Chaitanya Patel

Shared posts

Mark Tully’s views on Modi’s India…

Legislating is just not enough

More on the solar bubble

A yieldco is a growth-oriented publicly traded corporation formed to hold operating assets that generate long-term, low-risk cash flows. The cash flows are distributed to investors as dividends. Corporate level tax is shielded in whole or in part by the developer's retained share of accelerated depreciation and, in some cases, tax credits, and may also be offset by interest deductions on project acquisition debt. Additionally, yieldcos tend to attract investors that may be tax indifferent, such as tax-preferred pension plans. Because the yieldco sponsor is a developer, yieldcos usually have access to the developer's project pipeline through a right of first refusal. This provides the developer with a ready repository for its completed projects to replenish its capital and gives the yieldco the promise of growth...Yieldcos have drawbacks, including the high cost of an IPO and the need to keep acquiring projects to maintain cash flows and stock value... because they are publicly held, the public yieldco structure does not permit the most nimble decision-making processes.Apart from the risks associated with such financing engineering, large solar developers may be expanding far faster for their own good. SkyPower, another one of the large investors in India, has very aggressive plans to enter other markets too. They include large investments in Panama and Kenya. These are doubtless risky investments with very high likelihood of lack of complementary (mostly public) investments and potential failures.

Finally, especially in the US, the industry has thrived on the back of fiscal incentives - income tax credits and accelerated depreciation - which helped leverage tax-equity financing. Such incentives, while essential to catalyze the development of a market, may not be the most efficient way of financing post-maturity market expansion.

On the positive side, solar plants, unlike roads and thermal power plants, have smaller construction periods and can start generating revenues pretty quickly. But this is critically dependent on the availability of land and evacuation facilities.

37 years of performance: Sensex, Fixed Deposits, Gold and Silver

For the last 5 years, I’ve made it a practice to give performance comparison of various asset classes: Sensex (Equity), Fixed Deposit (Debt), Gold and Silver and the impact of inflation on them beginning from the financial year 1979-80. Why 1979-80? That is the year from which Sensex came into existence with base as 100.

Please find attached 3 files

a) 37 years return- FD & Sensex

b) 37 years return- Gold & Sensex

c) 37 years return- Silver & Sensex

1) Assume you’ve invested Rs.1 lakh each in FD, gold, silver and Sensex 37 years ago. As of 31’st March 2016 the value is as follows- FD: Rs.19.75 lakhs, Gold: Rs.36.53 lakhs, Silver: Rs.24.46 lakhs and Sensex: Rs.2.53 crores.

2) Unlike other assets mentioned above, Sensex has dividend yield in addition to capital growth. Assuming a dividend yield (duly reinvested) of 2% on an average, the Sensex return works out to Rs.4.76 crores.

3) To put it another way, during last 37 years:

Fixed Deposits has multiplied wealth by 20 times

Gold by 37 times

Silver by 24 times

Sensex by 253 times

4) In terms of percentage, the 36 years return (as given above) is as follows- FD: 8.39%, Gold: 10.21%, Silver: 9.02% and Sensex: 16.13% (18.13% if dividend yield is as assumed above)

5) When we talk about returns, we’ve to talk about inflation too. The average annualized inflation for the above period is 7.67%.

6) If Rs.1 lakh has been kept under the mattress instead of being invested, it’s value has come down to mere Rs.5208 (i.e.) purchasing power of rupee reduced by whopping 95% over 37 year period.

7) What we should look for is real returns (i.e.) returns after inflation and taxes. Since tax differs from each asset class and income category, I’ve taken only inflation and excluded taxation. Inflation is common for all.

8) After adjusting for inflation, the asset classes have grown by following annualized rate in real terms– FD: 0.72%, Gold: 2.54%, Silver: 1.35% and Sensex: 8.46% ( 10.46% including dividend yield). These numbers matter a lot. This is what our wealth would have grown after adjusting for inflation. Since we know the tax details for each asset class and for our income, we can work out the return after taxes too. FD would automatically turn negative. Gold and Silver would have provided a negligible return. Only equity would have provided a real rate of return of around 9%.

9) Gold’s real rate of return of 2.54% is made possible due to rupee significantly depreciating between 1980s to early last decade. Otherwise we might have got even a negative return; as globally gold fell by around 70% during the above period. I’ll explain this by example. Assume the rupee dollar conversion rate is 1 USD = Rs.65. For illustration purposes, let us assume the price of 1 gram of gold is 1 USD. With the above conversion rate, the value of 1 gm of gold is Rs.65. Imagine a scenario when rupee depreciates by 100% (i.e.) 1 USD = Rs.130. The gold price remains the same at 1 USD. The value of our gold would increase by 100% to Rs.130 though the price has not changed in the international markets and we being the net importer of gold.

10) Please use FD for contingency or emergency funds. Let gold be part of social requirement and not exceed 5% to 10% of investment portfolio. Silver is again part of only social or cultural needs. Equity is for building wealth.

11) Real estate would normally give returns better than fixed deposits but lesser than equity. There is no reliable long term data available for real estate. From what I understand from reading, in the long run, real estate can be expected to give 2% to 3% more than inflation. If inflation is 6%, we may expect a long term price growth rate of around 9%. By providing 16% for nearly 4 decades, equity has scored well over real estate.

12) Please go through the workings and assumptions in the attached files. I’ve tried my best. It may not be perfect but would be a useful pointer. Request your opinion and feedback.

The gains from sound macro and finance policy

Israel went through a complete transformation of macro and finance policy. They started out pretty bad, and put in all the key machinery : inflation targeting, floating exchange rate, open capital account, modern financial regulation, public debt management, etc.

A graph of the nominal yield curve for government borrowing is quite revealing [source]. It superposes the yield curve prevalent at many dates:

The curve at the top is the yield curve in October 1996: it goes out to only 3 years, and features nominal rates of 16 to 17%.

Through the years, as the macro and finance reforms fell into place, nominal interest rates for borrowing went down, and the maturity went up. By January 2012, inflation had stabilised at the target of 2%, the short rate was 1.5%, and the 30 year rate was 5.51%.

Note that the 2012 situation is without financial repression and without capital controls. Private persons voluntarily choose to lend to the government, for a 30 year horizon, at 5.51%. There are no other distortions in the picture. This is the `fair and square' cost of borrowing for the government.

This shows the the direct gains to the fiscal authority from doing the orthodox approach to macro and finance policy. Similar large gains became available to the private sector, as corporate bonds and bank loans are expressed as credit spreads off the government bond interest rates. We in India will get these gains by enacting and enforcing the Indian Financial Code.

Cost of financial planning services

Year end review

From the beginning, we’ve been sending your portfolio summary along with our review in the month of April. This would be for the financial year ended March 31’st. This is the only time we want you to see the portfolio. Frequent watching of portfolio may lead to impulsive unwanted decisions. I’m aware that not all of you listen to this piece of advice. It would be in your own interest if you can follow the same.

Sensex as on March 31’st 2015: 27,957

Sensex as on March 31’st 2016: 25,341

Sensex has fallen by 9.35% over last one year. It has been a hugely volatile year. Markets lost heavily in January and February, only to recover again in March.

Watching markets every other day would have been an emotional roller coaster ride. Seeing it once a year is good for your peace of mind and wealth.

In next couple of days, we would be publishing the comparison of asset classes since 1979-80 (the year in which the Sensex was formed). We’ve been doing this exercise for last 5 years and you’ve asked us to repeat the same at the end of every financial year. We are happy to oblige.

From 1979-80 to 2015-16; for the last 37 financial years, Sensex had 25 positive years and 12 negative years. So 68% of the time it is positive. You’ll have more positive years than negative years.

You all have committed a minimum period of 10 years for SIPs and for many of you the investment tenure is running into decades. You are betting on the future of India, its economy and companies. We are in for a huge growth in the coming years and decades and you would all be winning in your bet.

