Why do we need more farmers? What is the driving force behind U.S. Department of Agriculture policy?

Why do we need more farmers? What is the driving force behind U.S. Department of Agriculture policy?

Submitted by Chris Martenson via Peak Prosperity,

So let's pretend for the moment that the Federal Reserve gets everything it has stated it wants. And even further: that Washington, D.C. gets everything it wants, too.

The credit markets are repaired, and massive new loan growth flows out the door. Loans are made to businesses that hire gobs of new people. Consumers borrow and borrow some more to go to school and buy homes, cars, and gadgets.

Inflation remains low and job growth explodes. Tax receipts climb and the deficit falls. The stock market goes higher and higher, gold falls and then falls some more, as confidence in the system, its masters, and its institutions grows.

The Fed wins and D.C. wins.

But in reality, we all lose.

It's all just a matter of timing.

If we hold the view that humans are behaving unsustainably in terms of any of the 'three Es' – the economy, energy, or the environment – then any rapid resumption to a paradigm of exponential growth in our consumption of natural resources -- or in our growth of debt over income -- simply takes us more quickly to the bitter end of this story.

What good does it do to return to rapid economic expansion if we have not figured out how we are going to supply sufficient water for agriculture and basic living needs to the major population centers around the world? What's our plan for reversing collapsing oceanic fisheries? When do we have the substantive conversation about the long-term implications of the continuing Fukushima disaster?

Omnipresent signs of ecosystem stress -- ranging from dying bees to increasingly chaotic weather patterns -- suggest strongly that we need to be doing things differently and with an eye towards resilience. On the energy front, the temporary bonanza of oil and gas from US shale plays is just that: temporary. We need to be talking about where we want to be positioned when that, too, ends.

The really big picture here is that our economy, such as it is, is predicated on ever larger amounts of stuff being extracted, refined, produced, and then discarded. It's a model that works -- just not sustainably.

Instead of wondering where we're headed and engaging in a bit of introspection, all eyes are on the Fed to see if it can engineer higher stock prices while keeping interest rates low. So conditioned are the masses locked in this system, it's as if financial assets all by themselves are both necessary and sufficient to secure a prosperous future.

Without understanding the actual nature of where we are in this story, there's no way to meaningfully adjust our course towards a different destination. For now, I will constrain this analysis to the Fed and to the economy, and show that their efforts have not borne the fruit they hoped for and that it's well past time to admit that the grand money-printing experiment has not worked out as planned.

If we simply pump the economy back up at any and all costs, we will win that battle. But we'll lose the larger war. What we should be doing instead is using this as an opportunity to address some of the hard questions about where we are, where we are headed, and what kind of world we wish to enter into (and leave behind for our progeny).

In 1999, when Bernanke was essentially campaigning for the position of chairman of the Fed, he wrote a paper that lambasted Japanese monetary officials for not doing enough to prevent a sustained period of low inflation, sluggish economic growth, and torpid credit market growth:

Before becoming Fed chairman, Mr. Bernanke led a band of U.S. academics who argued that Japanese officials weren't doing enough to jolt their economy out of its torpor. In a 1999 paper, Mr. Bernanke lashed out at Japanese officials, saying their country's woes were the result of their own "self-induced" paralysis. Japan's responses to deflation, he charged in atypically blunt terms, were confused, inconsistent and too cautious.

(Source)

The basic ideas he set forth were simply that the proper course of action for Japan (said easily enough from his armchair academic position at Princeton) was to simply do more, promise more, and not pull back from stimulus until the economy and inflation were behaving properly.

If they had, he argued, then they could have avoided a prolonged period of low growth, high unemployment, and declining inflation.

More from that same article:

At a conference at sponsored by the Boston Fed in Woodstock, Vt., that October [1999], Kazuo Ueda, then a BOJ policy member, issued a warning to the largely American audience: "Do not put yourself into the position of zero rates," he said. "I tell you it will be a lot more painful than you can possibly imagine."

Mr. Bernanke shot back that Japanese policy makers might be making the same "extreme policy mistakes" Americans made in the 1930s—being too timid about reversing deflation. A few weeks later, in a blistering research paper, he said even though conventional tools were expended, there was plenty the Japanese could do to boost consumer demand, business spending and prices.

Among his suggestions: Cheapen the yen by selling it in the currency markets; or buy long-term debt from the Ministry of Finance to finance tax cuts, something he said was akin to just dropping money from a helicopter.

One objection at the time was that Japan's economic problems weren't the result of too little stimulus by the central bank but of structural problems in Japan's banking system and in protected industries.

Mr. Bernanke said structural problems didn't negate the need to find ways to push up consumer demand and business spending.

"Japanese monetary policy seems paralyzed, with a paralysis that is largely self-induced," he concluded. "Most striking is the apparent unwillingness of the monetary authorities to experiment, to try anything that isn't absolutely guaranteed to work."

Well, here we are: six years into Bernanke's own Japanese experiment, and the U.S. is mired in low growth, high unemployment, and declining inflation. To be blunt, none of his ideas are working out as easily in practice as they did on paper.

The hubris, the easily rankled ego of an academic, were on high display in Bernanke's comments to the Japanese. And that brings us to the nub of the issue today: the Fed's utter failure to back up and admit that its grand strategy is simply not working as planned here.

The evidence that the Fed's own efforts to shock the economy back to life have failed is quite clear. Anecdotally, pretty much everyone knows exactly what would happen to the equity and bond markets if the Fed stopped injecting $85 billion into the financial system each month: they would crater. So even there, we'd have to give the Fed a poor grade, if not a failing one, for creating markets now over-dependent on easy money.

Let's start with employment – or rather, its inverse, unemployment – because that's the main thing to which the Fed has tied its quantitative easing (QE) program.

At first glance, it looks like the Fed is winning the day, because even though unemployment is quite elevated by historical standards at 7.4%, it's at least moving in the right direction:

Like all U.S. government statistics, the headline number is about as fuzzy as they come, and it deserves just a little bit of inspection before we place much confidence in it.

To calculate the unemployment rate requires you to know two things: how many people are out of work, and how many can work. But the Bureau of Labor Statistics (BLS), the government agency that calculates the employment figures, has spent decades introducing one exclusion after another in order to reduce the accounting total for people who are out of work -- each time with the effect of reducing the headline unemployment rate.

After all, if fewer people are 'out of work', which means they are not counted, then unemployment rate will be lower. A smaller numerator creates a smaller fraction.

Fortunately, the BLS still calculates a more rigorous definition of total unemployment (although it is still not completely accurate) that goes by the name "U-6", which they define as follows:

U-6 – Total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all persons marginally attached to the labor force

This alternative measure of unemployment and underemployment stands at 14.0%, or nearly double the headline rate. It excludes those who have not even looked for a job in the last 12 months, and there's good reason to believe there are a lot of those individuals right now.

Evidence of that comes from the labor force participation rate, which measures all those who have a job (and, yes, having a part-time job counts the same in this calculation as having a full-time job). It has fallen to painful levels:

In the above chart, where everyone who is employed is divided by everyone of employment age, we can see that just under 59% of working-age Americans are employed. We have to go back to the early 1980s to find a similar employment proportion, and here we'll note that it is much harder to get by on one salary today than it was in times past, indicating something of the hardship embedded in this number.

It stands to reason that a lot of people who want to work, but have not looked recently enough to be counted, are contained in the above chart.

One other way we might surmise that some people have not looked for a job in over a year is to look at how long people tend to remain unemployed once they lose their job. Here the data is particularly grim:

Note that this chart is of the mean duration of unemployment, so roughly half of all people are out of work for just over 35 weeks, and half are out of work for longer than that. If we imagine a nice spread to the data, perhaps a reasonable bell curve, then it's not hard to imagine that quite a few people are well over the 52-week mark and that some of them could easily fall through the statistical cracks.

If QE is helping to bring down unemployment as the Fed claims and the media carefully repeats, then it's not clear at all that it's helping to bring down the mean duration of unemployment from levels that are without precedent in the 60-year-old data set.

