. That is enough to build more than 10,000 modern aircraft carriers a year, or the Eiffel Tower 75,000 times annually. The price of a common steel product called hot-rolled coil has dropped by 44% since March 2012...

The pace and scale of expansion in all these sectors was staggering and carried seeds of their own demise. Consider the example of tire industry with its linkages,

Between 2000 and 2013, China’s tire production soared threefold to about 800 million tires a year as the country grew into the world’s biggest auto market... Producers exported many of those tires, occasionally drawing complaints from tire industries in the U.S., Brazil, Turkey, India, Colombia and Egypt that China was dumping its excess supplies on their markets. All six nations imposed tariffs on Chinese tires... the more than 300 tire makers in China operate at 70% of capacity, far below the 85% that economists say is needed to generate profits. Chinese tire exports increased tenfold between 2000 and 2013.

Guangrao, a county in eastern China, is home to about 200 tire factories in an area dubbed Rubber Valley... Rubber Valley’s problems have rippled out to other countries, including ones where planters produce the raw material for tires. Rubber trees take about seven years to mature. Planters had to decide in 2007—when China’s gross domestic product expanded by 14.2%—how many trees to plant to meet demand in 2014. When it was time to harvest, the Chinese economic growth rate had fallen by about half... the price of the milky white sap, called latex, that is processed into rubber is down 60% from its high four years ago.

03 Jun 09:47

What’s your favourite day or time of the week? For somebody like me with a Monday-Friday job, the favourite part of the week usually is Saturday morning.

Latticework of Mental Models: Redundancy

by Anshul Khare

This article is the seventh of this weekly series called Latticework of Mental Models, which will be authored by my friend and partner in writing the Value Investing Almanack, Anshul Khare. Anshul will write on various mental models – big ideas from various disciplines – which can help you think more rationally while analyzing businesses and making your stock investment decisions.

What’s your favourite day or time of the week? For somebody like me with a Monday-Friday job, the favourite part of the week usually is Saturday morning.

Now, what could be the best way to ruin a Saturday morning? Let me tell how I (almost) achieved the feat.

On a cool and breezy weekend morning when most people prefer to sit in the balcony and sip on a hot beverage, I was standing just outside my front door with milk packet in hand and toothbrush in my mouth, wondering why do they build these auto-lock doors.

Yes, you guessed it right. I managed to lock myself out of my house. Everything including my keys, glasses, cell phone, wallet, and slippers were behind the door which was slammed shut by the very same saturday morning breeze.

However the story had a happy ending when I was rescued by my saviour. Saviour? Yes and it was none other than our mental model for today – Mr. Red (short for Redundancy).

Fortunately I had kept a spare key with my trustworthy friend living few blocks away. I quickly ran to his house, got my spare key and thanked Mr. Red.

Although it did raise few eyebrows among the neighbours when they saw a guy with disheveled hair, scurrying across the street barefoot with a milk packet in hand and toothbrush sticking out from mouth. Forgive me for being little too dramatic here but please stay with this post for a little longer to know more about the insightful personality of Mr. Red.

I know that sharing a spare key isn’t a novel idea. People do it all the time but it highlights the significance of building redundancy in our day to day affairs. If redundancy is so important in such small matters, imagine its utility in other critical matters. That’s what we are going to explore today. So let’s start with a working definition.

Redundancy is defined as the existence of more than one means for accomplishing a given task. To be more specific, redundancy refers to the process of adding ‘extra’ instances of critical components to a system so that one can take over for another if something breaks. Thus all of these ‘instances’ must fail before there is a system failure.

Look around you. Spare tyre in your vehicle, power backup generator sets in your apartment, fire exits in your office building, etc., are all typical examples of redundancy designs.

To an untrained eye, redundancy may seem ambiguous because it looks like a waste of resources if nothing unusual happens. Except that the complexity of modern world ensures that the unusual would happen quite frequently and unexpectedly.

Have you ever keenly observed the nature? It’s the best place to learn about redundancy.

Redundancy in Nature

If you look at the mother nature it’s easy to see that redundancy is everywhere. Nassim Taleb writes in Fooled by Randomness –

Mother Nature likes redundancies…the simplest to understand, is defensive redundancy, the insurance type of redundancy that allows you to survive under adversity, thanks to the availability of spare parts. Look at the human body. We have two eyes, two lungs, two kidneys, even two brains – and each has more capacity than needed in ordinary circumstances.

So redundancy equals insurance, and the apparent inefficiencies are associated with the costs of maintaining these spare parts and the energy needed to keep them around in spite of their idleness….Layers of redundancy are the central risk management property of natural systems.

A lot of species in animal kingdom give birth to multiple offsprings (it’s common for some insects and fishes to lay millions of eggs in a single season) to ensure that at least some of them survive and carry forward the gene. Isn’t that redundancy? Nature likes to over-insure itself.

As an aside to the central argument of redundancy, it’s worth mentioning an interesting insight which comes from Bill Gates. One of the focus areas for his philanthropic initiatives is to improve the child survival rates in poor African countries. For many naive armchair philosophers, it seems counter intuitive because logic says that instead of focusing on saving newborns, we should educate the poor women to have fewer kids since it’s common in these countries for families to have 3-4 children. Moreover saving children will eventually lead to a bigger population in future which in turn will worsen the living conditions further. Right? Wrong!

Look at this situation from the lens of redundancy mental model. One of the reasons people (and this could be a subconscious drive instilled by nature) have multiple children is – they assume some of those children aren’t going to survive to adulthood because of poor health care facilities. However Mr. Gates’ argument is that the moment you improve the survival rate for children, people won’t feel the need to have multiple children. So, over the long term, you end up eliminating the root cause of population growth. It’s a brilliant insight.

Let’s now shift gears a bit and turn to the field of engineering.

Redundancy in Engineering

We saw redundancy in nature is quite common but this mental model can be formally categorised as a big idea from the field of Engineering.

