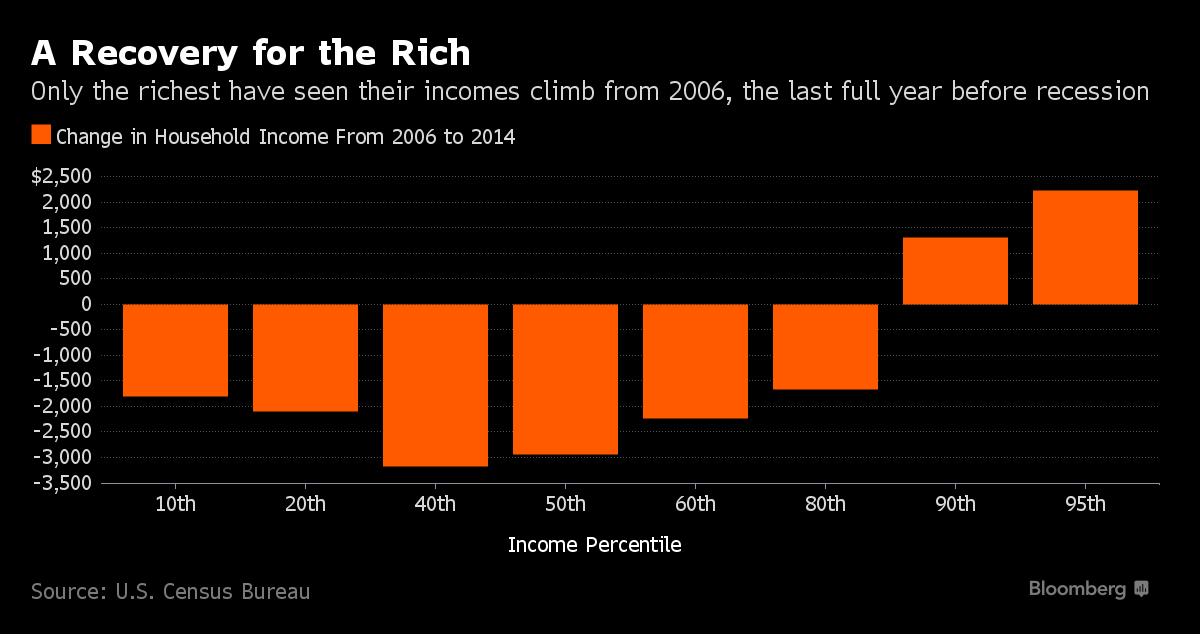

I clearly remember the day, it was in July 1999, when I was first introduced to the internet. I was so excited to get a brand new email address. I could now send and receive emails.

However, the excitement didn’t last very long. I quickly realized that the email address wasn’t of much use to me because none of my family or friends had any email addresses at that time. Who would I mail?

But slowly as more and more people started using internet, my email address became increasingly valuable.

Similarly, I remember the time when the social networking bug bit me and I signed up for Orkut. But within few years when all my friends had moved to Facebook, I was forced to abandon Orkut and climb on the Facebook bandwagon.

So you’d notice that the utility of certain products and services is directly proportional to its number of users. Another recent example that comes to mind is the social messaging app Whatsapp. There are quite a few other messaging services which offer better features than Whatsapp but majority of people continue to use Whatsapp because all their friends are on Whatsapp.

This is called Network Effect. Now the idea may sound very simple, but it’s actually fairly unusual.

When you board an airplane, do you get excited when you see that the flight is completely full? Or when you visit your favourite restaurant, do you prefer it to be crowded? In these cases, as a consumer you don’t get any benefit if the product or service is also being used by others.

But when it comes to social networks like Facebook, Linkedin and Twitter, members join these networks because other members are in this network.

These are the businesses that benefit from the network effect. The value of their product or service increases with the number of users. When network effects kicks in people feel compelled to use it, or are forced to use it because of its popularity.

For instance Microsoft Word is more commonly used because it’s packaged with Windows and comes free with windows PC. Since so many businesses and individuals utilize Word, their customers and suppliers are compelled to have it as well. The network effect leads to positive feedback in which the product’s presence in the market increases.

It’s not that Microsoft Office doesn’t have a competitor. “OpenOffice” offers almost all the features of MS Word and it’s free. In spite of that it hasn’t been able to make any dent to MS Word’s market share. Because of minor issues related to compatibilities between OpenOffice and MS Word, people just don’t bother using OpenOffice.

Bob Metcalf, the inventor of ethernet, stated that if there are ‘N’ people in a network, and the value of the network to each of them is proportional to the number of users, then the total value of the network (to all users) is proportional to N*(N-1).

If the value of a network to single user is Rs.1 for each other user on the network, then a network of size 10 has a total value of roughly Rs. 100. In contrast, a network of size 100 has a total value of roughly Rs 10,000. A tenfold increase in the size of the network leads to a hundredfold increase in its value.

Which means, as the network grows, the rate of growth of the network value (represented by number of connections between different nodes) is faster than the rate of growth of network (represented by number of nodes in the network).

The image below illustrates the ideas very well.

(Source: Little Book That Builds Wealth by Pat Dorsey)

Not all connections in a network are equally meaningful and valuable but it’s fair to say that the value of a network to its users is more closely tied to the number of connections than it is to the number of nodes.

A market can sustain only few network for a given kind of product or service. You don’t find many social networking sites out there. Facebook, Twitter and LinkedIn pretty much dominate the industry. In fact Orkut, in spite of having the first mover advantage, had to shut down when it was squeezed out by Facebook.