One other area in which QE has failed to help is in the types of jobs created. Of the meager few jobs created since the start of the financial crisis and recession in 2008 and 2009, respectively, nearly 4 million of them have been part-time jobs, which are counted and reported by the BLS with the exact same weighting as full-time jobs:

Here again we will note that QE is not having its intended effect if the goal is to create high-paying, full-time jobs. Instead, all we are getting are a lot of part-time jobs (i.e., lower pay and without benefits). Through the first 7 months of 2013, 953,000 jobs have been created. A full 731,000 of those, or 77%, have been part-time.

Of course, it's silly to blame QE for this, because QE has nothing to do with initiatives like Obamacare, which is one of many contributing factors towards more part-time work being offered and performed. But then again, that's the point. It's just plain silly to tie QE to employment at all in the first place, but that's what Bernanke did, which is why we're taking such a detailed look at it here.

On the subject of GDP growth, the data is even more dismal. The 'bounce' seen after the recession allegedly ended in 2010 is the worst on record, and GDP growth currently stands at a rate not seen outside of the context of a recession at any point over the prior 60 years:

For all of the talk of recovery and improvement and corporate earnings and such, and even with all of the statistical wizardry of the Bureau of Economic Analysis (BEA) at work, the GDP numbers here are indistinguishable from those of Japan after its bubble burst and the Bank of Japan began fighting its deflationary monster.

The other similarities to Japan are that the U.S. Fed is now stuck with a zero interest rate policy and finds itself in the business of monetizing enormous quantities of U.S. federal debt.

Like Japan, the U.S. finds its sovereign debt loads not just growing, but exploding at the fastest pace on record for six years now:

The summary here is that Bernanke, after dissing the Japanese efforts, has little more to show for his efforts than they do. The economy remains weak, inflation is low, he's trapped in a 0% interest rate policy, unemployment remains stubbornly high, and federal debt is exploding.

In fact, he does have results. It's just that they are indistinguishable from those of the Japanese.

In Part II: The Real Story To Focus On, we clarify the real issues we need to be dealing with if we want our entry into the future to be anything longer-lived than a kamikaze mission.

The Fed is doing an excellent job of demonstrating how fighting the wrong battles leads to losing the war.

If we want different results (and I do) then we need different behaviors. To get those, you either change willing through insight or else stone-hearted reality will force you to on its terms.

If we don't chose the former, the latter is a guarantee.

Click here to access Part II of this report (free executive summary; enrollment required for full access).

|

Last fall, voters in Los Angeles County passed Measure B, the “Safer Sex In the Adult Film Industry Act.” This measure requires the use of condoms in adult films during sexual intercourse. Vivid Entertainment, Califa Productions and porn star Kayden Kross sued. Among other things, they argued that the requirement infringed upon their constitutional right of free expression under the First Amendment.

On Friday, a federal district court judge denied the plaintiffs motion for a preliminary injunction. Although the judge agreed that the production of pornographic films is protected by the First Amendment, he found it likely that the law would satisfy intermediate scrutiny as a content-neutral regulation of expressive conduct. The judge did not reject all of the film companies’ claims, however, finding that some of the law’s administrative and enforcement provisions were too intrusive or prone to abuse.

Here’s early coverage from the L.A. Daily News and Business Insider. The opinion is here.

University of San Diego law professor Donald A. Dripps has an important new article in the Journal of Criminal Law and Criminology: “Dearest Property”: Digital Evidence and the History of Private “Papers” as Special Objects of Search and Seizure (103 J. Crim. L. & Criminology 49 (2013)). (H/T Mike Ramsey at The Originalism Blog). In it, he presents a powerful case that the seizure of private papers by government authorities for later perusal was considered a distinct and equal injustice as that of issuing general (nonparticularized) warrants. As such, one’s papers merited much greater protections from seizures that one’s “effects” or personal property. Indeed the “seizure” of one’s papers for later perusal to find incriminating information therein had the hallmarks of the evils of general warrants. He then connects this historical analysis with contemporary debates over the seizure of digital information. Here is a bit from the Introduction:

This Article argues that the history of seizing “papers” explains why the Amendment uses the term and offers the opportunity to ground special Fourth Amendment rules for digital evidence....

The Fourth Amendment refers to “papers” because the Founders understood the seizure of papers to be an outrageous abuse distinct from general warrants. The English courts and resolutions of the House of Commons condemned both abuses distinctly. The controversy was closely followed in America, where colonial Whigs sympathized with, and even idolized, John Wilkes, who successfully sued for damages for the seizure of his papers. America inherited the common law ban on searches for papers, adopted constitutional provisions that mentioned papers distinctly, and refused to modify the common law ban by statute until the Civil War. The one Founding-era attempt to authorize seizing papers by statute was condemned as contrary to common law and natural right and never passed into law. Although Congress authorized seizing papers to enforce the revenue laws during the Civil War, it took until the 1880s for a challenge to reach the Supreme Court. That challenge was Boyd, which remained the law for another ninety years. Boyd rightly held that “papers” deserve more constitutional protection than “effects.” Special protection does not, however, ineluctably mean absolute immunity. The seizures that aroused outrage in the 1760s were indiscriminate, expropriating, unregulated, and inquisitorial. A regulated, discriminate, and nonrivalrous process for inspecting documents is different. Indeed, the prohibition on seizing papers was never absolute. Stolen and contraband papers could be seized under warrant, and perhaps papers of only evidentiary value could be seized incident to arrest. Moreover, if the Fourth Amendment, as Story said, is “little more than the affirmance of a great constitutional doctrine of the common law,” the Amendment incorporates by reference “a great constitutional doctrine” that was dynamic on its own terms, subject to judicial evolution and statutory modification. The supposed choice between no special protection for private papers and complete immunity for private papers is a false dilemma.

This is from the middle:

Current doctrine seems premised on a supposed dilemma. If private documents do not enjoy heightened constitutional status, and the government can show probable cause to believe that one document among thousands is either contraband or evidence, the police may scan the entire lot. In some cases their suspicions will prove baseless and they will have searched thousands of innocent but private entries for no good purpose. If, on the other hand, documents do deserve heightened constitutional protection, the government has no right to pick through the haystack in search of the needle, and documentary evidence of serious crimes would, as a practical matter, become off-limits to law enforcement.... The pooling problem is not about either the lawfulness of the object of search or the particularity of a warrant. In the 1760s, libels could at least theoretically be seized; the problem was the need to look through reams of innocent private papers to find the contraband ones.

And this from the conclusion:

There are difficult questions about both the substance of structural safeguards on digital searches, and about the institutions best equipped to formulate those safeguards. All I have suggested here is that safeguards that greatly reduce the special evils that attended the seizures of papers in the 1760s might make digital-age Fourth Amendment law simultaneously more legitimate and more functional. If that turns out to be true, the time may come when structuring digital searches is not just best practice, but also the only practice that is not “unreasonable.”

The history is fascinating, and obviously germane to current cases and controversies. Beyond its claims about the Fourth Amendment, I had a number of reactions.

Professor Dripps’s paper is both fascinating and timely. I highly recommend it.

UPDATE: I neglected to mention that Professor Dripps cites with approval co-blogger Orin Kerr’s article, Digital Evidence and the New Criminal Procedure, 105 COLUM. L. REV. 279 (2005).

Following an uneventful flight from Lyons the crew prepared for a descent and approach to Strasbourg. At first the crew asked for an ILS approach to runway 26 followed by a visual circuit to land on runway 05. This was not possible because of departing traffic from runway 26. The Strasbourg controllers then gave flight 148 radar guidance to ANDLO at 11DME from the Strasbourg VORTAC. Altitude over ANDLO was 5000 feet. After ANDLO the VOR/DME approach profile calls for a 5.5% slope (3.3deg angle of descent) to the Strasbourg VORTAC. While trying to program the angle of descent, "-3.3", into the Flight Control Unit (FCU) the crew did not notice that it was in HDG/V/S (heading/vertical speed) mode. In vertical speed mode "-3.3" means a descent rate of 3300 feet/min. In TRK/FPA (track/flight path angle) mode this would have meant a (correct) -3.3deg descent angle. A -3.3deg descent angle corresponds with an 800 feet/min rate of descent. The Vosges mountains near Strasbourg were in clouds above 2000 feet, with tops of the layer reaching about 6400 feet when flight 148 started descending from ANDLO. At about 3nm from ANDLO the aircraft struck trees and impacted a 2710 feet high ridge at the 2620 feet level near Mt. Saint-Odile. Because the aircraft was not GPWS-equipped, the crew were not warned.Why this is interesting is that fuel economy drives the use of many of the modes in the Airbus:

On a jet, the most fuel efficient way to descend is of course to stay in the optimal cruising altitude as long as possible, then cut the thrust and glide with a certain glide speed to the destination deceleratate for the approach, and, ideally you only advance throttles as far as the outermarker to spool up for go-around.While I don't know details, I wouldn't be at all surprised that this was the intersection of a complicated cockpit control design and corporate policies that made pilots think twice before taking corrective action.

