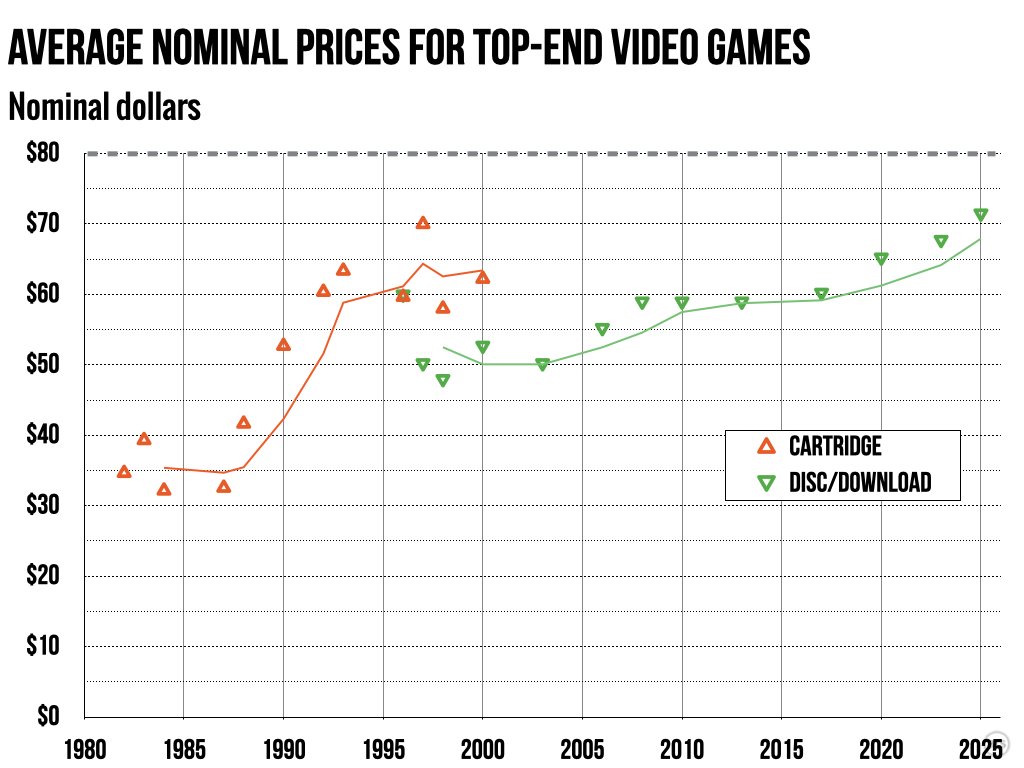

Console gaming's nominal price ceiling has gone up pretty consistently in the last 40+ years.

Credit:

Kyle Orland / Ars Technica

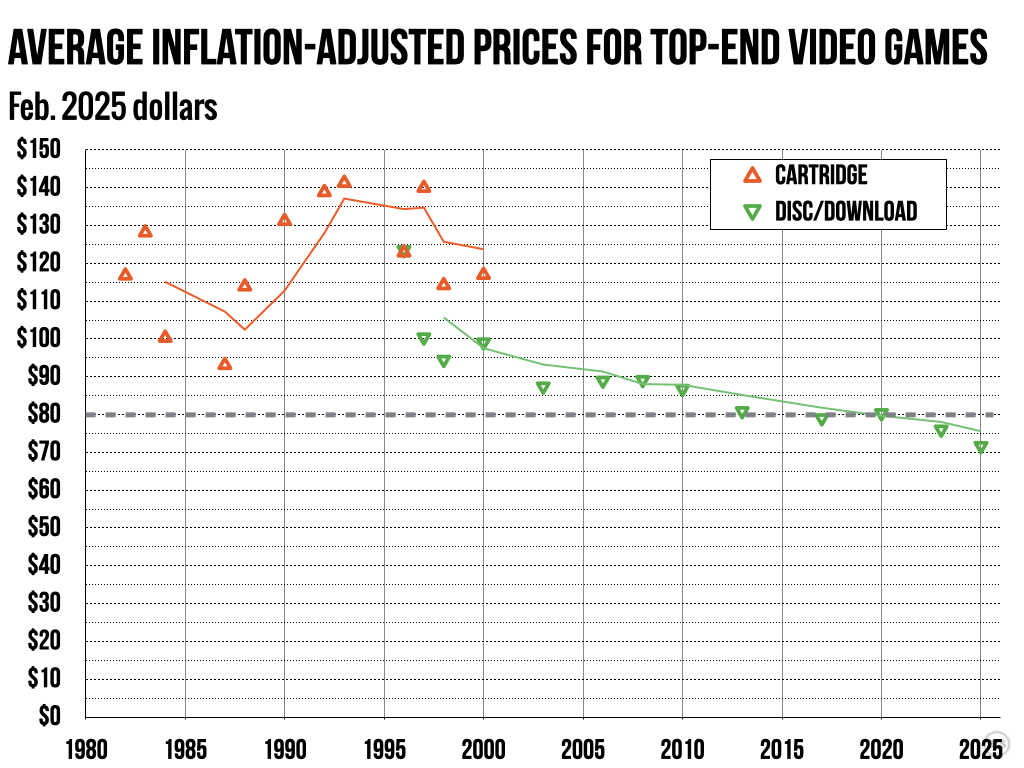

After adjusting for inflation, an $80 price level doesn't seem all that out of the ordinary.

Credit:

Kyle Orland / Ars Technica

When you adjust historical game prices for inflation, though, you find that asking $80 for a baseline game in 2025 is broadly in line with the prices big games were commanding 10 to 15 years ago. And given the faster-than-normal inflation rates of the last five years, even the $70 nominal game prices that set a new standard in 2020 don't have the same purchasing oomph they once did.

The data

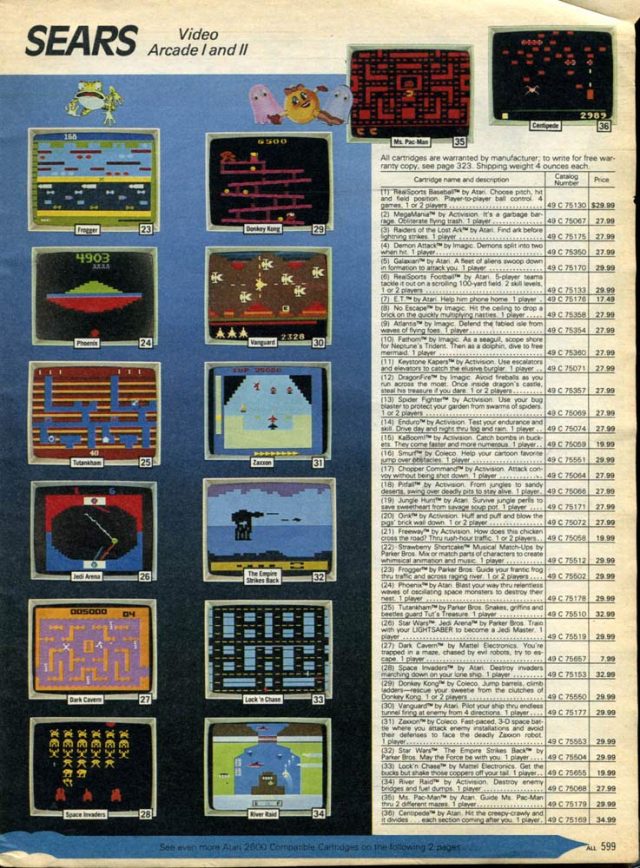

$34.99 for Centipede on the Atari 2600 might sound cheap, but that 1983 price is the equivalent of roughly $90 today.

Credit:

Retro Waste

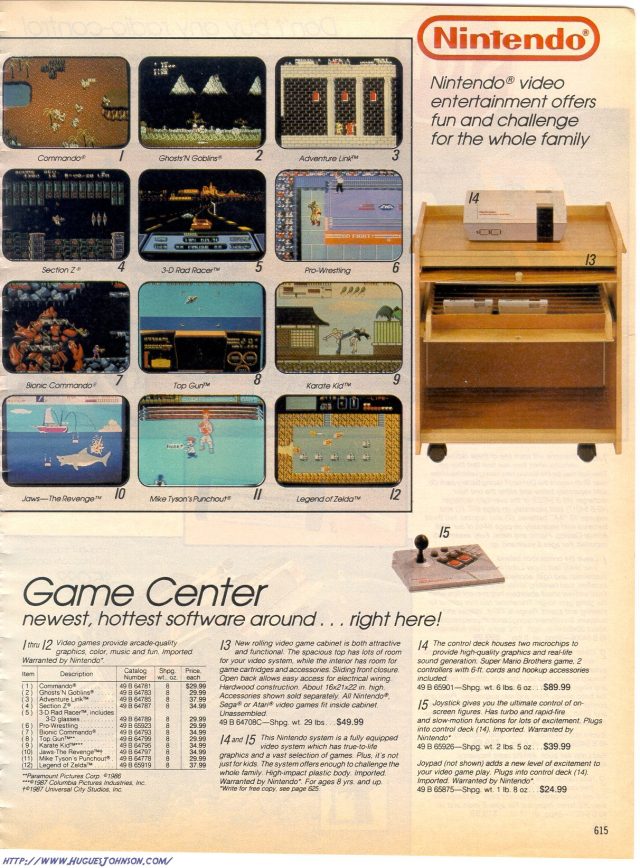

Check out the premium pricing for Zelda titles above other NES games in the 1988 Sears catalog.

