Here’s a simple question someone asked on Quora – Will I become a billionaire if I am determined to be one and put in the necessary work required?

Here’s how a lady answered this –

No.

One of the many qualities that separate self-made billionaires from the rest of us is their ability to ask the right questions.

This is not the right question.

(Which is not to say it’s a bad question. It just won’t get that deep part of your mind working to help you — mulling things over when you think you’re thinking about something else — sending up flares of insight.)

You’re determined. So what? You haven’t been racing naked through shark-infested waters yet. Will you be just as determined when you wash up on some deserted island, disoriented and bloody and ragged and beaten and staring into the horizon with no sign of rescue?

We live in a culture that celebrates determination and hard work, but understand: these are the qualities that keep you in the game after most everybody else has left, or until somebody bigger and stronger picks you up and hurls you back out to sea. Determination and hard work are necessary, yes, but they are the minimum requirements. As in: the bare minimum.

A lot of people work extremely hard and through no fault of their own — bad luck, the wrong environment, unfortunate circumstances — struggle to survive.

How can you *leverage* your time and your work?

Shift your focus away from what you want (a billion dollars) and get deeply, intensely curious about what the world wants and needs. Ask yourself what you have the potential to offer that is so unique and compelling and helpful that no computer could replace you, no one could outsource you, no one could steal your product and make it better and then club you into oblivion (not literally). Then develop that potential. Choose one thing and become a master of it. Choose a second thing and become a master of that. When you become a master of two worlds (say, engineering and business), you can bring them together in a way that will a) introduce hot ideas to each other, so they can have idea sex and make idea babies that no one has seen before and b) create a competitive advantage because you can move between worlds, speak both languages, connect the tribes, mash the elements to spark fresh creative insight until you wake up with the epiphany that changes your life.

The world doesn’t throw a billion dollars at a person because the person wants it or works so hard they feel they deserve it. (The world does not care what you want or deserve.) The world gives you money in exchange for something it perceives to be of equal or greater value: something that transforms an aspect of the culture, reworks a familiar story or introduces a new one, alters the way people think about the category and make use of it in daily life. There is no roadmap, no blueprint for this; a lot of people will give you a lot of advice, and most of it will be bad, and a lot of it will be good and sound but you’ll have to figure out how it doesn’t apply to you because you’re coming from an unexpected angle. And you’ll be doing it alone, until you develop the charisma and credibility to attract the talent you need to come with you.

Have courage. (You will need it.)

And good luck. (You’ll need that too.)

Well, the lady answering this was Justine Musk, the ex-wife of Elon Musk. And what she described above can easily be taken as a description (to the tee) of her ex-husband, who has set on a journey to save the human race from self-imposed or accidental annihilation – through his ventures in space (SpaceX), electric cars (Tesla Motors) and solar power (SolarCity).

I’ve been reading a lot on Elon Musk over the past few weeks and months. But when I got down to write about my learnings from his life and experiences, I realized most things about him were those I could have never learned in several lives, because I could have never practiced them in one.

What Musk is doing is just out of this world stuff (literally). And then, like there was just one Steve Jobs, there is just one Elon Musk.

As I first started reading about Musk, it was easy for me think of him as rash, arrogant and abusive, and was pitiful of people who worked under him.

Source – Elon Musk’s Biography by Ashlee Vance

In fact, my thoughts were validated when I read this from one of his employees’ postings on Quora – “Working with him isn’t a comfortable experience, he is never satisfied with himself so he is never really satisfied with anyone around him…the challenge is that he is a machine and the rest of us aren’t.”

And then, this frustrated anonymous commenter concedes that the way Elon is “is understandable” given the enormity of the task at hand, and that “it is a great company and I do love it.”

The more I’ve read about him, and the more I’ve tried to look at his side of the picture, my respect for him and his vision has just increased day after day.

Before I write more about Elon, and a few lessons from him that I think I can apply to my life and work, let me ask Sir Richard Branson to explain briefly his thoughts about man who comes closest to the real-life version of Iron Man’s Tony Stark –

Whatever skeptics have said can’t be done, Elon has gone out and made real. Remember in the 1990s, when we would call strangers and give them our credit-card numbers? Elon dreamed up a little thing called PayPal. His Tesla Motors and SolarCity companies are making a clean, renewable-energy future a reality…his SpaceX [is] reopening space for exploration…it’s a paradox that Elon is working to improve our planet at the same time he’s building spacecraft to help us leave it.

