Chaitanya Patel

Shared posts

How to talk to girls..?

India's courts need more "sunlight"

When to Deploy Capital

Photo Credit: edkohler || Buy Now and smile!

One of my clients asked me what I think is a hard question: When should I deploy capital? I’ll try to answer that here.

There are three main things to consider in using cash to buy or sell assets:

- What is your time horizon? When will you likely need the money for spending purposes?

- How promising is the asset in question? What do you think it might return vs alternatives, including holding cash?

- How safe is the asset in question? Will it survive to the end of your time horizon under almost all circumstances and at least preserve value while you wait?

Other questions like “Should I dollar cost average, or invest the lump?” are lesser questions, because what will make the most difference in ultimate returns comes from the above three questions. Putting it another way, the results of dollar cost averaging depend on returns after you put in the last dollar of the lump, as does investing the lump sum all at once.

Thinking about price momentum and mean-reversion are also lesser matters, because if your time horizon is a long one, the initial results will have a modest effect on the ultimate results.

Now, if you care about price momentum, you may as well ignore the rest of the piece, and start trading in and out with the waves of the market, assuming you can do it. If you care about mean reversion, you can wait in cash until we get “the mother of all selloffs” and then invest. That has its problems as well: what’s a big enough selloff? There are a lot of bears waiting for rock bottom valuations, but the promised bargain valuations don’t materialize because others invest at higher prices than you would, and the prices never get as low as you would like. Ask John Hussman.

Investing has to be done on a “good enough” basis. The optimal return in hindsight is never achieved. Thus, at least for value investors like me, we focus on what we can figure out:

- How long can I set aside this capital?

- Is this a promising investment at a relatively attractive price?

- Do I have a margin of safety buying this?

Those are the same questions as the first three, just phrased differently.

Now, I’m not saying that there is never a time to sit on cash, but decisions like that are typically limited to times where valuations are utterly nuts, like 1964-5, 1968, 1972, 1999-2000 — basically parts of the go-go years and the dot-com bubble. Those situations don’t last more than a decade, and are typically much shorter.

Beyond that, if you have the capital to spare, and the opportunity is safe and cheap, then deploy the capital. You’ll never get it perfect. The price may fall after you buy. Those are the breaks. If that really bothers you, then maybe do half of what you would ultimately do, but set a time limit for investment of the other half. Remember, the opposite can happen, and the price could run away from you.

A better idea might show up later. If there is enough liquidity, trade into the new idea.

Since perfection is not achievable, if you have something good enough, I recommend that you execute and deploy the capital. Over the long haul, given relative peace, the advantage belongs to the one who is invested.

If you still wonder about this question you can read the following two articles:

In the end, there is no perfect answer, so if the situation is good enough, give it your best shot.

Equity Risk Premium

It’s real

As you are aware, in April of every year, we provide comparison charts of various asset classes since 1979-80, the year in which Sensex was formed with a base as 100.

Just to refresh your memory I want to share here the annualised return of Fixed Deposits (FD), Gold and Sensex for last 36 years:

FD: 8.41%

Gold: 10.25%

Sensex: 16.93%

This shows equity has given 2 times the FD returns and 1.65 times the gold returns.

This number doesn’t convey the reality.

As I’ve repeatedly told you, what matters is real returns; the returns after inflation.

Inflation during the above period was 7.73%

So the real returns look like this:

FD: 0.68%

Gold: 2.52%

Sensex:9.2%

This shows equity has given a real return of 14 times the FD and 4 times the gold.

So when it comes to real return; which is how our wealth actually multiplies, FD and gold stands no chance in front of equity.

We’ve only accounted for inflation. What about taxation? FDs are taxed at the tax slab you belong to and gold at 20% of the indexed cost. But long term capital gain of equity is completely free.

So if we adjust for taxation also, FDs would not provide any real return and gold would provide significantly lesser than 2.52%. Whereas Sensex would still provide 9.2%.

You may be wondering about real estate. There is no reliable long term data for real estate. Real estate would normally provide around 3% above inflation. So what is true for gold above would more or less hold good for real estate as well.

Also one more thing. Sensex had a dividend yield of close to 2% over 36 years. That is not included in the above calculation. Equity is already a huge winner in terms of real returns and adding dividend yield would only make it returns further extra ordinary.

Go for the real wealth creator. Go for equity.

What A Shame!~LIC bails out Government with US $ 1.2 b in IOC Disinvestment

Equity Portfolios need maintenance

Corrections are normal

I’ve mentioned many times how corrections are absolutely normal in stock markets.

Given the scenario right now, I thought we may revisit this topic.

Be prepared for a drop of:

10% – very frequently

20% – periodically

30% – once in a while

50% – few times in your investing life

There have been instances of radical fall in a very short time as well. On October 19, 1987 (popularly known as ‘Black Monday’), the Dow fell by 22.61%. Nearly one fourth of market capitalisation got wiped out in a single day. This is the highest every one day stock market fall (in percentage terms) in U.S so far. Though many reasons are given including program trading, nobody saw it coming and no one knows why it happened.

The whole U.S. market got paralysed and dooms day prophets mushroomed. Everyone predicted a great catastrophe. The funny part is market recovered and closed marginally higher in December than what it opened in January. So 1987 was actually a positive year for Dow. In the long term graph, this one day fall of 22.61% looks like a minor blip.

Warren Buffett has mentioned that during last 50 years of Berkshire Hathaway, there has been a fall in share price by 50%; 4 times during the above 5 decades.

As I mentioned yesterday, temporary declines are not permanent losses unless we sell due to panic.

But for volatility, everyone would be an equity investor. Who wouldn’t want a smooth 18% annual return?

To earn the 18% kind of annualised return Sensex has provided in last 4 decades or 22.74% kind of annualised return CRISIL AMFI Equity fund index provided during last 2 decades; one has to willingly embrace volatility. If we want long term returns of equity, we’ve to accept the side effect of volatility.

We always need to remember that equity is best asset class in the long run, which provides real return significantly above inflation, increase our purchasing power and build our wealth.

SIP is a superb tool which makes us buy during down times, which otherwise we may hesitate to do.

As I mentioned in a tweet:

“Why SIP is powerful?

Removes emotion out of investing

No timing the market

Buy at lows which we otherwise won’t do

Time diversification”

So all you’ve to do is to continue your SIPs without worrying about what happens to markets in near term.

Don’t keep looking at your portfolio. This is a good habit to follow always; more so in down times.

Some of you wanted to invest your emergency fund in equity now. Please don’t do that. As the name suggest, it is for any unexpected emergency. Keep it as it is. Only long term money, what you don’t need for at least next 10 years, should be invested in equity.

It is sufficient if you stick to your SIPs and stay the course.

