Options are good, right?

Not necessarily.

Think about the last time you were in a grocery store. What kind of soap did you buy? What brand of cereal? Likely, it was one you’d had before — even if you aren’t completely satisfied with it.

Why is that? The reason is that there are just too many options for you to evaluate each one. So, your brain goes to the default.

You are not alone.

Consider this experiment:

“Shoppers at an upscale food market saw a display table with 24 varieties of gourmet jam. Those who sampled the spreads received a coupon for $1 off any jam. On another day, shoppers saw a similar table, except that only six varieties of the jam were on display. The large display attracted more interest than the small one. But when the time came to purchase, people who saw the large display were one-tenth as likely to buy as people who saw the small display.”

How can you compare 24 different types of jam? You can’t. That’s why the overwhelmed shoppers choose nothing. This is the Paradox of Choice in action.

Of course, this isn’t just about jam or groceries. The paradox of choice affects many areas of our life. BIG areas like our finances, our career, and even our productivity.

What happens when we have too many choices

The truth is, we have limited cognition and willpower and when we waste it processing minor decisions such as what type of jelly or soap to buy, this is what happens:

Even when we’re motivated to do big things — save money, find a new job, or finally finish that looming project — we don’t get it done.

But we’re not doomed to this pattern forever. By understanding how our brain works, we can take steps to reduce or even eliminate the effect of the paradox of choice when it really matters.

What to do about the paradox of choice

If you want to live a Rich Life, focus on the four or five big wins. Get a dream job. Negotiate your salary. Invest automatically so you don’t have to think about it. It’s not a decision.

This type of focus short-circuits the paradox of choice. If you do these four or five things, it doesn’t matter how many lattes you buy. It doesn’t matter if you buy a small Coke or a large Coke. You don’t have to worry about the never-ending stream of little questions because those micro decisions are irrelevant in the grand scheme of things.

In other words, you don’t have to worry about which type of spaghetti sauce is the most affordable per ounce because you’re earning enough not to care. Grab the one that looks most interesting and move on with your day.

Today, I want to show you how focusing on just three Big Wins can help you reduce the paradox of choice in your life.

Big Win #1: Eliminate the paradox of choice in your finances

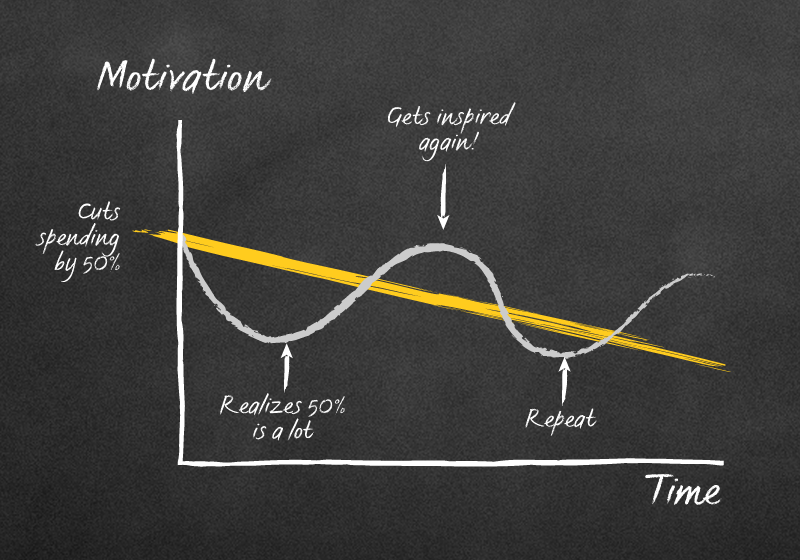

Think about the 50+ money decisions you have to make today: Should you save more? What should you cut down on? What about investing — real estate or stocks or index funds? Pay off debt? Did you send in that Comcast bill on time? Is it time to rebalance your portfolio?

Faced with an overwhelming number of choices, most people respond in the same way: They do nothing.