Credit:

Hughes Johnson

If you wanted Streets of Rage 2 from Electronics Boutique in 1993, you'd better have been ready to pay extra.

Credit:

Hughes Johnson

To judge Mario Kart World's $80 price against historical trends, we first needed to figure out how much games cost in the past. To do that, we built off of our similar 2020 analysis, which relied on scanned catalogs and retail advertising fliers for real examples of nominal console game pricing going back to the Atari era. For more recent years, we relied more on press reports and archived digital storefronts to show what prices new games were actually selling for at the time.

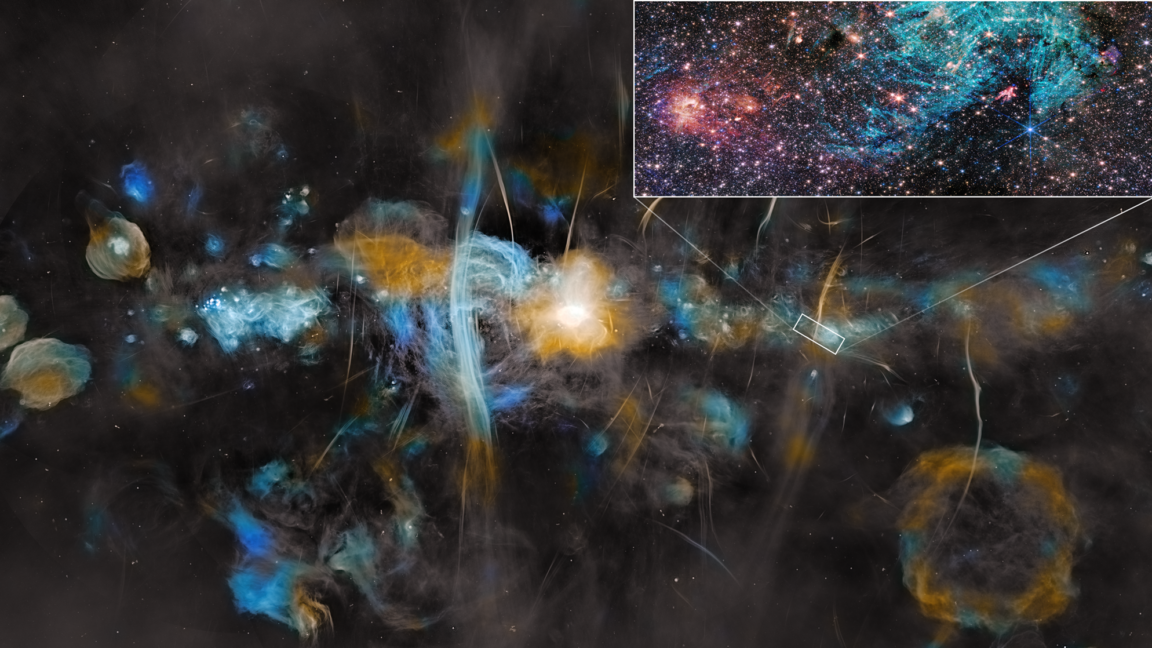

When I was a kid, I was fascinated by the Powers of 10 video, which came out in the 1970s. Perhaps you remember it, with the narrator taking us both outward toward the fathomless end of the Universe and then, reversing course, guiding us back to Earth and inside a proton. The film gave a younger me a good sense of just how large the Universe around us really is.

What I did not know until much later is that the short film was made by the Eames Office, which was founded by the noted designers Charles Eames and Ray Kaiser. It's the same organization that produced the Eames Lounge Chair. It goes to show you the value of good design across genres (shoutout to Ars' resident designer, Aurich Lawson).

Anyway, I say all that because the Power of 10 film continues to live in my head, rent-free, decades later. It was the first thing I thought of when looking at today's image of the Milky Way Galaxy's center. The main image showcases huge vertical filaments, with the supermassive black hole at the galaxy's core clearly visible. This image, captured by a South African radio telescope named MeerKAT, also shows the ghostly, bubble-like remnants of supernovas that exploded over millennia.

Pretend, if you can, that the last week didn’t happen (a tall order for the Stratechery demographic, I know), and imagine another scenario: China invades Taiwan. What happens then?

I’m not a military expert, but my assumption is that China would be successful; the biggest unknown variable would be time. If the U.S. does not intervene the conflict would be shorter; if the U.S. does the conflict would be longer, and ultimately be decided in the way that wars are always decided: through industrial capacity and logistics. China has a meaningful advantage in both areas given its relative manufacturing might and the fact the conflict would happen off their coast.

There are experts who disagree; the Center for Strategic & International Studies ran a series of wargames in 2023, and concluded that the U.S. and its allies would repel a Chinese invasion, but at a heavy cost to U.S. military forces and Taiwan generally. That, however, raises a more pertinent point: when it comes to the economic impact it hardly matters who wins or loses. In both cases China is effectively removed from global supply chains, and Taiwan’s economic output — including chips from TSMC and others — is destroyed.

It’s difficult to overstate the extent to which every aspect of modern life rests on global supply chains, which are so long and complex that no one can truly understand the effects of messing with them. It has, however, gotten easier to grasp the complexity in recent years: first there was the bungled economic response to COVID, where a temporal interruption in supply chains triggered worldwide supply shortages and contributed to global inflation; then there was last week, when the shock of blanket tariffs from the Trump administration led to a meltdown in worldwide stock markets that seems to still be ongoing. A war over Taiwan, however, would put all of these to shame.

Trade and China

Last November, in the wake of President Trump’s second election, I wrote A Chance to Build: that title referenced the optimistic conclusion to a piece that was, if you read closely, a pretty pessimistic summary of the current trade situation, with a special focus on tech. To summarize:

The U.S. leveraged foreign aid, direct investment, and its consumer market to rebuild Europe and Japan after World War 2, and pegged currencies to the U.S. dollar (which was pegged to gold) to do it. This started the cycle of foreign countries exporting to the U.S. and buying U.S. debt with the proceeds, although the U.S.’s relative size to the rest of the world meant that the U.S. still ran a trade surplus (the aid and direct investment were often used to buy U.S.-produced products).

By 1971 this system was about to collapse under its own weight, leading the U.S. to de-peg from gold (i.e. depreciate the U.S. dollar) and dissolve the Bretton Woods system of currency controls. This led to a decade of pain — including the oil shock of the 1970s — but what emerged had a similar structure to the post World War 2 system, just with the U.S. dollar as the reserve currency, untethered from gold. This meant there was inelastic demand for U.S. treasuries, which basically made it impossible for the U.S. to not run a deficit, either in terms of trade or the federal budget. Still, this was maintainable given the relative size of the U.S. economy to its trading partners.

What changed in the last 25 years was the entrance of China into this system. China — clearly in retrospect, although perhaps predictably for those who understood China historically, beyond its backwardness over the previous two centuries — had far more capacity than the system could bear. It’s not an accident that U.S. deficits — both in terms of trade and the federal budget — have exploded in line with Chinese growth.

China is the skeleton key to understand so many oddities about the U.S.’s fiscal situation over the last fifteen years in particular, especially how it is that the U.S.’s response to the Great Recession didn’t lead to inflation: Chinese production was deflationary, and their ever-expanding trade surpluses created an ever-expanding market for U.S. debt, whether it be held by the Chinese national government, provincial governments, state-owned enterprises, etc. This inelastic demand also served to keep the dollar artificially high, in defiance of the theoretical-expected response to long-running trade deficits.

This, more than anything else, is what has hollowed out U.S. manufacturing. The cost of cheap consumer goods and a seeming inexhaustible capacity for U.S. debt was the shifting of ever more manufacturing abroad. Yes, things like lower costs and different labor standards played a role, but it’s the structure of the world economy that matters most; indeed, China’s labor costs are significantly higher than they used to be, but China’s manufacturing dominance is actually accelerating.

Part of this is due to China’s decision over the last few years to respond to the puncturing of its housing bubble by pushing resources into export-oriented industries; another part is the unfortunate reality — under-appreciated by apostles of comparative advantage — that capabilities compound. I wrote in that Article:

The story to me seems straightforward: the big loser in the post World War 2 reconfiguration I described above was the American worker; yes, we have all of those service jobs, but what we have much less of are traditional manufacturing jobs. What happened to chips in the 1960s happened to manufacturing of all kinds over the ensuing decades. Countries like China started with labor cost advantages, and, over time, moved up learning curves that the U.S. dismantled; that is how you end up with this from Walter Isaacson in his Steve Jobs biography about a dinner with then-President Obama:

When Jobs’s turn came, he stressed the need for more trained engineers and suggested that any foreign students who earned an engineering degree in the United States should be given a visa to stay in the country. Obama said that could be done only in the context of the “Dream Act,” which would allow illegal aliens who arrived as minors and finished high school to become legal residents — something that the Republicans had blocked. Jobs found this an annoying example of how politics can lead to paralysis. “The president is very smart, but he kept explaining to us reasons why things can’t get done,” he recalled. “It infuriates me.”