Making sense of crashing markets

All of which is true. But what's new in that? Why should markets crash instead of declining in an orderly way? How does that explain the panic? One possible explanation is that the slowdown in China will be more severe than thought- growth won't be even 7 per, it would be, say, 6 per cent. But, again, why would markets latch on to this virtually overnight?

The other suspect is the impending Fed rate hike. But this has been long in coming. Also, it's not as if the Fed will press ahead regardless of what's happening to markets worldwide. An article in Business Insider highlights these points very well but does not come up with a plausible alternative. So let me stick my neck out and offer one.

Might worsening geo-politics be a factor? There's been news in recent days that both Russia and Nato have carried out exercises that military analysts see as a clear preparation for war. Then, there's been news that the US is moving some of its most advanced aircraft to its European allies. Oil prices have fallen to close to $40 and there's been another run on the rouble. This adds to Russia's economic woes and puts Russian president Putin under further pressure.

It could well be that the flight of funds from emerging markets is a sign of a full-blown global crisis that is not just economic in nature. I read in the Economist recently that Russia will find it difficult to hold on to Chechnya and other states in the federation the moment it runs out of cash. Any impending turbulence in Russia, with all the uncertainties it carries, would certainly frighten the life out of investors.

Worsening ties between the west and Russia are part of worsening geo-politics in general: think the situation in West Asia, China- Japan, India- Pakistan, etc. Don't get me wrong. I don't see any of these crises playing out in the near future. But worsening geo-politics makes it difficult to get the necessary focus on the economic situation. Indeed, crashing asset prices, notable that of oil, which is crucial to Russia, may just suit the agenda of the western powers.

My sense is that the US and its allies under-estimate Russia, as it has been under-estimated by others in the past. When this becomes clear enough, the geo-political situation should improve and panic should dissipate. However, this learning could be a long and painful process. Until then, however, risk aversion will be high. It's the combination of a weak economy and worsening geopolitics that, perhaps, explain the current panic.

(Updated on August 27, 2105)

Herd Mentality – If 10 Cr people say something Foolish, it is still Foolish

You see a stock zooming upwards and reaching new highs every day. You see your friends buying and calculating their notional profit every day. There is “positive” news on the stock always. You too go ahead and buy it and as everything that goes up must come down, the stock value plunges and you lose your hard earned money. Is this not a familiar story? What you did is, followed the herd and invested at a higher price without having the right reasons for investing.

What is Herd Mentality?

Herd Mentality is defined as individuals doing the same thing as others in the group so that they conform to the norm and their desires for acceptance and belonging to same group are met. They also feel they will be safe if they do the same thing as the group. Sometimes individuals subconsciously follow the group. They may think that their decisions are based on their own judgement and independent thinking. But that may not be always the case and they are just following the herd and accepting the group decision without thinking through it or because they are less experienced in taking such decisions.

Is it only limited to equities?

Not at all – sitting in financial market it’s easy for us to find & share those examples. But what about insurance as investment or Real Estate Price/Bubble (still people are not ready to accept that property prices can correct/crash including builders) or Recent Gold Rush or money making scheme like Speak Asia. Herd Mentality is not only limited to investments – it can also exist in fashion or brands. THINK

It is really tough to stand against Herd Instinct – I have always faced the brunt whenever I have wrote something against social proof. Kind of comments people write can tear your confidence & emotions.

How all that started?

Herd Mentality might be good in some cases. Think of nomads – staying together in a big herd in the jungles to stay protected from predators. You will be surprised but science has proved that our behaviour issues are because of how our civilisation has developed over 1000s of years.

But if you don’t do your research and follow the equity market just because everyone is doing the same is a risky proposition.

Height of Herd Mentality

Retail investors have faced the brunt of herd mentality many times. For example, in late 1990s and early 2000s, a lot of people started investing in “dot com” companies without really understanding the business model. People invested when they saw others investing and wanted to jump on the bandwagon. But the bubble burst, many people lost a lot of money when the businesses could not sustain themselves. There have been many cases like this across the world. And one of the major reason for every bubble is Herd Mentality.

Biggest issue with Herd Mentality

If you are following the herd in investing, it means that you are probably already late and you are buying it when it is expensive. Many times experts and analysts and well meaning friends say, “Gold is a good investment” or “’XYZ’ stock is a good buy” or “Real estate prices will rise”. Each time, if you react by selling what you have invested in and buying a new asset, your transaction costs & tax increase and you might sell off assets which may outperform. This means you do not get optimum returns.

It also happens the other way around. For example, markets are in a downward trend after the China incident. This does not mean, we should sell off all our stocks because many stocks are at much lower levels. Mutual Funds or quality stocks that you have purchased at the right price after thorough research should not be sold off even when prices are falling. Once markets consolidate, they may perform better. Assets should be bought and sold as per a planned investment strategy and not based on emotions.

WHY – Herd Mentality

Herd mentality also comes into play because as humans, we fear missing out on the opportunity, fear of being ignorant and greed. We always want the best and the most with least effort and as quickly as possible. But herd mentality mostly does not help us to achieve our financial goals.

How to save yourself from yourself

Though it is easy to follow the herd, you are better off following a sound financial and investment plan –

- You should do your research on the various investment options available.

- You should have an asset allocation model in place based on your risk profile.

- You should focus on your financial goals, long-term investment strategy and personal finance status and take investment decisions accordingly.

- You should be ready to face some ups and downs in the market. It is impossible to time the market correctly and buy at the lowest prices and sell at the highest prices. You should not get emotionally attached to the profits and losses made.

- You should take the help of a financial planner if you are not confident of making investment decisions. But you should be involved in financial planning and track and review actions taken by the financial planner.

You might still face losses or miss some opportunities but you should focus on your long term financial plan. But no one can get the best of the market each and every time. You should make investment decisions to achieve the short-term and long-term financial goals that you have set. If you see yourself being tempted by what is happening in the market and wanting to buy/sell, you should keep your emotions in check. You should force yourself to take a few days to review your buy/sell decision. Once you are more rational, you should consider how this step aligns with your long-term financial plan and then take a decision.

You should remember that aiming for financial stability and growth is more important than following the herd.

Do you think, you have made investment decisions following the herd? What was the impact of that decision on your investment portfolio and strategy?

Losing $6 billion, now worth $63 billion

Nick Murray has written a wonderful book ‘Simple Wealth, Inevitable Wealth’. I would rate this as one of the very few books both investors and advisors must read. I read this much late in life. I would have been a better advisor had I read this book earlier.

Joshua Brown in this excellent piece cites a passage from the above book and also shares some thoughts on the same.

Please remember that there was Russian Ruble crisis in 1998 (also don’t forget; there is always some crisis or other in the world) when the below incident took place.

“$6,200,000,000

Yes, that’s right, it’s six billion two hundred million dollars.

A very large sum of money, wouldn’t you say? Now what, you ask, does it represent?

