Not all the money advice you read necessarily applies to your personality—different types of people need to utilize different strategies. Whether you're too much of a perfectionist, a procrastinator, or a stockpiler of needless paperwork, here are four strategies to deal with your money persona.

This post originally appeared on LearnVest.

Chances are that organizing your finances probably doesn't rank at the top of your list of awesome ways to spend an afternoon. But this to-do is just as important—if not more so—than cleaning out your closet or tidying up the garage. And, at some point, we all just need to buckle down and tackle it.

But successfully getting your money in order has as much to do with who you are as what you're trying to do.

Translation: What works for someone else might not for you, and if you're trying to conform to a system that's not in tune with your personality, you're going to have a harder time staying on track.

That's why we decided to delve into the psychology behind the four most common money personas—and then asked finance and organization pros to offer advice on how each type can hone their strengths and weaknesses to get their financial life in better, well, order.

So whether you're a stockpiler or a perfectionist, balancing your budget and marshalling your money life just got a little easier. Trust us.

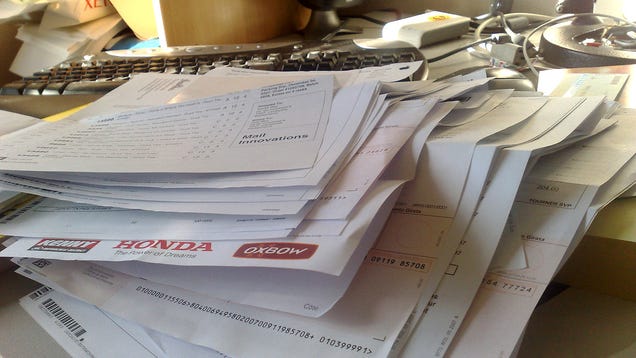

Personality Type #1: The Stockpiler

If computers suddenly wiped out all of the world's digitally-stored financial data, Stockpilers would be well prepared for the paperless Armageddon. They keep piles of receipts for months-old purchases, stacks of bank statements dating back to the Clinton administration, and utility bills for homes they no longer live in.

If this sounds like you, it's time to get your hoarding tendencies under control.

"Hoarding often stems from a lack of education on what you should keep versus toss," explains Jennifer Ford Berry, a life organization expert and author of "Organize Now!" "You're terrified that you might mistakenly throw out a document that you need, so you end up keeping everything just to be on the safe side."

On the one hand, kudos to you for being so vigilant about your personal financial information. However, in the long run, having a backlog of paperwork only makes life more difficult because when you finally do need to track down something specific, you'll have to sort through hundreds of files.

"Plus, if something should ever happen to you, it will be difficult for your heirs to sift through a mountain of disorganized bills and statements," Berry adds. "They might miss important information."

How Stockpilers Can Get Better Organized

Stockpilers can benefit from learning—and abiding by—some rules of thumb for how long to hold onto paperwork.

According to Russell Wild, a registered investment adviser and co-author of "One Year to an Organized Financial Life," you want to keep the following for tax purposes: records for any assets you own (home, stocks, etc.); pay stubs; financial statements for investment accounts, like retirement plans, mutual funds and college savings plans; bank statements; and any credit card statements that have a record of tax-deductible items you purchased.

The I.R.S. has three years to audit you once you file your taxes, so you should hold onto tax records and backup for at least that long. However, there are some exceptions to the rule: If you've under-reported income by 25% or more, the IRS can go back six years. If you claim a loss for bad debt or worthless securities, they can request records as far back as seven years. But if fraud is suspected, then the IRS has no time limits. So consider keeping up to seven years' worth of paperwork—or indefinitely if you want be extra careful.

Here's what you can safely shred: credit card statements that are more than a month old and don't include deductible purchases; utility and phone bills that are more than a month old (unless they're deductible); receipts and ATM deposit slips after you've reconciled them with your credit card and bank statements; and any paperwork that duplicates files that you've already securely stored online or in an external database.

And if the thought of getting rid of all that paperwork makes you feel anxious, remember the 80/20 rule. "80% of the paper we keep we don't need and never look at again," Berry says. "So let companies do their job to retain your records. If you need certain information, you can look it up online or call them."

Personality Type #2: The Procrastinator

Procrastinators totally intend to keep their financial life organized… just as soon as they walk the dog or drive the kids to soccer or watch the missed episode of their favorite show on the DVR.

"This personality tends to like the drama of the last minute," says "Zen organizer" Regina Leeds, co-author of "One Year to an Organized Financial Life." "You usually get things done in the end, but at a high cost to mind, body and soul."

Not to mention your wallet.

After all, putting off your finances can lead to late payments (and subsequently a plummeting credit score), stress during tax time and missed investment opportunities—all consequences that Wild often sees.

