Note: This article first appeared in the February 2015 issue (free to download) of our premium newsletter, Value Investing Almanack.

Let me make an offer to you which has a potential to make you richer by couple of million dollars and that requires an effort not more than wiggling a finger. Would you be interested?

“What’s the catch?” That would be your first question, right?

Well, I’ll leave it to you to figure out the catch. So here is the deal, in fact I’ll let Nassim Taleb, author of Fooled By Randomness, do the explaining –

Imagine you are offered $10 million to play Russian roulette, i.e., to put a revolver containing one bullet in the six available chambers to your head and pull the trigger[no effort, I told you!]. Each realisation would count as one history, for a total of six possible histories of equal probabilities. Five out of these six histories would lead to enrichment; one would lead to a statistic, that is, an obituary with an embarrassing (but certainly original) cause of death.

Although, Russian roulette is a hypothetical situation, a thought experiment, but it highlights a big flaw that exists in how we perceive the reality. Taleb adds –

The problem is that only one of the histories is observed in reality; and the winner of $10 million would elicit the admiration and praise…the public observes the external signs of wealth without even having a glimpse at the source.

So can you see how we are blind to alternative histories? The silent events i.e., the events which could have happened but didn’t. In the language of behavioural finance this irrationality is known as Survivorship Bias. The outcome which is visible, ‘survived’ and the ones which didn’t survive are hidden.

In effect, the general belief is that if the outcome is good, the process and decisions made to arrive at that outcome must have been sound.

Alas, life doesn’t follow such straight patterns. The randomness and ‘external factors’ play a defining role in life and, as we will see later in this post, in investing too. Taleb notes –

Reality is far more vicious than Russian roulette. First, it delivers the fatal bullet rather infrequently, like a revolver that would have hundreds, even thousands, of chambers instead of six. After a few dozen tries, one forgets about the existence of a bullet, under numbing false sense of security…

…one is thus capable of unwittingly playing Russian roulette and calling it by some alternative “low risk” name. We see the wealth being generated…people lose sight of their risks. The game seems terribly easy and we play along carelessly.

What are these Russian roulette(ish) games in real life, you may ask. Using debt to buy things (especially the things that you don’t need) is one such game. Buying stocks on debt or on margin is another.

What are these Russian roulette(ish) games in real life, you may ask. Using debt to buy things (especially the things that you don’t need) is one such game. Buying stocks on debt or on margin is another.

And then comes along somebody who warns investors not to play this simple looking (but risky) game, but his advice is ignored.

Say you engage in a business of protecting investors from rare events and say nothing happens during the period. Some of them will complain, “You wasted my money on insurance last year, the factory didn’t burn, it was a stupid expense. You should only insure for events that happen.”

Another unintended outcome of alternative history blindness is that we grow confident about our understanding of the game. We rationalize the causal link between the event and the associated outcome (also known as Narrative Fallacy or Hindsight Bias). Our thinking becomes outcome-centric.

In a wonderful book Everything is Obvious, the author, Duncan J. Watts writes –

In a variety of lab experiments, psychologists have asked participants to make predictions about future events and then reinterviewed them after the events in question had taken place. When recalling their previous predictions, subjects consistently report being more certain of their correct predictions, and less certain of their incorrect predictions, than they had reported at the time they made them.

An interesting experiment (you must read this) was designed to simulate parallel worlds and the results of this experiment proved that the role of randomness in success is bigger than we usually imagine.

Does it mean that we should ignore the past and stop making plans for the future? Of course not! It just means that we should have a healthy skepticism towards predictions and explanations that are served to us by others (including the ones served by our own lizard-brain).

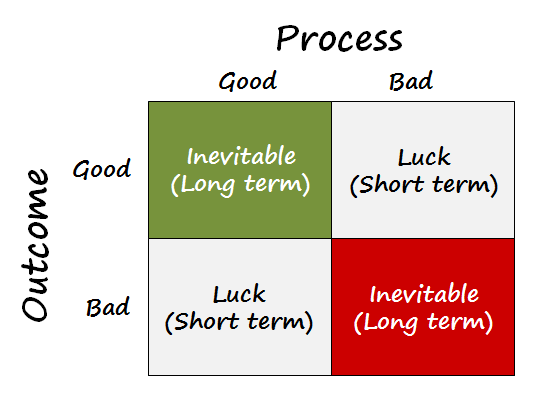

You should first focus on the path/process that was followed to achieve the outcome. A good process ensures a good outcome over long term. The following matrix is helpful in understanding the importance of ‘good process’ in decision making.

In Investing

As Taleb writes in his book –

…in time, if the roulette-betting fool keeps playing the game, the bad histories will tend to catch up with him. Thus, if a twenty-five-year-old played Russian roulette, say, once a year, there would be a very slim possibility of him surviving until his fiftieth birthday – but, if there are enough players, say thousands of twenty-five-year-old players, we can expect to see a handful of (extremely rich) survivors (and a very large cemetery).