In fact, when it comes to software engineering, building backup and additional redundant capacity is at the heart of architecting software systems. Large software enterprises (including Facebook, Google, Twitter, and all the banks) go as far as having multiple data centers spread across continents to ensure that even large scale catastrophic events don’t cause irrecoverable damage.

Most of the commercial airliners have multiple engines so in case of failure of even a single engine, the flight can continue with spare engines. And not just the engine, most of the critical parts in an airplane have redundancy of some form or other.

In fact, while designing critical systems, it doesn’t suffice to build redundancy based on the historical worst case scenario. You actually have to overcompensate. Because the so-called worst-case event, when it happened, exceeded the worst case at that time. Nassim Taleb has named this inconsistency as “The Lucretius Problem”.

Redundancy in Investing

The great Chinese philosopher Confucius said –

The superior man, when resting in safety, does not forget that danger may come. When in a state of security he does not forget the possibility of ruin. When all is orderly, he does not forget that disorder may come. Thus his person is not endangered, and his States and all their clans are preserved.

One of first things advised for personal finance is to create an emergency fund for yourself. This fund should cover 6 to 8 months of your expenses and it should be kept ultra safe i.e., either in FDs or liquid funds. That’s creating redundancy for securing the future of your family. Getting adequate medical and life cover adds additional redundancy.

The father of value investing, Benjamin Graham, pioneered the concept of margin of safety which is nothing but building redundancy in your investment portfolio. Warren Buffett, in his 1993 letter to investors, says –

We insist on a margin of safety in our purchase price. If we calculate the value of a common stock to be only slightly higher than its price, we’re not interested in buying. We believe this margin-of-safety principle, so strongly emphasized by Ben Graham, to be the cornerstone of investment success.

In fact, having redundant cash in your investment kitty isn’t merely a defensive strategy. Come a market crash and your defensive strategy opportunistically turns into an aggressive strategy. It’s more like an investment rather than insurance.

For that matter, debt is the inverse of redundancy. It not only takes away the safety, it actually makes your finances extremely fragile in the face of unexpected adversity.

Where It Fails

Before we become too obsessed with the idea of redundancy, it’s important to understand its limitations, lest we become the proverbial man with the hammer to whom every problem looked like a nail.

Can redundancy backfire? Shane Parrish, in his blog Farnam Street, explains it wonderfully –

First, in certain cases, the added benefits of redundancy are outweighed by the risks of added complexity. Since adding redundancy increases the complexity of a system, efforts to increase reliability and safety through redundant systems may backfire and inadvertently make systems more susceptible to failure. An example of how adding complexity to a system can increase the odds of failure can be found in the near-meltdown of the Femi reactor in 1996. This incident was caused by an emergency safety device which broke off and blocked a pipe stopping the flow of coolants into the reactor core. Luckily this was before the plant was active.

Second, redundancy with people can lead to social diffusion where people always assume it was someone else who had the responsibility.

Another way in which redundancy can cause damage is when it makes people overconfident. How?

You must have heard this joke floating around on the Internet – You don’t need a parachute for skydiving. You need it for trying skydiving more than once.

Every skydiver jumps with a reserve parachute. What if even the second doesn’t open up? Well…so much for skydiving! Irony is that presence of a backup promotes the skydivers to attempt even riskier maneuvers which defeats the purpose of having additional safety.

Similarly, as the automobiles become safer, drivers go faster and take on more risks. Same in case of sports too. The recent tragic demise of an Australian cricketer Phil Hughes can probably be attributed to the same reason.

Facing express bowlers of the past, whether Harold Larwood, Andy Roberts or Malcolm Marshall, helmet-less batsmen were less inclined to play the hook—a shot that involves swatting a short-pitched ball from in front of your nose—because of the danger of getting it wrong. They were also more likely to keep their eye on a threatening ball and sway out of the way at the last moment, as the coaching manual demands. Today, with greater protection, there seems to be more of a propensity for batsmen to flinch and turn their backs on anything nasty… those with exposed heads were more likely to play back-foot shots, which give batsmen extra time to follow the flight of the ball. (source: Economist)

So do you see the paradox of redundancy?

Nonetheless it’s an important mental model and extremely useful one in designing systems around us.

Conclusion

If you thought that after that fateful Saturday morning, I would have learnt my lesson, then you are underestimating me. I repeated the same blunder but this time with my car and as usual Mr. Red saved me again.

I guess it should be obvious to you by now that creating redundancy doesn’t mean avoiding the worst case scenario, but it assumes that the worst case will happen time to time and then making arrangements to minimize the harm.

So please don’t forget to make friends with Mr. Red.

Now that we have learned some mental models in past few weeks, the next questions is what to do with them? Shane of Farnam Street again answers this question beautifully –

After we learn a model we have to make it useful. We have to integrate it into our existing knowledge. Our world is multidimensional and our problems are complicated. Most problems cannot be solved using one model alone. The more models we have the better able we are to rationally solve problems. But if we don’t have the models we become the proverbial man with a hammer. To the man with a hammer everything looks like a nail. If you only have one model you will fit whatever problem you face to the model you have. If you have more than one model, however, you can look at the problem from a variety of perspectives and increase the odds you come to a better solution.

As always I would urge you to become a proactive learner. Reading educates, but when you put your own independent thinking to what you learn, it makes the lesson last longer. So I invite you to take a pause for few minutes and think about your own experiences and observations where these mental models might fit in.

If you can share them in Comments section of this post, others (including me) would benefit from your thinking and of course just the act of writing will unleash interesting insights in your own head.

So what are you waiting for? Lose the mouse, grab the keyboard and start typing.

It is my sincere hope that the latticework series will enrich your world by making it a more profitable and enjoyable place to invest, work, and live.

Take care and keep learning.

The post Latticework of Mental Models: Redundancy appeared first on Safal Niveshak.