It is roughly how much Warren Buffett’s personal shareholdings in his Berkshire Hathaway, Inc. declined in value between July 17 and August 31, 1998. And now for the six billion dollar question. During those forty-five days, how much money did Warren Buffett lose in the stock market?

The answer is, of course, that he didn’t lose anything. Why? That’s simple: he didn’t sell.

Berkshire Hathaway’s “A” shares had dropped in price from roughly $80,000 per share in June to $59,000 by the end of September. These same exact shares just hit a high of $229,000 this year. Buffett knew that while the price may have been changing for his company’s shares, the value that his companies were creating would not be permanently impaired. This allowed him to wait out the ’98 episode rather than reacting to it.”

I’m extremely happy that none of you got perturbed and called me yesterday. I’m glad that we are evolving together. Though it is expensive, I would suggest buying and reading Nick Murray’s ‘Simple Wealth, Inevitable Wealth’.

Only selling in panic, which most investors do, convert the temporary declines into permanent losses.

In the long run, index and good diversified equity funds would only keep going up.

I don’t know how the short term would pan out. But in the long run, a growing economy like India is a great place for investors.

Never lose faith. In the moments of doubt, please call me. We are always there to handhold you.

Flash mob performance of Beethoven’s “Ode to Joy”

One of my favorites, Beethoven’s 9th symphony is his final complete symphony. Composed between 1822 and 1824, it is considered to be his finest and some even think that it is the greatest composition in the Western classical music canon. In the final movement of the choral symphony, the chorus sings the words to Friedrich Schiller’s poem “An die Freude” (composed 1785). Beethoven conducted the symphony when it premiered. He was totally deaf by that time and so he had to see the ovation that followed, rather than hear it.

Here’s an enjoyable flash mob performance of the “Ode to Joy” in Sabadell, Spain, on 19th May, 2012. I love the way it begins. A very young girl steps up to put some money in the hat lying in front of a man with a double bass. Evidently the Bank of Sabadell sponsored the event. Certainly it is a corporate — and therefore professionally produced and recorded — event. But the responses of the public is spontaneous and genuine. Note the obvious fun the kids are having (see around 4:30 time stamp.) I get goosebumps in the final minute of the performance. The energy of the piece is palpable.

Now put on your headphones, crank up the volume and enjoy!

Addendum: Another flashmob version of the same. This one is in Nürnberg in 2014. It is a more tight performance. Naturally, Germans!

The average investor

This time is no different - EM shocks spares none

Discussing the not-so-glamorous under-belly of India’s e-commerce system

Market fell 1624 what people say or (will) say…

Prices Have Changed; Not Much Else Has Changed

Photo Credit: Moyan Brenn || My, now doesn’t that look peaceful…

There is the temptation when market prices move fast after they have been at recent highs to assume that things are going to fall apart. Well, guess what? That could happen.

I don’t think it is likely though, if falling apart means a scenario like 2008-9, 2000-2 or 1973-4. In order to have a significant drawdown in the market, you have to have a lot of leverage collapse, whether that is financial or operating leverage.

Financial leverage is bad debt. We have areas of that — student loans, agricultural loans, a modest amount of subprime lending for autos, and a decent amount of lending to junk-rated corporations, but not enough to create a self-reinforcing situation where bad debts can’t be borne by lenders, and lenders then collapse.

Operating leverage is bad assets — building up too much productive capacity such that there will not be enough demand to absorb it for the foreseeable future. Or, building capacity that isn’t productive… either way, assets will have to be written down.

There have been a number of parties kvetching about a lack of investment from US corporations, but let’s take this a different direction. There hasn’t been a lot of bad investment from US corporations… and part of that may be due to dividend and buyback policies. Yes, there are some IPOs that have come out that look marginal. I’ve looked at a variety of spin-offs where the underlying business is attractive, but they loaded the spin-off with a sizable slug of debt in order to pay a final dividend to the parent company saying farewell. But on the whole, I don’t see a lot of money being wasted by corporations on investments. That is another reason why profit margins are high.

Now, a lot of the furor in the markets stems from China, and the effects that slowing growth and/or bad debts in China will have on the US economy. Personally, I don’t think this is an issue to worry about, unless you have a lot of investments in China and other emerging markets. In general, US markets don’t get deeply hurt by slowdowns or even crises in other countries. Even if it means a slowdown in revenue growth for large US corporations, it would also likely mean that US interest rates might fall, which would often make equities fall less as bonds rally.

Also, for foreign affairs to affect the US in a big way, the US would have to have a lot of lending exposure to those nations that are struggling. (Think of the LDC nations in the early ’80s.) Maybe this is one of the benefits of running current account deficits — we don’t have money to lend to foreign countries from our net export earnings.

Think of all the significant foreign crises of the last 30 years. LDC crisis, Plaza Accords leading to Japan’s lost decades, Mexico, Asian Crisis, European Union difficulties with their fringe nations, Iceland, Greece, Greece, Greece, China, etc. There was always temporary indigestion in US markets, but when did it ever weigh on the US markets for a long period? Really, it never did. So why are we concerned over China?

Regarding the Fed, I abstract from this old post, which quoted a 2005 piece on Fed policy at RealMoney.com, and what blew up at the end of each tightening cycle. I list blow-ups up to that point, and mention that I think US Housing is next:

So it moves in baby steps, wondering if the next straw will break some camel’s back where lending has been going on terms that were too favorable. The odds of this 1/4% move creating such a nonlinear change is small, but not zero. But on the bright side, the odds of a 50 basis point tightening at any point in the next year are even smaller. The markets can’t afford it.

Or, these two posts, which you can look at if you want… one suggested that housing was the next bubble (in 2004), and the other critiqued Bernanke’s reasoning on monetary policy. (Aaron Task has an interesting rejoinder to the latter of these.) — [DM: these links are dead now.] |

Some worry now about future Fed policy — what will blow up when the Fed tightens too much? I would encourage everyone to relax. First, we don’t know that the Fed will do anything soon. Second, we don’t know if they will do anything much. Third, we don’t even know if the Fed has a coherent theory of monetary policy anymore. Face it: Yellen has never tightened rates once. Bernanke never tightened rates aside from finishing out Greenspan’s plan to invert the yield curve at the beginning of his Chairmanship. Almost no one on the FOMC has any significant practical experience with tightening rates. What will guide them out of their zero interest rate policy? What will be enough?

Even so, tightening cycles usually end with something blowing up. Maybe this time it is the emerging markets. I don’t see a large concentration of US-based bad debt that the Fed might inadvertently blow up, at least not yet. (Maybe the day will come when the US Treasury might complain about rising financing rates. After all, debt is high, but affordable while rates are low.)

Valuation is the main issue as I see it at present, as I commented in my recent piece “Stocks or Bonds?” When stocks are priced at a level that discounts 4.5%/year returns over the next 10 years, you don’t have a lot of margin for error, especially when you can create a safer bond portfolio that yields the same.