"For example, many of my clients have had cash in a money market account that pays close to 0% interest, minus the inflation rate," he explains. "You're losing 2% to 3% a year on your balance—and that's a high rate to pay for procrastination."

How Procrastinators Can Get Better Organized

A smart strategy for dawdlers is to reframe how they think about getting organized by transforming it from a task you dread into a task that's—believe it or not—pleasurable or at least tolerable.

"Don't sit in a hard chair in the corner to go through your bills," Berry says. Instead, light a candle, put on music and pour yourself a glass of wine. It can also help to use organizational tools that are more aesthetically pleasing, like colorful folders or a stylish planner. "If you love something, you'll be more likely to use it," she adds.

Berry also suggests treating yourself to a reward once you complete a money organization project. For example, after you've balanced your budget and paid your bills for the month, go out to dinner or indulge in a movie. Ending on a positive note will make you more apt to stay on the ball in the future and avoid problematic procrastination .

Personality Type #3: The Perfectionist

Type A and detail-oriented, perfectionists never cut corners. So when it comes to organizing their finances, they want to get everything just right, from alphabetized file folders to color-coded storage bins.

If you're a perfectionist, you're motivated to put things in order and keep a list of what financial tasks you need to do—but your control-freak tendencies can also shoot you in the foot.

"If you don't have time to do everything flawlessly, you might keep putting off the task and ultimately do nothing," explains Berry. "Plus, trying to complete it all perfectly can cause you needless stress."

For instance, you may waste precious energy printing out neat labels for your file cabinet, instead of channeling your efforts toward, say, figuring out how to rebalance your portfolio based on your last brokerage statement. Additionally, perfectionists tend to maintain an overly complicated financial tracking system, which can lead to spending a half-hour trying to find a misplaced receipt.

How Perfectionists Can Get Better Organized

When over-analysis leads to paralysis, keep it simple and just do it already!

"My motto is 'good enough is the new perfect.' Life is too busy to become the Martha Stewart of financial organization," Berry says. "As long as you know where your money is going, and you aren't paying late fees, you're doing a fine job."

And since perfectionists tend to be goal-oriented, setting a due date on a calendar to complete a financial task can also be an effective way to get yourself to finally tackle a given money to-do. "If you don't create firm boundaries," notes Leeds, "you will keep pushing back the deadline."

Personality Type #4: The Avoider

To say that dealing with financial issues is not on the avoider's radar is a huge understatement—it's not even in their stratosphere.

Unlike procrastinators, who mostly just need a motivational push toward better time management, avoiders wear money blinders that often lead to bigger issues, like consistently making late payments or racking up debt.

"You need to realize the consequences of avoidance," Wild says. "It's more pleasant in the short run not to think about finances, but it could lead to much greater anxiety down the line."

How Avoiders Can Get Better Organized

Begin taking control by figuring out the root of your evasion, which can give you the power to change your situation, says Leeds. "Your avoidance may have been shaped by your upbringing," she explains. "Perhaps you grew up in a chaotic household where money wasn't managed well."

Or your aversion could be fear-based. "You don't want to look at your balance and face all the bills that are due," Berry explains. "Organizing your finances might also feel overwhelming if you aren't sure where to start and how to do it correctly." As a result, you do nothing.

So once you've pinpointed the root cause of your avoidance tendencies, develop a systemized approach to get your finances in order. "If you have a routine, you'll be less likely to circumvent the task," Berry says.

For example, try paying your bills the same way each month—in the same place, at the same time. You can set a repeating alarm on your phone for a certain day and hour (say, 8 P.M. on the 15th), and have everything you need—your computer, checks, file folders, stamps and envelopes—at your fingertips in one central location.

You may also want to enlist someone to help keep you accountable. Maybe you plan to tackle the bills jointly with your spouse, or ask a friend to text you the next day to make sure you followed through on the task. You may even want to hire a professional organizer.

Finally, since avoiders tend to focus on when a chore is going to end, set a visual timer—such as on your phone—so that you can watch the minutes ticking away.

"Aim for a short period of time, just 15 or 30 minutes," Berry says. The hardest part is getting started in the first place, but once you're in the trenches, chances are you'll finish—even if it takes longer than your timer allots.

Clear the Financial Clutter: 4 Ways to Organize Your Money Based on Your Personality | LearnVest

LearnVest Planning Services is a registered investment adviser and subsidiary of LearnVest, Inc. that provides financial plans for its clients. LearnVest Planning Services and any third-parties listed, discussed, identified or otherwise appearing herein are separate and unaffiliated and are not responsible for each other's products, services or policies.

Image adapted from HomeStudio (Shutterstock). Additional photos by Joel Bez, Hannah Sheffield, Images Money, and Mitch Altman (Flickr).

Want to see your work on Lifehacker? Email Andy.

{kind=link}