This article is the eighth of this weekly series called Latticework of Mental Models, which will be authored by my friend and partner in writing the Value Investing Almanack, Anshul Khare. Anshul will write on various mental models – big ideas from various disciplines – which can help you think more rationally while analyzing businesses and making your stock investment decisions.

I was almost at the end of a beautiful evening drive. Refreshing cold breeze gently blowing on my face through the car windows coupled with minuscule traffic was like heaven on earth. Sporting an ear-to-ear smile I felt confident that nothing in the world had the power to take away my inner peace at that moment.

But, as usual, my faithful and ever reliable nemesis, the chaos-monkey, had different plans for me that evening.

Just when I was about to take a smooth turn on a closing traffic signal, a taxi cut me off while overtaking my car. The surprising rash maneuver from the taxi called for sudden brakes and by that time signal had turned red. As a result I missed my turn because of the insensitive driving by the taxi driver.

In the next few seconds, my Buddha smile turned into an angry frown and I was thrown out of my “appreciating the good things in life” mode.

Why did I feel so agitated? Well, for one, I was ahead of the taxi and it was me who was supposed to cross the signal first.

I felt as if the taxi guy had brutally robbed off my well deserved right to take the turn before him. You might find it amusing but the incident costed me a whopping two minutes of extra wait for the traffic signal to turn green again and of course my inner peace.

“Hey, cool down buddy! You’re exaggerating and using pretty strong words to describe a petty incident.” Probably this is what you would have said in an attempt to pacify me if you were with me that day.

But how could I take it easy? It was absolutely unfair! Why unfair?

Do unto others as you would have done unto you. Sounds familiar? Well I would never have done the same thing (it’s pretty close to encroachment in my dictionary) to anybody else.

Probably the taxi driver didn’t really think it was unfair. Perhaps he’d been at the receiving end of the same treatment many times in the past that he now considered it fair to pass the buck. Or may be he was just too busy marvelling at his own driving skills. Who knows what he was thinking!

Well, before you lose interest and stop reading, let me put an end to my rant about traffic manners and being a victim of unfair treatment. I hope you would’ve guessed by now that our mental model for today has got something to do with the above incident.

So let me ask you this. Have you ever experienced this feeling of being treated unfairly? May be in some small way like when one of your utterly undeserving colleague got promoted before you. Ouch, I’ve been there!

Kantian Fairness Tendency

Why is the human psyche so obsessed with the idea of fairness? Actually, it’s not just humans. Even monkey business (literally) isn’t immune to this tendency. Check out the video below (or click here), which proves that the tendency to seek fairness in all transactions is not an invention of modern man, but the behaviour has been tattooed at a much deeper level by evolutionary process.

The theory about rational human beings takes the view that people would accept any offer made to them as long as they were better off. But we know that humans are anything but rational and many

studies have shown that people will reject offers they view as unfair. Our ape just validated this hypothesis in the video.

This is the matter of discussion for today. Exploring the idea of what Charlie Munger calls Kantian Fairness Tendency. It’s one of the big ideas from Philosophy.

Let’s define fairness first. The basic idea is that we have devised certain rules that, when followed by everyone, result in a pretty smooth life for all involved. The key is that everyone needs to follow along. This unsaid understanding about ‘following along’ few ‘socially acceptable guidelines for conduct’ is what constructs the framework for fairness.

When a behaviour doesn’t fall (or doesn’t seem to fall) in this framework, we label it as unfair.

From Charlie’s talk, it’s not entirely clear why he has used the word Kantian but let me still take a stab at it. The word refers to the philosophical framework created by eighteenth century German philosopher Immanuel Kant.

Kant’s ethics are founded on his view of rationality as the ultimate good and his belief that all people are fundamentally rational beings. (Source: Wikipedia)

So somebody who uses Kant’s philosophy to construct an idea about fairness is probably suffering from Kantian Fairness tendency.

Now passing a judgement on ‘what is fair’ seems pretty simple when you are the subject matter i.e., when you are evaluating the fairness in matters involving you. What about the case when you have to take a decision about ‘what is fair’ for a third person?