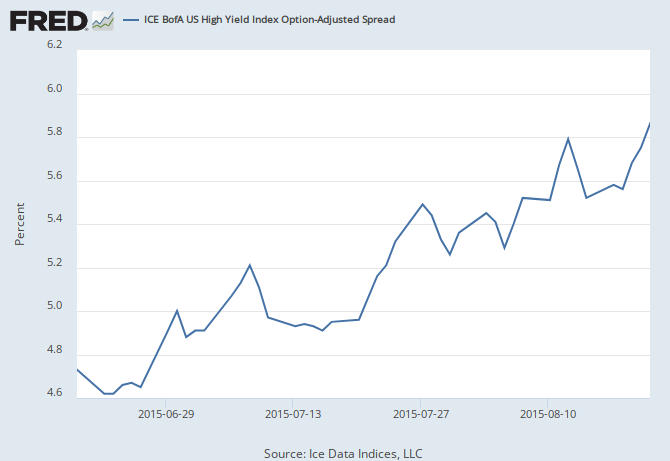

Now, since I wrote that piece, the S&P 500 is down around 10.5%. The bond portfolio is down around 4.5% (it was a risky portfolio, and some of the emerging markets bonds hurt), while the Barclays’ Aggregate is up 1%. High-yield bond spreads have widened over that time by ~1.2%.

The anticipated return on the S&P 500 has maybe risen by 1%/year over the next 10 years, to 5.5%. That said, so has the yield on the risky bond portfolio. I see the selloff as being in-line with the yields of risky debt, which at some higher level of spread, will attract buyers, given that there have been no significant defaults recently.

The US stock market could go down another 20% from here, but I think it will be less. My main point is that we shouldn’t get a big washout, but just a correction of valuation levels that got too high relative to other risky assets, like junk bonds.

So don’t panic. You could still move some assets from stocks to bonds if you want to sleep better, but don’t do anything severe.

The Markets Fall Big, But It Really Is Not Useful to Panic

The markets are 6% down. And in the carnage we saw it move from a bad open, to a worse mid-day, to an absolutely terrible afternoon.

The Nifty sank to nearly the lowest in a year (we went briefly below this level in Oct 2014).

This is not Normal of course. And markets haven’t tanked this much since…January 2009!

My Few Paise (Tweets)

1/ This has not been an easy day. It seems to be that investors have panicked. We’ll know who and when and how later.

— Deepak Shenoy (@deepakshenoy) August 24, 2015

2/ There would have been margin calls, panic selling, lower circuits and what not. This would have fed into even more selling.

— Deepak Shenoy (@deepakshenoy) August 24, 2015

3/ There wasn’t a letting up, right to the end. Which means it’s unlikely to be “speculators” that drove the markets down.

— Deepak Shenoy (@deepakshenoy) August 24, 2015

4/ There will be no end to reasons but it’s just this – just because markets have been calm recently, doesn’t mean they stay calm.

Market fell 1624 points what to do!!!

EPIC pictures of the Earth

This is a picture of our earth taken by NASA’s DSCOVR – Deep Space Climate Observatory – spacecraft which is parked in the L1 Lagrange point to observe the sun and the earth.

This is a picture of our earth taken by NASA’s DSCOVR – Deep Space Climate Observatory – spacecraft which is parked in the L1 Lagrange point to observe the sun and the earth.

This color image of Earth was taken by NASA’s Earth Polychromatic Imaging Camera (EPIC), a four megapixel CCD camera and telescope. The image was generated by combining three separate images to create a photographic-quality image. . . .

. . . Once the instrument begins regular data acquisition, EPIC will provide a daily series of Earth images allowing for the first time study of daily variations over the entire globe. These images, available 12 to 36 hours after they are acquired, will be posted to a dedicated web page by September 2015.

(Source: Click on the image above to get to the NASA site about EPIC pictures.)

A fine article by NASA astronaut Scott Kelly, “A New Blue Marble” makes for delightful reading. Quotes:

No one on this planet had ever seen a whole picture of the Earth until 1972.

. . . the first full photo of the Earth, taken on December 7, 1972, by the American crew of the Apollo 17 spacecraft. The original Blue Marble is thought by many to be the most-reproduced image of all time.

What made the Blue Marble so special? Sure, it might have been the first full photo of the Earth that we took, but we’ve taken a bunch more since then.

Like this one.

. . . it’s quite tricky to take a good photo of the entire Earth.

The first challenge is that our planet is big. The only way to view all of it at once is to get much farther away from the Earth than we do for many of our activities in outer space. The International Space Station, for instance, orbits at a height of just 400 kilometers, or about 249 miles away from Earth.

The second problem is a familiar one that plagues many photographers who are Earthbound: lighting. In order to view the Earth as a fully illuminated globe, a person (or camera) must be situated in front of it, with the sun directly at his or her back. Not surprisingly, it can be difficult to arrange this specific lighting scheme for a camera-set up that’s orbiting in space at speeds approaching thousands of miles per hour.

Go read the Scott Kelly piece. But of course the best meditation on a picture of the earth from deep space is Carl Sagan’s “The Pale Blue Dot.” Even if you have read it before, watch the video and read the transcript again and marvel at Sagan’s lyrical genius.

BONUS link: Everything you wanted to know about Lagrange points but were never neatly explained to you.

Limits to growth with Chinese characteristics

Don’t panic. Stay the course.

I wrote to you this piece in December’14 when the Sensex went to around 26000 levels due to Russian crisis. I again wrote you the same piece in March’15 when Sensex touched 27000 levels due to Yemen crisis.

Today, at the time of writing in the morning, the Sensex is around 26500 levels. Now the panic is due to Chinese crisis and the fear of global slowdown.

So I would like to repeat below what I said on the previous occasions.

For those of you who are our long term investors, this kind of panic situations are not new. We face almost one once in a year or two. In stock markets, you are always given frequent tests to check your conviction levels. Only investors who pass these tests are given the 18% kind of returns the market offers to those who stay invested.

Six months ago, we shared a CRISIL data as to how those who stayed invested in equity funds for 17 years got an annualised return of 22.6%. Those 17 years had innumerable panic like situations; both domestically and globally. But those who sat patiently were hugely rewarded. Indian markets have given around 270 times returns over last 3.5 decades when both globally and locally we went through one crisis after another.

Panic and euphoria; booms and busts are perfectly normal. This is how it has been and this is how it would be. Moreover, for good or worse, we are all getting better informed. Even 10 years ago, we didn’t have the kind of information we posses now on an everyday basis; be it RBI policies, global crude prices, inflation figures, changes in global markets, commodity prices, fed policies etc.

Some experts opine that this spread of information has shortened the span of cycles. The ups and downs in the market have become more frequent than ever. Increased volatility is the price for instant information. 10%+ corrections are frequent. 20%+ corrections happen on a regular basis. In your investing life, you may even see 50%+ corrections three of four times. This is how it would be.

