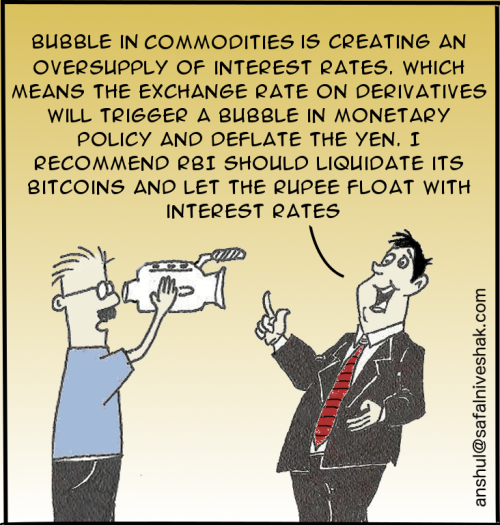

Open any financial news channel and often you can find a so called expert being interviewed on his opinion about the direction of the stock market and health of the economy.

On being asked such macro questions, the answer usually goes something like this –

Maybe the gentleman above has a point. But I just don’t see it. Do you? All I see is that his verbal diarrhea was completely useless.

In most cases, the right (and honest) answer is – I don’t know.

But how can experts not know? They are interviewed because they’re supposed to know about everything. And even if they don’t know, what is Google for? All the facts and figures are few key strokes away, so it’s a sin to not have an opinion about everything, especially if you’re considered an expert and probably being compensated by pay per word.

So does it mean you are entitled to have an opinion on a subject just because you know a lot of facts and figures about it?

The more books I read, bigger is the realization that “I don’t know” is usually the most honest answer and also the toughest one, more so if the questions are about complex world around us.

Then why is it that we find it so hard to acknowledge our ignorance?

I don’t know the answer to that but my guess is that saying “I don’t know” puts the human ego at risk, and to avoid looking like fools, people end up talking something which usually is crap.

That reminds me of this quote from Plato –

Wise men speak because they have something to say; Fools because they have to say something.

This ‘need to say something’ when one doesn’t have anything useful to say is what Charlie Munger dubs as Twaddle Tendency.

The word ‘twaddle’ means a speech or writing that is silly, trivial, pretentious and not true. In other words – nonsense.

Twaddle tendency is the smoke screen created by shallow thinkers to hide their ignorance. The unnecessary jargons and pompous language is used to disguise the intellectual laziness and half-baked ideas.

Sometimes this trick works, but only for a short while. And many a times this twaddle tendency is so obvious that it’s embarrassing. See what happened with this girl who ended making a big fool of herself.

Click here to watch the video.

It wasn’t her ignorance about the subject but her unwillingness to say, “I don’t know” that put her into real trouble. She felt she had to say something smart so she just twaddled.

Like other behavioural biases, this tendency is also tattooed deep into human behaviour and probably evolution is the culprit behind this. Often, if the person is not prepared to answer he or she will simply make something up instead of saying nothing at all.

Recently I met an accomplished value investor and asked his feedback about how to make Safal Niveshak more valuable for its readers. Instead of falling for the Twaddle Tendency and make up something, he did the most honest thing.

He said, “I can’t give you an answer off the cuff. Let me think about it.” It’s rare to find people like that.

According to Munger, people waste a lot of time talking about meaningless stuff which then leads to equally meaningless activities.

In Poor Charlie’s Almanack, Charlie Munger describes an interesting experiment …

A trouble from the honeybee version of twaddle was once demonstrated in an interesting experiment. A honeybee normally goes out and finds nectar and then comes back and does a dance that communicates to the other bees where the nectar is. The other bees then go out and get it.

Well some scientist, clever like B. F. Skinner [perhaps Charlie’s favorite scientist], decided to see how well a honeybee would do with a handicap. He put the nectar straight up. Way up. Well, in a natural setting, there is no nectar a long way straight up, and the poor honeybee doesn’t have a generic program that is adequate to handle what she now has to communicate.

You might guess that this honeybee would come back to the hive and slink into a corner, but she doesn’t. She comes into the hive and does an incoherent dance. Well, all my life I’ve been dealing with the human equivalent of that honeybee. And it’s a very important part of wise administration to keep prattling people, pouring our twaddle, far away from the serious work.

In 1998 Wesco meeting, Charlie added …

I try to get rid of people who always confidently answer questions about which they don’t have any real knowledge. To me they are like the bee dancing its incoherent dance. They are just screwing up the hive.

Twaddle is perhaps harmless for the twaddler (if there is such word) except that he loses respect in the eyes of wise people. But if you’re at the receiving end and your bullshit filter isn’t strong enough to separate the twaddle from real talk, then you run a risk of not only wasting your time hearing the trash talk but may also end up losing your money and resources.

In fact, most of the talking heads on financial TV (even the non-financial ones) are dishing out twaddle.

Charlie Munger is quite fond of the word and has used it at multiple occasions.