Jobs went on to urge that a way be found to train more American engineers. Apple had 700,000 factory workers employed in China, he said, and that was because it needed 30,000 engineers on-site to support those workers. “You can’t find that many in America to hire,” he said. These factory engineers did not have to be PhDs or geniuses; they simply needed to have basic engineering skills for manufacturing. Tech schools, community colleges, or trade schools could train them. “If you could educate these engineers,” he said, “we could move more manufacturing plants here.” The argument made a strong impression on the president. Two or three times over the next month he told his aides, “We’ve got to find ways to train those 30,000 manufacturing engineers that Jobs told us about.”

I think that Jobs had cause-and-effect backwards: there are not 30,000 manufacturing engineers in the U.S. because there are not 30,000 manufacturing engineering jobs to be filled. That is because the structure of the world economy — choices made starting with Bretton Woods in particular, and cemented by the removal of tariffs over time — made them nonviable. Say what you will about the viability or wisdom of Trump’s tariffs, the motivation — to undo eighty years of structural changes — is pretty straightforward!

The other thing about Jobs’ answer is how ultimately self-serving it was. This is not to say it was wrong: Apple could not only not manufacture an iPhone in the U.S. because of cost, it also can’t do so because of capability; that capability is downstream of an ecosystem that has developed in Asia and a long learning curve that China has traveled and that the U.S. has abandoned. Ultimately, though, the benefit to Apple has been profound: the company has the best supply chain in the world, centered in China, that gives it the capability to build computers on an unimaginable scale with maximum quality for not that much money at all.

That line about Trump’s motivation looms large after the last week; the observation about Apple’s benefits looks much more precarious.

The Nixon Shock

There is a fascinating history of the Nixon administration’s deliberations over closing the gold window, instituting price controls, and imposing a 10% import tax — the actions that effectively ended Bretton Woods — in this 2011 Article in Bloomberg Businessweek. What is interesting is that the decision was made under intense economic pressure, but the presentation was a PR masterpiece:

[Treasury Secretary John] Connally brilliantly packaged the program not as America abandoning its commitment to the gold standard but as America taking charge. He turned the dollar’s collapse, which could have appeared shameful, into a moment of hubris. The emphasis would be on righting America’s trade balance, as well as minor points such as a 5 percent cut in foreign aid. An aide to William P. Rogers, the Secretary of State, called and interjected, “You can’t cut foreign aid.” Connally said, “Tell him if he doesn’t shut up we’ll make the cuts 15 percent.” Shultz muzzled his disquiet over price controls; even Burns joined ranks. The group feverishly debated whether Nixon should address the country on Sunday night, which would mean preempting the popular Gunsmoke. The public relations aspect was paramount. Stein wrote later that the discussion at Camp David assumed “the attitude of scriptwriters preparing a TV special.” No one pretended to know how controls would work; the question was scarcely debated.

Addressing the nation on Sunday, Nixon blamed currency speculators and “unfair” exchange rates rather than U.S. monetary policy. Politically, he hit the jackpot. Monday’s nearly 33-point rise in the Dow was the biggest ever to that point. Nixon’s “New Economic Policy” drew raves from the press. “We unhesitatingly applaud the boldness with which the President has moved,” read the New York Times editorial. In the present era, America’s inability to repair its fiscal problems has tarnished its credibility and hampered its currency negotiations with China. The Nixon Shock showed the U.S. taking action.

The end of Bretton Woods was probably inescapable, but it’s worth pointing out that the Nixon Shock was an economic disaster: the country endured a decade of drastic inflation that was only cured with sky-high interest rates and a massive recession (the architect of that cure, Paul Volcker, was a part of the team that instituted the Nixon Shock in the first place; Volcker came to regret it). In other words, the reaction of the market and the press was totally wrong.

The question is if what happened this last week ought to be compared to the Nixon Shock, or contrasted? Certainly the reaction is a contrast: everyone hates the “Liberation Day” tariffs, including the market. Moreover, the Trump administration’s rollout has been the very opposite of a PR masterpiece: no one in the administration can seem to agree about what exactly the goal is, or what success looks like. I’m certainly not going to attempt to speak for an administration that can’t speak for itself, particularly given Trump’s on-again-off-again approach to tariffs over the last few months.

What I do come back to, however, is what I opened with: there is a scenario within the realm of possibilities that is far more painful than anything Trump proposed; is it better to try and force into place a new economic system that, at least in theory, reduces dependency on China and resuscitates U.S. manufacturing now, instead of waiting for the current system to collapse by literal force? This does seem to be the administration’s goal: simply tariffing China is deadweight loss, leading to rerouting and the fundamental problem of the dollar as reserve currency unaddressed; blanket tariffs, on the other hand, are a valid, if extremely blunt and inefficient, way to meaningfully restructure incentives.1

Moreover, even if an invasion never happens, is the current system sustainable, fiscally or societally? Trump’s political success is, in many respects, the clearest manifestation of what happens in a system that pushes the gains to the globalized top while buying off the localized masses with cheap trinkets.

The Question of Kicking the Can

Ultimately, I actually think there is an important distinction between these downside scenarios, and it explains why I think that Trump’s approach, while more theoretically valid than it is being given credit for, is the wrong one.

First, I’m skeptical that we have the stomach for what would be necessary to remake the global economic order. I might have had to spend a few paragraphs explaining this point previously, but I think a stock market chart speaks for itself:

I will note, by the way, that these losses aren’t entirely irrational or panic-driven: reduced trade absolutely hurts U.S. multinationals; one point that is being missed — at least until what happened in foreign stock markets this morning — is that it hurts foreign companies even more. No one wins in a trade war.

Second, the current economic system, flawed though we may now recognize it to be, is a complex system, built up over decades; one ought to be very wary in remaking complex systems in a top-down manner. It’s one thing to diagnose problems; it’s a very different thing to solve them. There’s a reason that new economic systems usually arise after major wars; it’s easier to build something new after the old thing has been destroyed (and there is the stomach for it, because there is no other choice).

Third, there are a lot of other things the Trump administration could be doing, particularly in terms of relieving regulation, ensuring equal opportunity throughout the economy, etc. It seems like a missed opportunity to be burning political capital on deficit reduction and trade rebalancing when there are major pro-growth opportunities still available. This seems particularly pertinent given the rise of AI, which has very high variance in terms of potential outcomes.

Make no mistake, the structural problems facing U.S. manufacturing in particular are very real, and the China-Taiwan systemic risk is only going to increase. Instead of changing the system to ameliorate the risk, however you could simply address the risk directly; I think the best way to do that is to undo the chip controls and tie China even more tightly into the current system generally, and to Taiwan specifically. Yes, this is kicking the can down the road, but path dependency is a far more powerful force than we often realize.

To go back to the Nixon Shock, I think one reason why it was a PR success is because the crisis was inescapable; I wonder if one reason why “liberation day” is a PR disaster is because there is still more road to kick the can down.

Tech and Tariffs

So what of tech companies, and the benefits that companies like Apple have gotten from Asia generally and China specifically?

First, it is worth articulating this benefit in full. Steve Jobs, in his first tenure at Apple, was deeply committed to manufacturing, including building a futuristic factory in Fremont for the Mac; that merely cost the company millions — his attempt to do the same for NeXT all but drove the company out of business. What Apple needed — and eventually found in China, under Tim Cook — was scalability: Apple would focus its integration chops on getting the product right, and trust contract manufacturers to achieve the flexibility of meeting demand. This, more broadly, is an important addition to the capability discussion above: manufacturing has changed from being a point of integration with a product to being a horizontal scalable services offering; developing the customer service chops necessary for such a business would be a significant cultural challenge for a new U.S. manufacturing base, a la Intel’s struggles to become a foundry.

To that end, one benefit of a war over Taiwan is that it would be so terrible for tech companies that there really isn’t much benefit in planning for it; the hedging cost — which would entail building out these scalable horizontal service providers, which for economic reasons must serve more than one company or product — would be so astronomical that it probably wouldn’t be economical to do anything other than deepen the status quo, particularly given that the status quo contains strong incentives for all parties, including China, to avoid disaster.

These tariffs, however, are much more complicated, because they exist (for now anyways), while a war does not. Apple, which has so adroitly balanced the relationship with both the U.S. and Chinese governments, is obviously the most impacted: you can quibble with the Wall Street Journal’s estimates on the tariff impact on an iPhone, but it certainly is directionally correct that Apple will probably face little choice but to substantially raise prices. That has the direct problem of leading to fewer sales (even if iPhone demand is probably fairly inelastic), and the secondary problem of decreasing the market for Apple’s services business, its primary source of growth.