Every generation produces a few people who change the world. It’s important for us to study such people. for there’s a lot we can learn from them.

Apart from the clichéd ones like take risks, follow your passion, be optimistic, never give up, think long term, and take criticism into your stride, here are my five big-big learnings from Elon Musk –

1. First Principles, First

Ralph Waldo Emerson wrote…

As to methods there may be a million and then some, but principles are few. The man who grasps principles can successfully select his own methods. The man who tries methods, ignoring principles, is sure to have trouble.

Boiling things down to the most fundamental truths – first principles – and then reasoning up from there, is one of the big ideas I’ve absorbed from my reading about Musk.

Source – Elon Musk’s Biography by Ashlee Vance

“The normal way we conduct our lives is we reason by analogy,” he said in an interview. “With analogy we are doing this because it’s like something else that was done, or it is like what other people are doing. With first principles you boil things down to the most fundamental truths…and then reason up from there.”

In simpler words, first principles thinking helps you to edit out complexity from your decision making so that you can focus on the most important things that matter to that decision. Let me explain with an example from Musk’s life and how he used first principles to start SpaceX.

If you are trying to estimate the cost of building a rocket, the simple way would be to look at the products available in the market, and add up all the costs. That’s analogy-based thinking – “Let me pay what others are paying for this product.”

But what Musk and his team did was that they figured out what the necessary parts of a rocket are (like its battery) and then found out how much the raw materials of those parts would cost.

In an interview, this is what Musk said about his usage of first principles in the rocket business –

Someone could – and people do – say battery packs are really expensive and that’s just the way they will always be because that’s the way they have been in the past. They would say, “It’s going to cost $600 / kilowatt-hour. It’s not going to be much better than that in the future.”

But when you think in first principles, you start asking fundamental questions, like Musk did…

What are the material constituents of the batteries? What is the spot market value of the material constituents? It has carbon, nickel, aluminum, and some polymers for separation, and a steel can. Break that down on a materials basis, if we bought that on a London Metal Exchange, what would each of these things cost?

Oh jeez, it’s $80 / kilowatt-hour. Clearly, you need to think of clever ways to take those materials and combine them into the shape of a battery cell, and you can have batteries that are much cheaper than anyone realizes.

The result of such thinking was astonishing. According to early Tesla and SpaceX investor Steve Jurvetson, using first principles, Musk calculated that the raw materials for building a rocket actually were only 3% of the sales price of a rocket at the time. By applying vertical integration and the modular approach from software engineering, SpaceX could cut launch price by a factor of ten and still enjoy a 70% gross margin!

Anyways, let me now put the first principles thinking to investing. Most people would ask – “How can I learn to invest like Warren Buffett” (thinking by analogy, which will not take you too far).

Instead of this, how about asking – “How can I improve myself to become a better investor than I am currently?” And then – “What areas should I work on to become a better investor?”

Here are the most fundamental rules you must know and practice if you want to become a sensible investor –

-

Look at stocks as part ownership of a business

- Learn to understand businesses, and differentiate between good and bad ones

- Think like an owner, and don’t enter stock market for short term excitement…but for long term profits

-

Look at Mr. Market – stock price fluctuations – as your friend rather than your enemy

- Avoid looking at daily stock prices and getting worried or excited when they are falling/rising

- Avoid making an investment decision based on what the stock is doing – instead consider what the underlying business is doing

-

Never forget margin of safety – the three most important words in investing

- Always pay lot less than what the stock is quoting at

- Only consider businesses that are simple to understand and simple to run, so that the probability of the management doing something wrong is less

- Build a good understanding of the business you are getting into, which also provides a margin of safety

Only if you can focus on these principles, and make them your guideposts, you do not need to search for any other success mantra in your investment lifetime.