Simply put, the speed (i.e. steepness of your glide/dive) calculation is based on economic fuel to flight time ratio (the cost index). So all you have to do is make a good decison about the top of descent point observing all the speed and altitude constraints ahead. Which is, obiously the tricky part.

For this regime the autopilot interface has a mode selector named Level Change (B) or Open Descent (A).

Should you find yourself short of the field, either you slow down (shallow your descent) - not good as you accumulate extra time on the flight, or add thrust - fuel penalty, the lower the worse.

This may have been fine when the Amendment was first conceived, but considering the changing context of culture and its artifacts, might it be time to amend it? When it was adopted in 1751, the defensive-power afforded to the citizenry by owning guns was roughly on par with the defensive-power available to government. In 1751 the most popular weapon was the musket, which was limited to 4 shots per minute, and had to be re-loaded manually. The state-of-the-art for “arms” in 1791 was roughly equal for both citizenry and military. This was before automatic weapons – never mind tanks, GPS, unmanned drones, and the like. In 1791, the only thing that distinguished the defensive or offensive capability of military from citizenry was quantity. Now it’s quality.

This is a pretty common argument. I’ll grant him, for the sake of argument, that the Second Amendment is primary founded on resistance to tyranny, even though our Courts seem to be more focused on the self-defense aspects of the right.

The chief mistake people make in this line of thought is to assume war is killing. That is not really the case. War is the use of force in an attempt to impose your political will onto others. Killing is just a means to accomplish that. If it were just about killing, the wars in Iraq and Afghanistan could have been settled in about thirty seconds, but they weren’t. Our goals in both cases was to impose a less outwardly militant democratic system of government on a population that had no tradition of it. When it comes to defeating an opposing army, all the things that make governments so remarkably powerful matter quite a lot. When it comes time to actually impose your political will, those things matter a lot less. A man in a tank can’t impose his will on me, he can only kill me. To impose his will he has to get out of the tank, plane, or ship, and essentially go from being a soldier to being a policeman, and at that point, we become a lot more equal. If our government ever wants to kill us, lots of us, we’re screwed. We have a much better chance resisting the imposition of someone else’s political will. It can be argued that firearms aren’t as important in that equation as other things, and I might agree with that, but such resistance is not beyond the reach of motivated individuals. The philosophies and attitudes that the right to keep and bear arms engenders in a population is likely just as important, if not more important, as the instruments of exercising that right.

On Friday, the Obama Administration released a “white paper” articulating its case for the legality of the NSA call records program under Section 215 of the Patriot Act and under the Fourth Amendment. I found the “white paper” a somewhat frustrating read, as it is essentially a brief for the government’s side with no brief coming to oppose it. Although the white paper raises some interesting points, it also fails to confront counterarguments and address contrary caselaw.

Consider the critical issue of whether a massive database of billions of records can be deemed “relevant” because some records inside the database are relevant. Here’s the key discussion of that issue from the white paper:

[C]ourts have held that the relevance standard permits requests for the production of entire repositories of records, even when any particular record is unlikely to directly bear on the matter being investigated, because searching the entire repository is the only feasible means to locate the critical documents.[FN7] More generally, courts have concluded that the relevance standard permits discovery of large volumes of information in circumstances where the requester seeks to identify much smaller amounts of information within the data that directly bears on the matter. Federal agencies exercise broad subpoena powers or other authorities to collect and analyze large data sets in order to identify information that directly pertains to the particular subject of an investigation. Finally, in the analogous field of search warrants for data stored on computers, courts permit Government agents to copy entire computer hard drives and then later review the entire drive for the specific evidence described in the warrant.

[FN7]See, e.g., Carrillo Huettel, LLP v. SEC, 2011 WL 601369, at *2 (S.D. Cal. Feb. 11, 2011) (holding that there is reason to believe that law firm’s trust account information for all of its clients is relevant to SEC investigation, where the Government asserted the trust account information “may reveal concealed connections between unidentified entities and persons and those identified in the investigation thus far . . . [and] the transfer of funds cannot effectively be traced without access to all the records.”); Goshawk Dedicated Ltd. v. Am. Viatical Servs., LLC, 2007 WL 3492762 at *1 (N.D. Ga. Nov. 5, 2007) (compelling production of business’s entire underwriting database, despite business’s assertion that it contained a significant amount of irrelevant data); see also Chen-Oster v. Goldman, Sachs & Co., 285 F.R.D. 294, 305 (S.D.N.Y. 2012) (noting that production of multiple databases could be ordered as a “data dump” if necessary for plaintiffs’ statistical analysis of business’s employment practices).

. . .

While these cases do not demonstrate that bulk collection of the type at issue here would routinely be permitted in civil discovery or a criminal or administrative investigation, they do show that the “relevance” standard affords considerable latitude, where necessary, and depending on the context, to collect a large volume of data in order to find the key bits of information contained within.

If you’re reading quickly, you might skip over the caveat “where necessary, and depending on the context” in that last paragraph. But it’s actually a significant caveat, and the white paper doesn’t discuss the precedent on the other side that complicates the Administration’s position.

A case that comes to mind is In re Grand Jury Subpoena Duces Tecum Dated Nov. 15, 1993, 846 F.Supp. 11 (S.D.N.Y. 1994) (Mukasey, J.). In that case, then-Judge (later Attorney General) Michael Mukasey quashed a grand jury subpoena that sought all computers and all electronic storage devices possessed by the target corporation. The subpoena failed Rule 17′s “relevance” standard because the computers contained so much irrelevant material intermingled with the data that was relevant to the investigation:

Government counsel have conceded on behalf of the grand jury that the subpoena demands irrelevant documents. Moreover, the government has acknowledged that a “key word” search of the information stored on the devices would reveal “which of the documents are likely to be relevant to the grand jury’s investigation.” Id. at 3. It follows that a subpoena demanding documents containing specified key words would identify relevant documents without requiring the production of irrelevant documents. To the extent the grand jury has reason to suspect that subpoenaed documents are being withheld, a court-appointed expert could search the hard drives and floppy disks.

“[B]ecause the subpoena at issue unnecessarily demands documents that are irrelevant to the grand jury inquiry,” Mukasey concluded, “it is unreasonably broad under Federal Rule of Criminal Procedure 17(c).”

Mukasey’s decision seems to cut against the Administration’s position. It blocks a subpoena for all the electronically-stored information because lots of the information to be obtained is not relevant even thought some of it is. Plus, the opinion is written by a recent Attorney General of the United States, which should give it extra prominence. And it’s a lot more significant a precedent than are Fourth Amendment cases involving warrants to search computers: Warrants do not apply the relevance doctrine while subpoenas do, so it seems odd to discuss the cases about computer warrants but not the cases on computer subpoenas. But the “white paper” doesn’t mention this case, so we don’t know if the Administration has a response to it– or if the FISC was ever alerted to it.

Granted, it’s possible to try distinguishing Mukasey’s decision. Mukasey seemed to think that a key word search would be responsive to the subpoena, so getting all the data was not necessary. There was an alternative way to proceed, namely by doing key word searches. The Administration presumably would argue that the Section 215 program is different because getting the whole database is in fact necessary: If the government doesn’t have the whole database, many of the records will be destroyed before the government can find the links it is looking for.

