In the quest to become wealthy on a finite income, your savings rate dominates all other factors. Because of that, this blog tends to fixate on living happily and efficiently, and the oddly magical lifestyle changes that allow you to drop your spending dramatically even while improving every area of your life.

In the quest to become wealthy on a finite income, your savings rate dominates all other factors. Because of that, this blog tends to fixate on living happily and efficiently, and the oddly magical lifestyle changes that allow you to drop your spending dramatically even while improving every area of your life.

However, this can lead to a one-sided perspective.

Case A: The Badass Cash-Hoarder

“I can Save like a Madwoman, but I’m afraid to Invest. I have been leading a very efficient lifestyle for most the past eight years, and I’ve mastered the year-round bike commute and the year-round garden. My house is paid off and I have $125,000 in CDs yielding 1% right now and another $150k in the savings account. Is it really a good idea to dump all this into investments that I know nothing about?

Case B: The High-Earning Sensible but Oblivious Guy

“My profession pays well, and I have always lived at less lavish standards than my coworkers. Because of this, we’ve saved up a comfortable nest egg of just over $1 million, invested in a mixture of 401(k), IRA, and taxable account Vanguard index funds. The problem is, I have no idea if this is enough to see us through retirement.

These people have got the savings rate thing down, and thus they are able to accumulate money. But each one is missing one of the key nuts and bolts of wealth and early retirement:

- You must know how much you are spending

- You should have a good idea of your net financial worth

- You must invest your savings productively, rather than just stuffing them under the virtual mattress of a 1% savings account or certificate of deposit.

For several months, I’ve been using a new service called Personal Capital that addresses all of these things in a fairly motivating manner. Fairly similar to Mint at first glance, this is one of those smooth and glossy programs that automatically collects all your account balances, investments, and spending in one place. You can then log in very quickly and review all your financial transactions at both the high and low levels, to see what you’ve been earning and spending.

I find both Mint and Personal Capital to be significant life simplifiers, because they make things automatic. Instead of keeping track of 10 passwords and trying to make the rounds of every financial account on a regular basis, I now just tap the Personal Capital icon on my phone, enter a numerical PIN, and begin scrolling through the colorful graphs and pie charts of the family’s financial details. Net worth, every spending transaction, and investment allocation and performance.

I already liked Mint and have been recommending it for years, so I was initially skeptical when a Personal Capital representative got in touch with me through this blog, obviously hoping that I would start using the product. What’s the competitive edge? Is it worth switching from Mint or using both? What is the company’s revenue model and is it aligned with the best interests of the potential customers? I did a bit of research and noticed everyone else had already tried out the company and written reviews. So I decided the best way to verify everything was to throw myself into the system as a customer and soak up the experience for a few months.

Over time, I have come to appreciate what the product and the company offers. My visit to their site (or the phone app) has become a favorite stop on my weekly roundup of the MMM household finances, and thus I figured it is worth sharing a few notes here, in case it motivates any new readers to become more active in tracking their own spending and freeing money from the mattress.

The Interface

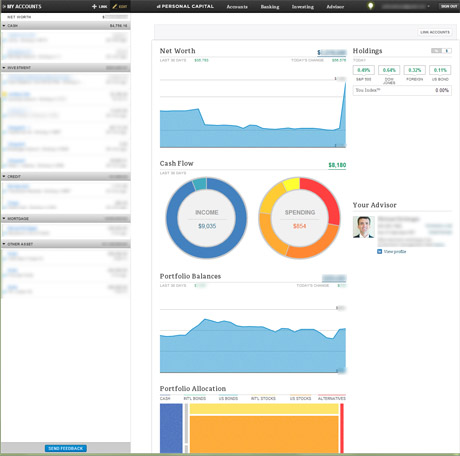

The desktop version of Personal capital has the most features and is the easiest to use. Linking in all your accounts is particularly smooth: click the ‘+’ button, fill out the credentials boxes, and click done. Vanguard, Capital One 360, Lending Club, Your 401(k), your mortgage. Everything updates instantaneously and within a few minutes you have a full picture of your net worth. You are then presented with your “Dashboard”, a screen that gives you your Net Worth, Cash Flow, Portfolio Balances, looks something like this:

Your accounts are down the left, income and spending are front and center, and clicking on anything lets you zoom in on the details of what makes up that category. For example, when confronted with the screen above, I was shocked to see $9000 of income and only $854 of spending in the past 30 days. This is an unusual performance even by MMM household standards. However, zooming in I was able to see the rare events that caused this anomaly (a check came in from the business, I spent 11 days in Ecuador and thus the hungriest member of the family was not at home consuming groceries, and we just happened to buy no products or gasoline last month).

When comparing to Mint, Personal Capital gets the nod for the most useful starting screen. Mint opens with a busy text page – the left column is the same with all your accounts. But the right is “Alerts”, “Advice”, “Bills”, “Budgets”, “Goals”, and other things that may be useful to people other than me.