We all by now know and have even experienced the benefits of staying the course despite all the negativity. Moreover, India is one of the few countries which are in an advantageous position now globally. In short term, like everyone else, we would be impacted by global happenings; as sentiments drive markets in the short term. In the long run, we are in a structural growth both in terms of economy and markets; as fundamentals drive markets in the long term.

Many of you tell me that you no longer need constant reassurances as you’ve understood the benefits of staying the course and investing for long term. I’m glad to hear that. However it is my responsibility to constantly reinforce the power of compounding, role of time in investments, sitting patiently, investing regularly, investing for long term etc.

You’ve heard this John Bogle’s quote from me many times. Please listen now for one more time.

“Stay the course. No matter what happens, stick to your program. I’ve said ‘stay the course’ a thousand times, and I meant it every time. It is the most important single piece of investment wisdom I can give to you.”

Don’t panic. Stay the course.

Products to avoid for Retirement Planning

This is really a very brave post that I am attempting, caveat emptor. Buyer Beware.

Clarification No. 1: the past is not a great indicator of the future. What happened in the past may / may not happen in the past, and the growth trajectories could be lower. For example the YTD on Nifty as of today is zero, and we believe we are in a Bull Market.

Clarification No. 2: To buy products today based on the taxation structure that is likely to be when you withdraw is supremely idiotic, but I am going to suggest such strategies, because i have no clue what will happen 30 years hence.

Clarification No. 3: If you see equities being taxed, Estate duty being brought in, etc. this strategy will not hold.

With these 3 caveats let me tell you what products are bad from an accumulation STAGE or from a WITHDRAWAL stage.

- The top of the list is ENDOWMENT INSURANCE: It does not matter whether it is a ULIP or a traditional life insurance product. The structure of the product is such that the amount accumulated at the end of 15-20 years will surely UNDER PERFORM a comparable product like PPF. So if you have 3-4 PPF accounts (self, wife, Huf, minor child) you can contribute about Rs. 6L a year in PPF. Do not touch an endowment plan.

- Pension plan from a Life Insurance company: inefficient while accumulating (very debt oriented and very high charges) and very inefficient while withdrawing (taxable as annuity). See no merits at all.

- Bank fixed deposits: ALWAYS gives a negative real return and is fully taxable. Terrible combination.

- NPS: I am not willing to play the ‘cost’ card nor the extra 50k deduction u/s 80C of the Income tax act, 1961.

- I am not even covering stupid products like chit funds, etc

- Land: if you think a piece of land will appreciate and fund your retirement, it will not.

Can you think of any other assets? I like one Retirement product from a mutual fund – but that my recommendation is to start small when you are young and pump real big time when you are 50+

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

The Cycle of Wealth and Poverty

Some years ago, a very wise gentleman told me of a saying that succinctly describes the decline and fall of family fortunes, which happens to cycle in approximately four generations. “Khattu, Nikhattu, Udharichand, Baychumal”.

It begins with the generation that works hard (Khattu) and builds up the family fortune. It is followed by a generation that is lazy (Nikhattu) and lives off the wealth. The third generation becomes more lazy and lives off borrowings (Udharichand) against the remaining assets. Finally, the fourth generation ends up selling the assets and ends up poor.

A version of this cycle must apply at larger scales too, that of societies and nations. It could be a global phenomenon and if so, other societies must have recognized the phenomenon and therefore also have similar sayings. And indeed they do. Here are a few from around the world. I got them off the web.

In Portuguese, they say “Pai rico, filho nobre, neto pobre”, meaning “Rich dad, noble son, poor grandson”. Among the French, they remark that “the first generation builds, the second strengthens, and the third spends it all.” Another version goes, “Le grand-père était un aigle; le père était un faucon; le fils est un vrai con”, meaning “The grandfather was an eagle; the father was a hawk, and the son is a real jerk.”

The Irish recognize the decline but also add something more to it: “The first generation is poor, the second is poorer, and the third gets robbed by the British.” Getting robbed by the British is what the Irish have in common with Indians (and a few dozen other nations.) For India, I think it would be “The first generation is rich, then the thieving British makes the second generation poor, and then the Indian Congress leaders who inherit the British raj leave the third generation destitute.”

The Americans put it tersely, “Blue collar to blue collar in three generations.” The Germans appear to agree and with the Americans. “Der Vater erstellt’s, der Sohn erhält’s, dem Enkel zerfällt’s.”: “The father creates it, the son receives it, the grandson ruins it.”

A quote from Otto von Bismarck: “Die erste Generation verdient das Geld, die zweite verwaltet das Vermögen, die dritte studiert Kunstgeschichte und die vierte verkommt vollends.” The first generation earns the money, the second manages the wealth, the third studies history of art, and the fourth degenerates completely. In Swedish the saying goes, “Förvärva, ärva, fördärva”. Acquire, inherit, ruin. In Dutch, that goes “verwerven, erven, verderven”.

In China, they say that wealth does not pass three generations. In Korea, it’s difficult to remain wealthy beyond three generations. In Japan too, they say “from rice paddy to rice paddy in three generations.”

I suppose the Arabs also have their saying on the matter. The former Prime Minister of the United Arab Emirates, Râshid bin Sa`îd Âl Makṫûm recognized the grand cycle and said, “My grandfather rode a camel, my father rode a camel, I drive a Mercedes, my son drives a Land Rover, his son will drive a Land Rover, but his son will ride a camel.”

Fortunes do not last forever. But that’s because nothing lasts forever. Anicca or impermanence is a basic feature of the world. That same impermanence is characteristic not just of family fortunes but also of firms. Cardwell’s Law derives from it. The essential implication of that is that no country can maintain its technological dominance forever. There’s churn among firms for leadership, just as there is among nations, societies and families. That’s the fractal nature of the universe.

C’est la vie.

This can destroy your Retirement

You have slowly, but surely built a nice nest egg. You are looking forward to a long retired life. You have a nice mix of assets, a mix of income streams, and you are confident that age 60 to end of life is well planned. Is there ONE thing which can completely destroy your retirement and make you dependent on somebody? Yes, there is.

Long Term Illness / dependence which requires nursing – Long Term Care – as it is called in the USA. Sadly India does not have Long Term Care Insurance and you will be on your own. You would be on your own and your spouse could help you. Now if you have no children, and no nephew / niece who want to help and your spouse has predeceased you, welcome to the bad, bad world.

Sounds dangerous? impractical? will not happen to you? Sure, hope not, but at least be aware of the implications…

Staying at home or in a geriatric ward of an old age home is going to get very expensive. Recently I saw the shortage of nurses in the WORLD. It is huge – especially in Europe and USA – both countries with a rapidly aging population and ability to pay well. So we are going to be competing in the international market for old age care.