Perhaps that’s right, but that argument would open up a difficult question of what the frame of reference is for assessing necessity. Does the risk that customer metadata would be deleted in the ordinary course of business create a “necessity” to overcollect? Do you assume that the government has a right to get access to all metadata of every telephone user in the United States, and that overcollection is “necessary” to effectuate that? Or do you assume that the government only has a right to get access to relevant metadata that exists at the time the government identifies the relevance of that specific metadata? I’m not sure there is a doctrinal answer to that issue, but the white paper doesn’t appear to acknowledge and confront the question.

In addition to not citing contrary precedent, the white paper also cites cases that strike me as relatively weak authority for its position. Consider the three cases cited in Footnote 7 above. In the first case, Carrillo Huettel, LLP v. SEC, 2011 WL 601369, at *2 (S.D. Cal. Feb. 11, 2011), the SEC issued a subpoena to the Bank of America for all the trust account records of an 8-lawyer firm (Carillo) suspected in misconduct involving at least 42 clients. The firm objected that getting all the account records would reveal what it was doing with the funds of 100+ clients beyond the 42 already tagged as involving misconduct. The government argued that it needed all the client records to really understand what was happening to the funds, and the Court agreed: “On balance, the Court finds the SEC has demonstrated that there is reason to believe that the Carrillo trust account information sought by the subpoena is relevant to a legitimate law enforcement inquiry. Although not every responsive document produced by BofA may be relevant, there is reason to believe that the records overall contain information relevant to the investigation.”

This Carrillo case provides at least some authority for the government’s position, but it seems like relatively weak authority. In that case, the government was investigating the records of a single smallish law firm, and it already knew that about 30% of the records to be collected involving firm clients were involved in financial wrongdoing. In that instance, it seemed plausible that most or all of the records were involved in the scheme, even if the government didn’t know it yet. And it would make sense to look through all the records to see which ones were tainted by the firm’s practices. That’s far different from government access to the records of hundreds of millions of customers to find a mere handful of bad actors.

The other two cases cited by the government seem much weaker. Both involve requests for records in civil discovery disputes. In Goshawk Dedicated Ltd. v. Am. Viatical Servs., LLC, 2007 WL 3492762 at *1 (N.D. Ga. Nov. 5, 2007), the court allowed the plaintiff suing an insurance company to get a copy of the actuarial database used to set the terms of the plaintiff’s policy. The court allowed the plaintiff access to the database because “its methodologies, policies, and practices of conducting life expectancy evaluations are themselves at the center of this litigation,” and the database was the key way to understand the insurance company’s methodology and practices. In the third case, Chen-Oster v. Goldman, Sachs & Co., 285 F.R.D. 294, 305 (S.D.N.Y. 2012), the court mentions the possibility of a “data dump” as part of the discovery process. But the case also cites Nicholas J. Murlas Living Trust v. Mobil Oil Corp., No. 93 C 6956, 1995 WL 124186, at *5 (N.D.Ill. March 20, 1995), in which the Court rejected turning over an entire database of information during discovery and seemed to agree with the objecting party’s claim that the demand was “outrageous.”

Having read Goshawk and Chen-Oster, it’s not clear to me how they are supposed to support the government’s position except in a very indirect way. The fact that a few courts have not categorically ruled out turning over things called “databases” does not shed a lot of light on whether it is lawful here. To be clear, there’s a lot of interesting and useful analysis in the white paper. But there is also a lot that the white paper leaves out, and some of the cases cited don’t seem to offer significant support the Administration’s position.

In other news, someone brought an baby deer that had been abandoned by its mother to a no-kill animal shelter in Wisconsin.

The no-kill shelter placed a few calls, found a licensed wildlife refuge that would take the baby, and kept the animal in their fenced wooded facility for two weeks until the slot opened up at the refuge.

But, thankfully, this evil criminal conspiracy was stopped in its tracks. Thanks to brave government employees, aerial photos were taken, surveillance was performed, a SWAT team was assembled, and then nine agents of the Department of Natural Resources and four deputies "all armed to the teeth", raided the no-kill animal shelter.

And shot the baby deer and stuffed its corpse into a body bag.

Because, you see, the law forbids private possession of wildlife. And those villains at the no-kill animal shelter weren't going to send the deer to the licensed wild life refuge until tomorrow

Not that I'm criticizing. Oh, gosh, no! I am completely loyal, friend State. I would never question your dictates, second guess your wisdom, disagree with any of the tens of thousands of men and women that you equip with body armor, submachine guns, assault vehicles, drug sniffing dogs, GPS surveillance, drones, court rulings providing exceptions to the fifth amendment, and more.

My loyalty is complete, friend State.

But that baby deer? Yeah, I'm pretty sure he was a mutant. Or at the very least, potentially diseased. Better safe than sorry, friend State.

Good call.

Mutants. Secret Society members. Communists. Baby deer. © 2007-2013 by the authors of Popehat. This feed is for personal, non-commercial use only. Using this feed on any other site is a copyright violation. No scraping.

I am free. I was born that way. Free as the wind blows. Free as the grass grows. You know the song.

I am free. I was born that way. Free as the wind blows. Free as the grass grows. You know the song.

Each day I leave my stall and roam the field. I eat. I watch the trains go by. I swat flies.

The sun makes it bright, and the clouds make it not so bright. The moon makes it night.

I feel safe in the field and safe in my stall. I feel that way since I know the man will take care of me. I am free to need the man, and the man likes me and gives me what I need.

The man was there when I was a calf. He is still there. The man brings feed and pours drink. He takes milk from the cows. He leaves nuts here and there in the field so more grass will grow.

This is a good deal but some cows and bulls must think it is a bad deal. One day some cows and bulls were gone. (One day I saw a cow slip in the mud by the fence near the trees, but that is not the same.)

I did not see them go, but I think they walked off. Why would they do that?

Look! A bird.

I am free. Are you free? © 2007-2013 by the authors of Popehat. This feed is for personal, non-commercial use only. Using this feed on any other site is a copyright violation. No scraping.

This is an excellent introduction to how the messages are sent, what they look like, and how NSA must be doing things. Highly recommended.In other words, a competent programmer can reliably parse out email addresses from the structured header fields with effectively no chance of getting user-entered content by mistake, unless the user was hand-crafting the email. All they have to do is stop reading the message at the first blank line (as I have marked in the example with a dividing line).In order to get occasional cases where the Xkeystore retrieves "metadata" in the form of email addresses that turns out to be user-entered content instead, the NSA must be retrieving and parsing the content of the email. They may have coded their application to only show what they think are email addresses, but they are extracting those email addresses from the content, not from the headers. Which means they must be collecting and analyzing the content, not just the metadata.

It's like a pretty girl who wants to change clothes in your bedroom. Does she trust you not to look or does she find a screen or use a bathroom or closet so that you can't look? Does it matter if you promise not to look?

Clearly, the NSA has the ability to intercept email content, not just metadata; just as clearly, they are actually interceptingthe full email content and collecting it for analysis. They are asking us to trust them not to look at the content, even though they already have it. Maybe they have built their application so that they can't look without getting permission, but according to Snowden, the permission system is a joke and a rubber stamp. We already know that Homeland Security does keyword scanning of content, and I'm betting the NSA is doing the same thing with its application, and if the right keywords are there -- or the right sender or recipient, two or three degrees away from a "suspected" terrorist -- the content is flagged for a closer look. Or the NSA analyst can make up his own justification and get it rubber stamped.

And we can't see how their application works, or have any way of knowing that it does what it says it does. In this analogy, the NSA is the guy wearing a nice Google Glass device, and he tells the pretty girl in his bedroom she can strip down right there in front of him and she will be perfectly safe -- he's written his own privacy app, you see, and when it detects a pretty girl in his field of view it doesn't let him look. He's just watching you to keep you safe, you see. He's not recording the whole thing and uploading it to his friends.

Submitted by Jim Quinn of The Burning Platform blog,

Yes. The national intelligence has fallen that far. The morons in West Philly can't spell 'Cat'. At least 75% wouldn’t know the Vice President of the U.S.. More than 50% can't add 5 + 5. And 80% wouldn't know when and why the Civil War was fought.

|

|

A Bayesian network analysis stamping on a human face forever.