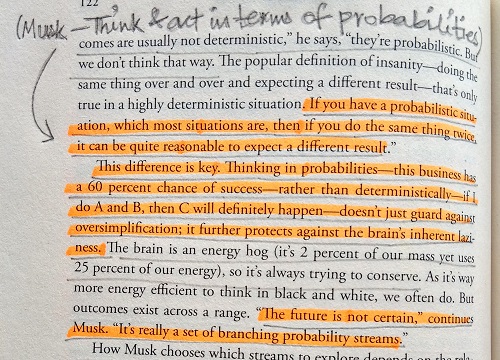

2.Think in Probabilities

Another one of Musk’s big lessons is to think in terms of probabilities, especially when you are pursuing things that are bold, and even otherwise.

Source – Bold by Peter Diamandis

“The future is not certain,” Musk says. “It’s really a set of branching probability streams.”

When you think in terms of probabilities, rather than being overconfident that anything you do would succeed, you are better prepared to guard against risks that might ensue. Musk said in an interview…

I think in general you always want to try to think about the future, try to predict the future. You’re going to generate some error between the series of steps you think will occur versus what actually does occur and you want to try to minimize the error. That’s a way that I think about it. And I also think about it in terms of probability streams. There’s a certain set of probabilities associated with certain outcomes and you want to make sure that you’re always the house. So things won’t always occur the way you think they’ll occur, but if you calculate it out correctly over a series of decisions you will come out significantly ahead.

This is such an important lesson for investors – think in terms of probabilities, that things can go wrong as probably as they could go right. Risk is, after all, the probability of permanent loss of capital. It’s thus so important to avoid investments where this probability – of permanent loss of capital – is high.

Predicting that the Sensex would touch 40,000 in 2 years is deterministic. But saying that there’s a 20% chance of the Sensex touching 40,000 in 2 years is probabilistic. In this second scenario, there’s a bigger 80% chance that the Sensex would not touch 40,000…and this is what the experts making predictions on business media would never tell you. They would make bold predictions, without letting you know that they deeply believe that the prediction will most probably not come true.

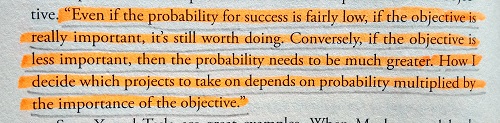

3. Probabilities are (Sometimes) Irrelevant

Musk says …

If something is important enough, even if the odds are against you, you should still do it.

Now, this lesson from Musk is an antithesis of the one above i.e., thinking and acting in terms of probabilities. Here, Musk is bringing the ‘objective’ into the picture.

Source – Bold by Peter Diamandis

If something is important enough, he says, even if the odds are against you, you should still do it. He has often mentioned that both Tesla and SpaceX had way less than 50% chance of being successful. But then…

I thought these were things that needed to be done. So even if the money was lost, it was still worth trying.

Now you cannot apply this lesson to investing, because here things that must not be done, must not be done. There’s no great purpose you can aim to achieve by betting on stocks for the short term, buying bad businesses, and indulging in reckless speculation.

I am sure when investors get into such troublesome things, where the probability of success in very low, they are not thinking – “I want to change the world doing this.”

Such things are never worth doing, unlike when you wish to get into something that would really benefit those around you…like educating people, starting an NGO, building schools and hospitals, or like Musk, building green cars.

This goes to the point Justine Musk made in the answer I shared at the start of this post –

Shift your focus away from what you want (a billion dollars) and get deeply, intensely curious about what the world wants and needs…The world doesn’t throw a billion dollars at a person because the person wants it or works so hard they feel they deserve it. (The world does not care what you want or deserve.) The world gives you money in exchange for something it perceives to be of equal or greater value: something that transforms an aspect of the culture, reworks a familiar story or introduces a new one, alters the way people think about the category and make use of it in daily life.

Given that he was on the verge of losing it all several times in his career and personal life, I’m sure Elon Musk didn’t ask himself, “What are some of the best ways I can make money or improve my life?” Instead, he must have often asked himself, “What are some of the problems that are likely to affect the future of humanity?”