03 Jun 09:25

What a Good Financial Adviser Must Do

by subra

There are many financial advisers in the world and many are wondering whether they will be replaced by an algorithm! Sure people can create software that can replace financial advisers, but certain things will keep the client with you, if you do it well:

1. Establish a great relationship: If you are the ‘Go To’ person for your client – whether it is a change of job, or career guidance for their kids, or changing home…if you establish a good relationship, chances are the client will stay with you and not go dating a computer!!

2. Have the guts to be blunt: If you have enough confidence to predict the future, do you have the guts to tell the client what can happen and what cannot? The ability to make the client understand the risk-return relationship, the fact that the next 5 years may see a sub par equity and debt funds run. Do you have the guts to say that the client has to increase his contribution?

3. These days I am seeing IFAs trying to fit too many things because they are afraid that the client will leave. This is funny. If you are an IFA clear the air and tell the client what he can get and WHAT HE CANNOT. Just because he is paying you a fee it does not mean he owns you. BE CLEAR IN YOUR communication.

4. Communicating to each client as per his emotional, psychological understanding is a very important professional requirement. Some clients do not mind discussing their personal life in public, most professionals can handle….

5. When a client visits too many websites, he might get a lot of impossible ideas. Be close to the client, to reality, and tell him what to read, what to believe and tell him like porn, do not build wrong expectations. It does not help in the long run.

and many more!!

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

03 Jun 09:16

Adani Enterprises Has Not Crashed 80%. It’s Been Demerged.

by Deepak Shenoy

Adani Enterprises seems to have fallen big time. Looking at the stock price, you wonder if Modi’s magic has completely collapsed!

But it’s not like that.

Adani Enterprises has been “demerged”, in a weird sort of way.

Adani Enterprises owned some stuff that were related to ports, power, and transmission. These, they decided, belong in specific companies. Adani ports and Adani Power are already listed entities, so the power plants and port operations move to those companies.

Adani Enterprises had investments in the Belekeri port in Karnataka, and also owned a big stake in Adani ports. This goes back into the ports business. In exchange, Adani Enterprises shareholders get shares of Adani ports (14,123 shares of Adani Ports for 10,000 shares of Adani Enterprises).

Adani Enterprises also had power assets and ownership they will pass on to Adani Power. Shareholders of Adani Enterprises will get 18,596 shares of Adani Power for every 10,000 shares in Adani Enterprises.… (Read On...)

02 Jun 03:43

The Three Marriages: Reimagining Work, Self and Relationship

by Shane Parrish

“Work-life balance is a concept that has us simply lashing ourselves on the back and working too hard in each of the three commitments. In the ensuing exhaustion we ultimately give up on one or more of them to gain an easier life.”

Few books I’ve read contain more marked passages and pages than David Whyte’s passionate and thought-provoking book, The Three Marriages: Reimagining Work, Self and Relationship, which argues we should stop thinking in terms of work-life balance.

The current understanding of work-life balance is too simplistic. People find it hard to balance work with family, family with self, because it might not be a question of balance. Some other dynamic is in play, something to do with a very human attempt at happiness that does not quantify different parts of life and then set them against one another. We are collectively exhausted because of our inability to hold competing parts of ourselves together in a more integrated way.

Whyte argues that we come to a sense of meaning and belonging “only through long periods of exile and loneliness.”

Interestingly, we belong to life as much through our sense that it is all impossible, as we do through the sense that we will accomplish everything we have set out to do. This sense of belonging and not belonging is lived out by most people through three principal dynamics: first, through relationship to other people and other living things (particularly and very personally, to one other living, breathing person in relationship or marriage); second, through work; and third, through an understanding of what it means to be themselves, discrete individuals alive and seemingly separate from everyone and everything else.

These are the three marriages, of Work, Self and Other.

These three lifelong pursuits, Whyte believes, “involve vows made either consciously or unconsciously.” Neglecting any one of these “impoverishes them all” because they are not mutually distinct but rather “different expressions of the way each individual belongs to the world.” Our flirtation with each differs and yet we are left to inter-weave the vows into a cohesive person, consciously or unconsciously.

Whyte’s premise is also his conclusion:

We should stop thinking in terms of work-life balance. Work-life balance is a concept that has us simply lashing ourselves on the back and working too hard in each of the three commitments. In the ensuing exhaustion we ultimately give up on one or more of them to gain an easier life.

… [E]ach of these marriages is, at its heart, nonnegotiable; that we should give up the attempt to balance one marriage against another, of, for instance, taking away from work to give more time to a partner, or vice versa, and start thinking of each marriage conversing with, questioning or emboldening the other two. … (once we understand they are not negotiable) we can start to realign our understanding and our efforts away from trading and bartering parts of ourselves as if they were salable commodities and more toward finding a central conversation that can hold all of these three marriages together.

Perhaps this resonates with me more than most because I’ve always found the argument that we should live a balanced life lacking. At its heart this implies we should trade one aspect for another, compromising as we go. To me this trimming of excess in one area to prop up another serves to remove, not create, meaning.

The other argument that Whyte surfaces penetrates the fabric of our human needs: the constant tug of war between our social desires and our need for space. This is another area where we naturally try to find balance and in so doing compromise part of ourselves.

The Three Marriages: Reimagining Work, Self and Relationship “dispels the myth that we are predominately thinking creatures, who can, if we put our feet in all the right places, develop strategies that will make us the paragons of perfection we want to be, and instead, looks to a deeper, almost poetic perspective.”

--

Sponsored By: Greenhaven Road Capital: You think differently - now invest differently.

02 Jun 03:39

Overconfidence: sure way to lose money

by subra

Why do people lose money in the equity market? Well there are many and I have written a lot about this…so a few more:

1. I have seen people take contrarian positions while doing a trade: for e.g. going long on Tata Motors and going short on Tata Steel. The reason? hoping that one of them will be right. This is funny because unless there is some very specific reason for taking such a view such pair trades normally hurt. So this guy who is a TRADER, calls himself an Investor and gets the community a poor name.

2. You have very strong political views and you will be bullish because NDA is in power and you are a BJP supporter: this is bullshit, but true.