“Hi, NSA? This is DEA. What? You KNEW we’d be in touch? Oh, riiiight. Yeah. So, ah, anyway, let’s do lunch…”

For a long time our government has had the luxury of not even being able to know about an ocean of petty, often victimless crime. Our laws were born into benign neglect. This was not by choice, but by technological necessity. Knowing everything just wasn’t possible: If some citizen grew a few pot plants, hired a couple of illegals, kept a modest cache of unregistered weapons, or paid — in cash — for sex, probably no one would ever be the wiser. As long as you weren’t a total dumbass about it, you wouldn’t face any legal consequence at all.

Like the fish in the water, we lacked a term for our happy state of affairs. We clearly need one now, and so I’ll coin it: For many years, our government’s benign ignorance was a limiting factor in the growth of the carceral state. That may be ending. When it does, our law enforcement will look very different.

Benign ignorance permitted the rise of legislation that no one ever expected to see systematically enforced: It’s illegal to grow vegetables in your front yard in Los Angeles. You often can’t legally photograph or video a cop. There are some very easily violated laws about the mails — images of which, yes, they’re scanning now. Do magic mushrooms grow wild on your land, as sometimes happens in, like, all of North America? Uh-oh. And let’s not even get started about intellectual property rights, which everyone violates absolutely all the time. Under benign ignorance, copyright only catches the really big fish, which is probably just how things should be. But without benign ignorance? Somebody better tell aunt Francine. (“And tell her in person, you dolt! Do not call her on the phone!”)

As we all know now, the NSA has our telephone and Internet metadata. They appear to be able to get our browsing and search history as well as our passwords. They very likely have mobile phone location data. Did you turn your phone off? It doesn’t matter. And we’ve just learned that they can also read encrypted VPNs.

That means the NSA knows. They know about your bitcoins. They know about your porn. They know about your guns. They know about your drug dealer. And they know about Ashley Madison. Or Grindr. Or Bang With Friends. Or whatever it is you depraved sickos get into these days. They also know about the illegal stuff, of which the less said the better.

It’s only natural that other government agencies are going to want what the NSA now has. If they get it, things are going to change in ways that we can’t even imagine. This story of a police raid after searching for “backpack” and “pressure cooker”? Only the beginning.

Now, readers, the linked is a developing story. It’s not yet clear how things will shake out in this particular case. But whether it’s true, or erroneous, or even just a very clever hoax will hardly matter long-term. Whatever it may be, the story has legs because it’s a vision of a terrible future, one that absolutely nobody wants. And it’s coming straight for us.

As far as I can tell, the only thing standing between us and that is the NSA’s tendency to follow rules — that is, the tendency to follow rules possessed by individuals who have shown absolutely no tendency at all to follow rules. At least not when they’re inconvenient.

Benign ignorance is dead. They’re not ignorant anymore. They haven’t been for a long time. Now we know that they know — and they know that we know that they know.

So what comes next?

It could be very, very bad, depending on our political will, or lack thereof. We might get the only thing worse than losing the drug war, which is actually finally winning the drug war — as in, anyone who uses pays the full, on-paper legal price for their crime. I don’t think anyone ever expected this to happen. We can’t count anymore on benign ignorance to keep people like the young Barack Obama, the young George W. Bush, the young Bill Clinton, and the young [everyone else now in overprivileged Washington] out of prison.

Making a new crime as a mere act of political theater has always had some costs, of course, and I’ve usually thought those costs were too high. Seldom is a law entirely without teeth. But as of today, the teeth bite harder.

Which may turn out to be a very good thing, in some ways: Those in power only pay attention when the laws affect them or the others close to them. They may think twice about future bad laws.

But the end of benign ignorance could also turn out to be a very bad thing. We have no particular reason to expect that the surveillance state will be administered impartially. There might be some neighborhoods, some exclusive Internet services, or some procedures that slip the net. With official approval, of course, subject to revocation by some elite. And those gatekeepers, whoever they are, will hold the real power.

#111

They moved the river to build the water wheel,

Then built a wooden race to divert the current.

Sluice opened, stones ground raw grain into meal

For a hundred years, until the old mill was spent.

River turning wheel turning gears turning stone,

A devolution of mechanics all to crush a seed.

The sun burns for years to dry an animal’s bones,

And countless gallons of water won’t break a reed.

I’m reluctant to approach the mill too closely

(Its ancient timbers are desiccated, ghostly),

Hear its stoppage rasped by the river’s relentless

Passage over the shattered race’s detritus.

Away from the wreck, a little waterfall churns

Spray, wrack, and spume, and, like time, it burns.

Note: This is one of more than 125 poems after paintings or images, which can be viewed at the blog, Zealotry of Guerin.

WickemtDC Can't Get Jewish Food Right

There hasn’t been a good Jewish deli in the D.C. area in ... well, forever, as far as I know. Many years ago, someone wrote to Phyllis Richman, food critic for the Washington Post, asking where he could get good Jewish deli in the D.C. area. Richman responded to the effect of, “if you live in the D.C. area and want good deli, take the red line to Union Station ... then take Amtrak to New York.”

Since then, several “New York” “Jewish” delis have come and gone, those those remain typically feature menu items such as Monterey Chicken Paninis, Crabcake Dinners, or even maple ham steak that basically disqualify them from the category they are supposed to be in.

Which brings me to the new Attman’s deli in Potomac, in the Cabin John Mall. Attman’s is a branch of a venerable Baltimore institution, and it opened in the same strip mall as Goldberg’s Bagels a very good (and kosher) bagel place and a Judaica store. It’s storefront is the former Pomegranate Restaurant, a defunct kosher restaurant. [Aside: Kosher restaurants rarely make it in the D.C. market, the Orthodox population is too small and many observers of kashrut go to Baltimore for shopping and eating-- Baltimore being the home of the amazing Seven Mile Market kosher supermarket, billed as the largest kosher supermarket in the U.S., whereas the two kosher markets in the D.C. suburbs are small, expensive, and lame.]

Anyway, Attman’s isn’t kosher, and it isn’t even quite kosher-style, as it mixes meat and cheese on the same sandwich. But it does make a big deal of its “Jewishness,” advertising “Jewish corn beef” (from a circumcised bull?) and so on. I didn’t see any bacon, ham, or other pork products on the menu, nor any trendy sandwiches, so it seemed a bit more like a traditional “Jewish” deli than other imitators.

But, and here’s the key, how was the food? Not so great.

Attman’s is apparently famous in Baltimore for its corned beef, but my wife and I both thought our corned beef was somewhat dry. (But if you like lean corned beef, it was that, so don’t bother paying extra for lean). Not bad otherwise. Overall a 6.

Pickles were a big disappointment. Unlike a traditional NY Jewish deli, no pickles were served gratis as appetizers, nor was cole slaw. I ordered some pickles anyway. Instead of sour and half-sour, the menu called them “green” and “well-done.” After confirming that well-done was the equivalent of “sour,” I ordered a mix. The “green” were pretty good, but the well-done were pretty bad, tasting more like a Vlasic pickle than a traditional sour garlicky “Jewish” pickle. Overall a 4. If you want a good sour pickle, go to Seven Mile Market instead and buy a jar from one of Baltimore or Brooklyn’s pickle purveyors.

We also ordered a potato knish, outrageously priced at $5.00 for a small knish. That nevertheless would have been a small price to pay for true knishy goodness. But this knish was mediocre and seemed (heresy!) like it might have been microwaved. My standard for a restaurant knish is that it has to at least be better than Gabila’s frozen that you can get at the supermarket and heat in your oven. This definitely wasn’t. Another 4.

At least the rye bread was very good, the mustard was good enough, and there wasn’t any mayo to be found. Overall a 5, a 6 if you can’t get to New York regularly and have real Jewish deli. But if you’re in the Potomac area and want some good Jewish food, Goldberg’s is just a few yards away.

Does a fish know that its nose is wet? Probably not. It swims in water, and assumes that is the only way any animal lives.

We live in an economic world. Economic models that were developed years ago were created based on observations of how the economy seemed to work at the time. As time goes on, it is becoming clear that early economists missed important connections. The most important of these is the role of energy and its connection to the economy. It takes energy to make anything, from a piece of steel to a loaf of bread. It takes energy to transport anything. Humans need energy in the form of food to continue to live. Clearly, energy should have a place in economic models.