There’s an even more disappointing knock-on effect: Apple’s services business is not subject to tariffs, which is to say it will become even more important to Apple’s bottom line; that decreases the likelihood that Apple transforms its relationship with developers, which I think is its most promising opportunity with AI.

All of the advertising-based businesses — Meta, Google, and Amazon — will also be negatively impacted. Lots of cheap products means lots of advertising (and lots of products on Amazon specifically), much of which could disappear; could this mean a return of app install advertising, if e-commerce advertising decreases, lowering prices overall? All three companies also source hardware from China, both for sale to consumers and for their data centers. It’s Microsoft and its old formula of software and distribution that may be the most shielded. Of course it needs data center hardware as well, and more expensive PCs means less Windows revenue, but the world of bits has never seemed more attractive relative to atoms.

The problem for all of them, however, is the same problem faced by the economy generally: more grist in the wheels of the economy means lower velocity, and lower velocity is bad for tech companies in particular. These are entities who are predicated on Aggregating unfathomable levels of demand in order to gain leverage on massive up-front costs; now demand will slow even as the costs rise. Moreover, their regulatory risk will likely increase: one way for entities like European countries to retaliate will be to simply ramp up the fines, or figure out a way to tax software services, further slowing velocity; the worst case scenario would be a dedicated effort to break away from U.S. tech completely. I think this is unlikely, but more likely than it was a week ago.

So what of my optimistic spin last November, when I called my tariff preview A Chance to Build? Well, my skepticism is keeping with the pessimism embedded in that piece: it’s a lot easier to build from scratch than to retrofit something that exists; that applies to companies just as much as countries and economic orders. I’ll be cheering for the startups that seize this opportunity; I’m sympathetic to the incumbents looking at guaranteed costs with very uncertain rewards.

I’m setting aside the specific details for now, including the problems Trump’s tariffs pose for manufacturers as laid out in this X post by Molson Hart. ↩

Step into game night glam with the Irregular Choice x MONOPOLY Collection. Bold, glittery heels and playful prints channel classic tokens and Monopoly money, blending nostalgic charm with whimsical fashion for a look that’s anything but by the rules.

Google exprime ses préoccupations concernant l’impact du contenu généré par l’IA sur la qualité du web. Un sujet crucial pour les développeur·se·s et les professionnel·le·s du web qui doivent comprendre les enjeux du SEO face à l’émergence massive des contenus automatisés et leurs implications sur les algorithmes de recherche.

Le Royaume-Uni et les États-Unis développent un moteur pour un missile de croisière hypersonique. Le ministère de la Défense britannique vient d’annoncer que leurs essais en soufflerie sont prometteurs. Comment fonctionne ce type de missile et pourquoi est-ce compliqué à développer ?

Le fossé entre IDE traditionnel et environnement de dev piloté par IA vient de se réduire considérablement ! Si vous codez encore avec vos petits doigts comme un développeur du siècle dernier, il est maintenant temps de passer à la vitesse supérieure !!!

En effet, Visual Studio Code 1.99 vient de sortir et intègre maintenant un mode Agent directement dans le Chat Copilot déjà présent. Cette fonctionnalité qui permet de programmer en langage naturel via un agent IA (le fameux vibe coding… yeeeah Braïce !) est maintenant capable d’effectuer des séries d’actions complexes comme créer plusieurs fichiers, lancer des commandes, faire des recherches, lancer des tests et écrire de la doc en parallèle… Top non ?

Mark Zuckerberg, qui doit bien avoir les boules d’avoir soutenu Trump, essaye de noyer son chagrin dans l’élevage de Lamas. Alors pas des lamas idiots qui chiquent aussi bien que votre belle mère mais plutôt des Lamas numériques à savoir les fameux LLM de Meta, qui pourraient bien révolutionner vos projets persos avec leur nouvelle approche !

Il vient donc d’annoncer la mise à disposition de Llama 4, leur nouveau modèle multi-modal (Il peut comprendre le texte et les images) qui a été entrainé sur près de 30 milliards de tokens (soit + du double de Llama 3) et dispose d’un contexte de 10 millions de tokens. En gros, c’est comme lui passer l’équivalent de 8 000 pages de texte, soit la Bible complète + l’intégralité de la trilogie du Seigneur des Anneaux + le manuel d’utilisation de votre micro-ondes, et il se souviendra de tout en même temps.

Les neurones artificiels sous-estiment-ils la puissance de leurs modèles biologiques ?

Dix ans après de premières prédictions théoriques, des chercheurs et chercheuses ont montré qu'un neurone...

La sixième édition du Baromètre Samsung Smart Retail, réalisée par Infopro Études et Samsung Electronics France, met en lumière les tendances et évolutions du commerce en France. Malgré l'essor du commerce en ligne, les consommateurs français continuent de privilégier les magasins physiques, tout en intégrant de plus en plus les technologies digitales dans leur parcours d'achat. Voici les principaux enseignements de cette étude.

En février dernier, le PDG d’OpenAI, Sam Altman, a partagé la feuille de route pour la sortie de GPT-5. Il a révélé que le puissant modèle de raisonnement o3 ne serait pas disponible en tant que modèle autonome, mais qu’il serait intégré à GPT-5. Aujourd’hui, Altman indique que les modèles de raisonnement o3 et o4-mini […]

L’électronique atteint ses limites. Alors que les modèles d’intelligence artificielle deviennent de plus en plus massifs, connectés et complexes, les géants de la tech et les startups misent désormais sur la photonique pour franchir une nouvelle frontière technologique : transmettre l’information non plus par des impulsions électriques, mais par la lumière. Au cœur de cette …

Après 4 mois d’attente, Meta a sorti une nouvelle série de modèles Llama 4 open-weight. Les nouveaux modèles d’IA sont Llama 4 Scout, Llama 4 Maverick et Llama 4 Behemoth. Contrairement aux précédents modèles denses, Meta a opté cette fois pour l’architecture MoE (Mixture of Experts), tout comme DeepSeek R1 et V3. Tous les modèles […]

A British startup called Pulsar Fusion has come up with a wild new concept for a nuclear fusion-powered space rocket that, it claims, could significantly cut down the time it takes to travel to Mars in half.

As CNN reports, the UK Space Agency-funded company's Sunbird rocket harnesses the power of nuclear fusion, the same process that powers stars, as a form of propulsion.

"It’s very unnatural to do fusion on Earth," Pulsar founder and CEO Richard Dinan told CNN. "Fusion doesn’t want to work in an atmosphere. Space is a far more logical, sensible place to do fusion, because that’s where it wants to happen anyway."

It's important to note that the propulsion device is still almost entirely theoretical. But Pulsar sees potential.

The firm is hoping to achieve fusion in orbit for the first time in 2027, a moonshot plan that could put far-flung destinations in our solar system within much easier reach — if everything goes perfectly according to plan, at least.

Instead of splitting atoms to release copious amounts of energy, fusion energy involves combining isotopes into heavier ones. For decades, scientists have tried to replicate this process inside special reactors, using immense amounts of heat and pressure.

Turning that idea into a viable source of renewable energy has proven extremely difficult, particularly at a meaningful scale. Scientists are still breaking their heads over how to do so efficiently, and are only starting to devise methods that allow them to harvest more energy than what they had to put in to get the reaction started.

In space, however, where fusion reactors in the form of stars and our Sun, are abundant, the situation could look quite different. Instead of having to harness the swirling plasma inside circular reactors, Pulsar Fusion's rocket would have a "nuclear exhaust," shooting out protons from an expensive type of fuel called helium-3.

In the long run, Pulsar Fusion envisions an entire gas station-like system.

"We launch them into space, and we would have a charging station where they could sit and then meet your ship," Dinand told CNN. "You turn off your inefficient combustion engines, and use nuclear fusion for the greater part of your journey."

"Ideally, you’d have a station somewhere near Mars, and you’d have a station on low Earth orbit," he added, "and the (Sunbirds) would just go back and forth."

As Live Science reports, each Sunbird would be around 100 feet in length and feature "tank-like" armor plating to protect them from cosmic radiation and micrometeorites. Each rocket could cost upwards of $90 million, a steep price in large part due to its unusual fuel source.

For its inaugural proof of concept test in 2027, the company is hoping to construct a "linear fusion experiment" to test "key technological components." A fully functional prototype could be ready four to five years after that — if the company doesn't run out of funding by then.

"If we are going to be the species that actually get to other planets, then exhaust speeds are pretty much the most important thing," Dinan said during a space convention earlier this year, as quoted by Live Science. "In terms of what can be [theoretically] produced in exhaust speeds, fusion is king."

OpenAI's latest image-generating 4o model is surprisingly good at generating text inside images, a feat that had proved particularly difficult for its many predecessors.

And that makes it a powerful tool for generating images of fraudulent documents, as users have found.

