I’ve been publicly tracking my income and expenses since I initiated this blog back in early 2011. I do this for a few reasons.

I’ve been publicly tracking my income and expenses since I initiated this blog back in early 2011. I do this for a few reasons.

First, I want to prove to the world that it’s possible to become financially independent at a relatively young age even if you don’t make a lot of money. I don’t make a six-figure income. I never have and I probably never will. But it’s not necessary. Oftentimes, people focus on income too much. Expenses are just as important, because if you make $200,000 per year, but spend $190,000 of it, you’ll never become financially independent. Conversely, bringing home $40,000, and learning to get by on half of it means you’ll likely be able to retire if you want to within 15 years or so. Making less means you have less potential income to save, but spending less means you need less passive income with which to retire off of.

The second reason I do this is because I want this to be a live look at one man’s journey. You can find countless books by financially successful people, but often it’s long after they’ve completed their trek to significant wealth that they’re then telling you how they did it. It’s easy to postulate. It’s much more difficult to actually show the whole process in action, for better or worse.

And finally, knowing that every dollar I spend is going to be published for the world to see serves as reinforcement to stay frugal. There’s been more than one occasion where I decided against a particular expense after realizing I might be a bit embarrassed to write about it.

So each month I will post my income and expenses for the previous month. I track every dollar in and out, so what you see is exactly what I earned and spent (rounded to the nearest dollar).

By the way, I use Mint and Personal Capital to track all of my income and expenses. Both are awesome (and free) services.

|

|

| Income From June 2015: |

|

|

|

| Online Income |

$6,245 |

| Dividend Income |

$845 |

| Other Income |

$657 |

|

|

| Total Income |

$7,745 |

|

|

| Expenses From June 2015: |

|

|

|

| Rent & Utilities |

$540 |

| Groceries |

$233 |

| Student Loans |

$224 |

| Health Insurance |

$193 |

| Hosting |

$158 |

| Fast Food/Takeout/Coffee |

$157 |

| Restaurants |

$84 |

| Pharmacy |

$70 |

| Cable/Internet |

$27 |

| Mobile Phone |

$25 |

| Amusement |

$22 |

| Gifts |

$13 |

| Transportation |

$12 |

| Everything Else* |

$165 |

|

|

| Total Expenses |

$1,915 |

Income

Well, June was absolutely incredible for income. I set a record for online income in May. And what happened in June? I blew that record away. I can’t believe it.

Much of the overall online income was actually pretty similar when looking at May’s and June’s reports. I stayed really busy in regards to writing – pumping out a massive amount of content – both here at Dividend Mantra and with freelance opportunities. Traffic was once more strong here at the site, coming in at approximately 375,000 pageviews for the month. And I continue to do my best in regards to maximizing content quality.

I’ve discussed before how I generate income online, and much is the same as it was a year ago. The main differences between then and now are simply that I write a lot more (due to having more time) and the blog continues to grow. So that has combined to increase the income rather dramatically YOY. And, of course, you readers help me tremendously whenever you sign up for products and/or services that are recommended. As always, I only recommend what I personally use and/or find value in, which is why I have so few affiliate partnerships. Thank you all for your continued support!

The one major difference between May’s online income and June’s online income (and what accounted for the increase this month) was the fact that I received my first royalty payment for my book!

This royalty amounted to approximately $1,200 for sales generated in April. April is, so far, my best month in terms of sales and the amount of income generated from the book. It drops off a bit for May’s sales and then rather dramatically thereafter. As I’ve noted before, the book will likely not amount to life-changing income for me, but I’m very proud of the project because I think that the book can lead to life-changing results for those that take the time to read it. Might not radically change my life, but I think it can (and will) change others’ lives. I hope to put something together this month discussing my experience with writing a book and what I learned from the project. I owe a big thanks to anyone and everyone that picked up a copy and/or spread the word. Means a lot to me.

Dividend income was, of course, wonderful for June. The last month of every quarter tends to be a real blockbuster for me and June was no different. Landing in at almost $850, that was one of my best months ever. That’s a ton of passive income for someone who doesn’t spend a lot of money. I’m truly fortunate that the me of 2010 decided to embark on this journey. It’s been a lot of fun. And I feel the best is yet ahead.

Other income was mostly related to the sale of my car. I’m going to spread the profit out over the course of the year so as to smooth any month-to-month variances out. So this will provide a nice boost to my monthly savings rates for the rest of the year, just like it was a drag on my monthly budgets last year. In addition to that, I also collected $57 in cash rewards from one of my credit cards.