3. Your expenses increase 2x your increments. Then there is a leverage asset buying spree also !! So money does not stay with you

4. Your SIP amount assumed that equity will give 18% return, so far your return has been 12%….but you are hoping for a reversion to the mean

5. You are sure that the market will turn around so you are doing SIPs more aggressively. God bless you.

6. You knew of course nothing would happen to you because you are generally healthy. However in one of your trips to London, the walk from the station to the taxi stand had too much of snow and it took a toll of your leg…

many many more….

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

02 Jun 03:20

What have we learned from the crises of the last 20 years?

by Amol Agrawal

Stan Fisher sums up the lessons he has learnt over the years. He misses the most important lesson – know the financial history and know it really well. Infact history is not even a word in the speech. Infact, if one follows history then you are unlikely to hype certain phases of economic and stock market growth […]

31 May 03:41

----------------

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.

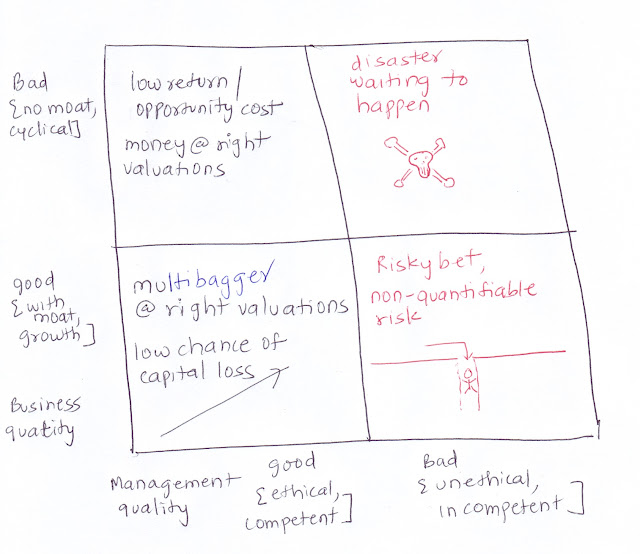

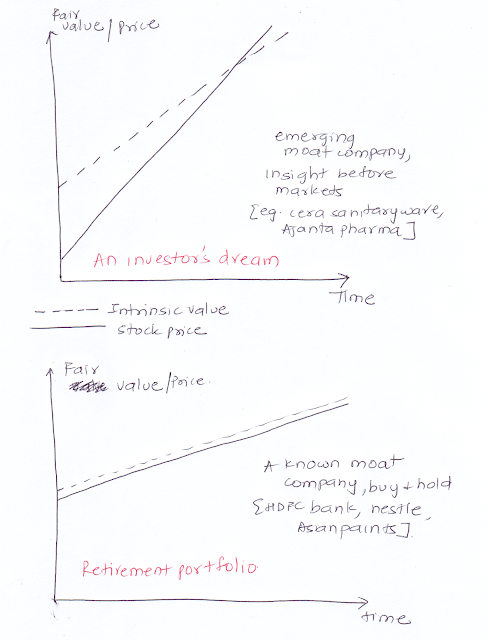

A picture worth a thousand words ?

by Rohit Chauhan

It is said that a picture is worth a thousand word. Hopefully ,some of the crudely drawn ones below, by yours truly are worth atleast a few words.

The Matrix

Time, Value and price

----------------

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.

30 May 04:38

How to buy a property?

by subra

A friend with pots of money wanted to invest in RE. So he went to a Mid sized mid Mumbai builder (for So Bo people Worli is not So Bo)…and asked for the price of a flat..he was told Rs. 18 for a flat. He saw a few flats and did not revert to the builder’s manager.

The manager called a few times and when this person said ‘yes i wanted to buy a few flats’ he got his boss the MD/owner to call him.

So they met…and this friend goes with a cheque book visible kept in the top pocket….and the conversation (as told to me) goes like this:

Builder: I heard you wanted to buy a few flats…

Friend: Yes, I have some money to invest for 5-6 years and was looking for an opportunity

Builder: How will you pay

Friend: Cheque, here is my cheque book…and puts it on the table and keeps his pen on top of the cheque book.

Builder: How much money do you wish to invest SIR?

F: I wish to buy 3-4-5 flats..tell me the price

Builder: Sir 4 flats will be Rs. 72

F: Chief that I know the math, please tell me the cheque amount for 4 flats

B: Sir 72 is the sticker price, will give it to you at Rs. 36..immediate cheque..NOW.

F: Here is a cheque for 36..i will leave it with my lawyer…he will whet the agreements…and make the payment across d table…

Moral: My friend got a 50% discount….this was not small.

Learning: My F told me he did not do any home work, but his brother tells me, they did fantastic background work. He found out that a builder in mid Mumbai had a payment to make to a housing finance company and was willing to borrow Rs. 100 for a period of 2 years. He was willing to pay up to 24% interest. This is a very good deal – considering that the was willing to give 10 houses costing Rs. 18 crs – which meant a 50% margin – almost. So this friend of mine knew that the builder was a) short of cash b) interested in preserving his credit rating c) desperate to sell the flats.

After knowing this he carried out this operation.

Learning for u and me:

We may not be in a position to sign a big cheque, but we can use FB and create a group for buying a flat. Suppose you are able to collect 20 people wanting to buy in Ulwe (a happening place!!! if u believe the RE dominated press). Once you have 20 people YOU can take the initiative buy land and build a building on your own. Instead of that go to a builder (Goldilocks – not too big not too small and negotiate. I will eat my right arm if you do not get a huge, hefty discount – from the builder AND from the financing company – free search fee, waiver of admin charges, discounted rate…..

WE DO NOT KNOW HOW TO BUY REAL ESTATE….THAT IS THE PROBLEM….

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

27 May 02:17

Yash Birla has a Swiss Account, what next?

by Manshu

PTI reported today that industrialist Yash Birla, along with four other lesser known businessmen hold Swiss bank accounts as confirmed by the Switzerland authorities.