Before I start pouring out my own ideas, I would like to mention that

Prof. Sanjay Bakshi has already compiled some of his thoughts on this topic in his blog post (which goes all the way back to year 2005). His discussion about ‘the law of higher good’ is another mental model that you need to be aware of. It kind of resolves the dilemma posed by Kantian Fairness Tendency.

Don’t miss his blog post since it covers a lot of ground for getting a better grip on the fallacy of Kantian Fairness Tendency. I have borrowed some of the quoted text from the same blog post.

Fairness and Envy

If you look at the monkey’s behaviour in the above video, it’s clear that the reward for performing a task is perfectly fair and acceptable to the monkey until the point he sees that his other monkey friend (I am just making an innocent guess about their friendship; they could have been professional rivals too) is getting a better reward for the same task. Of course, at this point, the first monkey goes berserk. He just can’t believe it. He is boiling with anger. A complete pandemonium follows in his cage.

My guess is that this extreme reaction against lack of fairness is because of envy, another mental model which we will discuss in detail some other time. However, Kantian Fairness Tendency limits the behaviour to accepting or rejecting the offered deal, whereas envy takes it to the next level (i.e., the emotional outburst) which could, and definitely would, get you into trouble.

You could say that a distorted worldview about fairness becomes the precursor to envious behaviour. That explains where the roots of envy lie.

Seeking Fairness

In the TV news when you see a guy robbing a lady, the obvious first thought is to seek punishment for the culprit. But soon the news reporter reveals that the thief’s mother was ill and he needed money for her treatment. Does this justify robber’s act as fair? May be yes. But then, is it fair to the society as a whole that anybody who needs money for a genuine cause is allowed to rob strangers?

As usual, Charlie Munger has some insights to deal with such situations. He has spoken about man’s overlove of fairness in his UCSB talk. He said –

It is not always recognized that, to function best, morality should sometimes appear unfair, like most worldly outcomes. The craving for perfect fairness causes a lot of terrible problems in system function. Some systems should be made deliberately unfair to individuals because they’ll be fairer on average for all of us. I frequently cite the example of having your career over, in the Navy, if your ship goes aground, even if it wasn’t your fault. I say the lack of justice for the one guy that wasn’t at fault is way more than made up by a greater justice for everybody when every captain of a ship always sweats blood to make sure the ship doesn’t go aground. Tolerating a little unfairness to some to get a greater fairness for all is a model I recommend to all of you. But again, I wouldn’t put it in your assigned college work if you want to be graded well, particularly in a modern law school wherein there is usually an over-love of fairness-seeking process.

Looking at the idea of fairness in isolation is akin to saying that a surgeon should refuse to operate on a patient because it will cause pain to him. Of course, an operation will cause pain (after the anesthesia wears out) and few days of inconvenience, but eventually it will prove to be a beneficial act for the patient.

So, may be, seeking fairness isn’t always wrong. What you have to know is – at what level are you seeking fairness? At an individual level, or at a group level, or at some other level altogether. Answering that question would bring some clarity as to what is fair and what isn’t.

I suggest you watch this lecture from Michael Sandel who is a professor in Harvard University. Some of the thought experiments that he discusses in his lecture are so unsettling that it seriously challenged my long held notions about morality and fairness.

The following story is from an

article I read in Wall Street Journal –

During the middle ages in Europe when the court couldn’t determine if a defendant was guilty they would offer him an option. The option was to either accept the punishment for their crime or put their hand in boiling water. The idea was that God, who knew the truth, would miraculously save any suspect who had been wrongly accused.

The trick however was that a guilty person and an innocent one often respond differently to the same incentive. Typically a guilty would choose to accept the punishment instead of sacrificing his hand. An innocent who believed in God would daringly agree for boiling water test.

In the ideal scenario, nobody really goes through the boiling water test, because the defendants are proven guilty/innocent based on their intentions only.

But if nobody was ever made to go through the boiling water test in front of the crowd, the trick will lose its effectiveness. People need to at least see some defendants suffering the boiling water torture to believe in the authenticity of the test. Which means some innocent people will have to go through the torture and it would be unfair to them. In order to keep the sanity and order in society few innocents will end up being victim of unfair play.

In other words, to make an omelette you need to break some eggs.

Fairness in Investing

One of the ways this bias comes into play in investing is when people expect that they should make the money in the same way they lost it, i.e., they focus on individual stocks to make money for them.