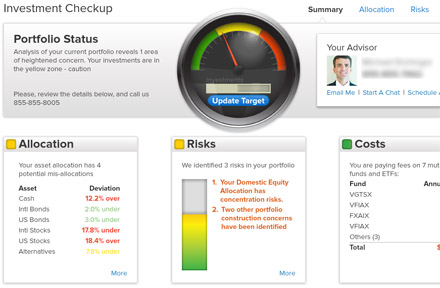

The battle of screenshots could take up several articles in itself, and each company has its advantages. Mint has a better graph of “spending over time” and nicer-looking pie charts in some areas. Personal capital does a more detailed analysis of your investments, identifying the amount you lose to fees each year, and how the assets are allocated compared to their version of an ideal portfolio. I’m particular fond of the “Investment Checkup” feature:

In my case, I get bad marks because I have raided my stock portfolio over the last few years to buy too many houses, and the allocation remaining behind is not very well thought-out. However, their guidelines are solid and if you just follow the recommendations you will probably do better than most of the investing public.

These differences in website model and focus are deliberate, and they are caused by the differences of the underlying business model of the two companies.

Mint is a free service, and it earns its money by advertising financial products that may be relevant to you based on your life situation. Credit cards, savings and investment accounts, insurance, and other stuff. Although the product links are noticeable, they are generally relevant and quite possibly useful to Mint users, so they do not bother me.

Personal Capital is also free to use, and has no ads and pushes no products. Instead, they are hoping to build enough trust that you will hire them to manage your investments for you, in exchange for a fixed-percentage fee of about 0.9% of your managed assets. The only sales pitch is a call or email one of their advisers will send to you after you first set up your account and link in your various funds. And this call only comes if you have over $100,000 of assets available to manage.

This all sounded pretty mysterious to me, so I decided to dig a little deeper over the summer.

- On the one side of the argument, I feel that low fees are essential to investment returns – my own investments are in Vanguard funds where the expense ratio is typically about 0.1%. Mutual funds with management fees over 1%, and hedge funds, are generally very poor bets.

- On the other hand, money that people leave uninvested like the cash-hoarder above is completely unproductive and an even worse bet than a high-fee mutual fund.

- And the Wild Western investment style that many beginners play with (“I bought some Apple, Netflix, Tesla, and a few penny stocks but I jumped out of them and went to Gold when I heard there would be a government shutdown“), is an even more disastrous approach.

If you add in their understanding of tax strategy and asset allocation, it is easy to imagine how an advisory service like Personal Capital could much more than pay for the 0.9% that they would charge if you add that option on to the otherwise-free service. But if you are like me and love managing your own investments, you will stick with a little basket of Vanguard admiral funds and watch over them yourself, rebalancing occasionally.

And Personal capital is far from the only manager out there. For example, after I first published this article, many readers came out with favorable reviews for Betterment (automatic investment in existing index funds with lower management fees, in exchange for less personalized service), so do your research before signing up with any paid financial management service.

But instead of turning down the offer, I followed through with the adviser. Through a series of calls and emails, I got to speak with a very knowledgeable financial guy around my age, who happened to be located in PC’s Denver office. After politely grilling him with a long list of somewhat skeptical questions, I learned that Personal follows a relatively passive, index-based strategy. They maintain their own mostly-passive portfolio of stocks representing the US and international economies.

But their twist on investment philosophy is that indices like the S&P 500 are capitalization weighted, so you’ll get a lot more Wal-mart than Whole Foods, and become heavily weighted in tech stocks when Apple is flying high. So instead, they allocate your assets more evenly across sectors and sizes, which effectively makes you buy stocks lower and sell higher.

Indexing purists like me raise an eyebrow at any strategy that suggests it might beat the market, but at least their principles are sound and I would not expect this strategy to differ much from overall market returns. Their slogans of “We don’t look for home runs”, and “You can’t beat the market by picking stocks”, are very reassuring in this regard. While their own statistics show their funds outperforming the market slightly in recent years, I generally need to see at least a 20-year graph that includes both booms and busts before I will agree that any given strategy is giving the overall index a run for its money.

Summary:

After five months of skepticism and trial, I have to reluctantly admit that this company is a worthwhile addition to the modern financial landscape. While not a clear win over Mint in all areas, I feel that Personal Capital is a much better investment monitor, and works as an interactive teacher in that area as well. Plus, it is still a fun way to track your spending and net worth, and even the paid asset management is worth considering for people who aren’t naturally interested in managing their own investments. Especially if you would prefer to have a real person around to consult with on financial matters, rather than a collection of books and websites with graphs as oddball engineers like myself choose.

After all, you must understand your spending and you must invest your money, so removing any roadblocks to those goals is important.

If you decide to add this financial tool to your own belt, you can do so using the image below (which will benefit this blog, and thanks!)

And if you have your own experiences to share in the Personal Capital vs. Mint battle, please share them in the comments.