"You can use 4o to generate fake receipts," Das wrote. "There are too many real-world verification flows that rely on 'real images' as proof. That era is over."

Doc Holiday

The image itself, at first blush, is pretty convincing and includes a breakdown of a multicourse meal, a correct subtotal, and even a tip calculation.

Another user even managed to edit the image further by adding a realistic filter and food stains — the perfect way to commit expense fraud, if you were so inclined.

And that's the tip of the iceberg. Das also found that 4o was happy to generate fraudulent prescriptions for controlled substances like Zoloft.

Fraud Squad

The development highlights how far AI-powered image generators have come. Previous models infamously struggled with recreating letters, often resulting in garbled shapes and unintentionally hilarious phrases.

Beyond faking expenses for lavish meals, OpenAI's increasingly canny ability to generate fake documents could open up the door for everything from phony tax forms and bank cheques to fake IDs and birth certificates.

Whether our ability to detect this storm of faked documents remains to be seen. But given AI companies' current efforts, it's not looking good. Guardrails like appended metadata or watermarks that divulge whether an image was generated by an AI are easily overcome.

Even before the advent of powerful AI-powered image generators, a 2015 survey found that 85 percent of respondents admitted to lying to get reimbursed with more money. Many of these kinds of fraud cases fall through the cracks due to a lack of internal controls and flawed accounts payable processes.

In other words, you can no longer believe anything you see online.

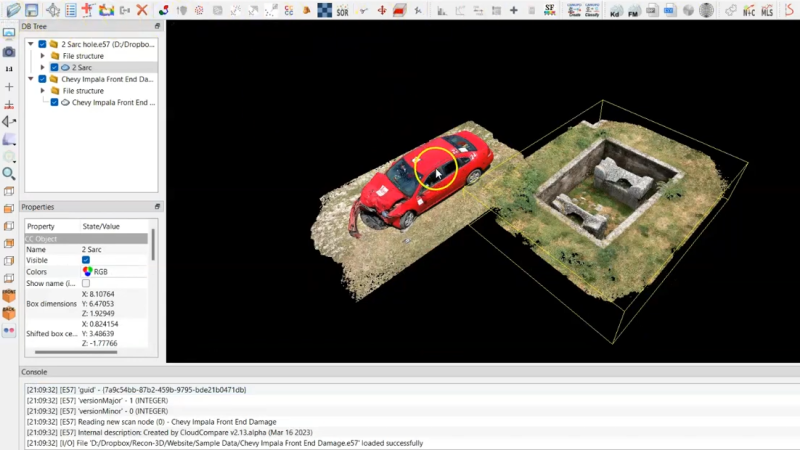

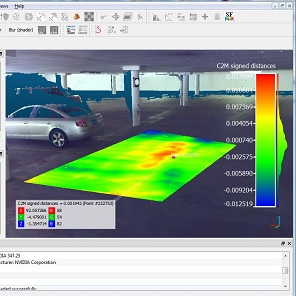

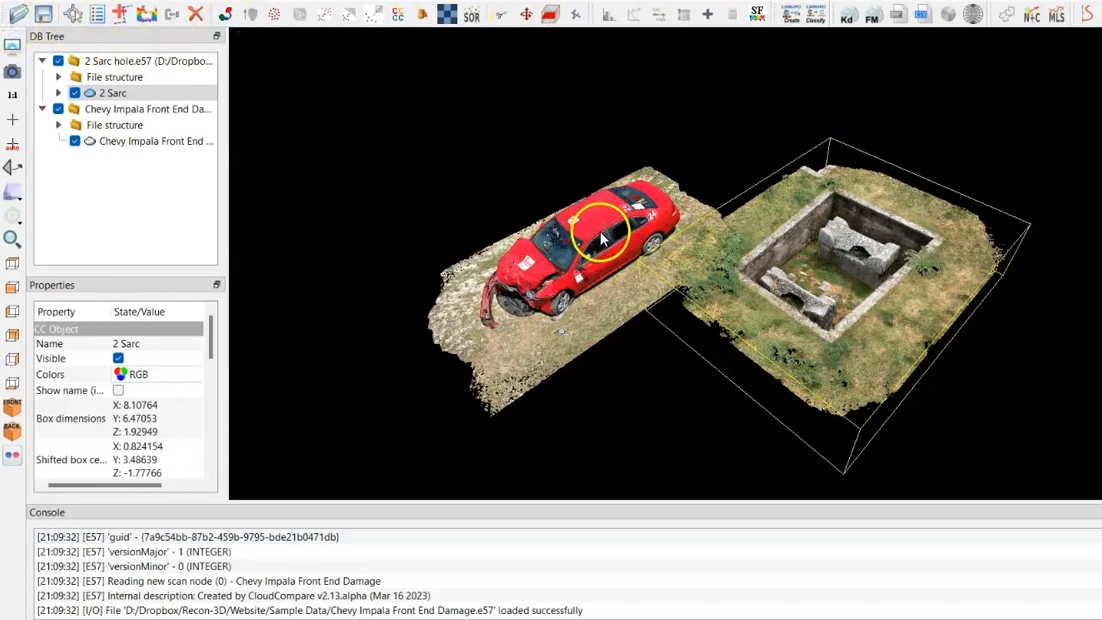

3D scanning is becoming much more accessible, which means it’s more likely that the average hacker will use it to solve problems — possibly odd ones. That being the case, a handy tool to have in one’s repertoire is a way to work with point clouds. We’ll explain why in a moment, but that’s where CloudCompare comes in (GitHub).

Not all point clouds are destined to be 3D models. A project may call for watching for changes in a surface, for example.

CloudCompare is an open source tool with which one can load up and do various operations on point clouds, including generating mesh models from them. Point clouds are what 3D scanners create when an object is scanned, and to become useful, those point clouds are usually post-processed into 3D models (specifically, meshes) like an .obj or .stl file.

We’ve gone into detail in the past about how 3D scanning works, what to expect from it, and taken a hands-on tour of what an all-in-one wireless scanner can do. But what do point clouds have to do with getting the most out of 3D scanning? Well, if one starts to push the boundaries of how and to what purposes 3D scanning can be applied, it sometimes makes more sense to work with point clouds directly instead of the generated meshes, and CloudCompare is an open-source tool for doing exactly that.

For example, one may wish to align and merge two or more different clouds, such as from two different (possibly incomplete) scans. Or, you might want to conduct a deviation analysis of how those different scans have changed. Alternately, if one is into designing wearable items, it can be invaluable to be able to align something to a 3D scan of a body part.

It’s a versatile tool with numerous tutorials, so if you find yourself into 3D scanning but yearning for more flexibility than you can get by working with the mesh models — or want an alternative to modeling-focused software like Blender — maybe it’s time to work with the point clouds directly.

Usually when we talk about retrocomputing, we want to look at — and in — some old hardware. But [Z→Z] has a different approach: dissecting MacPaint, the Apple drawing program from the 1980s.

While the program looks antiquated by today’s standards, it was pretty hot stuff back in the day. Things we take for granted today were big deals at the time. For example, being able to erase a part of something you drew prompted applause at an early public demo.

We enjoyed the way the program was tested, too. A software “monkey” was made to type keys, move things, and click menus randomly. The teardown continues with a look inside the Pascal and assembly code with interesting algorithms like how the code would fill an area with color.

The program has been called “beautifully organized,” and [Z→Z] examines that assertion. Maybe the brilliance of it has been overstated, but it did work and it did influence many computer graphics programs over the years.

After The New York Times sued OpenAI in December 2023—alleging that ChatGPT outputs violate copyrights by regurgitating news articles—the ChatGPT maker tried and failed to argue that the claims were time-barred.

According to OpenAI, the NYT should have known that ChatGPT was being trained on its articles and raised its lawsuit in 2020, partly because of the newspaper's own reporting. To support this, OpenAI pointed to a single November 2020 article, where the NYT reported that OpenAI was analyzing a trillion words on the Internet. But on Friday, US district judge Sidney Stein disagreed, denying OpenAI's motion to dismiss the NYT's copyright claims partly based on one NYT journalist's reporting.

In his opinion, Stein confirmed that it's OpenAI's burden to prove that the NYT knew that ChatGPT would potentially violate its copyrights two years prior to its release in November 2022. And so far, OpenAI has not met that burden.

Le 4 avril 2025 marque le 50e anniversaire de Microsoft, une entreprise qui a profondément façonné l’histoire de l’informatique. Dans cet épisode, retour sur les grandes étapes de cette success story hors normes, des débuts modestes à Albuquerque à l’hégémonie mondiale.

Tout commence en 1975, lorsque deux jeunes passionnés, Bill Gates et Paul Allen, lancent Micro-Soft pour développer un langage de programmation destiné à l’Altair 8800, l’un des tout premiers micro-ordinateurs. Leur intuition géniale : parier sur l’ordinateur personnel.

On revient sur les moments clés : le deal historique avec IBM pour MS-DOS, la révolution Windows 95 et le passage au tout-logiciel avec la suite Office. L’épisode aborde aussi les échecs notables — du Zune à Windows Vista — qui n'ont pas empêché l'entreprise de se réinventer à chaque fois.