In this post, I explain some of the basic principles as I see them:

1. Humans have evolved to be dependent on external energy.

2. Humans now supplement their own limited energy supply with external energy of various types. In general, the more external energy used, the more humans are able to control their environment.

3. Over the 1 million+ years during which humans have been able to control fire, humans have generally been in situations with favorable feedback loops, due to increasing efficiency in producing goods and services required to meet basic needs. Such loops allowed continued population growth and economic growth.

4. We are now reaching limits on these feedback loops. The result is feedback loops that are changing from favorable feedbacks to contraction.

5. Part of the change in feedback loops relates to the cost of energy sources, such as oil. A rise in the price of oil tends to reduce salaries of workers (because of layoffs) as well as reduce discretionary income (because of higher price of food and commuting), contributing to the trend toward contraction.

All of this is very concerning, because in the past, adverse feedback loops of this type seem to have led to collapse.

The Many Types of Energy

The most basic type of energy, at least from a human perspective, is human energy. This is the energy we as humans have that allows us to move our own bodies and allows us to think. Each of us is given approximately the same amount of energy, with males having somewhat more energy for lifting and pushing objects, and females having the special ability to give birth to new humans.

In order to use human energy, humans need to eat food of appropriate kinds. Most of this food is from plants and animals that we process in some way for this purpose. (This processing normally requires some type of energy.) The only food that is not from plants and animals is mother’s milk. Women need to increase their own intake of food from plant and animals, in order to produce enough milk for their babies.

Humans are able to leverage their own energy with many types of external energy. One very old source of external energy is burning wood and other plant matter. Such energy is used in keeping warm, cooking food, making sharper tools, and warding off predators. Another very old source of external energy is energy from dogs, trained to help with hunting, and from draft animals, trained to help with plowing and grinding tasks.

Humans have learned to harness various other forms of other energy, such as wind, water, and geothermal energy. In the last 200 years, the use of fossil fuels (coal, natural gas, and oil) has greatly expanded the amount of external energy available to humans.

Fossil fuels are important, not just because they can be burned directly, but because they enable the use of electricity from a wide range of sources—including hydroelectric, nuclear, and solar photovoltaic. While we think of these latter sources as non-carbon fuel sources, they are today available only within a system powered by fossil fuels. It takes fossil fuels to create metals in the quantity needed for electrical transmission; it takes fossil fuels to make and transport the type of concrete used in hydroelectric dams and wind turbines; it takes fossil fuels to purify silicon and other materials used in making solar PV.

While people talk about a system that does not require fossil fuels, no one has mapped out how the world could in fact transition from a system that uses fossil fuels to capture these types of energy to a system that would work without fossil fuels. The best we can hope for within the next 100 years is to use fossil fuels more sparingly.

One specialized form of energy is embedded energy that has been stored up in goods for the long term. Examples of early embedded energy includes heat-sharpened stone ax blades, used by hunter gatherers, and clothing, whether made by hand or machine. Today, there is much embedded energy in roads, pipelines, and electrical transmission systems. The vast majority of today’s embedded energy is derived from fossil fuels.

External Energy as a Human Need

Most animals seem to get along fine without external energy, other than the sun’s rays. They live in the parts of the world where they are adapted. They more or less live in balance with their predators. The number of a given species may rise for a while, but if the number grows too much, the species will exhaust its food supply, leading to population decline.

Humans have moved to a different model. The change came when humans (or predecessors to humans) first learned to control fire, over 1,000,000 years ago. Being able to control fire gave humans many advantages over other animals. Humans were able to cook part of their food. This had many advantages: It greatly reduced chewing time, allowing time for other activities, such as making tools and clothing. It improved nutrition, by making food more digestible. It allowed the human body to evolve in ways that used more energy for brain development, and less for chewing and digestion. [i]

The way the natural order works is that each species gives birth to far more offspring than is needed to survive to adulthood. “Natural selection” determines which of these offspring will survive. If humans had been like apes, chimpanzees, or gorillas, total population might have reached a plateau of perhaps 3,000,000, (based on historical animal populations). This limit would be reached because of competition with other species, and because climate is less hospitable outside of a narrow range.

With the help of external energy, such as the controlled use of fire and the use of dogs for hunting, humans were able to gain an advantage over other species and spread to all areas of the globe. This is what allowed population to grow, and continues to help it grow.

The natural order assures that far more human offspring are born than are needed to survive to adulthood. If humans are intelligent, they desire to extend their own lives and the lives of their offspring. The result of this dynamic is that there tends to be continual upward pressure on population.

There is a second dynamic as well. Because of humans’ intelligence, humans have the ability to over-consume at least some of the wildlife in the areas. For example, we learned on our recent visit to Iceland that when Vikings first discovered the island, there were both walruses and the flightless bird, the auk, on the island, but both disappeared soon after humans moved to the island.

Because of these dynamics, there has been tendency to need more food, and more energy supplies of other types, over time. To meet the need for greater food supply, humans began using agriculture about 10,000 years ago. With the advent of agriculture, the amount of human food available per acre was greatly increased.

The availability of agriculture added to the two dynamics noted previously for hunter-gatherers. As before, (1) population tended to increase, because the natural order provides for far more births than are needed for replacement, and because humans, with their intelligence, now had a way to provide more food per acre. Also, (2) there was a tendency of the amount of food available from a given acre of land to degrade over time, because the methods used for agriculture were less than perfect. Erosion was a problem, especially when planting was done on slopes. If irrigation was used, salt deposits often became a problem. Rising population combined with degrading resources led to a need recurring need for additional energy, since supplemental energy could indirectly add to food supply. In situations when additional energy was not found, populations had a tendency to collapse after many years of growth.

Besides the two basic dynamics of rising population and degrading resources leading to a need for additional resources, there were other forces that tended to add to the need for increasing amounts of energy:

a. Cheapest resources used first. Soon after agriculture began, humans began to use resources of other types, such as wood from forests and metals such as iron and bronze. With any of these resources, there is a tendency to use the “cheapest” (easiest to extract, closest at hand, highest ore concentration) first. If extraction is to continue, increasing amounts of energy per unit extracted are likely to be required for later extraction.

b. Increased disease transmission when population is packed more closely together. This issue can be overcome with techniques that kill germs and that keep humans separated from waste products of other humans. The need for these techniques adds to the need for external energy.

c. Deforestation. Without fossil fuels, there was a severe tendency to overuse forests. Deforestation occurred as early as 4000 B. C. E., according to Sing Chew. Historian Norman Cantor writes, “By 1500 Europe was on the edge of a fuel and nutritional disaster [from] which it was saved in the sixteenth century only by the burning of soft coal and the cultivation of potatoes and maize.” The use of coal allowed more energy per person, and took pressure off of limited forest resources.

d. Pull of Technology. The availability of fossil fuels, starting around 1800, has allowed much of what we now call “technology.” Without fossil fuels, our ability to make materials such as metals and glass is severely restricted. Without fossil fuels, we are also lacking for the basic building blocks for plastics, synthetic fabrics, and even modern medicines. Technology provided ways to use fossil fuel resources in ways that helped overcome many human limits. The desire to use more technology led to increasing use of fossil fuels in the 19th and 20th centuries.

Hunter-Gatherer Economies

There were no doubt many different types of economies in the over one million years when humans and pre-humans were hunter-gatherers. One documented approach is the gift-economy. With this approach, those who killed animals shared what they obtained with others in their group. Status was gained based on how much an individual was able to provide to others in the group. Members of the group played different roles—some were involved with caring for children, or too old to work, but what was available was shared with the group as a whole.

In the days of hunter-gatherers, the function of the economy was not too complicated. There was little need to “save for tomorrow,” because it was difficult to carry anything during travels. The amount of food an individual could eat was pretty much limited by appetite, so having “more food” for one individual wasn’t particularly helpful. If one person was the leader, he (or she) might have special adornment.

If population rose too high, relative to resources, this may not have been apparent in “normal” times—when weather was good, and when a particular hunter-gatherer group had an area to itself. But if there was a major weather problem or an encounter with another group needing space as well, population pressure could lead to a crisis. It seems likely that die-offs occurred from time to time, especially during natural “bottle-necks.”