So we can say that network based businesses tend to create natural monopolies and oligopolies.

Look at the world of credit card networks. It’s dominated by VISA, Mastercard and Amex. That’s a huge amount of market concentration. The barrier to entry in this industry is a result of network effect. Even if a competitor showed up on the scene next week, it has to first convince millions of merchants to accept the new card which require the competitor to first have millions of customer using the new card. In simple words it’s classic catch-22 problem for any new player to enter this market.

“A competing firm would need to replicate the network —or at least come close”, says Pat Dorsey, author of wonderful book The Little Book That Builds Wealth, “- before users would see more value in the new network and switch away from the existing one.”

Talking about common characteristics shared by businesses having network effect, Dorsey writes –

…you’re most likely to find the network effect in businesses based on sharing information, or connecting users together, rather than in businesses that deal in rival (physical) goods…this is not exclusively the case, but it’s a good rule of thumb.

That means you’re more likely to find the network effect in businesses which are heavy on technology. So businesses like eBay come out like text-book examples of network effect. Dorsey writes in his book –

As of this writing, eBay had at least an 85 percent share of Internet auction traffic in the United States…The buyers are on eBay because the sellers are there, and vice versa.

Even if a competing site were to launch tomorrow with fees that were a fraction of eBay’s, it would be unlikely to get much traffic—no buyers, no sellers, and so forth. And the intrepid first users wouldn’t have the benefit of eBay’s feedback ratings, telling them which other users they can trust to fulfill a transaction, nor could they be assured of getting the best price, given the paucity of other users. (I once asked a candidate applying for an analyst job at Morningstar what he would do if I played venture capitalist, gave him huge amounts of financial backing, and told him to go beat eBay at its own game in the United States. He thought for a minute and then replied, “I’d return the money.” Good answer.)

Similarly, in e-commerce space it’s almost impossible to displace Amazon from its position. It’s not just the network of buyers and sellers but imagine the immense value that the accumulated information about product ratings and reviews creates for the buyers. The product reviews on Amazon are tremendously useful for the buyers to make purchase decisions. And bigger the network of buyers and sellers grows, bigger is the value of the whole Amazon platform.

Once a certain critical mass is achieved the network effect starts riding on positive feedback loop and this self reinforcing virtuous cycle creates a winner-takes-all scenario.

Network effect can be seen in newspaper business also. More readers for newspaper attracts more advertisers and hence more valuable it becomes for the readers as a source of information about new products and services.

Warren Buffett wrote in his 2006 letter –

Advertisers preferred the paper with the most circulation, and readers tended to want the paper with the most ads and news pages. This circularity led to a law of the newspaper jungle: Survival of the Fattest.

Thus, when two or more papers existed in a major city (which was almost universally the case a century ago), the one that pulled ahead usually emerged as the stand-alone winner. After competition disappeared, the paper’s pricing power in both advertising and circulation was unleashed. Typically, rates for both advertisers and readers would be raised annually – and the profits rolled in. For owners this was economic heaven.

MCX, the multi-commodity exchange in India, which accounts for more than 85% of total value traded in the Indian commodity futures markets (2013), is another business which benefits from network effect. As more buyers and sellers utilize the MCX, the alternative exchanges become less attractive in terms of pricing and liquidity.

Another example is Info Edge, where the key business of Naukri benefits from a virtuous cycle –

Network effect is an important attribute to look for while evaluating the presence of economic moat, a metaphor for durable competitive advantage, in a business.

Network effect, according to Pat Dorsey, is an important sources of structural competitive advantage. The other being switching costs, cost advantage and intangible assets.

So if you can find a company with solid returns on capital and a presence of network effect in its business, you’ve likely found a company with a moat. In fact network effect and switching costs are related because network effect creates a switching costs for the consumer.

Here’s an interesting insight about Tesla Motors.

I am guessing that Tesla Motors are also on their way to creating a very strong moat using network effect. Like Google’s driverless cars, Tesla is also working on self-driving cars (it’s available as part of the latest software upgrade for Tesla cars). As thousands of Tesla electric cars are being driven around, each car is charting the roads. So each Tesla automobile effectively becomes a data gathering agent. The data is sent to Tesla (every car is connected to central Tesla server for downloading upgrades to its software) which helps in mapping the roads around the world.

Watch this video where the driver talks (at 5:20) about this feature.

As more and more people use Tesla and longer they use it, the data about geography (the road quality, unexpected curves on the road, real time traffic conditions, even proximity with rash drivers etc) will benefit the Tesla owners to rely more and more on the autopilot.

This looks like a moat in creation. The more robust the Tesla’s geographical data becomes, more the value of Tesla vehicle for the users. The more users drive Tesla cars the bigger and better Tesla’s data.

Isn’t this a network effect?

I am not sure if this is an intentional move by Elon Musk but if it is, then any other electric car company will find it very tough to replicate this competitive advantage.

Conclusion

So we have seen how network effect can create an extremely powerful competitive advantage. It’s a very powerful type of economic moat that can lock out competitors for a long time.

The great scientist Isaac Newton once said, “If I have seen further than others, it is by standing upon the shoulders of giants.”

By learning the big ideas from multiple disciplines and developing a latticework of mental models, we are allowing ourselves to stand on the shoulders of giants. People who have come before us and developed useful ideas in different subjects have already done the groundwork required for improved thinking. What remains to be done on the path to worldly wisdom is to learn these ideas, master them and begin using them in our decision making process.

The first and foremost beneficiary of this Latticework series is me. So do let me know what other mental models would you like to learn together.

Take care and keep learning.