Expenses

*The everything else category includes expenses I don’t have a regular budget for. So Claudia decided it was time for another dog. We’ve just had Diego, our little Chihuahua who knows a lot about happiness, for a few years now. But we just recently added Kiwi to the mix, another young Chihuahua who was a freebie off of craigslist. Great puppy. She’s incredibly sweet. But we also had to get her checked out by the vet. Turns out it was time for Diego’s annual visit anyhow, so that worked out perfectly. I pitched in half for the vet bill, which accounts for most of the money spent this month in this category. We also needed a new frying pan after literally wearing the nonstick coating off – that coating doesn’t exactly taste good in our food.

Speaking of food, I spent a lot there. I’ve come a long way from the days of eating ramen noodles day in and out. We ate well this past month. Perhaps a little too well, looking back on the numbers. But I’m not regretful.

Although it might look like I swing through the drive-thru at local fast food joints, the truth of the matter is I don’t. First, I don’t have a car, so that’s impossible. Second, I actually don’t eat much of it. But I categorize any food that isn’t at a sit-down restaurant as “fast” food. In addition, I’m writing more and more outside the house, patronizing a couple coffee shops within walking distance of the apartment. I spent something like $80 on these trips over the course of the last month. The me of a couple years ago would have scoffed at the notion. But I’m so much more productive (not to mention happy) when I write away from home that the additional income more than makes up for the expense. So it’s an investment of sorts.

Other than food, I think everything else is in line here. I really don’t spend that much on core expenses. $25 for the cell phone. Less than $15 on transportation. Less than $550 on shelter. I’m very pleased and content with the amount of money I’m spending, overall. Especially considering that I believe I’m living a rather high quality of life. Once you realize that material goods have little impact on long-term joy, it makes it easy to reallocate resources toward the things that do bring about lasting happiness; I’ve certainly found more happiness working from home than anything any store sells.

Savings

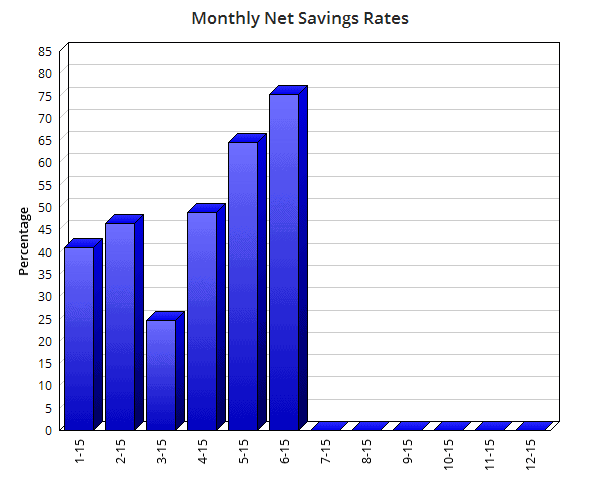

I managed to save 75.3% of my net income this month. I’m ecstatic! It’s been a long road back to the high savings rates I used to achieve with ease, but controlling expenses while simultaneously working hard to opportunistically increase income has turned out incredibly well. This is my highest monthly net savings rate since January 2013, so I feel like I’m getting back to the old me. I’m still very excited and very aggressive when it comes to saving money, investing, and fighting for financial independence. Haven’t lost my hunger at all.

One of my goals this year is to save 50% of my net income throughout 2015, averaged monthly. So far, I’ve hit rates of:

I’m now at an average of 50.1% for the year. Boom! Back above water. Took an insane June to get there, but I’ll take whatever I can get. Now that I’m back at the baseline I look to maintain, it’ll be slightly easier to keep at that level for the rest of the year. No more playing catch-up, which feels great.

I expect to have a fairly strong summer and fall for savings, save for the potential of some dental expenses. That should provide for a really nice margin of safety heading into the holiday season later this year. I think, from what I can see, the odds are very high that I’ll exceed my savings goal this year. Stay tuned to find out!

Did you save as much as you wanted in June? Hit your savings goals? On track for your goals this year?

Thanks for reading.

Photo Credit: bplanet/FreeDigitalPhotos.net

Note: Affiliate link included.

I’ve been trying a lot of things these days to connect my 10-year old daughter Kavya with a variety of new learnings – in life, human behaviour, how the mind works, ethics, and how to develop good lifelong habits.

I’ve been trying a lot of things these days to connect my 10-year old daughter Kavya with a variety of new learnings – in life, human behaviour, how the mind works, ethics, and how to develop good lifelong habits.