Of course, that’s what the idea is when you choose the stock to begin with. But expecting fairness in returns from the stock is a fallacy. Instead, you should make sure that you don’t lose money overall on your portfolio of stocks. No matter how much margin of safety and rigorous analysis you employ, you are bound to find (time to time) that you have a loser in your portfolio.

A natural reaction is to say, “It’s not fair. I have put in so much effort, analysis and money in this stock. It shouldn’t lose money.”

Being aware of Kantian Fairness Tendency can save you some unwanted heartache.

Now consider, for instance, a company that has historically paid good dividends to shareholders. As time goes on, if the company continues to grow and perform well, shareholders may rightly expect that their dividend should grow, too. But what if it doesn’t? What if something changes, maybe a slowdown in growth, or pressure on cash flows? And what if the company decides to cut back on dividends to preserve cash for future expansion?

Consider the example of Hawkins Cookers, which recently cut its dividend from Rs 60 per share in FY14 to Rs 45 in FY15 due to slowdown in growth and pressure on cash flows.

“It’s unfair!” lot of investors in the stock seem to be saying. “Did we pay 60x for this?”

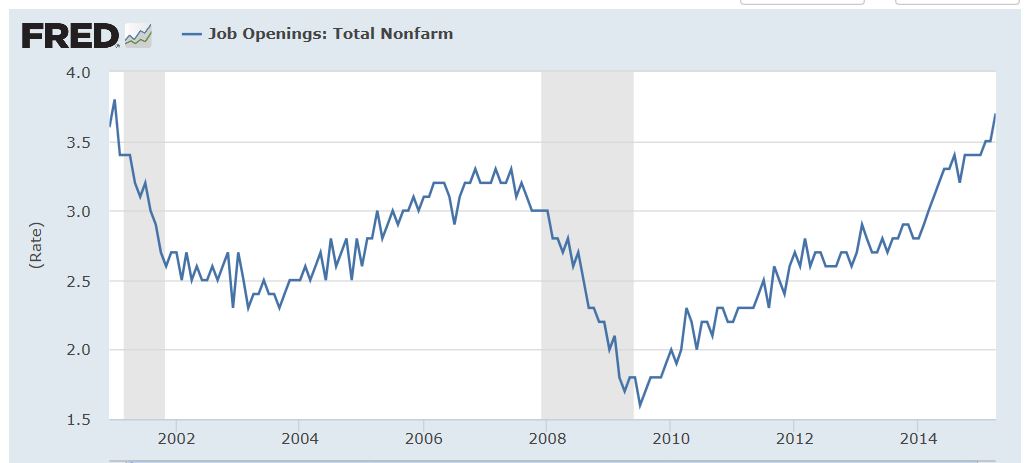

And, when a lot of investors start singing the unfair song, this is what happens to the stock –

On the surface, this may seem fair on the part of the management, who wants to protect precious cash that would help them tide over the immediate slowdown in business. And given the management of Hawkins, it surely seems to be thinking long term. But to most people who bought the stock with unfair expectations, it’s the management and the business that now looks unfair to them!

Conclusion

Life isn’t fair, but many can’t accept this. Tolerating a little unfairness should be okay if it means a greater fairness for all. However the question ‘what is truly fair for all’ isn’t an easy one to answer.

Before I end this discussion let me put up a caveat emptor. Some of my thoughts in this article have been a result of my speculation about the utility of Kantian Fairness Tendency.

There is a non-zero possibility that my arguments and conclusions are flawed, so instead of taking them at face value, please consider them as starting points to stimulate your own independent thought process.

Goes without saying that I would be more than happy to entertain any challenging arguments from your side too. So don’t hesitate! Just shoot your thoughts in the Comments section of this post.

Everybody should believe in something. I believe in having fun and I am having loads of it by sharing these ideas with you.

Don’t break this chain of acquiring worldly wisdom. Pass it on. You will be surprised with the kind of insights that pop up in your head while you’re explaining new ideas to other people.

Although I have tried my best to compile some useful knowledge in this article, but it might so happen that the real intellectual action takes place in the Comments section. So please don’t forget to share your insights there.

Take care and keep learning.