This news apparently delighted the finance minister who chalked this to successful diplomacy and cooperation between the Modi government and the Swiss government.

Almost all news articles I read talked about Yash Birla as if he were guilty already, and I was unsure as to what the charges were.

It seemed at first that holding a Swiss account that wasn’t disclosed to the Indian IT authorities is what these individuals did wrong, but if that were the case then I wasn’t sure why the Swiss decided to release these five names only. Surely, a lot more than five Indians hold Swiss accounts. Also interesting is the timing of the release because the Indian government does complete a year today, and this timing is rather perfect for them.

Deutsche Welle which is an international German newspaper also reported the story, and had a little more breadth to their reporting because of the international angle that the Indian papers lacked.

Switzerland has begun online publication of names of foreigners and foreign firms wanted in tax probes by their countries of origin, including Germany. American citizens are identified only by their initials.

So, from this piece of information you can gleam out that the reason why these names are published is that the Indian authorities have specifically asked for certain individual names from the Swiss stating that the Indian government is investigating these individuals for tax frauds.

The second big question is why the Indian government asked about some individuals specifically, and the article refers to names from the stolen list that became popular some time ago.

So, to that effect these names were present in a list of people who used to have Swiss accounts at one point in time, and now that the Swiss Authorities have confirmed that these people did in fact have Swiss Accounts at one point or the other — I imagine the Indian authorities will encourage these individuals to voluntary declare their incomes under the new Black Money Act and pay the fines per the new regulations.

I assume that Indian authorities will do that because there is still a very long way to go for India to actually get any details of how much money is there in these Swiss accounts or in fact if there is any money at all present there.

Would the people named in the stolen list have done nothing during this time?

And if there is no balance there presently, will the Swiss be willing to share where that money went? I wouldn’t bet my money on that.

I would like to see how this progresses and in fact if the IT department is able to do anything with just this confirmation since it doesn’t actually tell you the amount of money in the account, and I can’t imagine much being done without that information.

Also, if you haven’t read about this at all yet, this is a good article that will catch you up with the parts I assumed you have read already.

Update: An official spokesperson of Yash Birla Group has said that Yash Birla has no individual bank account in his name or in his control.

27 May 02:15

Scary 20 years yet what happened?

by Muthu

I was going through a HDFC mutual fund presentation. It has listed some negative things which have happened during last twenty years. Going through that, I developed the idea to write this post.

In 1996, Congress lost the general elections. This resulted in communist supported and participating third front government coming to power. A hardcore communist, Indrajit Gupta, was India’s home minister from 1996 to 1998.

You would also remember that BJP first came to power in 1996 and could survive only for 13 days. So between 1996 and 1998, there was huge political uncertainty and we had three governments in 3 years.

In 1997, Asian financial crisis happened. Much of East Asia went through severe currency crisis raising fears of serious economic meltdown.

In 1998, BJP again formed government, which only lasted for 13 months and was in constant turmoil due to tantrums of coalition partners.

In 1998, Indian conducted nuclear tests. Western sanctions were imposed crippling the country’s financial situation.

In 1999, we had a fight with our neighbour Pakistan. Kargil war brought both the nations to brink of a major confrontation.

In 2000, tech bubble burst. Technology stocks world over crashed eroding investors’ wealth.

In 2001, 9/11 attacks happened, creating a huge geo-political crisis. Markets tanked.

In 2001, Ketan Parekh scam happened. UTI crisis happened. IT stocks in India lost value as much as 90%.

In 2001, Indian parliament was attacked by terrorists.

In 2004 general elections BJP lost. Congress government dependant on left support for survival came to power. There was common minimum program and weekly breakfast meetings. Government has to keep on yielding to the left tantrums to stay in power.

After 2004, the global commodities prices started rising. Oil prices also started rising sharply.

In 2008, global financial crisis, considered as worst financial crisis after great depression happened. World markets collapsed, Sensex dropping more than 50%.

In 2008, Mumbai terrorist attack happened.

From 2010-13, corruptions, scams and scandals started hitting the government. 2G, Common Wealth Games and Coal gate are some of the major scams. UPA-2 was most part immobilised and was fighting one corruption scandal after another.

In 2013, markets panicked due to QE tapering worry. GDP growth slowed down. Current Account Deficit (CAD) and Fiscal Deficit (FD) worsened threatening ratings downgrade. Inflation was very high and the currency weakened.

In 2014, rise of ISIS.

If somebody looked for a certainty or lack of problems, he would have never found an opportunity to invest. Every day newspapers and 24/7 media would have never given him courage to go ahead.

Despite all the above problems, companies have grown, their sales and profits have grown, earnings and hence Sensex has grown, mutual fund’s returns have grown… lot of every day growth which would not make into daily news have been continuing to happen.

As I’ve mentioned earlier, many mutual funds multiplied investor wealth by 40 to 100 times during the above period.

As per a CRISIL study last year, during the past 17.5 years, equity funds as a category has given a return of 22.6%.

Despite worrying events and scary headlines, if one has stayed invested, he would have multiplied his wealth many fold.

Investors who bet on Indian entrepreneurism and the future of this country have been amply rewarded. What set of problems and issues we would face in next 20 years is not known now. But we can be sure that there would continue to be global and domestic challenges, surprises and shocks, scams, bull and bear markets in next twenty years as well.

Despite that we would continue to grow and both quantum and quality of growth would be much superior to what we have seen in the past.

If you believe this and invest accordingly, you can very well be part of this India growth story and reap rewards.

All you need to do is to keep looking far ahead (the bigger picture), ignore every day news, have great degree of patience and give time for your investments to grow into fortune.

Uncertainty would continue. We cannot wish it away. Though it may sound paradoxical, accepting every day uncertainty would bring certainty of wealth in the long run.