As I said in my NYT best-selling book, I Will Teach You To Be Rich:

The idea that — gasp! — there is too much information is a real and valid concern. “But Ramit,” you might say, “that flies in the face of all American culture! We need more information so we can make better decisions! People on TV say this all the time, so it must be true! Huzzah!” Sorry, nope. Look at the actual data and you’ll see that an abundance of information can lead to decision paralysis, a fancy way of saying that with too much information, we do nothing. Barry Schwartz writes about this in The Paradox of Choice: Why More is Less:

…As the number of mutual funds in a 401(k) plan offered to employees goes up, the likelihood that they will choose a fund — any fund — goes down. For every 10 funds added to the array of options, the rate of participation drops 2 percent. And for those who do invest, added fund options increase the chances that employees will invest in ultraconservative money-market funds.

For the exact step-by-step system to stop wasting mental energy on your money, I created the free Ultimate Guide to Personal Finance (including entire chapters from my NYT best-selling book).

No overwhelming choices here. Just the few tactics I’ve discovered and perfected for automating and optimizing your money. You can manage your money in less than an hour a month and start spending on things you love, guilt-free.

Big Win #2: Eliminate the paradox of choice in your career

The paradox of choice is a very real problem when looking for a job — and it starts early. Remember high school? What do I want to do? What electives should I take? What college should I go to?

At 15 (or younger) we’re told we’re deciding our fate for the rest of our lives. The trouble is our choices are nearly endless.

The decisions don’t stop there — What should I major in? What about a minor? Should I get my master’s or get a job? If I go back to school, how will I make money? Can I start my own business? What if I have multiple passions?

Our parents don’t get this. They’re like, “Go get a good job! They have really good benefits!” I once went home during college and a family friend was visiting. He worked at a very large consumer-packaged goods company and believed I was a lost soul who needed advice. Imagine my face when he gave me this advice:

“Ramit, you should join this company. You work here 30 years, you’ll have a MILLION DOLLARS when you retire!”

I looked at him in disbelief. A million? That’s it? 30 years from now?

See, we don’t WANT to work at the same company for 30 years. But at the same time, we’re stuck choosing among 2, 3, sometimes 10 different ideas. What if we choose the wrong one and close all the other doors?

In the video below, I explain how to get a handle on what you really want to do and narrow down your choices in a systematic way:

Big Win #3: Eliminate the paradox of choice and get more done

When we don’t focus on the Big Wins, our brain is constantly using our precious energy on all the little things we have to worry about — the dirty laundry, what to eat for dinner, when to call mom.

Even when we’re not aware, our brain is working on solving these minute problems — leaving less mental capacity for working on the big stuff. Which means we’re constantly making a choice like should I worry about the laundry or worry about my career. The result? Again, we do nothing.

When you look at masters of their craft, you’ll notice that they’ve always built routines for the ordinary parts of life, so they can focus on what they’re best at.

For example, Steve Jobs wore turtlenecks every day so he didn’t have to worry about clothes. And professional athletes stock their fridges with vegetables and lean protein so they don’t have to decide between cake and celery.

You can build microsystems in your daily life that eliminate the paradox of choice so we can focus on what really matters.

Watch this video to learn how to eliminate the effect of the paradox of choice so you can finally tackle your to-do list.

Bonus Win: How to eliminate worry with the Worry Vault technique

New sources of stress will always pop up in our day-to-day lives.

A few years ago, I stumbled across a simple technique for eliminating these little stressors and worries so I can focus on what really matters. No more choosing minute-by-minute or wasting my willpower and cognition.

You can learn it in this free bonus video: “Eliminate 99% of Your Worries With This One Simple Technique.”

In the video, you’ll learn:

- How to stop worrying about what you can’t control

- Simple ways you can clear your mind and sleep better every night.

- My “Worry Vault” technique — so you never have to stress about little things again.

I bet you can find at least 3 things you could put in your “Worry Vault” today and never stress about them again.

Enter your email for instant access to the free video: Eliminate 99% of Your Worries With This One Simple Technique.”

Name:

Email:

100% privacy. No games, no B.S., no spam.

How to overcome the paradox of choice is a post from: I Will Teach You To Be Rich.

This rate cut won’t make a difference immediately but it will require them to cut rates.

This rate cut won’t make a difference immediately but it will require them to cut rates.