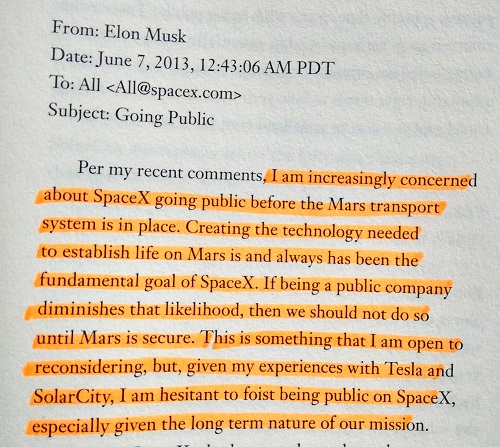

Read any of his interviews or any of the books written on him, and you will rarely (maybe, never) find a mention of “profit”. Rather, Musk only discusses how he plans to create businesses that serve the humanity – like SpaceX’s goal to make humanity into a multi-planetary species, or Tesla’s goal to accelerate the world’s movement toward having environment-friendly electric cars.

Like, here is what he wrote to SpaceX employees, showing his concern for going public…

Source – Elon Musk’s Biography by Ashlee Vance

In his fight, Musk is battling the giants of the US military-industrial complex, and the established car makers, but then he continues to fight to improve the world.

4. Imagine

Here’s a note from Ashlee Vance’s biography of Musk…

Source – Elon Musk’s Biography by Ashlee Vance

Visual thinking is a great way to understand complex or potentially confusing information, and also a way to organize your thoughts and improve your ability to think and communicate.

Imagine someone talking to you, and starting with the word – “Imagine…”

You are completely hooked, isn’t it?

Consider this excerpt from Richard Feynman’s The Pleasure of Finding Things Out, where his father helps him visualize about dinosaurs –

We had the Encyclopedia Britannica at home and even when I was a small boy my father used to sit me on his lap and read to me from the Encyclopedia Britannica, and we would read, say, about dinosaurs and maybe it would be talking about the brontosaurus or something, or tyrannosaurus rex, and it would say something like, ‘This thing is twenty-five feet high and the head is six feet across,’ you see, and so he’d stop and say, ‘let’s see what that means. That would mean that if he stood in our front yard he would be high enough to put his head through the window but not quite because the head is a little bit too wide and it would break the window as it came by.’ Everything we’d read would be translated as best as we could into some reality and so I learned to do that – everything that I read I try to figure out what it really means, what it’s really saying by translating.

Then consider how Warren Buffett visually convinced me why gold was a bad investment…

I will say this about gold. If you took all the gold in the world, it would roughly make a cube 67 feet on a side… Now for that same cube of gold, it would be worth at today’s market prices about $7 trillion dollars – that’s probably about a third of the value of all the stocks in the United States… For $7 trillion dollars… you could have all the farmland in the United States, you could have about seven Exxon Mobils, and you could have a trillion dollars of walking-around money… And if you offered me the choice of looking at some 67-foot cube of gold and looking at it all day, and you know me touching it and fondling it occasionally…Call me crazy, but I’ll take the farmland and the Exxon Mobils.

I’ve tried my hands at visual thinking this way…

So, visual thinking is not a new lesson that I would attribute to Elon Musk. But imagine the kind of businesses he is building, to save the world (imagine!), which he had originally visualized when he was under ten years of age.

When it comes to investing, you can avoid yourself a lot of pain by just visualizing your life after you’ve lost a lot of money trading and speculating in the stock market. If the visuals unnerve you, don’t do anything that would get you into such a situation. That’s also the concept of inversion.

I personally used visual thinking when I was deciding about quitting my job to start Safal Niveshak to help small investors become better at their investment decision making. Of course, when I had started planning my future after a job, the first visual was that of – not being successful in my future work, getting over my savings, and having to return to a job.

But another visual I saw was of helping people, enjoying the freedom of doing things my way, and spending a lot of time with my family. And I thank my stars that this was more powerful than the visual of losing everything.