26 May 08:48

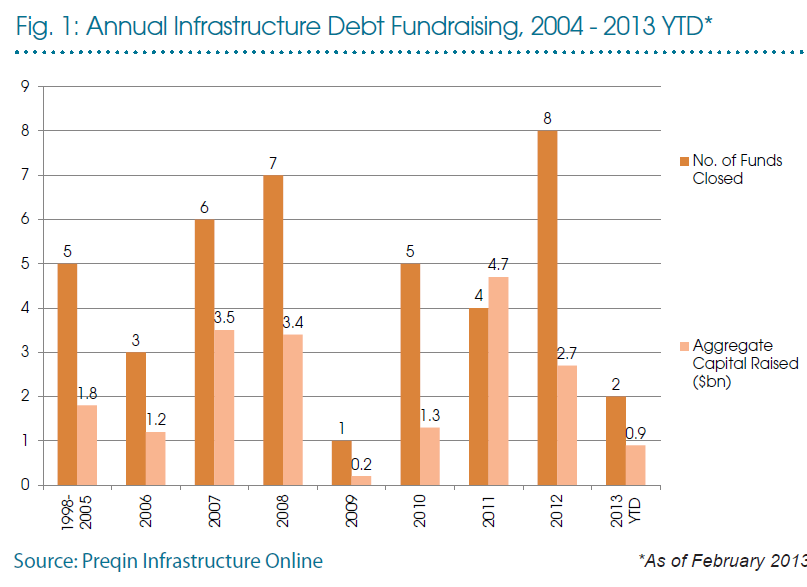

The infrastructure financing problem

by noreply@blogger.com (Gulzar Natarajan)

Where does infrastructure financing money come from? I blogged earlier about how, contrary to conventional wisdom, the overwhelmingly dominant share of infrastructure financing comes from bank loans and the bonds have a marginal role.

But for China, syndicated loans form the lion's share of infrastructure financing. The total annual infrastructure bonds raised have been around $10-12 bn for all emerging markets excluding China.

And about infrastructure debt funds, the amounts raised globally are minuscule compared to the requirement. Just $4.7 bn was raised in 2011, the highest ever raised globally in a year by infrastructure debt funds.

Infrastructure equity funds, which leverage capital from pension funds, while larger, too form a small share of the total infrastructure financing and are concentrated in developed markets, especially the US and Europe. Globally, they formed just above $36 bn in 2013.

Furthermore, structured equity or debt financing - infrastructure equity fund, infrastructure debt funds, or bonds - is rarer still in the construction phase, where bank loans are the most risk-appropriate form of financing. So as India explores various infrastructure financing alternatives, it would do well to keep in mind the reality that bank loans would necessarily have to form the lion's share of infrastructure financing. Alternative sources like structured debt and equity can only contribute marginally. This again underscores the importance of restoring bank balance sheets and their recapitalization.

In any case, whether financed through loans or structured capital, rigorous project preparatory work is critical to the success of any long-term project. These projects will be able to attract private investments only if adequate preparatory work is done and rigorous enough feasibility and commercial viability studies and detailed project reports are available. Its preparation generally takes at the least 18-24 months. It may therefore be appropriate if, atleast to the extent of flagship infrastructure projects, a shelf of works are identified and their due-diligence and documentation initiated immediately, through public finance, and kept investment-ready.

Update 1 (31.05.2015)

The sample of the latest Preqin report is here and it contains this graphic which points to the rising share of infrastructure assets in the portfolios of investors. In 2014, institutional investors had just 4.3% of their assets invested in infrastructure assets, against their target of 5.7%. The report states that 67% of the investors surveyed had plans to increase their infrastructure allocations.

As the FT reports, even a one percentage point increase of allocation can be dramatic. Pension funds, insurers and other big pools of long-term investors seeking investments in assets other than cash, stock, and bonds have $65 trillion in assets. Even a four percentage points allocation is several times the current investments. In fact, of the $296 bn worth unlisted infrastructure assets under management by June 2014, over $100 bn are yet to be committed funds, of which $13 bn is earmarked for Asian markets.

As the FT reports, even a one percentage point increase of allocation can be dramatic. Pension funds, insurers and other big pools of long-term investors seeking investments in assets other than cash, stock, and bonds have $65 trillion in assets. Even a four percentage points allocation is several times the current investments. In fact, of the $296 bn worth unlisted infrastructure assets under management by June 2014, over $100 bn are yet to be committed funds, of which $13 bn is earmarked for Asian markets.

There is a long-term dynamic driving this movement towards long-term infrastructure assets. Stagnant low yields in standard asset classes have forced asset managers to lower their target returns, making infrastructure assets extremely attractive.

There is a long-term dynamic driving this movement towards long-term infrastructure assets. Stagnant low yields in standard asset classes have forced asset managers to lower their target returns, making infrastructure assets extremely attractive.

Update 1 (31.05.2015)

The sample of the latest Preqin report is here and it contains this graphic which points to the rising share of infrastructure assets in the portfolios of investors. In 2014, institutional investors had just 4.3% of their assets invested in infrastructure assets, against their target of 5.7%. The report states that 67% of the investors surveyed had plans to increase their infrastructure allocations.

26 May 08:45

Decline Free Food

by David Merkel

There is no getting something for nothing. There is always a cost involved, even if it is feeling vaguely obligated to listen to the person giving you a gift. We are social creatures, and we want to favor people who are kind to us.

I get a lot a pitches in the mail because I profile well to wealth managers and those like them. The age, assets, income add up to a likely client, except that I am in a related business, and am not interested in making my assets less flexible, at least right now.

My advice to you is that you do not respond to free gifts, whether it is good food, baubles, etc. It’s not worth it, and if you have a need, it would be far better to draw up your own story, and send it to five wealth managers, putting them in competition with one another, so that you can compare and contrast what they do and charge.

Even in my own limited experience, going to free conferences I find that I am the product being sold, and for months thereafter I have to tell marketers that I am not interested — and to the pesky ones point out some flaw in what they do.

Your time is valuable. So is your money. Thus remember what I always say:

“Don’t buy what someone else wants to sell you. Buy what you have researched that you want to buy.”

Thus, make them play your game. Don’t play their game. Send out your proposal for competitive bid, and choose the one that is best for you.