So be confident and continue to stay the course. We foresee good growth for the markets in next few years once the earnings pick up.

We plan to complete sending the year end portfolio reports latest by end of April. If you don’t receive the same by then, please let me know.

I share with you one of my favourite quotes of John Bogle in the year end reports. I want to share it this year even before sending the reports.

“Stay the course. No matter what happens, stick to your program. I’ve said ‘stay the course’ a thousand times, and I meant it every time. It is the most important single piece of investment wisdom I can give to you.”

All the best.

Carl Braun on Communicating Like a Grown-Up

“Man is a gregarious animal. We work in herds, in teams. The bear can do exactly as he pleases, for he works alone. We do not work alone. We depend throughout our lives on the goodwill of other men. If a man does not learn to bend, to be friendly and considerate, and to respect his brother’s ego—in things both big and little—he’ll find himself disliked and locked up in his own unhappiness.”

— C.F. Braun

***

Carl Franklin (C.F.) Braun graduated from Stanford with an engineering degree in 1907 and within two years had opened his own engineering firm. Braun’s company would go on to manufacture and engineer products ranging from water filters to petroleum processing plants; large, complicated projects involving manpower and precision. He eventually employed 6,000 people and built over 250 petrochemical plants, well respected as the leader in his field for many years.

Braun had a unique corporate policy: If you were going to issue a directive, you had to tell the person Who, What, When, Where, and most importantly, Why someone was to do it. So strong was his belief in using why, it was said that Braun could fire you on the spot if he found you not issuing reasons. Many years later, Charlie Munger would come to sing Braun’s praises for this approach to Reason-Respecting Tendency.

One of Braun’s approaches to maintaining a productive corporate environment was by writing and issuing short books to all of his employees. They had barn-burning titles like Letter Writing in Action, Corporate Correspondence, and Presentation for Engineers and Industrialists. They’re all out of print, but you can find them if you look. And look we did.

One of my favorites is called Fair Thought and Speech; it’s a short primer on how to communicate in an organization in a way that gains and keeps respect and gets people to go along with good ideas and work together productively. It’s a simple idea, but Braun lays out the task:

Why don’t I get along better? I know my work. I know how to present things clearly and logically. I work hard. And yet, something holds me back. This is the quandary of many and many a capable man. The answer too often is that he lacks a generous and kindly way of thinking, a considerate and objective view, and a friendly way of writing and speaking.

There’s more here than meets the eye. Braun saw the way a man communicated as reflective of how he thought.

Get a man to write and speak more objectively, and you get him to think more objectively. Braun was focused, above all, on what worked. He needed to get complicated oil refineries built, and built well. He was also an astute student of human nature, and that comes across in his writing. It’s the simplest and most straightforward writing style imaginable; short, declarative statements one after another. (He studied his Strunk & White.) But he’s also witty and to the point, which is enjoyable to read.

These are really a guide to communicating and working with others like a mature grown-up. Like a man. Like a woman. Not like a petulant child, which we all do at times.

We won’t reprint the whole of the book here, but here are some of our favorite dictums from Braun. I try to look them over once in a while and see which ones I’m committing most frequently.

Assume Good Motives

No matter how clear and fair a case may seem to us, somebody is apt to disagree. And this is good, for we need the stimulation of disagreement. Let’s question his information, his reasoning, his conclusions — but never his motives. If we start assuming or imputing ill motives, we lose all chance of influencing our listener. But even worse, we degrade ourselves.

Remind, Not Tell

Even if we are sure somebody had overlooked a bet, or is overlooking it, let’s tender our advice as though we are reminding him of something that he had intended to do, but that something else has crowded out. Let’s lean over backwards in giving to others the credit for ideas. This is the generous thing. It’s the thing that wins respect, both for us and for our ideas.

Put Error to Work

But let’s never, never, cover up error with the misguided thought that we must protect someone — either our brother, or our department, or our own pet ego. The recognition of error and its examination, if openly talked of, is a sure way to avoid its being repeated, either by the same man or by others. Everyone errs at one time or another. The Company pays for it. Okay. But the Company should not have to pay twice. Nor should other men be denied the benefit of warning-signs.

Overt Respect

In all this matter of respect for others, of consideration, tolerance, interest, it is not enough that we feel these things. They cannot be effective if we carry them about locked up within us. We must plainly show them in word, in expression, in countenance, in bearing, in act. We cannot help others, encourage them, or be understood by them, or get willing help from them, if we leave them to guess at our thoughts and intentions.

Invite Acceptance

If we want our opinions or beliefs to be accepted, the worst thing that we can do is to press too hard for them, or to make a personal issue of them. Better not crowd for acceptance, but rather invite it. Better tender our advice with a softening It seems to me. Or an It appears. Or a Perhaps. Or with some similar concession to the ideas of our listener. True, there are times when we must speak as authorities in no uncertain terms. Even then, reasonable humility is seldom amiss.

Easy Does It

If we want to observe how others feel about being rushed, or crowded, or pushed into a corner, just look at a pet of any kind, or at a child. Try to make friends with one of these by being forceful, abrupt, intense. The child will run. The dog will bristle. The cat will jump up on a rafter. Better place yourself or your wares where they can be seen. Then lay off. Give interest, curiosity, and natural friendliness, a chance to work.

Grudging Assent

And when we do give assent (to others), let’s give it cheerfully. No moaning because we lost out. No suggesting that other people are unreasonable, or that they do not understand us. No intimating that we are merely out-argued. We had our fair chance to speak up like a man. No hinting, then, that we merely bow to higher authority. We must all bow to higher authority — to weightier considerations perhaps, or to expediency, or to public opinion, or to our client. If we are stiff-necked about it, we are on the road to ruin.

Writing for the Record

Some men have an irresistible desire to justify their every action. Some like to magnify themselves. Others like to provide an alibi ready for use if needed. Some, perhaps, just don’t think. In any event, they write a letter to some other department or to the boss. The letter first tells how much the writer or his group are doing. Then it puts the finger on others. Just write a few letters like this with plenty of copies sent around, and you’ll dig a grave you’ll never get out of.

Unwise Citing

We have all been approached at some time or other by the Unwise Citer. He asks us to take some action, or refrain from one, solely because certain other people have done so under supposedly like circumstances. The citer, lacking good arguments, has sought to substitute secondhand opinions. This is unfair. It is not helpful. And it directly assaults our ego. We are not given credit for having brains and judgment of our own. Bad stuff.

Air of Prejudice

We don’t have to use words, either, to be unfair. Did you have to sit in court and listen to a prejudiced witness? He’s too intense. He’s too vehement. Quite evidently, he’s not satisfied with stating the facts as he knows them. No, sir! He’s out to prove the other fellow wrong. Result — nobody pays attention to him. Well, let’s be sure when we sit around a conference-table, we’re not like him. Better state our facts clearly, or our views. But let’s not be too anxious. Let’s not try to push either judge or jury. It doesn’t work.

Negation

We all know the chap who is quick to tell us when we are wrong. He probably doesn’t know too much about the subject himself, and hasn’t the confidence to take a positive position. His ego prods him into a negative one. He corrects us with great assurance on the tuning of radios, on the eating of spinach, on other matters of opinion. Let’s feel sorry for his difficulty with his ego. But let’s be sure first, that we’re not perhaps a wee bit like him. We always are.

Refinement

A somewhat more subtle form of negation, is refinement of measurement. One man says that a tank weights ninety tons. And for that particular discussion, accuracy is of no consequence. Yet someone’s ego speaks up and says, Ninety-two tons. Maybe he’s right at that. But he’s wrong just the same. […] This is a favorite husband-and-wife game. Let’s be on guard against it.