I am translating this cost to about to Rs. 50,000 per person per month. So assuming you require this for about 5 years, you will require about Rs. 50,000*12*5 = Rs. 30,00,000. There is not enough data about how long you will require this – in the sense there is not generic data, so the assumption of 5 years.

This amount is largely being drawn out of your retirement corpus. Hopefully LTC insurance will be introduced in India over the next few years, but let me warn you – the premium will be really high. LTC insurance is very expensive even in USA – where it has a longer history and a much record keeping track record.

The best things that you can do is to take proper care of your health (there is nothing you can really do to prevent Parkinsons or Alzheimers except pray). Be prepared for it mentally, physically and financially. Remember if this has to happen to you and your spouse cannot manage complex financial transactions, you will be left with 2 poor options – tax inefficient too – annuities and bank fixed deposits. So you need to have a big corpus that assumes at least about 20% taxation.

What all can you really do?

- accept that some illness / disease / fall can confine you to bed

- that will involve somebody having to assist you with simple daily operations which you have been doing for 70+ years

- for women it could mean a change of how you dress

- even for men it could mean wearing a gown instead of a payjama

- institutional care could be impersonal, do not have any expectation

- your spouse may need counselling on how to cope

- you may need counselling on how to cope with the illness/ trauma care

- your children with all good intentions MAY NOT be able to help you

- we have no clue how a Reverse Mortgage amount will be treated in your hands

- Geriatric care is very difficult to find, and if you have community, caste or geographic bias, you are doomed

- your mind may be active and your body may not co-ordinate making you VERY angry with the world

- Meditation may help

- death maybe a better solution, but you could live till 97 with the illness

Sorry, I will be happy if somebody can give this a happy twist.

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

LIFE is not about buying things you may not need…

Long ago when I had many brokerage clients and we ran a business, my partner asked me “how many diwali greetings do you need” and I absent mindedly said 2000-2500. He said be specific. I looked up and he said “look we have cards of last year lying in the loft which we have not thrown away…”

I realised that we do waste too much. Just way too much. 22 people recently travelled from point A to point B – and back in 9 cars. Same starting point, same destination, not a timed event, ..they could have travelled in 5 cars. Full stop.

As a generation we waste too much. Just too much. We buy too much, waste too much. We buy with money we do not have (borrow) to buy things we do not need (look around your house), by borrowing from banks we do not like, and repay this by doing jobs we do not like to do.

SURELY SOMETHING IS WRONG WITH US….what say? read on

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

Time In The Market Trumps Timing The Market For The Long-Term Investor

It’s funny. Add just a smidgen of volatility to the stock market and people go crazy.

It’s funny. Add just a smidgen of volatility to the stock market and people go crazy.

The last few days of last week proved to be a little volatile for the stock market. Oil prices are at multi-year lows right now. Questions about global growth, China, and Greece continue to dominate headlines.

But does any of this really matter for a long-term investor?

Not really.

Let’s Keep Perspective

If you look at the S&P 500’s price change over the last five years, it looks almost like a straight line up. The broader market is up almost 84% (before dividends) over that time frame, which is an incredible run coming off of the the financial crisis. As I recently discussed, the broader market appears overvalued right now. Although, many stocks within the market appear to actually be attractively valued.

Moreover, the broader market is down a little over 4% on the year. A correction across the board still hasn’t come to pass – the market is down something like 7% from recent highs. These are very small numbers. So if the recent volatility frightens you, now would be a really good time to figure out whether stocks have a major role to play in your asset allocation. Stocks aren’t for everyone.

Now, when you read headlines like “Stock market endures worst day in 18 months“, it makes sense to keep perspective. I mean we’re talking about a little volatility here in what has otherwise been more than five years of almost relentless increases across the board.

But the short term can be scary, even for a long-term investor. No one knows where the prices of stocks are going to be tomorrow.

But would this foreknowledge be helpful if you could have access to it? We all know timing the market isn’t possible, but what if you could time it? What if you had $20,000 to invest right now, but wanted to make sure you bought in after a major drop (should one occur)?

Turns out it doesn’t make that much of a difference over the long haul…

Black Monday

Black Monday. October 19, 1987.

The Dow Jones Industrial Average fell 22.61% on that one day.

Now that’s volatility.

So let’s say you had that same $20,000 (which would have been worth a lot more) to invest back in 1987. And let’s just say your best friend had a crystal ball. And that crystal ball told you that things were going to get really crazy on October 19.

You could have gone about it a number of ways. You could have invested in the S&P 500 (through a broad-based index fund) immediately after the drop. You could have spread that capital across any number of high-quality stocks that pay and grow dividends (what I’d do and am currently doing). You could have even bet large on one company.

Let’s take a look at what that would have done for you over the following 28 years.

Let’s say you decided to put all $20,000 in the Vanguard 500 Index Fund (VFINX), which is an index fund based on the S&P 500. And let’s say you gave it one day for things to cool off and put all $20K in on October 20, 1987. If we fast-forward to August 21, 2015, you’d have $293,128 sitting there for you. That’s an annualized return of 10.12%. Boy, you’d owe your best friend a lot of money, right?

Not quite.

Compare that to the person who lacked a crystal ball and decided to invest all $20K in VFINX the very Friday before Black Monday, on October 16, 1987. Just imagine the feeling in that person’s stomach when they woke up Monday to find out that their investment just took a major haircut. Well, this is where time in the market comes to save the day.

That same $20K invested in VFINX on October 16, 1987 would currently be worth $245,530. That’s an annualized return of 9.42%.

A difference of almost $50,000 shouldn’t be understated, but what do we see here? We see someone who still did incredibly well. An annualized rate of return still near 10%. While I’m not factoring in taxes or inflation, I also factored in a scenario where someone would invest all of their money all in one day, and that day happened to be the very day before one of the worst stock market crashes in history (the crash has its own name, after all).

But investing all of your money on the very worst day possible is highly, highly unlikely. It’s far more likely and reasonable to assume that you’re dollar cost averaging your way into stocks. And this smooths the results out even more, to the point where timing the market is almost negligible.

Time in the market is more important than timing the market because you have control over time in the market. Meanwhile, you can’t control timing the market. Longer periods of time provide an effect where short-term fluctuations almost disappear. The longer the period, the less short-term fluctuations show up.

And over long periods of time, high-quality dividend growth stocks tend to appreciate at an attractive rate while also growing their dividends well over the rate of inflation, increasing one’s purchasing power. That attractive growth rate over the long term can and does make up for poor short-term timing.

Take a look at Johnson & Johnson (JNJ) using the same dates and capital above. For the person who had access to their friend’s crystal ball, they ended up with an annualized return of 14.14%. That led to an investment worth $795,615. The investor that timed the market horribly but decided to hold on for the long haul and stick to the plan ended up with an annualized return of 13.73% and an investment worth $721,340. This is assuming reinvested dividends.

You can see this play out over and over again with any number of stocks. One would do better if they had access to a crystal ball, but not that much better. And the longer we go, the less it will matter.