26 May 08:44

Simple Steps to Retirement Planning

by subra

Pattabhiraman Murari of www.freefincal.com has asked me to speak for 3 hours on retirement planning. It is difficult to speak for 3 hours on retirement planning, because it is a simple topic and does not take so much time. Please understand being simple means – simple to understand. Not saying it is easy to do.

Like my friend Shammi Gupta. She is a brilliant Yoga teacher. It is very easy and nice to watch her do. Doing it? OMG that is the problem!!

So Retirement Planning 101, let us say consists of the following things:

1. Knowing when you will retire.

2. Knowing how long you and your spouse will live.

3. Knowing how much you will spend in this period

4. Knowing how much your medical expenses will be.

5. Starting to save/ invest as soon as possible (understanding, and so tapping Compounding)

6. Investing as much as possible, as quickly as possible, and not interrupting the compounding.

7. Understanding asset classes – equity, debt, cash and real estate

8. Understanding asset class returns, standard deviation, mean, and reversion to the mean.

9. Understanding Asset Allocation.

10. Knowing that Cost really matters, and one way of mitigating costs is through higher saving.

That is all. And I am going to speak about just the following items…and nothing new.

You will hear about all this on Friday, 29th May, 2015 at Chennai. Nothing great.

I hope that you realise that 1-4 is a joke – nobody can estimate these 4..so what you have to do is from 5 to 10 !!

Start of with a prayer on your lips, a white board, Pattu’s calculators, and an adviser. Chances are in about 5 years you would have learnt why you do not need an adviser. If the adviser is good he would have delivered good results by now and you would do away with the doubt of whether you need an adviser….

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

26 May 02:16

India.Inc Employees Are Most Productive In The First Two Hours At Office

by Alnoor M Peermohamed

Productivity is one of the most important metrics when it comes to building a great business and it pays to know when best to rally the troops or retreat and live to fight another day.

According to a survey conducted by JobBuzz, the first two hours of work are the most productive period for most Indian employees. The period managers should expect the least amount of interest from their troops? The two hours after lunch.

Over 65% of the respondents said that they were most productive in the first two hours after reaching office, while the two hours post-lunch was seen as the least productive period by 70% of the respondents.

Hours Spent At Work

Of all the people surveyed, 63% worked between 8-10 hours while the rest reported they worked 6-8 hours. Regardless of the time spent at work, most respondents voted for the first two hours of work being the most productive.

Nearly 70% of those who work 8-10 hours a day and 64% of those who work between 6-8 hours a day voted for the first two hours of work to be the most productive. This clearly shows that spending more time at the office doesn’t really assure that more quality work gets done.

Experience

In terms of experience, the more an employee has of it, the more probable it is that the first two hours at work are their most productive. Over 80% of senior and experienced professionals said they were most productive in the first two hours.

Entry and mid-level employees too voted for the first two hours being their most productive, but they also felt the last two hours were quite productive.

Male v/s Female

Of the respondents that took part in the survey, 56% were comprised of male and 44% female. While 88% of the male respondents said the first two hours of work were the most productive, only 37% females shared the opinion.

A further 32% of the female respondents found that the two hours before lunch was the most productive period in their work day. This shows that more female than male employees are productive post lunch.

The Monday Culture

The survey found that 45% of the respondents said Monday was the most productive day of the week, while 19% voted for Wednesday. The least productive day of the week turned out to be Thursday.

The percentage of employees who felt Monday was the most productive went up to 50% in the case of startups. 40% of the respondents working for large corporations said Monday was the most productive day, while 30% voted for Wednesday.In terms of experience, 80% of employees with over 5 years experience voted for Monday being the most productive day. When it came to entry and mid-level employees however there was a 50-50 split between Monday and Wednesday being the most productive day.

In terms of experience, 80% of employees with over 5 years experience voted for Monday being the most productive day. When it came to entry and mid-level employees, however, there was a 50-50 split between Monday and Wednesday being the most productive day.

The post India.Inc Employees Are Most Productive In The First Two Hours At Office appeared first on NextBigWhat.

26 May 02:16

Countering the Inside View and Making Better Decisions

by Shane Parrish

“You can reduce the number of mistakes you make by thinking about problems more clearly.“

In his book Think Twice: Harnessing the Power of Counterintuition, Michael Mauboussin discusses how we can “fall victim to simplified mental routines that prevent us from coping with the complex realities inherent in important judgment calls.” One of those routines is the inside view, which we’re going to talk about in this article but first let’s get a bit of context.

No one wakes up thinking, “I am going to make bad decisions today.” Yet we all make them. What is particularly surprising is some of the biggest mistakes are made by people who are, by objective standards, very intelligent. Smart people make big, dumb, and consequential mistakes.

[…]

Mental flexibility, introspection, and the ability to properly calibrate evidence are at the core of rational thinking and are largely absent on IQ tests. Smart people make poor decisions because they have the same factory settings on their mental software as the rest of us, and that software isn’t designed to cope with many of today’s problems.

We don’t spend enough time thinking and learning from the process. Generally we’re pretty ambivalent about the process by which we make decisions.

… typical decision makers allocate only 25 percent of their time to thinking about the problem properly and learning from experience. Most spend their time gathering information, which feels like progress and appears diligent to superiors. But information without context is falsely empowering.

That reminds me of what Daniel Kahneman wrote in Thinking, Fast and Slow:

A remarkable aspect of your mental life is that you are rarely stumped … The normal state of your mind is that you have intuitive feelings and opinions about almost everything that comes your way. You like or dislike people long before you know much about them; you trust or distrust strangers without knowing why; you feel that an enterprise is bound to succeed without analyzing it.

So we’re not really gathering information as much as trying to satisfice our existing intuition. The very thing a good decision process should help root out.

***

Ego Induced Blindness

One prevalent error we make is that we tend to favour the inside view over the outside view.