Claim-Jumping

One irritating form of pretending is that of claiming priority. Someone suggests a desirable precaution, or action, or change. Up jumps our ego. We had thought of that, we say. We’d intended to do it tomorrow. Maybe we had. Maybe we hadn’t, though — for our imagination at times plays strange tricks on us. In any event, we didn’t come up with it first. We’d better keep quiet, or we’ll surely be suspected of bluffing.

Repetition

Here is an easy trap to fall into. Someone comes out with an idea. It sounds good to us. Our ego grabs hold of it, dresses it in slightly different language, and puts the idea out as our own. We act as though we’d independently arrived at the same conclusion. Maybe so, maybe not — for we cannot trust our memories as to when we first thought a thing, or what it was that started the train of thought. Let’s restrain our egos from grabbing credit. All we wind up with is discredit.

All-Knowing

The worst trick our ego can play on us, is to demand that we know everything. Let’s discipline ourselves until it’s easy to say, I don’t know. And let’s keep out of discussions when they’re on subjects outside of our recognized sphere. Our lack of real knowledge and experience is bound to display itself, and bring resentment from those who are really qualified to speak. Let’s slap our ego down whenever it starts laying claim to knowledge that’s too various.

Don’t Beg

Another thing. Don’t beg. People don’t like it. If then we speak up for some better job that’s open, let’s not till our talk with such words as hoping, thanking, eagerly, favor. If we are really worthy of the job, the Company will benefit by giving it to us every bit as much as we will profit by getting it. The thing works both ways. Why then use begging words that suggest we are thinking of ourselves, not of the Company? And why suggest that we’re not too confident in our ability?

He’s Partly Right at Least

With our eye on our brother’s ego, we’ll see that concession is the very cornerstone of good human relations. We cannot reach human agreements without mutual concession. The self-respect that every man feels impelled to maintain, demands that he appear at least partly right. Therefore, let’s not ever try to prove anyone wholly wrong. Let’s find something herein we can feel that he’s right. Then let’s say so. We simply must not build up our own ego at any unnecessary expense of our brother’s ego. Let’s keep an eye on concession.

--

Sponsored by: Slack - Making teamwork simpler, more pleasant, and more productive.

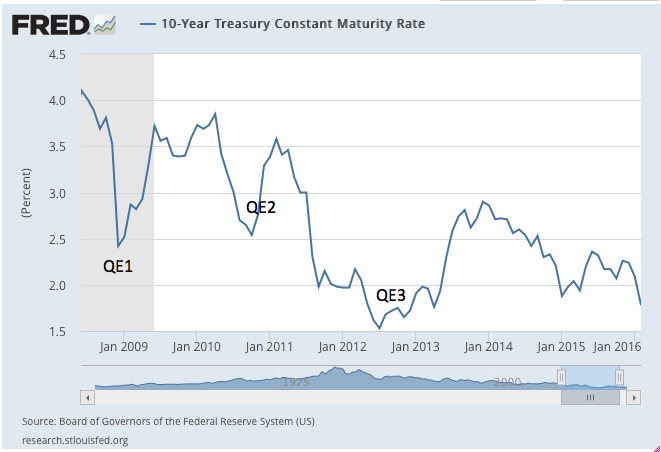

Central Banks need to get real (not nominal)

In all these debates there seems to be an unusual amount of what economists call money illusion or lack of understanding of the difference between nominal and real interest rates. This confusion, in my view, is partly motivated by the communication strategy of central banks that seem to obsess with the asymmetric nature of their inflation targets (for both the ECB and US Fed, inflation targets are defined as close but below 2%) and are not clear enough on their final goal and its timing.

How do we want interest rates to react to aggressive monetary policy? The common answer is that we want interest rates to go down. This is correct if we think in real terms: given inflation expectations (or actual inflation), we want interest rates to move down relative to those inflation levels. But in some cases, in particular when inflation expectations are lower than what central banks would like them to be, the central bank by being aggressive is targeting higher inflation expectations and this can possibly lead to higher nominal (long-term) interest rates.

This is what happened in the three rounds of quantitative easing by the US Federal Reserve. 10-Year interest rates went up which was a signal of increasing inflation expectations (and even higher expectations of future real interest rates). This was seen as a success.

Addressing poverty traps through migration, in the small and in the large

People who were pessimistic about the future of BIMARU states and other poverty traps have long felt that migration out of these bad places was a good way out. In recent months, an empirical literature in the US has suggested that there are large positive effects upon poor people when taken out of poverty traps. Let's think about policies that assist or retard migration, and about downstream implications. Some things that make a difference (positive or negative) to migration are well known:

- `Workfare' programs like NREGA may hamper migration.

- A malfunctioning land market makes it harder for people who own land to leave. Laws that make it difficult for SCs or STs to sell land are particularly harmful in locking people to the land.

- Improvements in urban governance will help increase migration flows to cities.

- A better criminal justice system will increase the safety of migrants and thus assist migration flows.

- Divergence of per capita income across states will spur migration flows.

- More use of English in education and in government creates a nationwide labour market where people from all over the country are able to move, get jobs, access government services, file a complaint in a police station, etc. We should aim to become more like the US (a nationwide labour market with English) and less like Europe (where barriers of language reduce migration flows).

While leaving is good for the household or the individual who leaves, it's interesting to think about the consequences of departure. In the US, the standard intuition is expressed in the Tiebout model, where labour mobility creates local neighbourhoods for people with homogeneous preferences. I worry that we have a different problem in India. We should think more carefully about the consequences for a place like Uttar Pradesh when many people choose to leave.

We may conjecture that the more capable people leave. I'm reminded of the HMY model: there's a fixed cost of migration, and paying this activation energy is justified when the NPV of future cashflows is large enough. In the HMY model, only more productive firms export or do outbound FDI. In similar fashion here, more capable people are likely to make the jump.

In the small, this is not a problem. But what if a sufficiently large phenomenon of migration-by-the-best takes place. Could this rob a poverty trap of the people who can exercise leadership in starting a business, teach, do research, criticise wrong-doing, or engage in politics? For a sufficiently strong selectivity process, and for a sufficiently large exit-by-the-elite, we could get an explosive process where the departure of the elite leads to a reduction in the quality of government and the local economy, which encourages more elite flight, and so on. Badlands with warlords might become worse if there is a systematic bias where people who could fix things tend to leave.

For this unpleasant dynamics, migration has to take place on a large enough scale to adversely affect the talent pool at the source location. As an example, in the 1960s, Jagdish Bhagwati worried about the `brain drain' out of India. With the benefit of hindsight, we know this was not a big issue. There has been no real problem in the talent pool within India for the purpose of teaching, doing research, criticising wrong-doing, leading firms, participating in politics, etc. The scale of out-migration from India was not large enough to damage the upper tail in India.

Could conditions in Bihar or Uttar Pradesh be different? Could the selection process and the magnitude of out-migration create an explosive process which knocks out the upper tail? If such a vicious cycle is present, it changs the way we think about federalism. In a happy Tiebout world, politicians compete to offer local public goods that are attractive to the median voter, and the tails of the distribution of preferences leave. At the same time, there would be in-migration of people who are attracted to the package of local public goods that the politicians are offering. In this benign world, more federalism is undoubtedly a good thing. If, on the other hand, we get feedback loops through which poverty traps get trapped with warlords, this raises concerns about the outcomes associated with the democratic process in poverty traps.

We should be careful to distinguish between two distinct issues. The subsidiarity principle suggests that the best accountability for local public goods is obtained by placing the votes and the voice in the hands of people who are at the lowest possible level of government. This favours decentralisation. However, if there are conditions where an explosive process can remove the upper tail of the talent pool in a poverty trap, this can adversely affect the quality of local politics, and the ability to create productive firms. Under these conditions, we should worry about decentralisation.

Regulatory priority: punish, deter or protect?