The key takeaway here is that one still does incredibly well over the long haul if they stick to the plan, even if they put their capital to work right before major volatility strikes. Buy quality, ignore the noise, reinvest the dividend income.

Dollar Cost Averaging And Spreading Your Capital Around

Now, it’s more likely that you’re going to be investing smaller amounts of money over a longer period of time. You’re likely going to be spreading that capital out across many high-quality companies. And you likely would have been investing both before and after the big drop.

Let’s break that $20K down over the course of a year (using totally random dates) and across 10 different stocks (that were known for their dividend prowess even back then) just to see what happens:

- $2K invested in The Coca-Cola Co. (KO) on February 2, 1987 would have provided an annualized return of 12.21% and a total investment now worth $53,769.

- $2K invested in Exxon Mobil Corporation (XOM) on March 25, 1987 would have provided an annualized return of 10.29% and a total investment now worth $32,339.

- $2K invested in Johnson & Johnson (JNJ) on May 7, 1987 would have provided an annualized return of 10.31% and a total investment now worth $32,195.

- $2K invested in General Electric Company (GE) on June 29, 1987 would have provided an annualized return of 9.11% and a total investment now worth $23,278.

- $2K invested in Procter & Gamble Co. (PG) on September 9, 1987 would have provided an annualized return of 11.97% and a total investment now worth $47,227.

- $2K invested in 3M Co. (MMM) on October 26, 1987 would have provided an annualized return of 11.98% and a total investment worth $46,652.

- $2K invested in Colgate-Palmolive Company (CL) on December 2, 1987 would have provided an annualized return of 15.25% and a total investment worth $102,512.

- $2K invested in Consolidated Edison, Inc. (ED) on December 22, 1987 would have provided an annualized return of 10.21% and a total investment worth $29,496.

- $2K invested in General Motors Corporation (GM) on January 13, 1988 would have resulted in an investment eventually worth $0 (assuming one held all the way to bankruptcy, which would be unlikely; and dividends would have provided some return unless reinvested all the way along, which I’m assuming here).

- $2K invested in McDonald’s Corporation (MCD) on February 10, 1988 would have resulted in an annualized return of 12.79% and a total investment worth $55,079.

I hate doing backtesting like this because it’s easy to cherry pick certain stocks to make a point. But I think most investors investing the way I do now would be interested in stocks like the ones I listed above even back in 1987 and 1988. Many were part of the DJIA at the time and all of them had some dividend pedigree already. In the end, though, this is purely illustrative.

However, you can see what dollar cost averaging both before and after a major stock market drop looks like when the time frame is drawn out across almost 30 years. The total return across the entire portfolio is pretty outstanding, even factoring in the eventual bankruptcy of the old GM. This portfolio would now be worth $422,547. That’s more than had you invested in the S&P 500 on the day after Black Monday. And that’s assuming 10% of your portfolio eventually became worth nothing.

What I also see here is that quality matters more than anything else. Coca-Cola did very well for shareholders over the last few decades, even for those that bought in not long before Black Monday. But those who may have scored GM at a cheaper price after the crash eventually found themselves in a poor position. So value matters. But quality matters much more.

Conclusion

I don’t often put forth backtesting. I’m more interested in what the journey to financial independence looks like in real-time with real money. But I think it’s important to keep perspective whenever there’s some volatility in the market, and the illustrative examples used above helps further the discussion.

If you’re able to focus on quality, ignore the noise, reinvest your dividends, buy when the value is there, and hold for the long haul, your odds of achieving very satisfactory returns and growing dividend income over the long term are very good. For the long-term investor, time in the market trumps timing the market by a large degree. I take comfort in knowing that I wouldn’t do much better than I’m already going to do, even if I had a crystal ball that told me when the stock market was next going to fall substantially.

So stick to your long-term plan. Ignore the headlines that tell you the sky is falling. Don’t let Mr. Market bully you into making poor choices. Use short-term volatility as a long-term opportunity, because the long term smooths out short-term fluctuations. However, those short-term fluctuations can provide for even better deals on high-quality assets. It might seem scary at the time, but your future you will be in a much better position if you stay focused on time in the market rather than timing the market.

Full Disclosure: Long KO, XOM, JNJ, GE, PG, and MCD.

What do you think? Do you think time in the market matters more than timing the market? Is timing the market – an impossible task – worth the effort?

Thanks for reading.

Photo Credit: cooldesign/FreeDigitalPhotos.net

Edit: Added note about GM dividends.

Edit: Corrected error.

Another teachable moment in currency management

Oil dominates the country's export basket and contributes the lions share of the government's revenues, as seen from this 2013 export products graphic.

Nigeria, which has stubbornly kept its currency pegged to the US dollar, thereby suffering a steep drop in its oil revenues, looks most likely to soon burn out its reserves and be forced to let the over-valued naira depreciate steeply.

Under successive presidents, Colombia put together a framework that aimed for structural fiscal balance, instituted inflation targeting and achieved relatively broad-based growth... Over the past year, the economy’s exposure to the oil price (more than 50 per cent of exports) has resulted in the Colombian peso being one of the weakest freely-traded currencies in the world, by falling 36 per cent over the past 12 months. Like most EM currencies, it received another kick downwards from China’s renminbi devaluation last week. The rapid depreciation alongside falls in dollar-denominated oil prices means that in recent months, Colombia’s oil revenues in domestic currency terms have fallen relatively little, even compared with other oil economies. Economists at Barclays calculate that oil priced in Colombian pesos fell just 1.3 per cent from early May to late July, compared with falls of 6.2 per cent in Russian rouble terms and 14.4 per cent if priced in Nigerian naira...

(unlike its peers) the Colombian central bank has left monetary policy on hold since last August. Colombian consumer price inflation has recently risen to 4.5 per cent, just above the central bank’s 2-4 per cent target band, but inflationary expectations have remained well anchored... the IMF forecast that the economy would expand 3.4 per cent this year, below last year’s 4.6 per cent but far better than the recessions forecast in Russia and Brazil, and that inflation would drop back below target.

An example illustrates the point. If a truly serious CPI target had been in place five years ago at the time of the global financial crisis, then Kazakhstan would have faced a difficult and unnecessary dilemma when it was hit by adverse shocks in oil prices, the housing sector, and the banking system. The country would have had either to forego the necessary February 2009 depreciation of the tenge or else to violate strongly the CPI target as the devaluation pushed up import prices. The former choice would have been dangerous for the economy, while the latter choice would have largely defeated the purpose of having announced IT in the first place (that purpose being long-term monetary credibility).