An inside view considers a problem by focusing on the specific task and by using information that is close at hand, and makes predictions based on that narrow and unique set of inputs. These inputs may include anecdotal evidence and fallacious perceptions. This is the approach that most people use in building models of the future and is indeed common for all forms of planning.

[…]

The outside view asks if there are similar situations that can provide a statistical basis for making a decision. Rather than seeing a problem as unique, the outside view wants to know if others have faced comparable problems and, if so, what happened. The outside view is an unnatural way to think, precisely because it forces people to set aside all the cherished information they have gathered.

When the inside view is more positive than the outside view you effectively have a base rate argument. You’re saying (knowingly or, more likely, unknowingly) that this time is different. Our brains are all too happy to help us construct this argument.

Mauboussin argues that we embrace the inside view for a few primary reasons. First, we’re optimistic by nature. Second, is the “illusion of optimism” (we see our future as brighter than that of others). Finally, is the illusion of control (we think that chance events are subject to our control).

One interesting point is that while we’re bad at looking at the outside view when it comes to ourselves, we’re better at it when it comes to other people.

In fact, the planning fallacy embodies a broader principle. When people are forced to look at similar situations and see the frequency of success, they tend to predict more accurately. If you want to know how something is going to turn out for you, look at how it turned out for others in the same situation. Daniel Gilbert, a psychologist at Harvard University, ponders why people don’t rely more on the outside view, “Given the impressive power of this simple technique, we should expect people to go out of their way to use it. But they don’t.” The reason is most people think of themselves as different, and better, than those around them.

So it’s mostly ego. I’m better than the people tackling this problem before me. We see the differences between situations and use those as rationalizations as to why things are different this time.

Consider this:

We incorrectly think that differences are more valuable than similarities.

After all, anyone can see what’s the same but it takes true insight to see what’s different, right? We’re all so busy trying to find differences that we forget to pay attention to what is the same.

***

How to Incorporate the Outside View into your Decisions

In Think Twice, Mauboussin distills the work of Kahneman and Tversky into four steps and adds some commentary.

1. Select a Reference Class

Find a group of situations, or a reference class, that is broad enough to be statistically significant but narrow enough to be useful in analyzing the decision that you face. The task is generally as much art as science, and is certainly trickier for problems that few people have dealt with before. But for decisions that are common—even if they are not common for you— identifying a reference class is straightforward. Mind the details. Take the example of mergers and acquisitions. We know that the shareholders of acquiring companies lose money in most mergers and acquisitions. But a closer look at the data reveals that the market responds more favorably to cash deals and those done at small premiums than to deals financed with stock at large premiums. So companies can improve their chances of making money from an acquisition by knowing what deals tend to succeed.

2. Assess the distribution of outcomes.

Once you have a reference class, take a close look at the rate of success and failure. … Study the distribution and note the average outcome, the most common outcome, and extreme successes or failures.

[…]

Two other issues are worth mentioning. The statistical rate of success and failure must be reasonably stable over time for a reference class to be valid. If the properties of the system change, drawing inference from past data can be misleading. This is an important issue in personal finance, where advisers make asset allocation recommendations for their clients based on historical statistics. Because the statistical properties of markets shift over time, an investor can end up with the wrong mix of assets.

Also keep an eye out for systems where small perturbations can lead to large-scale change. Since cause and effect are difficult to pin down in these systems, drawing on past experiences is more difficult. Businesses driven by hit products, like movies or books, are good examples. Producers and publishers have a notoriously difficult time anticipating results, because success and failure is based largely on social influence, an inherently unpredictable phenomenon.

3. Make a prediction.

With the data from your reference class in hand, including an awareness of the distribution of outcomes, you are in a position to make a forecast. The idea is to estimate your chances of success and failure. For all the reasons that I’ve discussed, the chances are good that your prediction will be too optimistic.

Sometimes when you find the right reference class, you see the success rate is not very high. So to improve your chance of success, you have to do something different than everyone else.

4. Assess the reliability of your prediction and fine-tune.

How good we are at making decisions depends a great deal on what we are trying to predict. Weather forecasters, for instance, do a pretty good job of predicting what the temperature will be tomorrow. Book publishers, on the other hand, are poor at picking winners, with the exception of those books from a handful of best-selling authors. The worse the record of successful prediction is, the more you should adjust your prediction toward the mean (or other relevant statistical measure). When cause and effect is clear, you can have more confidence in your forecast.

***

The main lesson we can take from this is that we tend to focus on what’s different whereas the best decisions often focus on just the opposite: what’s the same. While this situation seems a little different, it’s almost always the same.

As Charlie Munger has said: “if you notice, the plots are very similar. The same plot comes back time after time.”

Particulars may vary but, unless those particulars are the variables that govern the outcome of the situation, the pattern remains. If we’re going to focus on what’s different rather than what’s the same, you’d best be sure the variables you’re clinging to matter.

--

Sponsored By: Greenhaven Road Capital: You think differently - now invest differently.

26 May 02:15

Why maintenance of roads is as important a target as developing new roads..

by Amol Agrawal

Came across this yet another article on NDA vs UPA comparison. The earlier ones were between UPA I and II vs NDA I and the recent ones are between NDA-II (in first year) vs UPA. The article is on road development target in the two regimes: Road transport minister Nitin Gadkari’s claim of highway construction falling […]

26 May 02:15

No Matter What Scrabble Says, Don’t Ever Use These 10 Words at Work

by Evil HR Lady

Scrabble just added 6,5000 new words to the official word list. For those of you who play, that can mean more opportunities to use that Q on a triple word square. Good news all around! But, does this mean that a word that is allowable in Scrabble should automatically make it into the office?

Of course not. Just because Scrabble says something is a word doesn’t mean using it in a business setting is an appropriate thing to do. Sure, if you’re discussing Inuits at the office, go ahead and throw out “quinzhee,” a newly approved word which means a snow shelter (which would undoubtedly be a game winner in an actual Scrabble game), but don’t be shocked if your coworkers look at you blankly. But, the following Scrabble approved words? Save them for the weekend competition.