It’s obvious that if a company generates high returns on capital and reinvests at high returns, it will do well. But this wouldn’t sell books, so there’s a lot of twaddle and fuzzy concepts that have been introduced that don’t add much.

~ Charlie Munger, WESCO annual meeting, 2000

I think the notion that liquidity of tradable common stock is a great contributor to capitalism is mostly twaddle. The liquidity gives us these crazy booms, so it has as many problems as virtues.

~ Charlie Munger, BRK Annual Meeting, 2004”

At Farnam Street, Shane Parrish writes…

While we all hold an opinion on almost everything, how many of us do the work required to have an opinion?

The work is the hard part.

You have to do the reading. You have to talk to anyone you can find and listen to their arguments. You have to think about the key variables that govern the interests. You have to think about your biases and incentives.

You have to think not emotionally but rationally.

And you need to become your most intelligent critic. Part of doing that means you need to have the intellectual honesty to kill some of your best loved ideas.

Only then, when you can argue better against yourself than others can you hold an opinion.

After you’ve done that, after you’ve done the work, that is the time you can say “Hey, I can hold this view, because I can’t find anyone else who can argue better against my view.”

Simply regurgitating facts and anecdotes doesn’t add any value to an argument. Unless somebody has struggled with an idea and spent some mental energy thinking about it, his or her knowledge is pretty superficial, second hand and precursor to a twaddle.

Munger says, “I never allow myself to have an opinion on anything that I don’t know the other side’s argument better than they do.”

Unless one qualifies Munger’s test to have an opinion, whatever he or she speaks on a subject, especially with overconfidence, is possibly just twaddle.

In his book The Art of Thinking Clearly, Rolf Dobelli summarizes the idea very well …

Verbal expression is the mirror of the mind. Clear thoughts become clear statements, whereas ambiguous ideas transform into vacant ramblings. The trouble is that, in many cases, we lack very lucid thoughts. The world is complicated, and it takes a great deal of mental effort to understand even one facet of the whole. Until you experience such epiphany, it’s better to heed Mark Twain: ‘If you have nothing to say, say nothing.’ Simplicity is the zenith of a long, arduous journey, not the starting point.

So how do you identify a twaddle?

Whenever you hear a talk or read a statement with signs of overconfidence, colored with hindsight bias, suggesting anecdotal evidences, predictions about unknowables, and high sounding complicated jargons, you can be pretty sure that the person is either lying or mad and possibly both.

Having a latticework of mental models greatly helps in filtering out the balderdash thrown at you. Multidisciplinary thought process helps you build a strong bullshit filter.

I don’t know who said this but there is some degree of truth to this statement –

Unsolicited advices are like armpits. Everyone has one and they stink.

Based on my personal experience I know when something needs to be ignored – when somebody pulls me aside and gives a free and especially an unsolicited advice.

Here’s how Elon Musk cuts through the twaddle when he is recruiting people …

When you struggle with a problem that’s when you understand it…when I interview people, I ask them to tell me about the problems that they worked on and how they solved them. And if someone is really the person who has solved it then he would be able to answer it at multiple levels…if they aren’t then you can say ..oh! this isn’t the person who really solved the problem. Because anyone who struggles hard with a problem, never forgets it.

It’s amazing how quickly you can find somebody’s edge of knowledge. Just ask why a couple of times and you can see how deeply that person has thought through the problem or issue. That’s what Musk means by ‘multiple levels’.

And do you know the most dangerous form of twaddle? It’s the one which you tell yourself.

Because the easiest person to fool is always yourself, says Richard Feynman.

So keep asking WHY from yourself. This simple trick will accelerate your learning like anything.

Take care and keep learning.

Update: Our tribe member, Ankit Kanodia, shared an example of annual report containing twaddle. You can download the annual report from here. Check out page 16. The company, Sanwaria Agro Oils Limited, refers to itself as Dabur. It’s not just a copy paste blunder, but shows how little thought they have put into their most important communication letter.

There are not so many people who know the art of time management well. However, all people want to be productive. In short, being a productive person means to complete tasks faster without sacrificing the quality. Obviously, it is a great thing to learn, but we all reduce our productivity in different ways, even without knowing that. If you are interested in increasing your productivity (but not reducing), read on… #1. Sleeping Many people believe that waking up earlier (or going to sleep later) is a key to success, as they might have more time to complete their tasks. Some workers sleep 4-5 hours per night to be able to work more. In fact, having a healthy sleep (around 7-9 hours per night) helps you […]

There are not so many people who know the art of time management well. However, all people want to be productive. In short, being a productive person means to complete tasks faster without sacrificing the quality. Obviously, it is a great thing to learn, but we all reduce our productivity in different ways, even without knowing that. If you are interested in increasing your productivity (but not reducing), read on… #1. Sleeping Many people believe that waking up earlier (or going to sleep later) is a key to success, as they might have more time to complete their tasks. Some workers sleep 4-5 hours per night to be able to work more. In fact, having a healthy sleep (around 7-9 hours per night) helps you […]