When a serious breach of market integrity is suspected, what should the regulators’ priorities be: should it try to punish the guilty, or should it seek to deter other wrong doers or should it focus on protecting the victims? Both bureaucratic and political incentives may be tilted towards the first and perhaps the second, but in fact it is the last that is most important. I have been thinking about these issues in the context of the order of the Securities and Exchange Board of India in the matter of Sharepro Services, a Registrar and Share Transfer Agent regulated by SEBI. The order which is based on six months of investigation and runs into 98 pages finds that:

Shares and dividends have been transferred from the accounts of the genuine investors to entities linked with the top management of Sharepro without any supporting documents

Records have been deliberately falsified avoid the audit trails.

Sharepro and its top management have authorized issuances of new certificates without any request or authorisation from shareholders.

The management of Sharepro has not cooperated with the investigation which being carried out by SEBI and on several occasions, it has attempted to mislead the investigation in the matter.

If one assumes that these findings are correct, then the key regulatory priority must be to take operational control of Sharepro and thereby protect the interests of investors who might have been harmed. A Registrar and Share Transfer Agent is a critical intermediary whose honest functioning is essential to ensure market integrity and maintain the faith of investors in the capital markets. I think that SEBI’s powers under section 11B of the SEBI Act would be adequate to achieve this objective, but in case of need, resort could also be had to section 242 of the Companies Act 2013.

The SEBI order does take some steps to punish the top management of Sharepro but does too little to protect the investors who appear to have lost money. It does not even cancel or suspend the registration of Sharepro as a Registrar and Share Transfer Agent, but merely advises companies who are clients of Sharepro switchover to another Registrar and Share Transfer Agent or to carry out these activities in-house. The only investor protection step in the order is the direction to companies who are clients of Sharepro to audit the records and systems of Sharepro. But if the records have been falsified, then only a regulator or other agency with statutory powers can carry out a meaningful audit by obtaining third party records.

A decade ago, when the Satyam fraud occurred, I was among the earliest to write that the government should simply take control of the company. I would argue the same in the case of Sharepro as well assuming that the SEBI findings are correct.

6 Investing Lessons from the Valeant Pharmaceuticals Scandal

It’s not every day that a company with a market cap of more than US$ 70 billion (almost same as India’s largest company by market cap), and one that is favoured by a lot of savvy investors, loses 80% in nine months (65% in just last one month). But that’s what has happened with investors in the Canada-based Valeant Pharmaceuticals, where a spate of scams has been discovered over the past few months – from bad M&A accounting, to wrongful income reporting, and now the company is facing a potential default.

Valeant is a typical case of a high-growth business where people think nothing could go wrong and overpay ignoring the complexities and fuzziness, and which ultimately presents itself as a classic case on what not to do in business and investing.

Like I wrote about the Volkswagen scandal a few months back, there are several lessons one can learn from the fall from grace of Valeant. Here are just six of them.

1. “Not Just One Cockroach” Theory Works

Problems at companies are never isolated. Like cockroaches, there is never just one problem. The first big cockroach from Valeant’s kitchen emerged in September 2015 when the company was accused of jacking up prices for the drugs it had bought through several mergers and acquisitions, some as high as 500% to 800%.

Then, in October 2015, trading in Valeant’s stock was halted three times as it declined by 28% in a day following a report that claimed that the company was using a pharmacy chain called Philidor to store inventory and record the transactions as sales. A major allegation was that, by controlling the pharmacy services offered by Philidor, Valeant steered the latter’s customers to expensive drugs sold by it.

Another big cockroach in Valeant’s kitchen is the huge amount of debt it holds on its balance sheet (US$ 30 billion), which has led to the company facing a looming default. Secondly, Valeant’s loans are not owned by one bank or even a few large investors but by around 753 funds over 103 fund managers in the form of collateralized loan obligations, or CLOs (essentially loan funds that buy and hold lower credit debt). So, it’s now a systemic risk and not just Valeant specific.

Warren Buffett wrote in his 2002 letter –

When managements take the low road in aspects that are visible, it is likely they are following a similar path behind the scenes. There is seldom just one cockroach in the kitchen.

It’s a great lesson in case you own a company where the management has taken the low road – maybe too many acquisitions, or bad accounting. There is seldom just one cockroach in the kitchen.

2. Beware of Serial Acquirers

If the acquirer is not Warren Buffett’s Berkshire Hathway that has a long-long track record of making sensible acquisitions, I am not willing to bet on a company that is trying to grow fast through this route. Most acquisitions are made not for any “strategic fit,” but to satisfy the egos of top managers making the acquisitions. So, most acquisitions are brash, and thus expensive. Aswath Damodaran wrote this in his recent post –

The Valeant story reinforces many of my existing biases against companies that grow primarily through acquisitions. I am willing to concede that this strategy can pay off, if companies maintain discipline, but my experience with these companies is that they inevitably hit a wall, either because they become too large to stay disciplined or because the accounting creates too many opportunities to obfuscate and hide problems.

In this case, Valeant appears to have been both too large to stay disciplined and willing to surf on the non-transparency of M&A accounting. There are lessons galore from India on this front, Tata Steel, Suzlon and 3i Infotech being on top of my mind – though all of these cases were bad more for the indiscipline/overpaying than fuzzy M&A accounting.

3. Intrinsic Values Can be Permanently Destroyed

Often for companies that lose their reputation due to their own wrongdoings, it’s very difficult to come back to business as usual. Their customers won’t trust them anymore, and so would their suppliers. As more problems emerge – the “not just one cockroach” theory – and bad news leads to more bad news, business takes the backseat. Subsequently, the intrinsic value that is driven by the company’s earning power is impaired, often permanently.

A lot of investors equate low stock prices i.e., cheapness, with value. This can be a dangerous equation for companies that actually deserve that cheapness owing to their deteriorated fundamentals. For instance, Aswath Damodaran has tried to calculate Valeant’s intrinsic value using this excel file, but just the number of variables that need to go right – which is entirely based on whether Valeant would get its house in order – to justify the calculated intrinsic value would make you drowsy.

When you wear the Grahamian hat and buy cheap stocks believing they would revert to mean, you must practice extreme-extreme diversification. But when you are looking to invest only in high quality businesses, you must know how “high quality” looks like and must be willing to change your mind when that quality deteriorates.

After all, margin of safety in a stock may decline not always when the stock price rises to meet intrinsic value, but also when the intrinsic value falls to meet the stock price.

4. Biases are Impossible to Eliminate

In all my workshops when I talk about behavioural biases that effect investors, I end with a caveat that these biases are impossible to eliminate because that’s how our brains are wired. One of the biases I talk about is that of Confirmation/Commitment and Consistency. This is how Robert Cialdini explained this bias in is brilliant book Influence –

Once we have made a choice or taken a stand, we will encounter personal and interpersonal pressures to behave consistently with that commitment. Those pressures will cause us to respond in ways that justify our earlier decision.

Charlie Munger uses the inverted version to represent the bias it causes and calls it ‘inconsistency-avoidance bias’. He explains that the human brain conserves programming space by being reluctant to change.

This bias is especially at play when you are losing money on a bad business, but your internal “yes-man” continues to seek evidences that confirm your original thesis to conclude that you could not be wrong.

Now, one of the hardest things to do in investing is to find the balance between staying put with your high conviction ideas through unfavorable times, and realizing that you were wrong in your conviction and changing your mind.

Consider Bill Ackman’s vociferous and continuous support for Valeant while the stock was falling off the cliff as more cockroaches were jumping out of its cupboard. Here’s what he wrote to clients in his Jan. 2016 letter (emphasis mine) –

The inception of the portfolio’s decline began with Valeant in August. We have discussed at length the events at Valeant which catalyzed the stock’s initial decline: political attention on drug pricing and the industry, regulatory scrutiny, attacks by short sellers, and the termination of a distribution arrangement representing ~7% of Valeant’s sales. But, we would never have expected that the cumulative effect of these events would have caused a nearly 70% decline in the stock, nor do we believe that they will permanently impair Valeant’s intrinsic value.