Kazakhstan is vulnerable to a variety of possible shocks, such as a fall in the world oil price, which would be better accommodated by a more flexible exchange rate regime... An alternative anchor for monetary policy, in place of either the dollar exchange rate or any version of the CPI, is nominal GDP... the innovation would in fact be better suited to middle-income commodity-exporting countries like Kazakhstan. The reason is that supply shocks and trade shocks are much larger in such countries. In the event of a fall in dollar oil prices, neither an exchange rate target nor a CPI target would let the tenge depreciate. An exchange rate target would not allow the depreciation by definition, while a CPI target would work against it because of the implications for import prices. In both cases sticking with the announced regime in the aftermath of an adverse trade shock would likely yield an excessively tight monetary policy. A nominal GDP target would allow accommodation of the adverse terms of trade shock: it would call for a monetary policy loose enough to depreciate the tenge against the dollar.

Taxation in Retirement

Let us look at what assets you are likely to draw upon while in retirement, and how it is taxed. By the time you retire you would have accumulated some direct equities, mutual funds – debt, equity and balanced, own provident fund, gratuity, public provident fund, Nps, bank fixed deposits, bonds, real estate, retirement plans from a mutual fund, retirement plans from a life insurance company, and the likes.

Let us see from a tax point of view what you should / should not do when you are YOUNG so that suddenly at the age of 60years you are not left with tax inefficient assets.

1. Direct equities: In India this is the darling from a tax point of view. Dividends and capital gains both are tax free. If you have accumulated a decent direct equities portfolio and are confident of managing it during your retirement, keep this going till your age of 70-75 years, Use that money to buy an annuity at that age – use up say AT LEAST 50% of the equity portfolio to buy an annuity without return of premium.

2. Equity mutual funds as well as balanced funds (with more than 65% in equities) are in the same category as direct equities – and when you are accumulating for the long term please opt for the Growth option.

3. Debt funds: If you have accumulated money in debt funds over a long period of time (Growth plan) you are likely to have accumulated a decent sum of money in these accounts too. In case you withdraw from here on a regular basis (SWP: Systematic withdrawal plan) you are likely to pay a very low rate of tax. This is treated as capital gains and the money accumulated for say 20 years will come back to you almost tax free. This is because of the taxation structure and capital gains being taxed less than regular income. This is one solid reason why you should choose a debt fund over bank / company fixed deposits.

4. Your own provident fund comes back to you as a lumpsum which you can invest as you wish. This amount is tax free and you get this within a month or two post retirement.

5. Gratuity: Most of the gratuity plans in India are bought with LIC – this gets commuted and becomes a pension. The amount is generally received on a regular basis – monthly or quarterly. This is FULLY TAXABLE in your hand. The annuity is just like your salary that you were receiving when you were in service. No deduction or indexation or anything is available for this.

6. NPS, Pension from employer, etc. Pension from a life insurance company: are all treated the same as the annuity from the gratuity. These are the most inefficient ways to invest, but are very popular because the media pushes these things very hard. Also life insurance companies which have sold pension plans fall under this category.

7. When you accumulate a pension under a pension policy of a mutual fund, you are better off because you have an option of when to withdraw, how much to withdraw, etc. – the taxation is also friendlier. You are treated like a debt fund and the taxation is like capital gains. So you will be taxed much lesser than the taxation if the plan were in a life insurance company.

Post office schemes, bank fixed deposits, etc. are taxed on an actual basis – when you get the income / when it accrues you pay the tax.

Post Footer automatically generated by Add Post Footer Plugin for wordpress.

Weekend Reading Links

The North American rig-count has dropped to 664 from 1,608 in October but output still rose to a 43-year high of 9.6m b/d June... Gas prices have collapsed from $8 to $2.78 since 2009, and the number of gas rigs has dropped 1,200 to 209. Yet output has risen by 30pc over that period.

Interestingly, coming in the same week as this scathing indictment of Amazon's work practices, this essay on India's own Amazons appears to have hardly raised a flutter. Does it reflect poorly on the quality of public debates in India? As an aside, the real story with e-commerce would be one which shows how most of these firms are bleeding capital and it could be a very prescient curtain raiser on what looks certain to be India's first real dot-com bubble and bust.

If average bank capital in 2008 had been, say, 20 or even 30 per cent of assets (instead of the recent levels of 10 to 11 per cent), serial debt default contagion would arguably never have been triggered. Had Bear Stearns and Lehman Brothers continued as capital-conscious partnerships, a paradigm under which both thrived, they would probably still be in business. The objection to a capital requirement of 20 per cent or more, even when phased in over a series of years, is that it will supress bank earnings and lending. History, however, suggests otherwise...

If history is any guide, a gradual rise in regulatory capital requirements as a percentage of assets (in the context of a continued stable rate of return on equity capital) will not suppress phased-in earnings since bank net income as a percentage of assets will be competitively pressed higher, as it has been in the past, just enough to offset the costs of higher equity requirements. Loan-to-deposit interest rate spreads will widen and/or non-interest earnings will increase. An important collateral pay-off for higher equity in the years ahead could be a significant reduction in bank supervision and regulation.4. Livemint points to a report on ownership of equities in the Indian stock markets. Foreign participation has been rising in recent years, as reflected in the steadily rising share of foreign holdings on BSE 200 equities...

By lowering interest rates we can weaken our exchange rate and take demand from our trading partners. We can also take demand from the future by inducing more borrowing against future income and also by a “wealth effect” when lowering interest rates makes future cash flows appear more valuable. So we can steal demand from foreigners, induce people to borrow more than they otherwise would, or make rich people appear richer.

Quebec's trees produce more than 70 percent of the world’s supply and fills the majority of the United States’ needs. The federation, in turn, has used that dominance to restrict supply and control prices of the pancake topping. It is effectively a cartel, approved by the provincial government and backed by the law. In 1990, the federation became the only wholesale seller of the province’s production, and in 2004, it gained the power to decide who gets to make maple syrup and how much... In 2003, a majority of federation members voted to make production quotas mandatory, meaning farmers could sell only a certain amount each year. Farmers are required to sell all of their syrup through the federation or its designated agents... When the federation suspects farmers are producing and selling outside the system, it posts guards on their properties. It seeks fines from producers and buyers who do not follow the rule. In the most extreme situations, it seizes production...

It defends the system, saying it keeps prices high and stable... To keep prices high, the federation enforces strict quotas for the province’s 7,400 producers. Instead of flooding the market during years with bumper crops, all syrup produced beyond that amount is stored in the federation’s warehouse, which helps prop up prices by limiting supply. When seasons are lean, it releases the syrup, to maintain stable supply and pricing... Stacked in barrels nine high, the reserve currently holds about 60 million pounds of maple syrup. Prices are set by the federation, in negotiation with a buyers’ group. The federation holds most of the power, given that it controls a majority of the world’s production.

Companies have raised $290bn of debt to buy competitors this year — almost triple the level in the same period in 2014. The number of issues, however, has risen only 46 per cent, so the average size has been much larger. In the first half of the year there were $987.7 bn of deals in the US... the highest since records began in 1980.