A Simple Agricultural Economy

Thinking about a simple agricultural society gives us some insight as to how early economies must have operated.

Consider a simple economy in which some members produce barley; others produce fish. The fish can be salted and dried, so both the fish and the barley can be stored, if desired. The big issue in such a system is how efficient the barley and fish operation is. If in order to feed the group, half of the group must work full time growing barley, and half of the group must work full time catching, salting, and drying fish, then no matter what kind of economic system is in place, the result will simply be trading fish for barley. Everyone will continue to have to work at either producing fish or barley. The economic system will simply move some of the fish to the barley producers, and some of the barley to the fish producers.

Let’s suppose instead that the barley and fish producers are much more efficient. Suppose that with 10% of the population working at barley production and 10% of the population working at fish production, the population can provide enough food for the full population, leaving 80% of the population (100% – 10% barley producers – 10% fish producers) to pursue other activities. How the remaining 80% of the population will spend its time will depend on resources available and the desires of the citizens. Perhaps 30% of the citizens would make goods of various types (build homes, make clothing, and make furniture) and 20% of the citizens would provide services of various types (education, health, artwork, and hair cutting). This would leave 30% for government and finance. The government portion would include pay for government officials and police and transfer payments to the elderly and disabled.

The total wealth of the community is then the sum of all of the goods and services in this community. The financial system will redistribute the goods and services produced among the members of the community, perhaps allowing some “savings” for future consumption. Those producing goods and services will expect to be included in the redistribution, but so will others, if this has been the tradition in the community.

If the economy operates without fossil fuels, the quantity produced is limited by the speed with which biomass regrows. Thus, unless the community is willing to live with deforestation, it can’t use much wood each year. This puts a severe limit on the amount of goods produced. Printing more money does not change this dynamic.

In the example above, I suggested an efficient economy might need only 20% of its population for food production. In fact, the percentage of the population involved in food production varies greatly across economies. Before fossil fuels use, typically 80% of the population of a country was involved in agriculture. With so many involved in agriculture, the number who were involved in manufacturing and services of all types (including government services) was necessarily very limited, because they needed to be “squeezed into” the remaining 20% of the economy.

Figure 1. Percent of Workforce in Agriculture based on CIA World Factbook Data, compared to Energy Consumption Per Capita based on 2012 EIA Data.

If, in our hypothetical community, population rises because more children live to maturity, this adds a new dynamic. There is a need for more food, clothing, and housing for the growing population. Unless land area keeps increasing, there becomes a need to grow more barley per acre. In a world without fossil fuels, increasing grain yields becomes difficult. More farmers can be added to a given plot, but the additional yield for additional manual effort (perhaps picking off insects that might eat the crop) is not very high. This dynamic tends to lead to what we think of as falling wages of the common worker, when population becomes high relative to resources available. As I have mentioned in previous posts, based on the book Secular Cycles by Turchin and Nefedof, collapse often occurs in such situations. Governments have promised significant services, but it becomes difficult to collect enough taxes to pay for these services, with falling wages of the common worker.

The dynamic is similar if energy supplies of types other than food (such as oil and coal) does not rise as fast as population. The amount of goods produced using these energy supplies will tend to fall, unless technology advances are able to offset the decline in energy consumption per capita. Such technology is normally fossil fuel dependent. If goods per capita falls, this will be reflected in what we think of as falling inflation-adjusted wages, since it is not possible for workers to have more than what is produced.

Adding Fossil Fuels

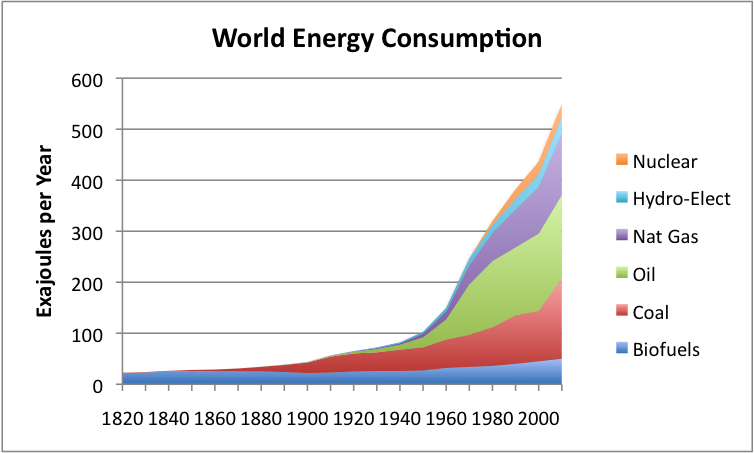

Figure 2. World Energy Consumption by Source, Based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects and together with BP Statistical Data on 1965 and subsequent

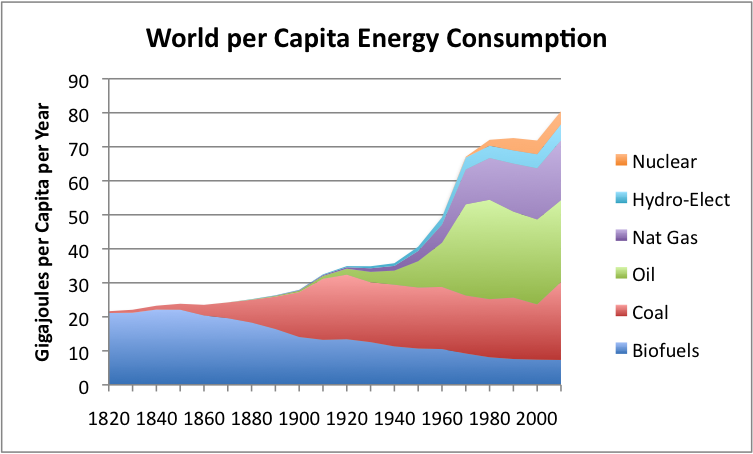

Figure 3. Per capita world energy consumption, calculated by dividing world energy consumption (based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects together with BP Statistical Data for 1965 and subsequent) by population estimates, based on Angus Maddison data.

If metal tools can be used—say metal plows—these metal tools can greatly ramp up efficiency of farming, allowing fewer people to work in the agricultural sector. If we think about the result in the last section, this situation allows a greater proportion of the population to be employed in producing discretionary services, and thus more wealth for the community as a whole.

The problem with making metals such as iron using renewable resources is that huge amounts of charcoal are needed to make even small amounts of iron. If one wants reasonable quantities of metal, or modern alloys such as steel used in plows and trucks, a person needs fossil fuels.

If a person wants to add fossil fuels and the things that fossil fuels can make to a community that does not have fossil fuels, the question becomes how to pay for the new goods using fossil fuels. As an extreme example, if farmers have always planted barley with a stick, the amount of barley each farmer produces is tiny, and the population is likely mostly farmers. If a farmer can use a new tractor, with the latest equipment, a single farmer can perhaps feed the whole community. The tractor will provide the improved efficiency needed to free up a whole community of workers for other purposes.

The secret to adding fossil fuels (or any kind of energy source that can improve efficiency, and allow fewer people to produce essential goods and services) is debt. While the farmer cannot pay for the new tractor with his earnings from growing barley using a stick, the farmer can indeed pay for the tractor with all of the goods and services that the whole community can produce, as the result of the tractor handling work that now takes many workers to do. By growing much more grain, and selling that grain to all of the workers who are now freed up to provide discretionary services, the farmer will have enough funds in the future to repay the loan for the equipment which will allow much greater efficiency. (The problem is that the tractor requires a huge amount of embedded energy from fossil fuels. Workers who have been working without fossil fuels will not be able to earn enough to pay for this embedded energy without debt.)

Salaries of Workers

In my imaginary simplified economy, there is only one country. In such a country, the amount of salaries that workers receive then is closely related to the amount of goods and services that the economy produces. There will be part of the production that goes to the owners of factories, farms, and other sources of production, but they cannot eat any more than anyone else, or sleep in more than one place at a time. If they get paid much more than others, some of it must be in the form of “paper income” that they can theoretically use at some time in the future, but does not involve current consumption.