Note that even as Ackman wrote about the multiple serious issues faced by Valeant, he maintained that all this would not “permanently” impair the company’s intrinsic value. Now I have no idea if Ackman is right or wrong here. But I know how hard it is to admit being wrong after sinking a lot of money into one idea (he recently increased his holding in Valeant by 30%, and now owns 9% stake).

There is a big difference between patience and stubbornness, and not admitting that you are wrong even when all the facts are against you, is being stubborn. But admitting that you were wrong, which indirectly is an admission that all the hard work you did in the past has come to zero, really hurts. And that’s why it’s basic human nature to remain committed to and consistent with your old ideas. But then, as Charlie Munger said –

Failure to handle psychological denial is a common way for people to go broke. You’ve made an enormous commitment to something. You’ve poured effort and money in. And the more you put in, the more that the whole consistency principle makes you think, “Now it has to work. If I put in just a little more, then it ‘all work.” People go broke that way, because they can’t stop, rethink, and say, “I can afford to write this one off and live to fight again. I don’t have to pursue this thing as an obsession in a way that will break me.”

It’s difficult for even the smartest of investors to avoid falling into this trap of holding on to their old, bad, losing ideas…but then you don’t need to be so smart to understand the implications of such thinking, given the long history of how others have destroyed wealth under the spell of this bias.

Morgan Housel wrote this in his recent post –

How do you avoid this trap?

It’s so difficult. But here’s an idea to help reduce errors: Avoid investments of such vague appeal that a team of Harvard MBAs needs three years and $50 million of research to get to the bottom.

I see people whose investment beliefs rival religious passion. They believe so strongly in their views that they literally can’t understand why you’d disagree with them. The basis of their passion is usually years of deep study, which creates the impression of expertise but may actually just be a supernova of confirmation bias and self-delusion. “Expertise is great,” investor Dean Williams once said, “but it has a bad side effect: It tends to create an inability to accept new ideas.”

5. Humility is a Big Virtue

It’s important to stay humble when you have had a successful investment track record in the past…and especially when you have had a successful track record.

Consider Warren Buffett and Charlie Munger who have what they call a “too hard pile.” Here’s Munger on this idea –

If something is too hard we move on to something else. What could be simpler than that?

We have three baskets: in, out, and too tough. We have to have a special insight, or we’ll put it in the ‘too tough’ basket.

Buffett and Munger have made it quite clear at several times that they do not have methods to value every company in every industry. If they can’t determine a basic fact like the present value of the business with the degree of accuracy they desire, they just move on to the next opportunity. That’s humility served on a platter.

Compare this with most other investors – big or small. People often get enchanted by complexity, or shiny stuff that is outside their circle of competence. Consider Valeant for instance. As I read more about the company, it has always been a difficult stock to analyze for a number of reasons. Its serial acquisitions make for difficult financial comparisons across years. It doesn’t provide sales data for its major drugs. The management has often emphasized clumsy figures like “cash earnings per share” in their reporting, which exclude some very legitimate costs. And then its scamming relationship with Philidor, the impact of which most people don’t know about.

In all, as more and more bad news emerged from Valeant’s stable, the company became too complicated to figure out, and thus too complicated to own. Bill Ackman, considering his long investment experience, should have known this.

Here is what I read from his note on “humility” in his latest letter, where he described the reasons for poor performance of his fund in 2015 and his thoughts for 2016 –

…in order to be a great investor one needs to first have the confidence to invest without perfect information at a time when others are highly skeptical about the opportunity you are pursuing. This confidence, however, has to be carefully balanced by the humility to recognize when you are wrong. While no one here is enthusiastic about delivering our worst performance year in history in 2015, it certainly does a good job reinforcing the humility-side of the equation that is necessary for long-term investment performance. In 2016, we would like to generate results that reinforce the confidence side of the equation. Humility and skepticism will help get us there.

Ironically, in Valeant’s case, Ackman has neither been humble nor a skeptic…and this has caused his downfall.

6. Concentration Can be Hugely Risky

While I am a diversified investor and have nothing against concentration, I believe the latter is a relatively risky strategy for small investors because blow up in 1-2 stocks could wipe out a large amount of your net worth.

In Valeant’s case, many previously successful fund managers put a huge portion of their clients’ assets in the stock. Apart from Ackman, the Sequoia Fund, a mutual fund that Warren Buffett had recommended in the past, put around 30% – that’s almost one-third of their clients’ money – of the fund into the stock.

Of course, all investing involves risk, and everyone makes mistakes so I’m not criticizing any of those money managers for taking a chance on the Valeant brilliantly made up story. All I am saying is that a company with so many moving parts and unknowns and with so many potential downsides (with more emerging by the day) shouldn’t make up such a large part of your portfolio. Because when that is a case, and you lose big money on that company, you tend to remain consistent and committed to your original decision because a large money is at stake, and accepting the mistake would hurt a lot.

The Trouble is…

If you know the future of your investments, it’s silly to play the defensive game. You should behave aggressively – employ maximum leverage and concentrate in the greatest potential winners. After all, there can be no loss to fear.

But then, if you don’t know what the future holds, it’s foolish to act as if you do. Amos Tversky, the noted cognitive and mathematical psychologist and a collaborator of Daniel Kahneman said –

It’s frightening to think that you might not know something, but more frightening to think that, by and large, the world is run by people who have faith that they know exactly what’s going on.

Then, Mark Twain supposedly said –

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.

In investing, overestimating what you’re capable of knowing or doing can be extremely dangerous. Acknowledging the boundaries of what you can know – and working within those limits rather than venturing beyond – can give you a great advantage.

Bill Ackman, and a host of other leading investors in Valeant did not pay heed to this aspect, and they have paid the tuition fee in billions of dollars. I am sure the lessons from the Valeant fiasco would cost you cheap in case you are open and willing to learn from the misadventures of others.

It’s a random, crazy world out there. Play it safe. Play it sensibly. It’s your money after all. Isn’t it?

The post 6 Investing Lessons from the Valeant Pharmaceuticals Scandal appeared first on Safal Niveshak.

Cheap motivation

I’m reading this (so far – I’m blogging in the middle of reading) excellent piece by Charles Assisi in Mint On Sunday about motivation for careers. At the point where I’ve stopped reading his piece and started writing, I’m looking at this graph he has put on the source of motivation:

This reminds me of this conversation I had with a few classmates from business school a few months back. One of them is a successful brand manager for a large packaged goods company, and he was telling us that what gives him the thrills in his job is to see his product replace his rival companies’ products on store shelves.

It is a rather logical motivation – to see the share of the brand you manage improving. However, what was interesting was the way he put it (I’ve surely paraphrased here) – that the thrill came out of his brand doing well at the expense of a rival brand, and of watching the rival brand sink.

It got me thinking about what motivates us, and if motivations are as profound as we like to mention in either a statement of purpose or in an interview. When writing a cover letter for a job, for example, it is likely that you chart out your career path so far detailing motivations for each career move, and what motivates you to take up this job you are applying for.

With a few honourable exceptions, it is likely that it is all a lie, and that you have invented these motivations to retrofit your career progression thus far. Sometimes the real motivation could be as simple as money – you took up a certain job because it paid you well, but for whatever reason it isn’t politically correct to put this on a cover letter (it can work the other way also. I once interviewed for a proprietary trading position and the interviewer was surprised that money wasn’t my number one motivation).