5. Teach Yourself

Again, not a new lesson but just the way Musk did it is amazing. Here’s a note from his biography…

Source – Elon Musk’s Biography by Ashlee Vance

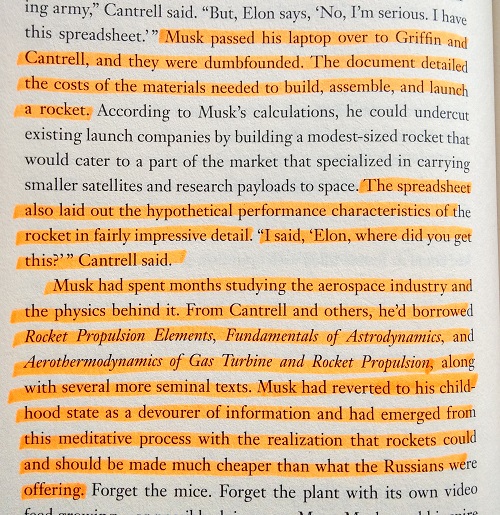

Musk had a bachelor’s degrees in physics and economics from the University of Pennsylvania, I’m sure those did not prepare him to run his space company SpaceX.

Jim Cantrell, an aerospace consultant at the time Musk was starting out with SpeceX, became its first VP of business development and Musk’s industry mentor when the company launched in 2002. As per him, Musk taught himself rocket science by reading textbooks and talking to industry heavyweights.

“He would quote passages verbatim from these books,” Cantrell said in an interview. “He became very conversant in the material.”

Apart from teaching himself from books, Musk also got headlong into learning from other people’s expertise. Cantrell says, “It was as if he would suck the experience out of them. He truly listens to people.”

These are wonderful attributes to have – teaching yourself things you are passionate about, and then keep learning…from books and people.

Learning about space is surely difficult, but learning how to invest sensibly isn’t so. But then, you must bring the passion and willingness to learn on the table…or no books or courses would help you.

Bonus Lesson – Believe in the J-Curve

It’s easy to consider Elon Musk and his advance in space, electric cars, and solar power as ridiculously rapid. But that’s not the case at all.

SpaceX was founded in June 2002, and Tesla in July 2003…that’s around 12-13 years back.

So, while we are seeing huge acceleration in what these companies can do, these have not been overnight successes. It’s only that they have become better (and rapidly now) with time.

So, what we are really seeing with Musk’s businesses are the returns on the far side of the J-curve.

In private equity, the J-curve is used to illustrate the historical tendency of private equity funds to deliver negative returns in early years and investment gains in the outlying years as the portfolios of companies mature.

In business, the J-curve signifies the accelerated payoff from investments made in the past, which suggests that it’s not always a great idea to reject companies that are running negative cash flows as of now, because they may be investing for a highly cash-rich future. Only that you must ensure sufficient margin of safety in case the curve doesn’t become a J, and never picks up after falling of the initial cliff.

As an investor or a businessmen, it’s important to believe in the J-curve effect when considering good businesses or ventures to invest in – though after considering the probability of the effect taking place (you may not want to apply the J-curve thinking with most e-commerce businesses).

Is Musk Steve Jobs 2.0?

Elon Musk may give an impression of being the next Steve Jobs, but I see a few dissimilarities between the two. Most important of them is their focus. While Jobs was intensely focused on what the consumer wanted, Musk is focused on what the humanity needs. Of course, both have been super achievers in their chosen field and have been great storytellers, Musk is busy pushing the limits of human ability.

The genius of Steve Jobs lied in marketing technology as an extension of a human being. It’s to his credit that while humanity will survive without an iPhone or an iPad or any such toy, an Apple fan may not.

But Musk is aiming for something spectacular. Of course, dramatic risks accompany just about everything he does. But his seems to possess a level of conviction that is intense and exceptional, and which is a lesson so hard to learn for anyone.

A Risky Life?

One lesson I may never take from Musk is that of working hard enough to not care about my health and personal life. Here’s a note from his biography…

Source – Elon Musk’s Biography by Ashlee Vance

Musk expects entrepreneurs to work

80 to 100 hours a week, or around 11-14 hours a day, seven days a week, if they want to create a dent on history.

Well, I have nothing to add here because I aim for 3-4 hours of work a day, and am doing just fine in my own objectives in life.

The J-curve also works with your health, and things can get really out of order (in the negative sense) if you don’t care of your body for a long period of time. So this is one lesson – of working super hard even at the risk of compromising your health – I would never take from Elon Musk.

But then, there’s a lot to learn from this man who has given us hope and renewed faith in what technology can do for mankind.

Hail Musk!