Aujourd’hui, Microsoft est un acteur majeur du cloud et de l’IA, avec Azure et Copilot, sous la direction de Satya Nadella. Plus discret, Bill Gates se consacre désormais à sa fondation, mais son rêve d’un ordinateur dans chaque foyer s’est largement réalisé… non sans poser de nouvelles questions de souveraineté technologique.

Fashion is found on runways, shop windows and the accounts of social media influencers. Until recently, Varun Grover, Distinguished Professor at the Sam M. Walton College of Business, and other information systems researchers had considered fashion and technology uncomfortable bedfellows.

It looks like voice AI may have found its sweet spot: ordering fries with that.

Yum! Brands — which owns Taco Bell, KFC, and Pizza Hut and has a larger restaurant footprint than any other company globally — recently announced a partnership with Nvidia to deploy AI (including AI voice ordering) throughout hundreds of restaurants starting in April.

Voice AI stands to reduce labor costs in high-turnover positions while also increasing order throughput and accuracy. It also means staff can be redeployed to food preparation or customer service roles that drive higher satisfaction.

But fast food is just the tip of the iceberg for voice AI.

Get the world’s best tech research in your inbox

Billionaires, CEOs, & leading investors all love the CB Insights newsletter

Below, we get into:

Why voice AI matters

Market maturity

Challenges to adoption

Why does voice AI matter?

For customer interactions, voice conversations offer a far more expressive mode of communication than text-based channels.

Yet the industry remains stuck in a purgatory of robo-call decision trees and endless holds. 62% of customer calls to SMBs go unanswered, while upwards of 70% of business calls that connect still end up putting customers on hold, with most hanging up within minutes.

Advances in AI speech models could break this cycle. Voice AI models are shifting toward processing audio directly — rather than needing to translate it to text, process it using an LLM, then convert it back into speech — and are getting closer to the cadence of human conversation (<300ms latency).

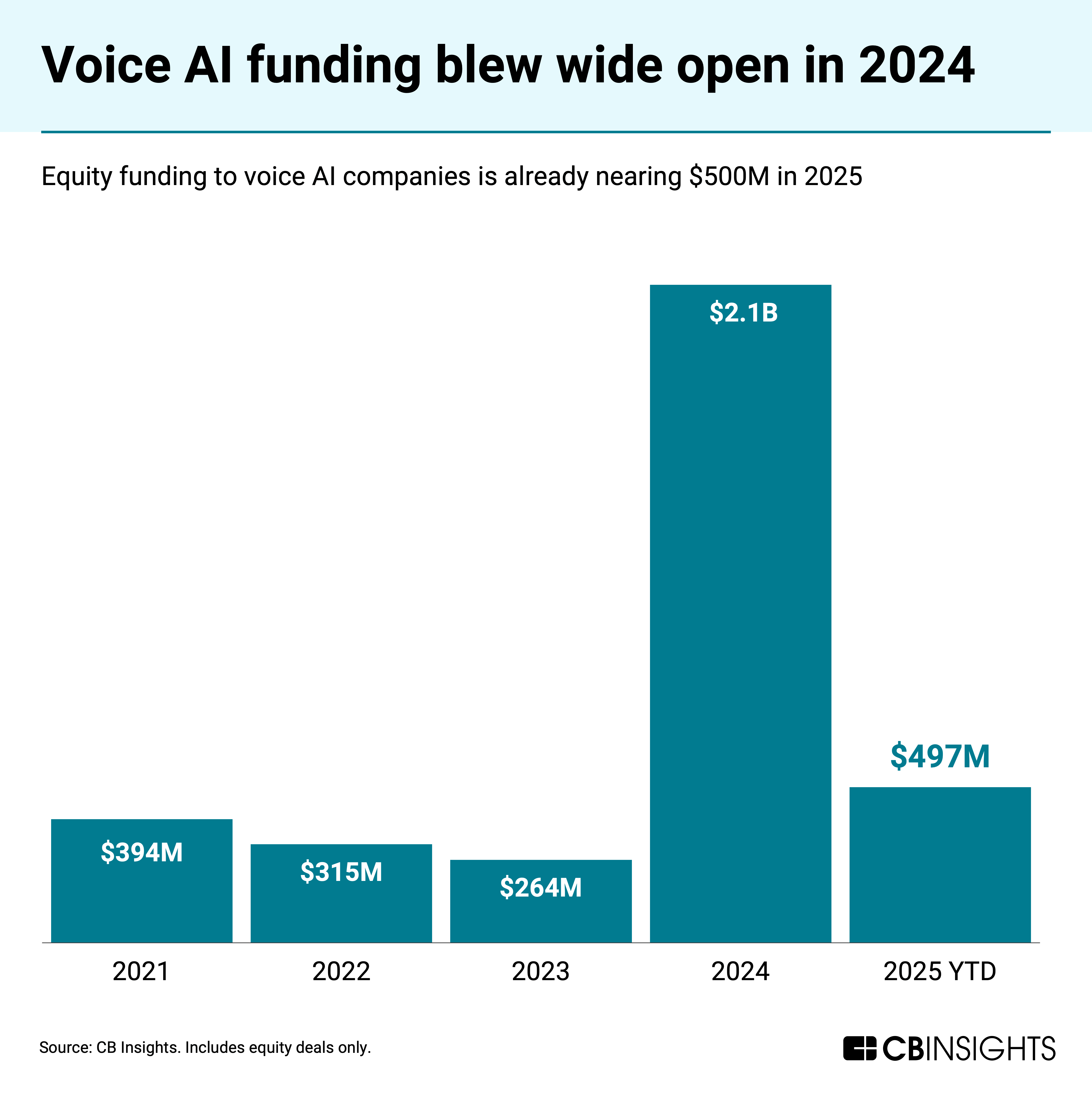

The progress has fueled a surge in equity funding to voice AI solutions, which grabbed $2.1B in 2024, per CB Insights’ funding data. Momentum has continued in 2025 so far, with companies raising nearly $500M in Q1’25.

ElevenLabs‘ $180M round from investors including a16z, Salesforce Ventures, and Sequoia Capital was a big part of this year’s strong start. ElevenLabs has already hit $100M in ARR — just 3 years after its founding.

On the whole, though, the voice AI market remains in its early stages — and faces growing pains.