In general, the more goods and services produced relative to the population, the more workers will receive in inflation-adjusted salary. If the economy is so distorted that most of the goods are made with machines, the government must play a much bigger role, providing transfer payments to those who cannot find employment (unless the government is prepared to handle uprisings by citizens). If workers are not receiving adequate wages to pay the taxes, taxes will need to come from some other source–possibly from the owners of the sources of production.

To see how a rise in oil prices will affect the economy, lets consider what can be expected to happen to a manufacturing company. Suppose that for a particular manufacturer, costs are distributed as follows (the actual percentages aren’t important–just the point that wages tend to be a big piece of the total):

If the cost of oil doubles and the manufacturer is not able to raise prices, the higher cost will wipe out profits. In fact, the cost of other raw materials is likely to rise as well, because oil is used in extracting and transporting raw materials. This will make the impact on profit even worse than the oil-only comparison would suggest.

To “fix” the problem, the manufacturer has to make some sort of adjustment, and the adjustment will almost certainly lead to less dollars being paid for wages. One such approach is to “make a smaller batch,” with the amount produced equal to what can be sold at the higher price. If this is done, the manufacturer will employ fewer workers. It will also cut back on oil consumption, other raw materials, electricity consumption, and rent. The result will look like recession.

Thus, a rise in oil prices, such has happened since the early 2000s, can be expected to affect feedback loops for countries that use very much oil.

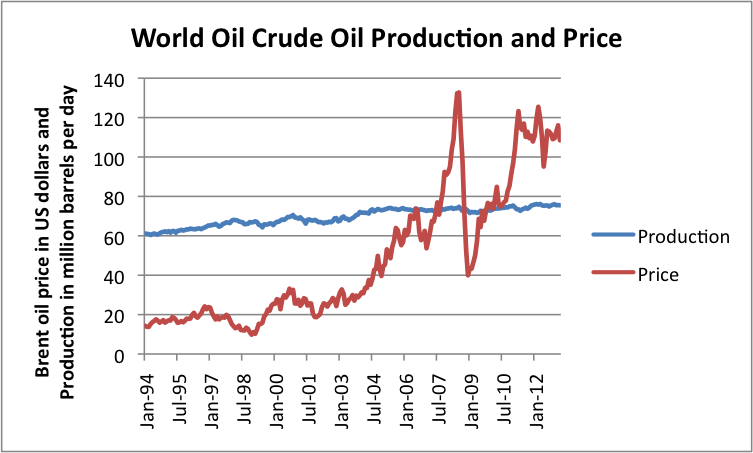

Figure 4. World crude oil production and Brent spot oil price, both based on EIA data.

The Positive-Feedback Loop

When can an economy grow? If an economy can grow in efficiency—that is, fewer and fewer people employed creating the basic requirements for life, then more of the population can be employed in providing discretionary services. In total, the wealth of the economy will grow. Historically, this has happened as increasing amounts of fossil fuel energy is added to supplement human energy.

If an economy can increase its debt, and that debt can finance equipment or infrastructure that will allow greater efficiency in producing basic services, this will also allow an economy to grow.

In economic analyses, increases in population are counted as part of economic growth. The problem with population growth is that it leads to more population per acre available for cultivation, and more population relative to external energy sources of all types. This sets up a competition: can enough external energy be added to maintain (and even increase) goods and services per capita?

Economies of scale are also important as producing positive feedback loops. Once an energy investment, such as a road, is made, it can be used for an increasingly large population, often without much additional cost. Businesses also find growth beneficial, since they can build a factory, and operate it more hours, with little additional cost.

The combination of all of these favorable feedbacks leads to the pattern of growth that economists seem to think always occurs.

What Can Go Wrong?

The big “oops” that takes place happens when we start hitting natural limits:

1. The cost of oil extraction goes up, because we pulled the easy-to-extract oil out first. This means that workers start having less discretionary income, rather than more, because they now needed to spend more on commuting to work and on food. Wages tend to stagnate or decline, for reasons described above. A larger percentage of the population needs to work in oil extraction, and more fossil fuels of various types must be used in oil extraction, leaving fewer workers and less energy supplies for other purposes.

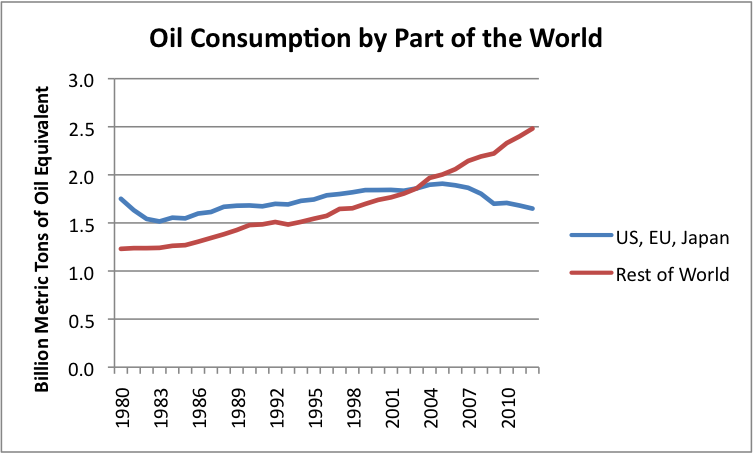

2. The economies of countries consuming large amounts of oil are disproportionately affected by rising prices, and oil consumption begins to drop in these countries, even though world oil consumption in total is still rising.

Figure 5. Oil consumption based on BP’s 2013 Statistical Review of World Energy.

3. Debt added to produce oil tends to produce fewer and fewer barrels of oil per dollar invested, as the cost of oil extraction rises. With fewer barrels of oil produced per dollar of investment, less goods are transported per dollar invested. If other energy products also rise in cost of extraction, or if the cost of making metals increases, we reach a situation where increasing debt, in general, starts adding a smaller and smaller quantity of goods per dollar of investment. (Substituting a different high-cost source of energy does not fix the situation.) Eventually, so little benefit is gained from additional debt that huge defaults occur. These huge defaults are likely to lead to higher interest rates and more layoffs.

Of course, during favorable feedback loops, the economic growth that comes with increasing energy consumption plays a major role in permitting debt to be paid back with interest. If energy consumption, in fact, starts contracting, this contraction will contribute to debt defaults.

4. As the economies of individual countries got richer and richer, the natural tendency was to add more government services. Pensions and health care were promised, based on what looked possible when the economy was growing rapidly. Now, the economy is not growing as rapidly, and increasing wage disparity is occurring. There is no way to tax the common people enough to pay for the benefits promised to people. People become very unhappy when told that the government cannot pay promised pension benefits. The tendency is toward increasing unhappiness with government status quo, perhaps even leading to new (cheaper) forms of government.

5. Because of energy limits, we find a need to conserve, but in the process discover that we are inadvertently hitting “diseconomies of lack of scale” instead of “economies of scale”. Instead of continually adding new jobs based on construction of new infrastructure, job opportunities for young people start to disappear. This adds to the dynamic of contraction, even if changes are planned.

6. All the time, natural forces are eroding the huge amount of infrastructure that has been built. Hurricanes and earthquakes cause destruction that must be fixed, if the current system is to be maintained. Lesser forces, such as freezing and thawing and roots of trees growing tend to ruin roads over time, and cause buildings to need repairs. While this has always happened, if the government is poorer, the cost becomes an increasing burden.

______

As a result of these influences, the natural feedback loop is now changing to contraction, instead of continually adding a positive increment. This is an unknown situation relative to what we are used to. There is no “reverse gear” on the economy.

We know that in the past, economies that have hit these adverse feedback loops have tended to collapse. The situation is indeed worrisome.

[i] Despite evolving in the direction of requiring external energy, there is still a possibility that a few individuals in particularly advantageous parts of the world might be able to “get along” without external energy. These individuals would probably live in areas where raw fish is available for food, and where predators are not particularly a problem. If these individuals are able to use stored energy in the form of modern knives, shoes, and clothing, such stored energy may take the place of other external energy that ancient people normally required.

The NSA just won their Congressional battle of Asculum. The House of Representatives voted down a proposal to strip them of their power to collect domestic data on American citizens without a warrant. The NSA won this clash of philosophies. The vote was 205 in favor of stripping them of their power, and 217 opposed.