For the most part, however, I argue that the real motivation for most things is something rather trivial – so trivial that nobody will trust you it can actually be a motivation. Like you join a hobby class because that allows you to stay out late. Or go for some other activity because it is near the house of someone you have taken a fancy for. Or you participate in an event because it allows you to travel to a particular city. I had once gone for a recruiting event because it was being held in a five star hotel and the agenda included lunch.

A trivial motivation need not always lead to results – the sheer triviality of the motivation means that you are less likely to generate good results from such processes. However, what trivial motivations allow is to expand the range of activities and opportunities you take part in, and the sheer volume of such expansion can take you to places you had never imagined you would get to. In other words, while at some point in time, you do use serious motivations, it is likely that the seed for such activities or pursuits had been set in more trivial settings.

So when you want to do something purely for the cheap thrills it gives you, go ahead – it might help you learn something about yourself that you’d not known before. And might motivate you to an extent well beyond what motivation you can get from profound sources.

On a Letter from an Expatriate

A friend I haven’t heard from in many years since he left the USA wrote me. He closed the letter in an unusual way, saying:

PS — USA has gone completely bonkers these days? or what the heck is going on over there? would love to pick your mind over a glass of wine. someday!

I’m not intending on writing on politics as a regular habit at Aleph Blog, and most of what I am going to say is economics-related, so please bear with me. Hopefully this will get it out of my system.

To my friend,

There are a lot of frustrated people in the US. Though you’ve been gone a long time, you used to know me pretty well; after all, I trained you on economic matters.

Let me give a list of reasons why I think people are frustrated, then explain how that affects their political calculations, and finally explain why they have mostly misdiagnosed the issues, and won’t get what they want regardless of who is elected.

The electorate is frustrated because:

- Living standards have declined for the lower 80% of society.

- Many people lost jobs, homes, pensions, etc., during the recent financial crisis… those assets are not coming back anytime soon. Much of the fault was theirs, but they don’t recognize that, preferring to blame others for their problems.

- Many formerly attractive jobs are disappearing either due to technological change or offshoring (whether corporations or subsidiaries).

- The economy muddles along, and economic policies that average people don’t understand dominate discussion. Many wonder if anyone is seriously trying to improve matters. They generally distrust the Fed.

- It doesn’t seem to matter who gets elected, Democrat or Republican — the status quo remains because business interests support the Purple Party, which is the consensus of establishment Republicans and Democrats who duopolize politics in the USA.

- Nothing good seems to happen in DC, and what few significant pieces of legislation have occurred in the Obama years have turned out to be bad (Obamacare) or useless (Dodd-Frank to the average person who doesn’t get it).

- Immigration issues get short shrift, also trade issues.

- Moral issues have basically disappeared from the political agenda in any classical form. Everything is pragmatic, geared to serve the Purple Party.

- In general, the candidates are pretty lousy, and the moral tone of the campaign has been poor. That said, negative campaigning works, and the candidates that focus on being negative are doing better.

Now take a moment and think about what people do when they are desperate. In short, they take longer-shot chances than they would ordinarily take. They think:

“This person couldn’t be that much worse than what we have going now, and he sounds a lot different than the politicians that I have been hearing for so many years, ad nauseam. He talks about issues that affect my situation, and is not willing to mince words. He could be a LOT better than the status quo, which stinks.

So, the downside is limited, and the upside could be significant. I don’t care about the rough edges of this guy; the media always blows things out of proportion anyway, and helps foster the consensus candidates that never solve anything. So, I’m just going to hold my nose and vote for (fill in the blank).”

In my opinion, that’s why politics is nuts over here right now. Given the relative inability of the electorate to digest complex explanations, there are a lot of matters that they can’t understand, and as a result, regardless of who they elect, they won’t be happy.

Most of the economic and political problems stem from:

- Technological change

- Increasing returns to those that are smart versus those that are not

- Not enough productive children being born

- Attempts to improve the economy that don’t work

- Gerrymandering

- A diminishing consensus on what is right and wrong, and the proper role of government

The technological change is the most important factor, and explains why attempts to limit immigration or limit free trade won’t help. As a result of the internet, businesses can set up in many areas and benefit from the different aspects of each area — labor here, capital there, taxes way over there. Unless governments are willing to work together to limit this, and they compete, they don’t cooperate here, this can’t be solved.

Information technology can make lower skilled workers far more productive, leading to a diminution of jobs in many sectors. This can happen anywhere — in banks, investment shops, factories, and restaurants. It works anyplace where you can turn 80%+ of a job into a set of rules. That can move jobs away from where they currently are to places where inexpensive labor can do the work.

In the short-run, this is a problem for many. In the long run, it will release labor to more valuable pursuits. That said, many older people will not be capable of retraining, and younger people will gain the opportunities if they are smart. the “know nots” are becoming “have nots.”

Part of this is payback for not studying enough in school, and/or studying topics that would eventually valuable in college. As I have said before, “Follow your bliss” is selfish and dumb. Real value comes, and society improves, from facilitating the bliss of others. The more people you make happy, the greater the rewards are.

Now, demographics are getting worse for most developing economies. Most economies do better when the fertility rate is over 2.1 — i.e., that population is growing. Typically that means that opportunities are growing. When working populations shrink, social benefit plans begin to collapse, and when populations shrink, countries lose vitality and creativity. We need youth to replenish its ranks to keep our societies healthy.

Note that efforts to fix fertility by offering tax incentives do not work. Once women are convinced it is not valuable to have kids, no reasonable amount of effort will change that.

As for economic policy, we are still running policy off of a model that assumes that debts are not high on order for policy to work. That is why continued deficit spending and abnormal monetary policy (QE & Zero or Negative Interest Rates) aren’t helping. Helicopter money has its own issues.

Regardless of what happens to the presidency, Congress will remain the same because of gerrymandering. There’s only so much that even a good President can do if Congress is occupied by ideologues from both sides of the political spectrum.

Finally, the sides of the political spectrum are further apart because there is less consensus on what is right and wrong, and the proper role of government. In some ways the internet facilitates this because you can filter out the arguments of those who disagree with you more easily. I set up my news sources so that I am always reading liberals and conservatives, as well as those that don’t fit well on the political map, but few others do.

And that, my friend, is why the political scene is nuts in the US now. There are a lot of disappointed and desperate people who are willing to try anything to get their prosperity back, even though none of the politicians can do anything that will genuinely help the situation.

It is a recipe for disaster, and absent an act of God, I don’t see anything that will change the attitudes rapidly. People across the political spectrum are happily believing their own myths; it will take a lot of pain to puncture them all.

PS — I’ve given up alcohol. We’ll have to figure something else out if we get together.

The land above the tracks

Almost exactly a year ago, we were on our way from Vienna to Budapest and ended up reading the Vienna Hauptbahnhof Railway Station some three hours early. It had been snowing that morning in Vienna (it was April 1st, and supposed to be spring), and not wanting to go anywhere in that shit weather, we simply got to the railway station. It didn’t help matters that our train (which was coming from Munich) had been delayed by a further hour.

We were not short of options for entertainment in at the railway station, though. In fact, it hardly looked like a railway station, and looked more like a mall – for there were no tracks to be seen anywhere. We spent the four hour wait shopping at the mall (it was just before Easter, so there were some good deals) and having breakfast and lunch at what could be considered to be the mall food court. And when it was time for our train to arrive, we simply took one of the escalators that went down from the mall, which deposited us at our platform.

Each platform had its own escalator going down from the mall, which had been built on top of the railway tracks. It can be considered that the entire Vienna Hbf station was built on the “first floor”, making use of the land above the railway tracks. Land that would otherwise be wasted was being put to good use by building commercial space, which apart from generating revenues for the Austrian Railways, also made life significantly better for passengers such as us who happened to reach the station insanely early.