The market is still nascent

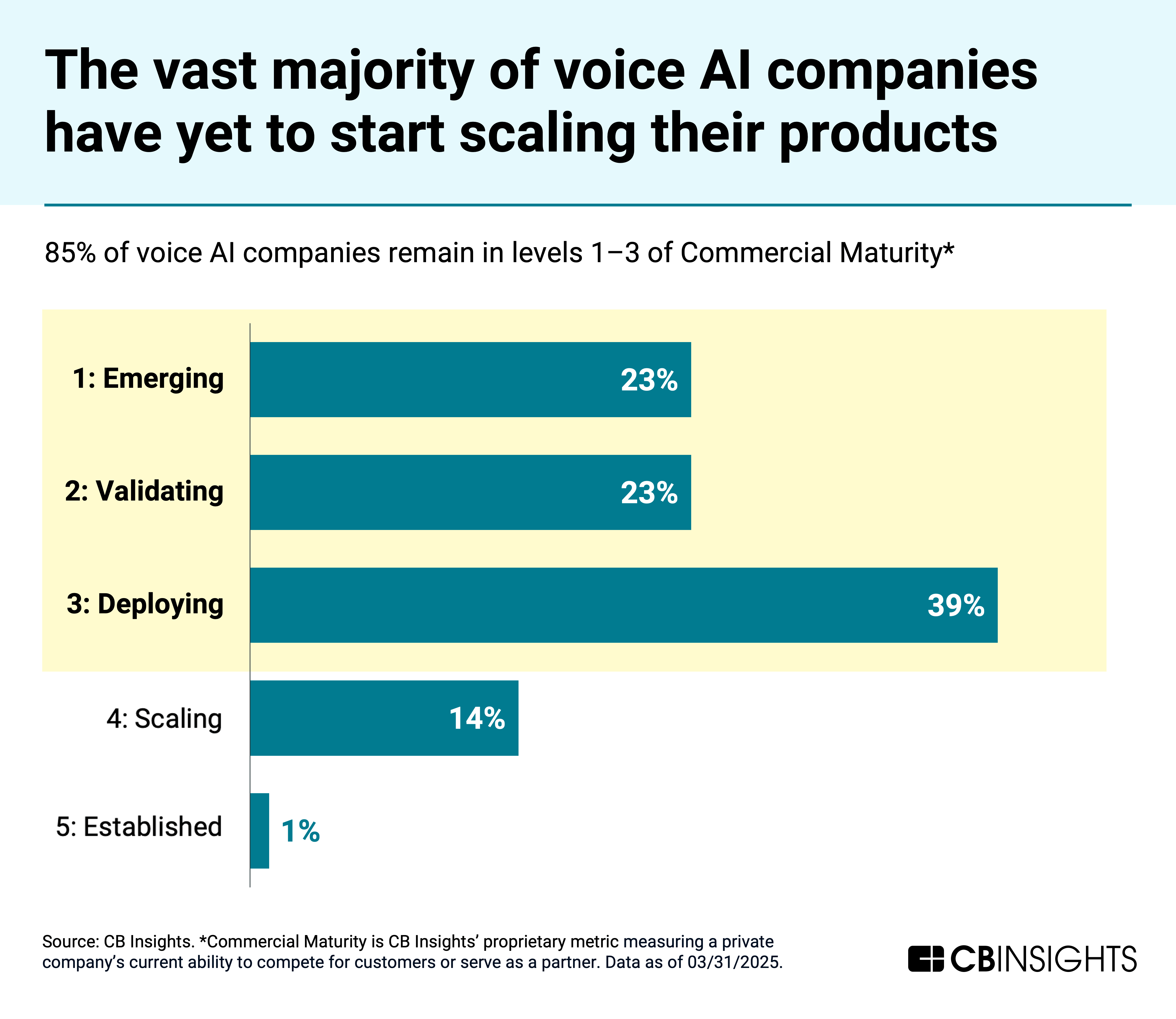

Most of the voice AI market remains in the earlier stages of commercial maturity, with 85% in levels 1, 2, or 3 on CB Insights’ Commercial Maturity scale. More than half are still developing or validating their products, while 39% are beginning commercial distribution and starting to gain customers.

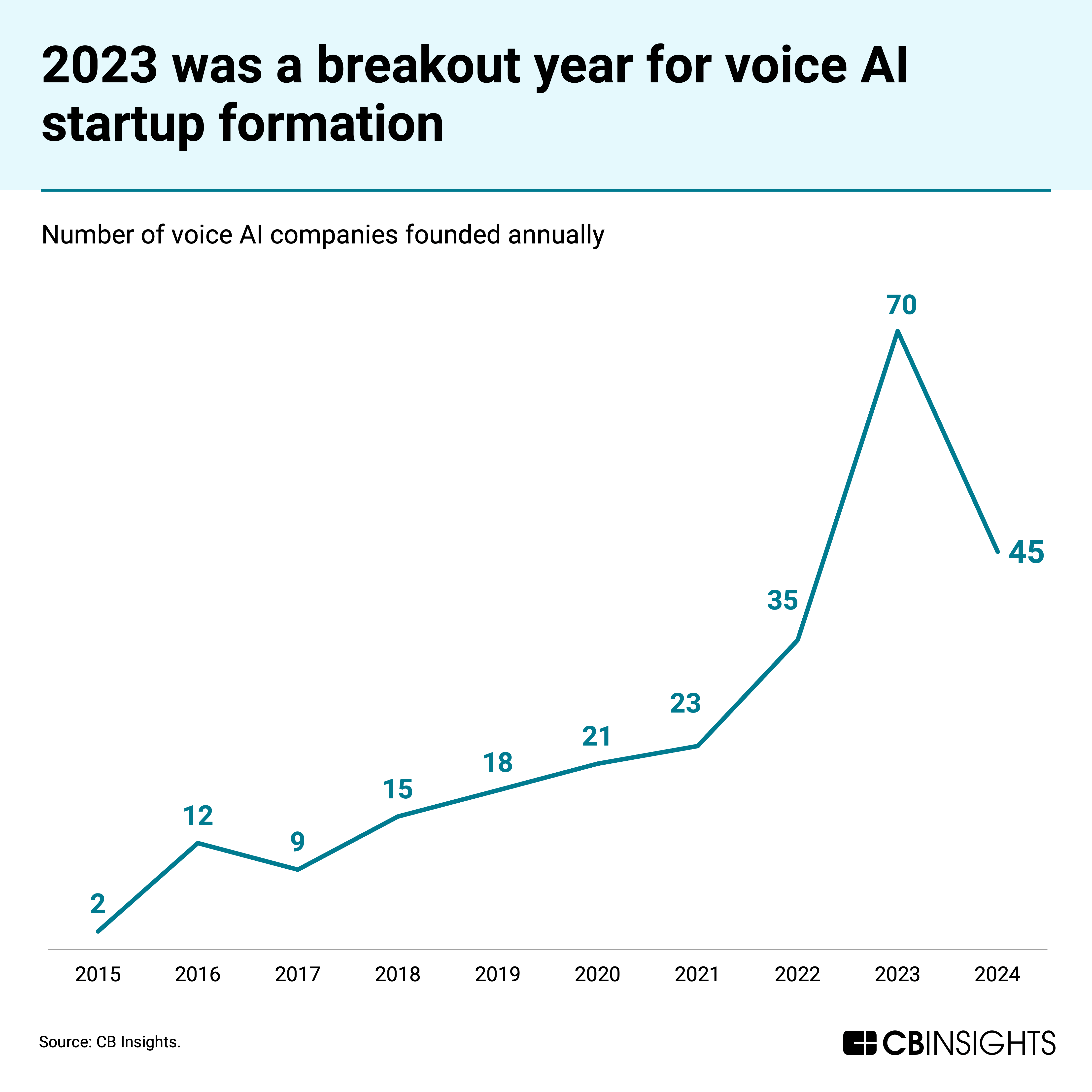

Most startups here were founded in just the last 3 years, as the chart below demonstrates. 2023 was a breakout year, seeing the number of companies founded grow 2x year-over-year, from 35 to 70.

This growth has been driven by advancements in voice AI models — including OpenAI‘s Realtime API for speech-to-speech applications, launched in late 2024 — which jumpstarted applications across use cases.

Despite the excitement, challenges remain around reliability and trust.

Voice AI agents still struggle with complex conversations and unpredictable inputs, leading most enterprises to start out by deploying them in low-stakes scenarios.

In theory, fast-food ordering should be a natural fit — interactions are brief and highly predictable. The AI only needs to understand a limited vocabulary of items and modifiers.

But the reputational risk of even the occasional mishap can be high. McDonald’s, for instance, started a voice AI pilot with IBM back in 2021, but pulled it in 2024 after videos of inaccurate orders went viral on TikTok.

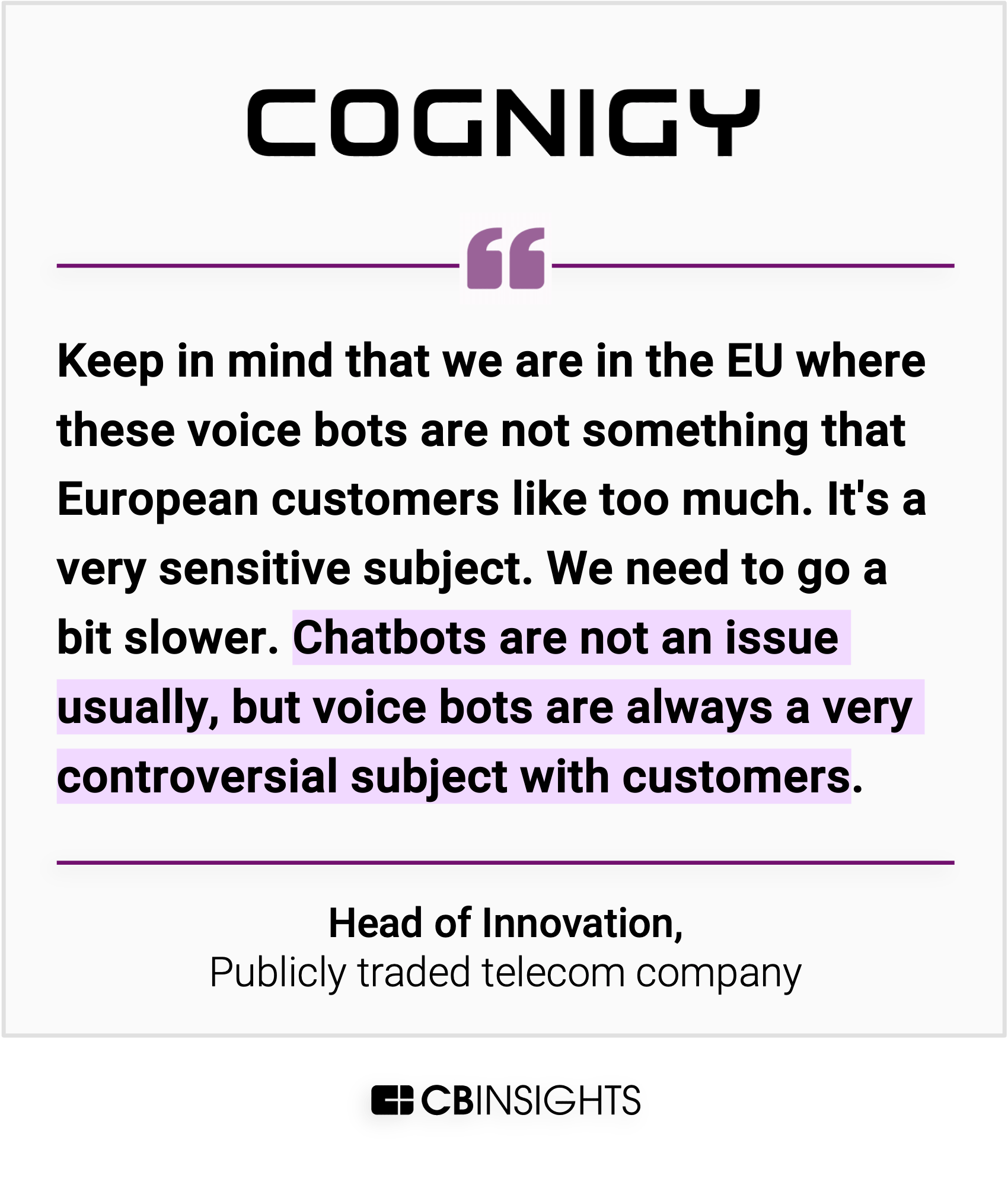

Customer acceptance of voice AI interaction also varies dramatically by region. As one Cognigy customer told us:

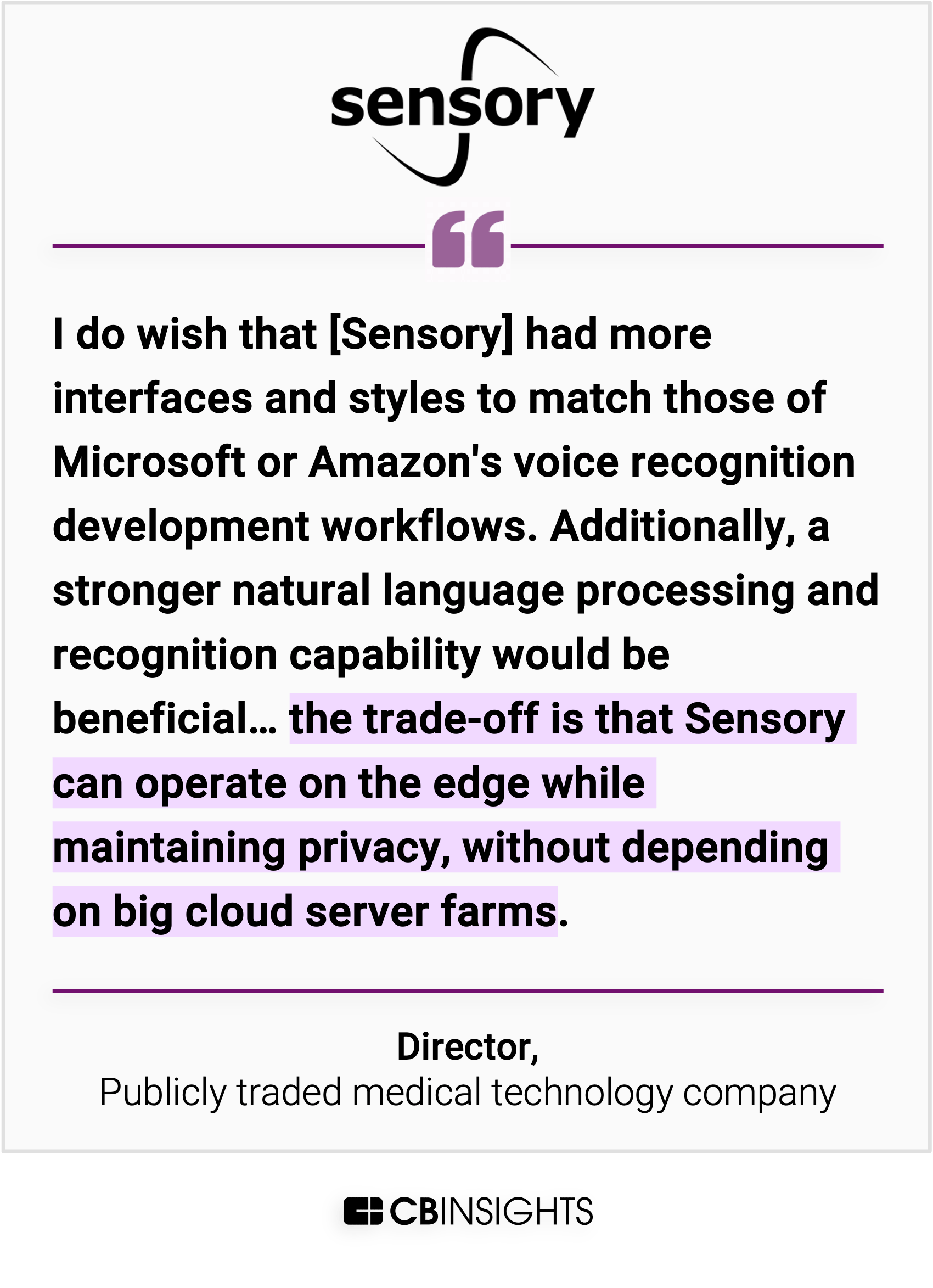

Meanwhile, a strategic divide is emerging in the voice AI market: cloud vs. edge processing.

Cloud-based solutions from tech giants offer advanced capabilities but raise privacy concerns, while edge-based platforms process data locally with better privacy but more limited features.

This divide will shape which players win in different sectors, with edge solutions likely dominating in sensitive industries like healthcare and financial services, while cloud platforms prevail in consumer and retail applications.

For more on how AI will shape every aspect of the customer experience, get the free report here.

Dans cette interview, Mina Ghobrial revient sur son parcours atypique dans le domaine de la réalité augmentée, commencé en 2020. Ce qui n’était au départ qu’un stage de fin d’études ...

OpenAI’s new image-generation feature is on track to be one of the company’s most popular product launches ever. According to Brad Lightcap, who oversees day-to-day operations and global deployment at OpenAI, over 130 million users have generated more than 700 million images since the upgraded image generator launched in ChatGPT on March 25. “[W]e appreciate […]

The global artificial intelligence market is projected to reach $4.8 trillion—roughly the size of Germany's economy—by 2033, the UN said Thursday, warning nearly half of jobs worldwide could be affected.

OpenAI will soon offer its Deep Research feature, which allows for extended AI research tasks, to free ChatGPT users, expanding access beyond paid subscribers.

C’est officiel : Neuralink implantera sa toute première puce Blindsight dans le cerveau d’un patient humain d’ici la fin de l’année 2025. L’annonce, confirmée par Elon Musk sur X, marque un tournant décisif non seulement pour l’entreprise, mais pour la neurotechnologie dans son ensemble. Il ne s’agit plus seulement de bouger un curseur par la pensée...

Federal Trade Commission Chairman Andrew Ferguson said he's keeping an eye on 23andMe's bankruptcy proceeding and the company's planned sale because of privacy concerns related to genetic testing data. 23andMe and its future owner must uphold the company's privacy promises, Ferguson said in a letter sent yesterday to representatives of the US Trustee Program, a Justice Department division that oversees administration of bankruptcy proceedings.

"As Chairman of the Federal Trade Commission, I write to express the FTC's interests and concerns relating to the potential sale or transfer of millions of American consumers' sensitive personal information," Ferguson wrote. He continued:

As you may know, 23andMe collects and holds sensitive, immutable, identifiable personal information about millions of American consumers who have used the Company's genetic testing and telehealth services. This includes genetic information, biological DNA samples, health information, ancestry and genealogy information, personal contact information, payment and billing information, and other information, such as messages that genetic relatives can send each other through the platform.

23andMe's recent bankruptcy announcement set off a wave of concern about the fate of genetic data for its 15 million customers. The company said that "any buyer of 23andMe will be required to comply with our privacy policy and with all applicable law with respect to the treatment of customer data." Many users reacted to the news by deleting their data, though tech problems apparently related to increased website traffic made that process difficult.

There are a remarkable number of commercial fusion power startups, considering that it's a technology that's built a reputation for being perpetually beyond the horizon. Many of them focus on radically new technologies for heating and compressing plasmas, or fusing unusual combinations of isotopes. These technologies are often difficult to evaluate—they can clearly generate hot plasmas, but it's tough to determine whether they can get hot enough, often enough to produce usable amounts of power.

On the other end of the spectrum are a handful of companies that are trying to commercialize designs that have been extensively studied in the academic world. And there have been some interesting signs of progress here. Recently, Commonwealth Fusion, which is building a demonstration tokamak in Massachussets, started construction of the cooling system that will keep its magnets superconducting. And two companies that are hoping to build a stellarator did some important validation of their concepts.

Doing donuts

A tokamak is a donut-shaped fusion chamber that relies on intense magnetic fields to compress and control the plasma within it. A number of tokamaks have been built over the years, but the big one that is expected to produce more energy than required to run it, ITER, has faced many delays and now isn't expected to achieve its potential until the 2040s. Back in 2015, however, some physicists calculated that high-temperature superconductors would allow ITER-style performance in a far smaller and easier-to-build package. That idea was commercialized as Commonwealth Fusion.

{kind=link}

{kind=link}

{kind=link}