If you draw a parallel to this in the stock market, in a field populated by thousands of traders, speculators, and people buying stocks on leverage, at the end of a say 10-15 years, you may still find a very few lucky survivors, but there will also be a very large cemetery (of those who destroyed wealth using the same routes).

Sometimes, people are indeed aware of the risks inherent in Russian roulette kind of investing, and they still do it. However, the quality of money earned this way (a stressful process) is not the same as the one earned by non-fatal means like sensible, patient, long-term investing without borrowing other people’s money (stress-free process).

Of course, in the end, you may earn a similar amount of money either ways – through day trading, speculation, and leverage OR patient, long-term investing – but the former’s dependence on randomness is greater than the latter’s.

To the accountant, they would be identical; to your next door neighbour too. Yet, deep down, you know that they are qualitatively different.

As an investor, you may want to minimize the heart-wrenching rides that you may experience during the course of investing period. This is how Prof. Sanjay Bakshi concluded in his article on “Return per unit of stress” –

“My advice to those who ignore the stress part of the equation but focus only on returns per unit of risk: You cannot take it away with you, so what’s the point of all that stress, just for the money?”

The legendary Howard Marks wrote this in one of his memos to shareholders in 2006…

In the investing world, one can live for years off one great coup or one extreme but eventually accurate forecast. But what’s proved by one success? When markets are booming, the best results often go to those who take the most risk. Were they smart to anticipate good times and bulk up on beta, or just congenitally aggressive types who were bailed out by events? Most simply put, how often in our business are people right for the wrong reason?

The people Marks is referring to are the ones Taleb calls “lucky idiots,” and in the short run it’s certainly hard to differential between them and skilled investors.

Here is what Marks wrote in a 2002 memo…

I find that I agree with essentially all of Taleb’s important points.

- Investors are right (and wrong) all the time for the “wrong reason.” Someone buys a stock because he or she expects a certain development; it doesn’t occur; the market takes the stock up anyway; the investor looks good (and invariably accepts credit).

- The correctness of a decision can’t be judged from the outcome. Nevertheless, that’s how people assess it. A good decision is one that’s optimal at the time it’s made, when the future is by definition unknown. Thus, correct decisions are often unsuccessful, and vice versa.

- Randomness alone can produce just about any outcome in the short run. In portfolios that are allowed to reflect them fully, market movements can easily swamp the skillfulness of the manager (or lack thereof). But certainly market movements cannot be credited to the manager (unless he or she is the rare market timer who’s capable of getting it right repeatedly).

- For these reasons, investors often receive credit they don’t deserve. One good coup can be enough to build a reputation, but clearly a coup can arise out of randomness alone. Few of these “geniuses” are right more than once or twice in a row.

- Thus, it’s essential to have a large number of observations – lots of years of data – before judging a given manager’s ability.

Invert, Always Invert!

Although Survivorship Bias is a serious cognitive bias and leads to erroneous decision making, I believe it can be used for our benefit also. Using the idea of inversion, let me make an attempt to find a useful way to exploit this bias.

It’s actually a nice little hack related to the concept of alternative history. I frequently use this imagination trick to increase the quality of my day to day life.

Right now I am sitting on a comfortable chair, writing on my laptop while sipping an organic tea. But there is another possible path that history could have taken. In that alternative path, I imagine being born in a poor African country where (forget internet or even electricity) one has to walk 5 miles every day to fetch drinking water.

Thinking about this alternative history forces my mind to be grateful for all the blessings that are present in my life right now. After all alternative histories aren’t just about Russian roulettes and investing.

Conclusion

Warren Buffett’s appendix to the fourth revised edition of The Intelligent Investor describes a contest in which each of the 225 million Americans starts with $1 and flips a coin once a day. The people who get it right on day one collect a dollar from those who were wrong and go on to flip again on day two, and so forth. Ten days later, 220,000 people have called it right ten times in a row and won $1,000.

Buffett writes, “They may try to be modest, but at cocktail parties they will occasionally admit to attractive members of the opposite sex what their technique is, and what marvellous insights they bring to the field of flipping.”

After another ten days, we’re down to 215 survivors who’ve been right 20 times in a row and have each won $1 million. They write books titled How I Turned a Dollar into a Million in Twenty Days Working Thirty Seconds a Morning and sell tickets to seminars.

“Worse yet,” Buffett writes, “they’ll probably start jetting around the country attending seminars on efficient coin-flipping and tackling skeptical professors with, “If it can’t be done, why are there 215 of us?”

If you don’t know how to separate a good process from a bad one, you’ll surely fall for these ‘efficient coin-flipping’ wizards.

Learn to focus on the process more than the outcome. Use common sense and your own thinking to filter out the outcome-centric hindsight-heavy theories.

Take care and keep learning.