This is a possible source of revenues that Indian Railways would do well to consider, especially in large cities. The Railways sit on large swathes of land above and around the rail tracks, especially at stations (where such tracks diverge). Currently, the quality of experience in Indian railway stations is rather poor. If a swanky mall (and maybe other commercial space) were to come up above the tracks, it could completely transform the railway experience.

There will be considerable investment required, of course, but given the quality of real estate on which most Indian railway stations sit, it is quite likely that private developers can be found who will be willing to invest in constructing these “railway station malls” in return for a share of subsequent rent realisation. There is serious possibility for a win-win here.

As the Vienna Hbf website puts it,

The BahnhofCity Wien Hauptbahnhof features 90 shops and restaurants occupying 20,000 m² of floor space. A fresh food market, textile shops, bakeries and cafés are designed to make BahnhofCity a meeting place. During the week, it will be opened until 21:00 and many shops will also open on Sundays. Excellent public transport links and 600 parking spaces complement the offer.

An idea well worth considering for the Indian Railway Ministry.

Why blogging has been intermittent

Things have been slow around here, you may have noticed. A few people have asked why. Part of the reason has been that I have been really distracted. First there was the travel. I had left for India early December 2015. Visiting places and meeting people is distracting although fun. I started back from India on Jan 23rd. First stop was Brussels. I arrived at Zaventem airport in Brussels at 8 AM on Jan 23rd. That was two months ago. Seeing the pictures of the bombed-out departure hall brings back memories. I have walked that hall close to a dozen times over the last few years. Yesterday’s terrorist attack at Brussels airport felt somewhat personal to me. After Brussels, I stopped for a week on the East coast to visit friends in New Jersey and Boston, and got home to San Jose on 2nd February.

I should have started writing on the blog but I had another distraction. My blog had been hosted on servers in India. Last December while I was in India, I received a notice from some legal outfit representing one person threatening to sue me for an article on my blog. The threat was made on behalf of an organization which has really deep pockets. The article was innocuous enough but freedom of speech in India rests on very weak foundations, and while I would have prevailed in court, the nuisance of going to court to defend myself was too much to even contemplate. Deep pockets can cause massive injury even if they lose the case. I took down the article, promising myself to put it back up again after I had moved the hosting of this blog to the US. That finally got done just a couple of days ago. (Hat tip: JP for all his help.)

Those two reasons (travel and migrating the blog) are basically excuses. The truth is that the real reason that I have neglected writing is this. Part of it is that I have been lazy, and part that I have been struggling with a writer’s block. Why the writer’s block? Because I have been reading. So? What I have been reading makes me hesitate to write. The hesitation arises from the recognition that brilliant others have figured out the solutions and there’s fancy little I can add to advance that line of inquiry. Reading is rewarding but can also reveal how intellectually puny one is relative to the giants.

Still, one cannot just throw up one’s hands and give up. Let’s see where this goes from here. Be well, do good work and please keep in touch.

What Can We Learn From the Prolific Mr. Asimov?

To learn is to broaden, to experience more, to snatch new aspects of life for yourself. To refuse to learn or to be relieved at not having to learn is to commit a form of suicide; in the long run, a more meaningful type of suicide than the mere ending of physical life.

Knowledge is not only power; it is happiness, and being taught is the intellectual analog of being loved.

— Isaac Asimov, Yours, Isaac Asimov: A Life in Letters

Fans estimate that the erudite polymath Isaac Asimov authored nearly 500 full-length books during his life. Even if some that “don’t count” are removed from the list — anthologies he edited, short science books he wrote for young people and so on — Asimov’s output still reaches into the many hundreds of titles. Starting with a spate of science-fiction novels in the 1950s, including the now-classic Foundation series, Asimov’s writing eventually ranged into non-fiction with works of popular science, Big History, and even annotated guides to classic novels like Paradise Lost and Gulliver’s Travels.

Among his works were a 1,200 page Guide to the Bible; he also wrote books on Greece, Rome, Egypt, and the Middle East; he wrote a wonderful Guide to Shakespeare and a comprehensive Chronology of the World; he wrote books on Carbon, Nitrogen, Photosynthesis, The Moon, The Sun, and the Human Body, along with many more scientific topics. He coined the term “robotics” and his stories led to modern movies like I, Robot and Bicentennial Man. He wrote one of the most popular stories of all time: The Last Question. He even wrote a few joke books and a book of limericks.

His Intelligent Man’s Guide to Science, a 500,000 word epic written in a mad dash of eight months, was nominated for a National Book Award in 1961, losing only to William Shirer’s bestselling history of Nazi Germany, The Rise and Fall of the Third Reich.

His science-fiction books continue to sell to this day and are considered foundational works of the genre. He won more than a dozen book awards. His science and history books were considered some of the best published for lay audiences — the only real complaint we can make is that a few of them are outdated now. (We’ll give Asimov a pass for not updating them, since he’s been dead for almost 25 years.)

In his free time, he was reputed to have written over 90,000 letters while keeping a monthly column in the Magazine of Fantasy and Science Fiction for 33 years between 1958 and 1991. Between the Magazine and numerous other outlets, Asimov compiled somewhere near 1,600 essays throughout his life.

In other words, the man was a writer through and through, leading to a question that begs to be asked:

What can we mortals learn from the Prolific Mr. Asimov?

Make the Time — No Excuses

Many people complain that they don’t have time for their passions because of the unavoidable duties which suck up every free moment: Well, Asimov had duties too, but he got his writing career started anyway. From 1939 until 1958, Asimov doubled as a professor of biochemistry at Boston University, during which he completed 28 novels and a list of short stories long enough to fill most writers’ entire career. He simply made the time to write.

In a posthumously published memoir, Asimov reflects on the “candy store” schedule implanted on him by his father, who’d worked long hours running a convenience store in New York after emigrating from Russia. As Asimov became a professional writer, he kept the heroic schedule for himself:

I wake at five in the morning. I get to work as early as I can. I work as long as I can. I do this every day of the week, including holidays. I don’t take vacations voluntarily and I try to do my work even when I’m on vacation. (And even when I’m in the hospital.)

In other words, I am still and forever in the candy store. Of course, I’m not waiting on customers; I’m not taking money and making change; I’m not forced to be polite to everyone who comes in (in actual fact, I was never good at that). I am, instead, doing things I very much want to do — but the schedule is there; the schedule that was ground into me; the schedule you would think I would have rebelled against once I had the chance.

Know your Spots, and Stick to those Spots

“I’m no genius, but I’m smart in spots, and I stay around those spots.”

—Thomas Watson, Sr., Founder of IBM

Even though he’d been writing in his spare time as a professor, Asimov was not doing any academic research, which did not go unnoticed by his superiors at Boston University. Asimov’s success as an author combined with his dedication to his craft had forced him into a decision: Be an academic or be a popular writer. The decision needed no fretting — he was making so much money and such a large impact as a writer, he knew he’d be a fool to give it up. His rationalization to the school was wise and instructive:

I finally felt angry enough to say, “…as a science writer, I am extraordinary. I plan to be the best science writer in the world and I will shed luster on the medical school [at BU]. As a researcher, I am simply mediocre and…if there’s one thing this school does not need, it is one more merely mediocre researcher.”

[One faculty member complimented him on his bravery in fighting for academic freedom.] I shrugged, “There’s no bravery about it. I have academic freedom and I can give it to you in two words:

“What’s that?” He said.

“Outside income,” I said.

In other words, Asimov knew his circle of competence and knew himself. He made that again clear in a 1988 interview, when he was asked about a number of other projects and interests outside of writing. He demurred on all of them:

SW: Do you have any time left for other things besides writing?

IA: All I do is write. I do practically nothing else, except eat, sleep and talk to my wife.

[…]

SW: Have you ever written any screenplays for SF movies?

IA: No, I’m no talent for that and I don’t want to get mixed up with Hollywood. If they are going to do something of mine, they will have to find someone else to write the screenplays.

[…]

SW: Do you like the covers of your books? Do you have any input in their design?

IA: No, I don’t have any input into that. Publishers take care of that entirely. They never ask any questions and I never offer any advice, because my artistic talent is zero.

[…]

SW: Do you have a favorite SF painter?

IA: Well, there is a number of painters that I like very much. To name just a few: Michael Whelan and Boris Vallejo are between my favorites. I’m impressed by them, but that doesn’t necessarily mean anything – I don’t know that I have any taste in art.

[…]

SW: Have you ever tried to paint something yourself?

IA: No, I can’t even draw a straight line with a ruler.

[…]

SW: Do you have any favorite SF writers?

IA: My favorite is Arthur Clark. I also like people like Fred Pohl or Larry Niven and others who know their science. I like Harlan Ellison, too, although his stories are terribly emotional. But I don’t consider myself a judge of good science-fiction – not even my own.

Asimov knew and recognized his own constitution at a fairly early age, smartly seizing opportunities to build his life around that self-awareness in the way Hunter S. Thompson would advise young people to do years later.

In a separate posthumously published autobiography, Asimov reflected on his highly independent nature:

I never found true peace till I turned my whole working life into self-employment. I was not made to be an employee.

For that matter, I strongly suspect I was not made to be an employer either. At least I have never had the urge to have a secretary or helper of any kind. My instinct tells me that there would surely be interactions that would slow me down. Better to be a one-man operation, which I eventually became and remained.

Find What you Love, and Work Like Hell

To be prolific, he warns, one must be a

“single-minded, driven, non-stop person.”

— Interview with Isaac Asimov, 1979

Although Asimov was working the “candy store” hours and producing more output than nearly anyone of his generation, it was clear that he did it out of love. The only reason he was able to write so much, he said, was “pure hedonism.” He simply couldn’t not write. That would have been unfathomable.

One admission from his autobiography tells the tale best:

One of the few depressing lunches I have had with Austin Olney [Houghton Mifflen editor] came on July 7, 1959. I incautiously told him of the various books I had in progress, and he advised me strongly not to write so busily. He said my books would compete with each other, interfere with each other’s sales, and do less well per book if there were many.

The one thing I had learned in my ill-fated class in economics in high school was “the law of diminishing returns,” whereby working ten times as hard or investing ten times as much or producing ten times the quantity does not yield ten times the return.

I was rather glum after that meal and gave the matter much thought afterward.

What I decided was that I wasn’t writing ten times as many books in order to get ten times the monetary returns, but in order to have ten times the pleasure.

One of Asimov’s best methods to keep the work flowing was to have more than one project going at a time. If he got writers’ block or got bored with one project, he simply switched to another project, a tactic which kept him from stopping work to agonize and procrastinate. By the time he came back to the first project, he found the writing flowed easily once again.

This sort of “switching” is a hugely useful method to improve your overall level of productivity and avoid major hair-pulling roadblocks. You can also use this tactic with books to improve your overall reading yield, switching between them as your mood and energy dictates.

Never Stop Learning

If anything besides sheer productivity defined Asimov, it was a thirst for knowledge. He simply never stopped learning, and with that attitude, he grew into a mental giant who was more than once accused of “knowing everything”:

Nothing goes to waste, if you’re determined to learn. I had already learned, for instance, that although I was one of the most overeducated people I knew, I couldn’t possibly write the variety of books I manage to do out of the knowledge I had gained in school alone. I had to keep a program of self-education in process.

[…]

And, as I went on to discover, each time I wrote a book on some subject outside my immediate field it gave me courage and incentive to do another one that was perhaps even farther outside the narrow range of my training…I advanced from chemical writer to science writer, and, eventually, I took all of my learning for my subject (or at least all that I could cram into my head — which, alas, had a sharply limited capacity despite all I could do).

As I did so, of course, I found that I had to educate myself. I had to read books on physics to reverse my unhappy experiences in school on the subject and to learn at home what I had failed to learn in the classroom — at least up to the point where my limited knowledge of mathematics prevented me from going farther.

When the time came, I read biology, medicine, and geology. I collected commentaries on the Bible and on Shakespeare. I read history books. Everything led to something else. I became a generalist by encouraging myself to be generally interested in all matters.

[…]

As I look back on it, it seems quite possible that none of this would have happened if I had stayed at school and had continued to think of myself as, primarily, a biochemist…[so] I was forced along the path I ought to have taken of my own accord if I had had the necessary insight into my own character and abilities.

(Source: It’s Been a Good Life)

Still interested? Check out Asimov’s memoir I, Asimov, his collection of stories I, Robot, or his collection of letters, Yours, Isaac Asimov: A Life in Letters.

--

Sponsored by: Slack - Making teamwork simpler, more pleasant, and more productive.

Banking distress: containing the damage

But there are also some other issues due to which non-performing assets have added up in the banking system," he said, adding that some genuine economic reasons for the delays in repayments to banks needed to be dealt with. In steel, he said, it was dumping by China. In sugar, it was low global prices, while in power, it was indiscriminate moves by some states to sell electricity below cost, forcing distribution companies to resort to borrowing. In highways, it was poor policy implementation that had crippled the sector, Jaitley said, listing the reasons for the rise in bank NPAs.

These observations are welcome. I am inclined to think, however, that much damage has already been done by strong statements made by people at the top and also by the media coverage of the issue. I would imagine that fear psychosis is pervasive and PSB bankers would be reluctant to lend to large corporates and especially for infrastructure. It does not help at all that the CBI has swung into action.Since the NPA position can't be tackled without fresh funds coming and projects moving towards completion, it does look as though the problem is going to stretch out for a while.

What can be done with stressed assets? Well, broadly there are three options:

i. Identify cases where the stress has happened for genuine reasons. In these cases, banks should take a hit and fresh money should come in. But PSBs will be most reluctant to do so in the present atmosphere. I would suggest that the government set up a Settlement Advisory Board comprising ex-bankers, chartered accountants, academics and others to vet loan settlements above a certain value. That would give bankers the courage to move ahead. Fresh funds can come either from the banks or the National Infrastructure Investment Fund.

ii. Use SDR to convert debt into equity, dislodge existing promoters and management and bring in new promoters. This sounds fine in principle but it hasn't happened in a single instance so far. Borrowers can stymie such moves by approaching courts. Bankers don't have the expertise to find fresh promoters. Again, if new promoters are to come in, valuation issues will arise. I don't think SDR will work/

iii. Government takes over some of the stressed assets, completes the projects and repays banks' loans. So, for example, NHAI could take over road projects, SAIL could acquire steel projects, NTPC could acquire power projects and so on. The key issue is: do they have the ability to complete the projects in their present condition? In some cases at least, this is worth exploring.

While resolving stressed assets, we need to ensure that systems are strengthened so as to avoid a repetition of past mistakes. The Bank Board Bureau must professionalise bank boards and induct high quality people as MDs. The BBB is not as envisaged by the P J Nayak committee. The Nayak committee wanted a BBB without any government representatives. That is completely unrealistic in my view. Government as the owner has to take the lead in making appointments. The job of the BBB Chairman and other members is to ensure that the government gets these appointments right. But much depends on the intentions of the government.

The BBB is no merely the old Appointments Board minus the RBI Governor. The Appointments Board could not prevent wrong appointments. So the onus really is on government to make the right choices. One hopes that the present crisis brings out the best in government as crises typically do.

Why would a manufacturer finance a bank's capital expenditure?

Usually a manufacturing company goes to a bank to finance its capital expenditure. But last month witnessed a deal where the US manufacturing giant GE stepped forward to finance the capital expenditure of one of the largest banks in the world – JPMorgan Chase – when the latter decided to buy 1.4 million LED bulbs to replace the lighting across 5,000 branches in the world’s largest single-order LED installation to date.